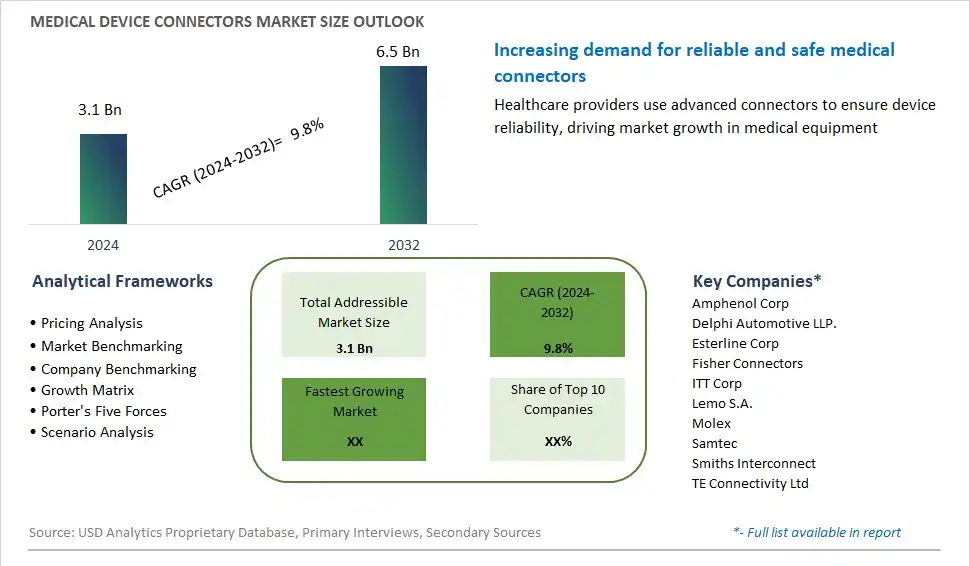

Global Medical Device Connectors Market Size is valued at $3.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 9.8% to reach $6.5 Billion by 2032.

The global Medical Device Connectors Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Radio Frequency Connectors, Magnetic Medical Connectors, Embedded Electronics Connectors, Others), By Application (Diagnostic Imaging, Patient Monitoring, Cardiology, Electrosurgical, Dental Devices, Others), By End-User (Hospitals, Diagnostic Laboratories and Imaging Centers, Ambulatory Surgical Centers)

An Introduction to Medical Device Connectors Market

The medical device connectors market in 2024 is witnessing robust growth, driven by the increasing demand for advanced connectivity solutions in the healthcare industry. Medical device connectors, which facilitate the connection and communication between medical devices, play a crucial role in patient monitoring, diagnosis, and treatment. The market benefits from the rising adoption of digital health technologies, such as wearable devices, remote patient monitoring systems, and medical imaging equipment. Innovations in connector design, including miniaturization, wireless connectivity, and compatibility with various medical devices, have improved interoperability and data exchange in healthcare settings. Additionally, the emphasis on patient-centric care and healthcare efficiency supports the adoption of advanced connector solutions. As healthcare systems continue to integrate digital technologies and improve patient outcomes, the demand for medical device connectors is set to grow robustly.

Medical Device Connectors Competitive Landscape

The market report analyses the leading companies in the industry including Amphenol Corp, Delphi Automotive LLP., Esterline Corp, Fisher Connectors, ITT Corp, Lemo S.A., Molex, Samtec, Smiths Interconnect, TE Connectivity Ltd, and Others.

Medical Device Connectors Market Dynamics

Medical Device Connectors Market Trend: Miniaturization and Connectivity in Medical Devices

A prominent trend in the medical device connectors market is the increasing demand for miniaturization and connectivity in medical devices. With advancements in medical technology and the rise of digital healthcare solutions, there's a growing need for smaller, lighter, and more versatile connectors that can seamlessly integrate with a wide range of medical devices and systems. This trend is driven by factors such as the miniaturization of medical devices for minimally invasive procedures, the adoption of wireless and wearable medical devices for remote patient monitoring, and the emphasis on interoperability and data exchange in healthcare ecosystems. Medical device connectors equipped with advanced features such as high-speed data transmission, secure communication protocols, and compatibility with electronic health records (EHR) systems enable healthcare providers to improve patient care, streamline workflows, and enhance clinical outcomes. As the healthcare industry continues to embrace digital transformation and innovation, the demand for medical device connectors that facilitate connectivity and interoperability is expected to grow, driving market expansion and technological advancements.

Market Driver: Increasing Adoption of Telemedicine and Remote Monitoring

An essential driver fueling the medical device connectors market is the increasing adoption of telemedicine and remote monitoring solutions in healthcare delivery. With the rise of telehealth platforms, virtual consultations, and remote patient monitoring technologies, there's a growing need for medical devices and sensors that can transmit patient data securely and reliably to healthcare providers and electronic medical records (EMR) systems. This driver is reinforced by factors such as the aging population, the prevalence of chronic diseases, and the need to reduce healthcare costs and improve access to care, especially in remote or underserved areas. Medical device connectors play a crucial role in facilitating the connectivity and interoperability of medical devices used in telemedicine and remote monitoring applications, enabling real-time data collection, analysis, and decision-making by healthcare professionals. As telemedicine and remote monitoring become integral components of healthcare delivery, the demand for medical device connectors that support these technologies is expected to increase, creating opportunities for market growth and innovation.

Market Opportunity: Integration of Smart Features and Cybersecurity Solutions

A significant opportunity within the medical device connectors market lies in the integration of smart features and cybersecurity solutions to address emerging challenges and enhance patient safety and data security. There's an opportunity to develop medical device connectors equipped with intelligent sensors, embedded diagnostics, and predictive maintenance capabilities to monitor device performance, detect anomalies, and proactively address issues before they impact patient care. Additionally, there's an opportunity to enhance cybersecurity measures in medical device connectors to protect sensitive patient data and mitigate the risk of cyber threats and data breaches. This includes implementing encryption protocols, authentication mechanisms, and secure data transfer protocols to ensure the confidentiality, integrity, and availability of healthcare information. By integrating smart features and cybersecurity solutions into medical device connectors, manufacturers can enhance the reliability, safety, and security of medical devices and systems, meet regulatory requirements, and address the evolving needs of healthcare providers and patients in an increasingly connected healthcare environment. As healthcare organizations prioritize patient safety and data security, the opportunity to develop innovative and secure medical device connectors presents significant potential for market growth and differentiation.

Medical Device Connectors Market Share Analysis: Radio Frequency Connectors held the dominant market share in 2024

Radio Frequency (RF) connectors represent the largest segment in the medical device connectors market. This prominence is due to their critical role in ensuring reliable and high-speed data transmission, which is essential in modern medical devices and systems. RF connectors are extensively used in imaging systems such as MRI and CT scanners, where precise and rapid data transfer is crucial for accurate diagnostics. Additionally, the growing adoption of telemedicine and remote patient monitoring devices, which rely on RF technology for wireless communication, has significantly boosted the demand for these connectors. Their ability to maintain signal integrity over long distances and in various environmental conditions further enhances their appeal. As healthcare facilities continue to integrate advanced diagnostic and monitoring equipment that necessitates robust and efficient connectivity solutions, the RF connectors segment is expected to maintain its leading position and drive substantial market growth.

Medical Device Connectors Market Share Analysis: Patient Monitoring market is poised to register the fastest growth rae over the forecast period to 2032

The patient monitoring segment is the fastest growing in the medical device connectors market. This rapid growth is driven by the increasing adoption of continuous and real-time monitoring systems across healthcare settings, fueled by the rising prevalence of chronic diseases and the aging global population. Patient monitoring devices, which include vital signs monitors, glucose monitors, and remote monitoring systems, require reliable and secure connectors to ensure accurate data transmission and device functionality. The surge in telehealth and home healthcare services, accelerated by the COVID-19 pandemic, has further amplified the demand for advanced patient monitoring solutions. These systems necessitate connectors that offer durability, ease of use, and resistance to environmental factors. As healthcare providers prioritize early diagnosis and proactive patient management, the patient monitoring segment is set to experience substantial growth, driven by technological advancements and the need for efficient healthcare delivery.

Medical Device Connectors Market Share Analysis: Hospitals held the dominant market share in 2024

Hospitals represent the largest segment in the medical device connectors market. This dominance is primarily due to the high volume of medical procedures and the extensive range of diagnostic and therapeutic equipment utilized in hospital settings. Hospitals require a vast array of medical devices, from imaging systems and patient monitors to surgical instruments and infusion pumps, all of which rely on reliable connectors for optimal performance and patient safety. The continuous need for device interoperability and efficient data management in hospitals drives the demand for advanced and robust medical connectors. Additionally, hospitals often have larger budgets for medical technology investments, allowing them to adopt the latest and most efficient devices and connectors. As hospitals strive to improve patient outcomes, enhance operational efficiency, and comply with stringent regulatory standards, the demand for high-quality medical device connectors remains substantial, ensuring this segment's leading position in the market.

Medical Device Connectors Market Segmentation

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Medical Device Connectors Companies Profiled in the Study

Amphenol Corp

Delphi Automotive LLP.

Esterline Corp

Fisher Connectors

ITT Corp

Lemo S.A.

Molex

Samtec

Smiths Interconnect

TE Connectivity Ltd

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Medical Device Connectors Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Medical Device Connectors Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Medical Device Connectors Market Share by Company, 2023

4.1.2. Product Offerings of Leading Medical Device Connectors Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Medical Device Connectors Market Drivers

6.2. Medical Device Connectors Market Challenges

6.6. Medical Device Connectors Market Opportunities

6.4. Medical Device Connectors Market Trends

Chapter 7. Global Medical Device Connectors Market Outlook Trends

7.1. Global Medical Device Connectors Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Medical Device Connectors Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Medical Device Connectors Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Chapter 8. Global Medical Device Connectors Regional Analysis and Outlook

8.1. Global Medical Device Connectors Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Medical Device Connectors Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Medical Device Connectors Regional Analysis and Outlook

8.2.2. Canada Medical Device Connectors Regional Analysis and Outlook

8.2.3. Mexico Medical Device Connectors Regional Analysis and Outlook

8.3. Europe Medical Device Connectors Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Medical Device Connectors Regional Analysis and Outlook

8.3.2. France Medical Device Connectors Regional Analysis and Outlook

8.3.3. United Kingdom Medical Device Connectors Regional Analysis and Outlook

8.3.4. Spain Medical Device Connectors Regional Analysis and Outlook

8.3.5. Italy Medical Device Connectors Regional Analysis and Outlook

8.3.6. Russia Medical Device Connectors Regional Analysis and Outlook

8.3.7. Rest of Europe Medical Device Connectors Regional Analysis and Outlook

8.4. Asia Pacific Medical Device Connectors Revenue (USD Million) by Country (2021-2032)

8.4.1. China Medical Device Connectors Regional Analysis and Outlook

8.4.2. Japan Medical Device Connectors Regional Analysis and Outlook

8.4.3. India Medical Device Connectors Regional Analysis and Outlook

8.4.4. South Korea Medical Device Connectors Regional Analysis and Outlook

8.4.5. Australia Medical Device Connectors Regional Analysis and Outlook

8.4.6. South East Asia Medical Device Connectors Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Medical Device Connectors Regional Analysis and Outlook

8.5. South America Medical Device Connectors Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Medical Device Connectors Regional Analysis and Outlook

8.5.2. Argentina Medical Device Connectors Regional Analysis and Outlook

8.5.3. Rest of South America Medical Device Connectors Regional Analysis and Outlook

8.6. Middle East and Africa Medical Device Connectors Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Medical Device Connectors Regional Analysis and Outlook

8.6.2. Africa Medical Device Connectors Regional Analysis and Outlook

Chapter 9. North America Medical Device Connectors Analysis and Outlook

9.1. North America Medical Device Connectors Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Medical Device Connectors Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Medical Device Connectors Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Medical Device Connectors Revenue (USD Million) by Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Chapter 10. Europe Medical Device Connectors Analysis and Outlook

10.1. Europe Medical Device Connectors Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Medical Device Connectors Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Medical Device Connectors Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Medical Device Connectors Revenue (USD Million) by Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Chapter 11. Asia Pacific Medical Device Connectors Analysis and Outlook

11.1. Asia Pacific Medical Device Connectors Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Medical Device Connectors Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Medical Device Connectors Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Medical Device Connectors Revenue (USD Million) by Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Chapter 12. South America Medical Device Connectors Analysis and Outlook

12.1. South America Medical Device Connectors Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Medical Device Connectors Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Medical Device Connectors Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Medical Device Connectors Revenue (USD Million) by Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Chapter 13. Middle East and Africa Medical Device Connectors Analysis and Outlook

13.1. Middle East and Africa Medical Device Connectors Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Medical Device Connectors Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Medical Device Connectors Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Medical Device Connectors Revenue (USD Million) by Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Chapter 14. Medical Device Connectors Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Amphenol Corp

Delphi Automotive LLP.

Esterline Corp

Fisher Connectors

ITT Corp

Lemo S.A.

Molex

Samtec

Smiths Interconnect

TE Connectivity Ltd

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Medical Device Connectors Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Medical Device Connectors Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Medical Device Connectors Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Medical Device Connectors Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Medical Device Connectors Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Medical Device Connectors Market Share (%) By Regions (2021-2032)

Table 12 North America Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Table 15 South America Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Table 17 North America Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Table 18 North America Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Table 19 North America Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Table 26 South America Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Table 27 South America Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Table 28 South America Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Medical Device Connectors Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Medical Device Connectors Market Share (%) By Regions (2023)

Figure 6. North America Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 12. France Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 12. China Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 14. India Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Medical Device Connectors Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Medical Device Connectors Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Medical Device Connectors Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Medical Device Connectors Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Medical Device Connectors Revenue (USD Million) By Product (2021-2032)

By Product

Radio Frequency Connectors

Magnetic Medical Connectors

Embedded Electronics Connectors

Others

By Application

Diagnostic Imaging

Patient Monitoring

Cardiology

Electrosurgical

Dental Devices

Others

By End-User

Hospitals

Diagnostic Laboratories and Imaging Centers

Ambulatory Surgical Centers

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)