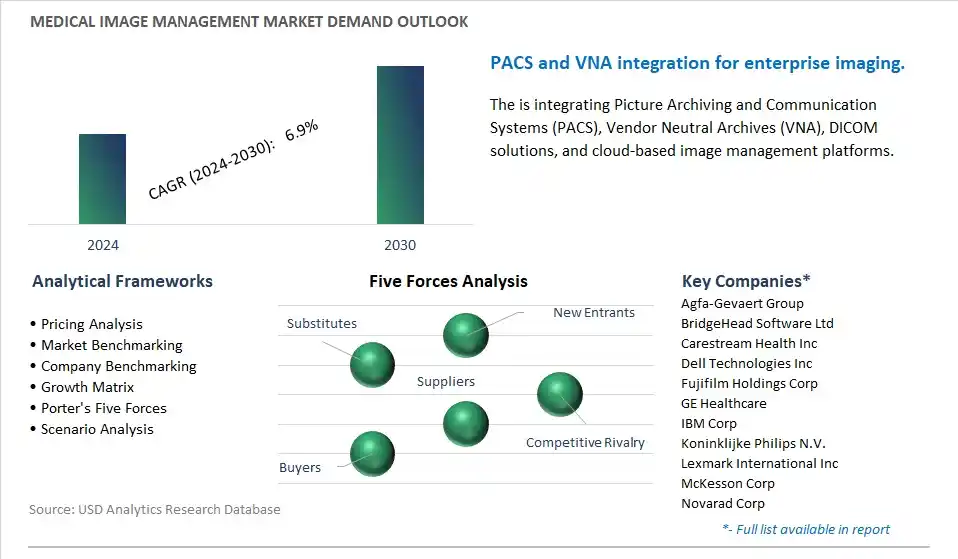

Medical Image Management Market is estimated to increase at a Compounded Annual Growth Rate of 6.9% CAGR over the forecast period from 2024 to 2030

The Medical Image Management Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By System (Vendor Neutral Archive, Picture Archiving and Communications System (PACS), Others), By End-User (Hospitals, Diagnostic Centers, Ambulatory Surgery Centers).

An Introduction to Medical Image Management Market in 2024

Medical image management encompasses the storage, retrieval, distribution, and analysis of medical images generated through various imaging modalities, such as radiography, computed tomography (CT), magnetic resonance imaging (MRI), ultrasound, and nuclear medicine. In 2024, medical image management systems continue to play a crucial role in healthcare delivery by facilitating efficient access to diagnostic images, supporting clinical decision-making, and enabling collaboration among healthcare providers. These systems include picture archiving and communication systems (PACS), vendor-neutral archives (VNA), and enterprise imaging platforms, which consolidate and centralize medical image data from disparate sources, enabling seamless integration with electronic health records (EHR) and clinical workflows. Advanced features such as cloud-based storage, scalable infrastructure, and artificial intelligence (AI) algorithms for image analysis enhance the efficiency, scalability, and interoperability of medical image management systems, enabling healthcare organizations to meet the growing demand for diagnostic imaging services, improve diagnostic accuracy, and enhance patient care outcomes. Moreover, interoperability standards such as DICOM (Digital Imaging and Communications in Medicine) and HL7 (Health Level Seven International) facilitate seamless integration with other healthcare IT systems, telemedicine platforms, and mobile devices, enabling secure access to medical images anytime, anywhere. As the volume and complexity of medical imaging data continue to increase, medical image management systems play a pivotal role in optimizing clinical workflows, reducing diagnostic errors, and empowering healthcare providers with timely access to actionable insights for improved patient outcomes.

Market Trend: Adoption of Cloud-Based Solutions and Artificial Intelligence

A prominent trend in the medical image management market is the increasing adoption of cloud-based solutions and artificial intelligence (AI) technologies. Healthcare organizations are shifting towards cloud-based image management platforms to overcome the limitations of traditional, on-premises systems, such as scalability, accessibility, and data security. Cloud-based solutions offer benefits such as remote access to medical images, seamless collaboration among healthcare professionals, and cost-effective storage and archiving. Additionally, the integration of AI algorithms into image management platforms enables automated image analysis, diagnosis assistance, and workflow optimization, enhancing the efficiency and accuracy of medical imaging processes. As healthcare providers seek to leverage the power of cloud computing and AI to streamline image management workflows, improve clinical decision-making, and enhance patient care, the demand for advanced image management solutions is expected to grow, driving market expansion and innovation in the sector.

Market Driver: Growing Volume and Complexity of Medical Imaging Data

A key driver fueling the demand for medical image management solutions is the growing volume and complexity of medical imaging data. Medical imaging modalities, such as X-ray, MRI, CT, ultrasound, and PET-CT, generate vast amounts of digital images that need to be stored, managed, and accessed efficiently for diagnostic and treatment purposes. The increasing adoption of advanced imaging techniques, such as 3D imaging, functional imaging, and molecular imaging, further contributes to the complexity of medical imaging data, requiring sophisticated management solutions capable of handling diverse image formats and large data sets. Moreover, regulatory requirements for image retention, data security, and interoperability impose additional challenges on healthcare organizations, driving the need for robust image management platforms that ensure compliance, accessibility, and data integrity. As the demand for medical imaging services continues to rise with aging populations, advances in medical technology, and the prevalence of chronic diseases, the market for image management solutions is expected to expand to meet the growing needs of healthcare providers and imaging centers.

Market Opportunity: Integration with Electronic Health Records and Telemedicine

A significant opportunity for the medical image management market lies in the integration with electronic health records (EHR) and telemedicine platforms. Seamless integration between image management systems and EHR platforms enables healthcare providers to access patient images directly within the electronic medical record, facilitating comprehensive patient care, clinical decision-making, and care coordination. Moreover, integration with telemedicine platforms enables remote access to medical images, enabling virtual consultations, image sharing, and second opinions among healthcare professionals and patients. By developing interoperable image management solutions that seamlessly integrate with EHR and telemedicine systems, vendors can enhance workflow efficiency, data accessibility, and patient engagement, driving market differentiation and adoption in the rapidly evolving healthcare landscape. Additionally, leveraging emerging technologies such as blockchain for secure image exchange and interoperability can further enhance the value proposition of integrated image management solutions, presenting opportunities to address evolving healthcare needs and challenges in the digital age.

Medical Image Management Market Share Analysis: Vendor Neutral Archive (VNA) for Diagnostic Centers is the fastest growing segment over the forecast period to 2030

Among the segments listed, the Vendor Neutral Archive (VNA) for diagnostic centers is experiencing rapid growth in the medical image management market. This growth is primarily driven by the increasing adoption of digital imaging technologies, such as magnetic resonance imaging (MRI), computed tomography (CT), and digital radiography (DR), across diagnostic centers. VNAs offer a centralized repository for storing, managing, and sharing medical images and patient data, regardless of the imaging modality or vendor-specific formats. They provide interoperability and scalability, allowing diagnostic centers to efficiently manage large volumes of medical images while ensuring data integrity and compliance with regulatory requirements. Additionally, VNAs facilitate seamless integration with existing Picture Archiving and Communication Systems (PACS) and electronic health record (EHR) systems, enabling diagnostic centers to streamline workflow processes, enhance diagnostic accuracy, and improve patient care outcomes. The growing emphasis on digitization, data interoperability, and healthcare efficiency is driving the rapid adoption of VNA solutions among diagnostic centers.

Medical Image Management Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossAgfa-Gevaert Group, BridgeHead Software Ltd, Carestream Health Inc, Dell Technologies Inc, Fujifilm Holdings Corp, GE Healthcare, IBM Corp, Koninklijke Philips N.V., Lexmark International Inc, McKesson Corp, Novarad Corp, Siemens Healthineers AG

Medical Image Management Market Segmentation

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Medical Image Management Market Companies

Agfa-Gevaert Group

BridgeHead Software Ltd

Carestream Health Inc

Dell Technologies Inc

Fujifilm Holdings Corp

GE Healthcare

IBM Corp

Koninklijke Philips N.V.

Lexmark International Inc

McKesson Corp

Novarad Corp

Siemens Healthineers AG

Reasons to Buy the Medical Image Management Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Medical Image Management Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Medical Image Management Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Medical Image Management Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Medical Image Management Market Size Outlook, $ Million, 2021 to 2030

3.2 Medical Image Management Market Outlook by Type, $ Million, 2021 to 2030

3.3 Medical Image Management Market Outlook by Product, $ Million, 2021 to 2030

3.4 Medical Image Management Market Outlook by Application, $ Million, 2021 to 2030

3.5 Medical Image Management Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Medical Image Management Industry

4.2 Key Market Trends in Medical Image Management Industry

4.3 Potential Opportunities in Medical Image Management Industry

4.4 Key Challenges in Medical Image Management Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Medical Image Management Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Medical Image Management Market Outlook by Segments

7.1 Medical Image Management Market Outlook by Segments, $ Million, 2021- 2030

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

8 North America Medical Image Management Market Analysis and Outlook To 2030

8.1 Introduction to North America Medical Image Management Markets in 2024

8.2 North America Medical Image Management Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Medical Image Management Market size Outlook by Segments, 2021-2030

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

9 Europe Medical Image Management Market Analysis and Outlook To 2030

9.1 Introduction to Europe Medical Image Management Markets in 2024

9.2 Europe Medical Image Management Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Medical Image Management Market Size Outlook by Segments, 2021-2030

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

10 Asia Pacific Medical Image Management Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Medical Image Management Markets in 2024

10.2 Asia Pacific Medical Image Management Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Medical Image Management Market size Outlook by Segments, 2021-2030

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

11 South America Medical Image Management Market Analysis and Outlook To 2030

11.1 Introduction to South America Medical Image Management Markets in 2024

11.2 South America Medical Image Management Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Medical Image Management Market size Outlook by Segments, 2021-2030

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

12 Middle East and Africa Medical Image Management Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Medical Image Management Markets in 2024

12.2 Middle East and Africa Medical Image Management Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Medical Image Management Market size Outlook by Segments, 2021-2030

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Agfa-Gevaert Group

BridgeHead Software Ltd

Carestream Health Inc

Dell Technologies Inc

Fujifilm Holdings Corp

GE Healthcare

IBM Corp

Koninklijke Philips N.V.

Lexmark International Inc

McKesson Corp

Novarad Corp

Siemens Healthineers AG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By System

Vendor Neutral Archive

Picture Archiving and Communications System (PACS)

Others

By End-User

Hospitals

Diagnostic Centers

Ambulatory Surgery Centers

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)