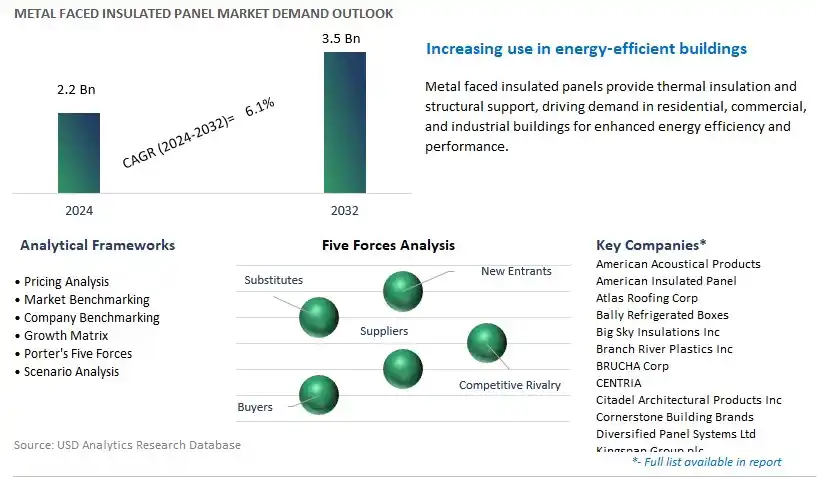

Global Metal faced Insulated Panel Market Size is valued at $2.2 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.1% to reach $3.5 Billion by 2032.

The global Metal faced Insulated Panel Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Core Material (Blowing Agents, Polyurethane (PU), Polyisocyanurate (PIR), Mineral Wool, Polystyrene (PS), Phenolic (PF)), By Usage (Internal, External), By End-User (Residential, Commercial, Industrial, Institutional, Infrastructure, Others).

An Introduction to Metal faced Insulated Panel Market in 2024

Metal-faced insulated panels are composite building materials used in walls, roofs, and facades of residential, commercial, and industrial structures to provide thermal insulation, structural support, and aesthetic appeal. In 2024, the market for metal-faced insulated panels is experiencing robust growth, driven by factors such as energy efficiency regulations, green building certifications, and demand for sustainable construction materials. Metal-faced insulated panels typically consist of an insulating core material such as polyurethane, polyisocyanurate, or mineral wool sandwiched between two metal facings, usually steel or aluminum. These panels offer superior thermal performance, fire resistance, and durability compared to traditional construction methods, reducing energy consumption, operational costs, and environmental impact over the life cycle of buildings. With advancements in panel manufacturing technologies and design innovations, manufacturers are producing metal-faced insulated panels with customizable thicknesses, profiles, and finishes to meet the diverse requirements of architects, builders, and building owners. Further, the adoption of prefabricated panel systems and off-site construction methods is accelerating construction timelines, reducing labor costs, and minimizing waste generation on construction sites. As the construction industry embraces sustainable building practices and seeks cost-effective solutions for energy-efficient buildings, the market for metal-faced insulated panels is poised for d expansion, offering versatile and sustainable solutions for modern building envelopes.

Metal faced Insulated Panel Market Competitive Landscape

The market report analyses the leading companies in the industry including American Acoustical Products, American Insulated Panel, Atlas Roofing Corp, Bally Refrigerated Boxes, Big Sky Insulations Inc, Branch River Plastics Inc, BRUCHA Corp, CENTRIA, Citadel Architectural Products Inc, Cornerstone Building Brands, Diversified Panel Systems Ltd, Kingspan Group plc, Metl-Span, Nucor Corp, Nudo Products, Inc., Owens Corning, Portafab Corp, Premier Building Systems Inc, and others.

Metal faced Insulated Panel Market Dynamics

Market Trend: Growing Demand for Energy-efficient Building Solutions

A significant trend in the metal-faced insulated panel market is the growing demand for energy-efficient building solutions. Metal-faced insulated panels offer excellent thermal insulation properties, helping to reduce heat transfer and energy consumption in commercial, industrial, and residential buildings. With increasing emphasis on sustainability and energy efficiency, building owners and developers are seeking cost-effective solutions to meet stringent energy codes and regulations. Metal-faced insulated panels provide an efficient way to improve building envelope performance, enhance indoor comfort, and reduce heating and cooling costs, making them increasingly popular in construction projects worldwide. This trend is expected to continue as the construction industry prioritizes sustainable building practices and energy conservation, driving the adoption of metal-faced insulated panels as a preferred choice for building envelope systems.

Market Driver: Construction Industry Growth and Urbanization

The primary driver behind the growth of the metal-faced insulated panel market is the growth of the construction industry and urbanization. As urban populations continue to rise, there is a growing demand for new infrastructure, commercial buildings, residential complexes, and industrial facilities. Metal-faced insulated panels offer a versatile and efficient solution for construction projects, providing benefits such as speed of installation, lightweight construction, and design flexibility. The demand for metal-faced insulated panels is driven by the need for cost-effective, durable, and high-performance building materials that can meet the requirements of modern construction projects. With ongoing urbanization and infrastructure development initiatives worldwide, the market for metal-faced insulated panels is poised for significant growth, creating opportunities for manufacturers, contractors, and suppliers.

Market Opportunity: Innovation in Sustainable and Customized Panel Solutions

An opportunity for the metal-faced insulated panel market lies in innovation in sustainable and customized panel solutions. With increasing emphasis on environmental sustainability and building performance, there is a demand for metal-faced insulated panels that offer improved energy efficiency, recyclability, and sustainability credentials. Manufacturers can capitalize on this opportunity by investing in research and development initiatives to develop next-generation panel solutions with enhanced thermal performance, reduced environmental impact, and innovative features such as integrated renewable energy systems or smart building technologies. Additionally, there is an opportunity to offer customized panel solutions tailored to specific project requirements, such as large-scale commercial developments, cold storage facilities, or high-rise residential buildings. By offering innovative and sustainable panel solutions that address the evolving needs of the construction industry, manufacturers can differentiate their products, capture market share, and drive growth in the metal-faced insulated panel market. Expanding into sustainable and customized panel solutions presents an opportunity for the market to meet emerging market demands, enhance competitiveness, and contribute to a more sustainable built environment.

Metal faced Insulated Panel Market Share Analysis: Polyurethane (PU) Core Material segment generated the highest revenue in 2024

Within the metal-faced insulated panel market, the Polyurethane (PU) Core Material segment is the largest. Polyurethane foam offers excellent thermal insulation properties, high strength-to-weight ratio, and versatility, making it a preferred choice for core materials in insulated panels. The PU core provides effective insulation against heat transfer, reducing energy consumption for heating and cooling in buildings and refrigerated storage facilities. Additionally, polyurethane insulated panels are lightweight, easy to install, and durable, offering long-term performance and cost savings over their lifespan. Moreover, PU foam is compatible with various facing materials and can be customized to meet specific performance requirements, further enhancing its suitability for a wide range of applications in construction, cold storage, transportation, and industrial facilities. As industries prioritize energy efficiency, sustainability, and building performance, the demand for polyurethane core insulated panels continues to grow steadily, driving the dominance of the PU Core Material segment within the market.

Metal faced Insulated Panel Market Share Analysis: External is poised to register the fastest CAGR over the forecast period

Within the metal-faced insulated panel market, the External segment is the fastest-growing. External insulated panels are increasingly utilized in construction projects to enhance building envelope performance, energy efficiency, and aesthetic appeal. These panels offer superior thermal insulation properties, effectively reducing heat loss or gain through exterior walls, roofs, and facades. As energy codes and regulations become more stringent worldwide, the demand for external insulated panels rises as builders and developers seek solutions to meet energy efficiency standards and reduce carbon emissions. Additionally, external insulated panels contribute to improved indoor comfort by maintaining stable indoor temperatures and reducing heating and cooling costs. Moreover, the trend towards sustainable and green building practices further accelerates the adoption of external insulated panels, as they contribute to LEED (Leadership in Energy and Environmental Design) certification and other green building rating systems. As a result, the external segment experiences rapid growth within the metal-faced insulated panel market, driven by the increasing demand for energy-efficient building solutions and the emphasis on sustainable construction practices.

Metal faced Insulated Panel Market Share Analysis: Commercial segment generated the highest revenue in 2024

Within the metal-faced insulated panel market, the Commercial segment is the largest. Commercial buildings, including offices, retail stores, hotels, restaurants, and healthcare facilities, represent a significant portion of the overall demand for metal-faced insulated panels. These panels are extensively used in commercial construction projects for walls, roofs, partitions, and ceilings to provide thermal insulation, structural support, and fire resistance. Additionally, commercial buildings often have diverse and complex requirements for energy efficiency, sustainability, and design flexibility, making metal-faced insulated panels an ideal choice due to their versatility, customization options, and ease of installation. Moreover, as commercial property owners and developers seek to enhance building performance, reduce operating costs, and comply with energy codes and regulations, the demand for metal-faced insulated panels in the commercial segment continues to grow steadily. Furthermore, the trend towards mixed-use developments, urban revitalization projects, and sustainable building practices further drives the adoption of metal-faced insulated panels in commercial construction. As commercial construction activity remains robust globally, the commercial segment maintains its position as the largest within the metal-faced insulated panel market, supported by its indispensable role in meeting the diverse needs of the commercial building sector.

Metal faced Insulated Panel Market

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Metal faced Insulated Panel Companies Profiled in the Study

American Acoustical Products

American Insulated Panel

Atlas Roofing Corp

Bally Refrigerated Boxes

Big Sky Insulations Inc

Branch River Plastics Inc

BRUCHA Corp

CENTRIA

Citadel Architectural Products Inc

Cornerstone Building Brands

Diversified Panel Systems Ltd

Kingspan Group plc

Metl-Span

Nucor Corp

Nudo Products, Inc.

Owens Corning

Portafab Corp

Premier Building Systems Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Metal faced Insulated Panel Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Metal faced Insulated Panel Market Size Outlook, $ Million, 2021 to 2032

3.2 Metal faced Insulated Panel Market Outlook by Type, $ Million, 2021 to 2032

3.3 Metal faced Insulated Panel Market Outlook by Product, $ Million, 2021 to 2032

3.4 Metal faced Insulated Panel Market Outlook by Application, $ Million, 2021 to 2032

3.5 Metal faced Insulated Panel Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Metal faced Insulated Panel Industry

4.2 Key Market Trends in Metal faced Insulated Panel Industry

4.3 Potential Opportunities in Metal faced Insulated Panel Industry

4.4 Key Challenges in Metal faced Insulated Panel Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Metal faced Insulated Panel Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Metal faced Insulated Panel Market Outlook by Segments

7.1 Metal faced Insulated Panel Market Outlook by Segments, $ Million, 2021- 2032

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

8 North America Metal faced Insulated Panel Market Analysis and Outlook To 2032

8.1 Introduction to North America Metal faced Insulated Panel Markets in 2024

8.2 North America Metal faced Insulated Panel Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Metal faced Insulated Panel Market size Outlook by Segments, 2021-2032

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

9 Europe Metal faced Insulated Panel Market Analysis and Outlook To 2032

9.1 Introduction to Europe Metal faced Insulated Panel Markets in 2024

9.2 Europe Metal faced Insulated Panel Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Metal faced Insulated Panel Market Size Outlook by Segments, 2021-2032

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

10 Asia Pacific Metal faced Insulated Panel Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Metal faced Insulated Panel Markets in 2024

10.2 Asia Pacific Metal faced Insulated Panel Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Metal faced Insulated Panel Market size Outlook by Segments, 2021-2032

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

11 South America Metal faced Insulated Panel Market Analysis and Outlook To 2032

11.1 Introduction to South America Metal faced Insulated Panel Markets in 2024

11.2 South America Metal faced Insulated Panel Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Metal faced Insulated Panel Market size Outlook by Segments, 2021-2032

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

12 Middle East and Africa Metal faced Insulated Panel Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Metal faced Insulated Panel Markets in 2024

12.2 Middle East and Africa Metal faced Insulated Panel Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Metal faced Insulated Panel Market size Outlook by Segments, 2021-2032

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

American Acoustical Products

American Insulated Panel

Atlas Roofing Corp

Bally Refrigerated Boxes

Big Sky Insulations Inc

Branch River Plastics Inc

BRUCHA Corp

CENTRIA

Citadel Architectural Products Inc

Cornerstone Building Brands

Diversified Panel Systems Ltd

Kingspan Group plc

Metl-Span

Nucor Corp

Nudo Products, Inc.

Owens Corning

Portafab Corp

Premier Building Systems Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Core Material

Blowing Agents

Polyurethane (PU)

Polyisocyanurate (PIR)

Mineral Wool

Polystyrene (PS)

Phenolic (PF)

By Usage

Internal

External

By End-User

Residential

Commercial

Industrial

Institutional

Infrastructure

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)