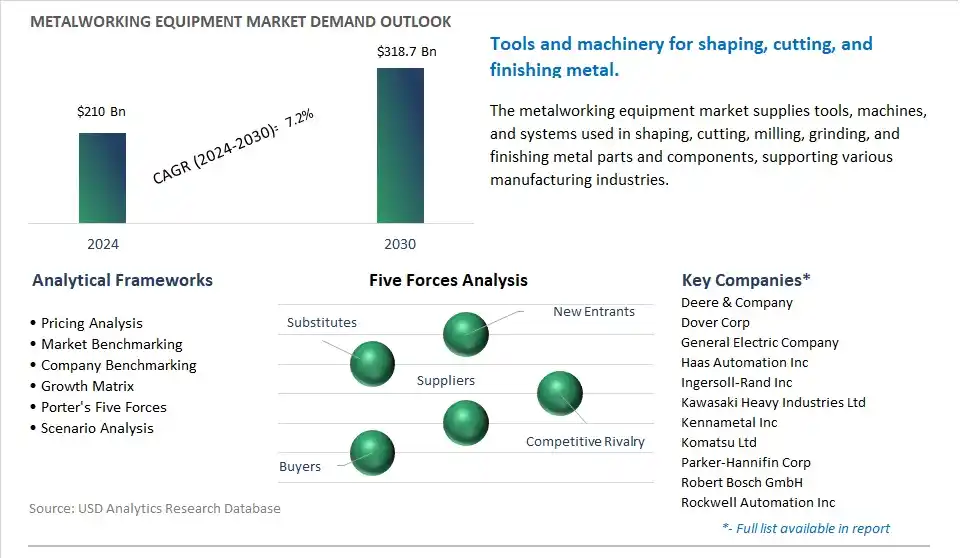

The global Metalworking Equipment Market is poised to register a 7.2% CAGR from $210 Billion in 2024 to $318.7 Billion in 2030.

The global Metalworking Equipment Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Lathe Machines, Milling Machines, Grinding Machines, Drilling Machines, Saw Machines, Others), By End-User (Automotive, Manufacturing, Construction, Marine, Others).

An Introduction to Global Metalworking Equipment Market in 2024

The future of metalworking equipment is shaped by several key trends reflecting advancements in technology, automation, and sustainability in manufacturing industries. One significant trend is the increasing adoption of Industry 4.0 principles, leading to the integration of data-driven systems, IoT sensors, and AI-powered analytics into metalworking equipment. This enables real-time monitoring, predictive maintenance, and optimization of production processes, resulting in improved efficiency, reduced downtime, and higher quality output. Additionally, there is a growing focus on sustainability, with metalworking equipment designed for energy efficiency, waste reduction, and recycling initiatives, aligning with environmental regulations and corporate sustainability goals. Moreover, the demand for versatile and customizable metalworking equipment capable of handling a wide range of materials and geometries is increasing, driven by the need for flexibility in manufacturing operations to meet changing market demands and product specifications.

Metalworking Equipment Market Competitive Landscape

The market report analyses the leading companies in the industry including Deere & Company, Dover Corp, General Electric Company, Haas Automation Inc, Ingersoll-Rand Inc, Kawasaki Heavy Industries Ltd, Kennametal Inc, Komatsu Ltd, Parker-Hannifin Corp, Robert Bosch GmbH, Rockwell Automation Inc, Sandvik AB, The Black & Decker Corp, Yamazaki Mazak Corp.

Metalworking Equipment Market Dynamics

Metalworking Equipment Market Trend: Adoption of Industry 4.0 Technologies in Metalworking

A significant trend in the Metalworking Equipment market is the adoption of Industry 4.0 technologies. As manufacturing industries undergo digital transformation, metalworking equipment is being equipped with advanced technologies such as Internet of Things (IoT), artificial intelligence (AI), machine learning, and robotics. These technologies enable real-time monitoring, predictive maintenance, automated production, and data-driven decision-making, leading to increased productivity, efficiency, and quality in metalworking processes. Manufacturers are embracing Industry 4.0 to optimize their operations, reduce downtime, and stay competitive in a rapidly evolving market landscape.

Metalworking Equipment Market Driver: Growth in Manufacturing Industries and Industrialization

A key driver propelling the Metalworking Equipment market is the growth in manufacturing industries and industrialization globally. With increasing urbanization, population growth, and economic development, there's a rising demand for manufactured goods across sectors such as automotive, aerospace, construction, and consumer electronics. Metalworking equipment, including machine tools, machining centers, welding machines, and sheet metal equipment, is essential for producing components and parts used in various industries. As manufacturing industries expand and modernize their production facilities, the demand for metalworking equipment continues to grow, driving market demand and investment in advanced manufacturing technologies.

Metalworking Equipment Market Opportunity: Customization and Specialization of Equipment

An opportunity in the Metalworking Equipment market lies in customization and specialization of equipment. While standard metalworking equipment meets the needs of many industries, there's potential for growth through the development of specialized equipment tailored to specific applications and industries. Manufacturers aim to capitalize on this opportunity by offering customized solutions such as multi-axis machining centers, laser cutting systems for specific materials, robotic welding cells, and additive manufacturing systems for prototyping and production. Additionally, there's an opportunity to provide value-added services such as training, technical support, and aftermarket services to enhance customer satisfaction and loyalty. By focusing on customization and specialization, manufacturers can address niche markets, differentiate their offerings, and meet the unique requirements of diverse industries, thus driving growth in the Metalworking Equipment market.

Metalworking Equipment Market Share Analysis: Milling Machines generated the highest revenue in 2024

The Milling Machines segment stands as the largest in the Metalworking Equipment Market due to its versatility, precision, and widespread application across various industries. Milling machines are essential tools in metalworking processes, enabling the shaping, cutting, and finishing of metal components with high accuracy and efficiency. These machines utilize rotary cutters to remove material from a workpiece, allowing for the creation of complex shapes, contours, and surface finishes. Further, milling machines are utilized in a wide range of manufacturing operations, including aerospace, automotive, electronics, mold making, and general machining. The ability of milling machines to perform a diverse array of machining operations, such as face milling, end milling, slotting, and profiling, makes them indispensable in metalworking workshops and production facilities. Furthermore, advancements in milling machine technology, such as computer numerical control (CNC) systems, multi-axis machining capabilities, and high-speed cutting tools, enhance productivity, precision, and automation in metalworking operations, further driving the demand for milling machines. As industries continue to evolve and demand higher levels of precision and productivity, the Milling Machines segment maintains its position as the largest and most essential segment in the Metalworking Equipment Market.

Metalworking Equipment Market Share Analysis: Construction segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Construction segment is the fastest-growing segment in the Metalworking Equipment Market. The construction industry is experiencing significant growth worldwide, driven by urbanization, infrastructure development, and housing demand. Metalworking equipment plays a crucial role in construction projects by fabricating structural components, building materials, and architectural elements. Additionally, the adoption of advanced metalworking technologies, such as computer numerical control (CNC) machining, laser cutting, and robotic welding, enhances efficiency, precision, and productivity in construction-related metal fabrication processes. Furthermore, the increasing complexity and customization of construction projects necessitate specialized metalworking equipment capable of meeting diverse project requirements. Further, the construction sector's shift towards sustainable building practices and innovative construction materials drives the demand for metalworking equipment that can work with eco-friendly materials and processes. As construction activities continue to expand globally, fueled by infrastructure investments and urban development projects, the Construction segment experiences rapid growth in the Metalworking Equipment Market.

Metalworking Equipment Market Report Segmentation

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Metalworking Equipment Companies Profiled in the Market Study

Deere & Company

Dover Corp

General Electric Company

Haas Automation Inc

Ingersoll-Rand Inc

Kawasaki Heavy Industries Ltd

Kennametal Inc

Komatsu Ltd

Parker-Hannifin Corp

Robert Bosch GmbH

Rockwell Automation Inc

Sandvik AB

The Black & Decker Corp

Yamazaki Mazak Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Metalworking Equipment Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Metalworking Equipment Market Size Outlook, $ Million, 2021 to 2030

3.2 Metalworking Equipment Market Outlook by Type, $ Million, 2021 to 2030

3.3 Metalworking Equipment Market Outlook by Product, $ Million, 2021 to 2030

3.4 Metalworking Equipment Market Outlook by Application, $ Million, 2021 to 2030

3.5 Metalworking Equipment Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Metalworking Equipment Industry

4.2 Key Market Trends in Metalworking Equipment Industry

4.3 Potential Opportunities in Metalworking Equipment Industry

4.4 Key Challenges in Metalworking Equipment Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Metalworking Equipment Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Metalworking Equipment Market Outlook by Segments

7.1 Metalworking Equipment Market Outlook by Segments, $ Million, 2021- 2030

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

8 North America Metalworking Equipment Market Analysis and Outlook To 2030

8.1 Introduction to North America Metalworking Equipment Markets in 2024

8.2 North America Metalworking Equipment Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Metalworking Equipment Market size Outlook by Segments, 2021-2030

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

9 Europe Metalworking Equipment Market Analysis and Outlook To 2030

9.1 Introduction to Europe Metalworking Equipment Markets in 2024

9.2 Europe Metalworking Equipment Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Metalworking Equipment Market Size Outlook by Segments, 2021-2030

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

10 Asia Pacific Metalworking Equipment Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Metalworking Equipment Markets in 2024

10.2 Asia Pacific Metalworking Equipment Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Metalworking Equipment Market size Outlook by Segments, 2021-2030

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

11 South America Metalworking Equipment Market Analysis and Outlook To 2030

11.1 Introduction to South America Metalworking Equipment Markets in 2024

11.2 South America Metalworking Equipment Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Metalworking Equipment Market size Outlook by Segments, 2021-2030

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

12 Middle East and Africa Metalworking Equipment Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Metalworking Equipment Markets in 2024

12.2 Middle East and Africa Metalworking Equipment Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Metalworking Equipment Market size Outlook by Segments, 2021-2030

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Deere & Company

Dover Corp

General Electric Company

Haas Automation Inc

Ingersoll-Rand Inc

Kawasaki Heavy Industries Ltd

Kennametal Inc

Komatsu Ltd

Parker-Hannifin Corp

Robert Bosch GmbH

Rockwell Automation Inc

Sandvik AB

The Black & Decker Corp

Yamazaki Mazak Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Lathe Machines

Milling Machines

Grinding Machines

Drilling Machines

Saw Machines

Others

By End-User

Automotive

Manufacturing

Construction

Marine

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)