The Neurointerventional Devices Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Product (Stents, Embolic Coils, Catheter, Wires, Others), By Indication (Brain Aneurysm, Stroke, Others), By Application (Hospitals, Ambulatory Surgical Centers, Others).

In 2024, the market for neurointerventional devices continues to expand, driven by advancements in minimally invasive techniques for diagnosing and treating a wide range of neurovascular disorders, including stroke, aneurysms, arteriovenous malformations (AVMs), and intracranial stenosis. Neurointerventional devices encompass a variety of tools and technologies used in endovascular procedures to access and treat abnormalities within the blood vessels of the brain and spinal cord. These devices include catheters, guidewires, stent retrievers, embolic coils, flow diverters, thrombectomy devices, and intracranial stents, among others, designed to provide precise navigation, thrombus removal, vessel reconstruction, and embolization of abnormal vascular structures. Technological advancements in neurointerventional devices include the development of biocompatible materials, improved imaging modalities such as digital subtraction angiography (DSA) and cone-beam computed tomography (CBCT), and the integration of robotics and navigation systems for enhanced procedural accuracy and safety. Moreover, the emergence of neurovascular implants with bioactive coatings, drug-eluting properties, and advanced flow dynamics optimization offers potential benefits for reducing restenosis, promoting vessel healing, and improving long-term outcomes for patients undergoing endovascular interventions. With the increasing emphasis on rapid treatment of acute stroke, early detection of intracranial aneurysms, and personalized approaches to neurovascular care, the market for neurointerventional devices is poised for continued growth and innovation, offering neurosurgeons, interventional radiologists, and neurologists advanced tools and techniques for addressing complex cerebrovascular pathologies and improving patient outcomes.

A prominent trend in the neurointerventional devices market is the continuous advancements in minimally invasive procedures for the diagnosis and treatment of neurological conditions, driving the demand for innovative neurointerventional devices. Neurointerventional procedures involve the use of specialized devices such as stents, catheters, coils, and embolic agents to access and treat vascular abnormalities in the brain and spinal cord, including aneurysms, arteriovenous malformations (AVMs), and ischemic stroke. Recent developments in imaging technology, interventional radiology techniques, and endovascular devices enable neurointerventionalists to perform complex procedures with greater precision, safety, and efficacy, while minimizing patient trauma and recovery times. This trend is driven by the growing preference for minimally invasive treatment options that offer reduced procedural risks, shorter hospital stays, and improved patient outcomes compared to traditional surgical approaches. Additionally, advancements in neuroimaging modalities such as digital subtraction angiography (DSA), magnetic resonance imaging (MRI), and computed tomography angiography (CTA) provide detailed anatomical information and real-time guidance during neurointerventional procedures, enhancing procedural planning and patient safety. As healthcare providers and patients seek less invasive alternatives for neurovascular conditions, the market for neurointerventional devices is expected to witness significant growth and innovation, driven by the imperative to improve clinical outcomes and enhance the patient experience in neurointerventional practice.

The primary driver propelling the neurointerventional devices market is the rising incidence of neurovascular diseases and stroke, driving the demand for effective interventional therapies and devices to address critical care needs and improve patient outcomes. Neurovascular diseases, including ischemic stroke, hemorrhagic stroke, intracranial aneurysms, and cerebral arteriovenous malformations (AVMs), represent leading causes of morbidity and mortality worldwide, posing significant challenges to healthcare systems and public health initiatives. Ischemic stroke, in particular, is a medical emergency requiring rapid intervention to restore blood flow to the brain and prevent irreversible neurological damage. This driver is further fueled by demographic trends such as population aging, increasing prevalence of stroke risk factors such as hypertension and diabetes, and lifestyle factors such as smoking and physical inactivity, which contribute to the growing burden of neurovascular diseases and stroke-related disabilities. Additionally, advancements in acute stroke care protocols, telestroke networks, and endovascular thrombectomy techniques have revolutionized the management of acute ischemic stroke, driving the demand for neurointerventional devices such as clot retrieval devices and stent retrievers. As healthcare systems prioritize stroke prevention, early intervention, and comprehensive stroke care pathways, the market for neurointerventional devices is expected to experience sustained growth and innovation, driven by the imperative to reduce stroke-related morbidity and mortality rates and improve patient outcomes across the continuum of stroke care.

An opportunity within the neurointerventional devices market lies in the development of next-generation technologies that offer improved safety, efficacy, and patient outcomes in neurointerventional procedures. Novel neurointerventional devices, such as flow diverters, intrasaccular devices, and neurothrombectomy devices, hold promise for addressing unmet clinical needs and enhancing treatment options for neurovascular diseases and stroke. Flow diverters, for example, are stent-like devices designed to redirect blood flow away from intracranial aneurysms, reducing the risk of rupture and promoting aneurysm healing over time. Intrasaccular devices, such as flow disruptors and flow diverting stents, offer alternatives for treating complex aneurysms and preventing recurrence. Neurothrombectomy devices, including aspiration catheters and stent retrievers, enable rapid and complete removal of blood clots in acute ischemic stroke, improving recanalization rates and functional outcomes for patients. By leveraging advancements in biomaterials science, device engineering, and neuroimaging technology, manufacturers can develop innovative neurointerventional devices that address specific clinical challenges, enhance procedural outcomes, and expand treatment options for neurovascular diseases and stroke. Additionally, collaborations between academic research institutions, medical device companies, and regulatory agencies can accelerate the translation of novel technologies from bench to bedside, facilitating the development and commercialization of next-generation neurointerventional devices. As the field of neurointerventional medicine continues to evolve, the market for advanced neurointerventional technologies presents opportunities for differentiation, market expansion, and leadership in addressing unmet clinical needs and improving patient care in neurovascular practice.

The fast-growing segment within the neurointerventional devices market is embolic coils for the treatment of brain aneurysms. This growth is driven by several factors. Firstly, embolic coils are widely used in endovascular procedures, such as coil embolization or endovascular coiling, for the treatment of intracranial aneurysms. These devices are deployed within the aneurysm sac to promote thrombosis and occlude blood flow, thereby preventing rupture and reducing the risk of hemorrhagic stroke, a potentially life-threatening complication of untreated or ruptured aneurysms. Secondly, the increasing incidence of intracranial aneurysms, particularly in aging populations and individuals with risk factors such as hypertension, smoking, and genetic predisposition, underscores the clinical need for effective and minimally invasive treatment options to mitigate the morbidity and mortality associated with aneurysmal rupture. Embolic coils offer advantages such as precise placement, conformability to the aneurysm anatomy, and the ability to achieve durable occlusion while preserving parent vessel patency, making them a preferred choice for endovascular treatment of both ruptured and unruptured aneurysms. Additionally, advancements in coil design, material composition, and delivery systems enhance the navigability, trackability, and retrievability of embolic coils, facilitating safe and successful embolization procedures in challenging anatomical locations and complex aneurysm morphologies. Moreover, the growing adoption of minimally invasive neurointerventional techniques and the expansion of neurointerventional capabilities in hospitals and ambulatory surgical centers drive the demand for embolic coils as a frontline treatment modality for intracranial aneurysms, offering patients a less invasive alternative to traditional surgical approaches such as clipping. Furthermore, collaborations between medical device manufacturers, neurointerventionalists, and academic research institutions spur innovation and investment in embolic coil technology, leading to the development of next-generation coils with enhanced thrombogenicity, radiopacity, and biocompatibility to optimize treatment outcomes and reduce the risk of recurrence or rebleeding in patients undergoing endovascular aneurysm repair. Overall, the combination of clinical need, technological innovation, and procedural advancements positions embolic coils for brain aneurysm as the fast-growing segment within the neurointerventional devices market.

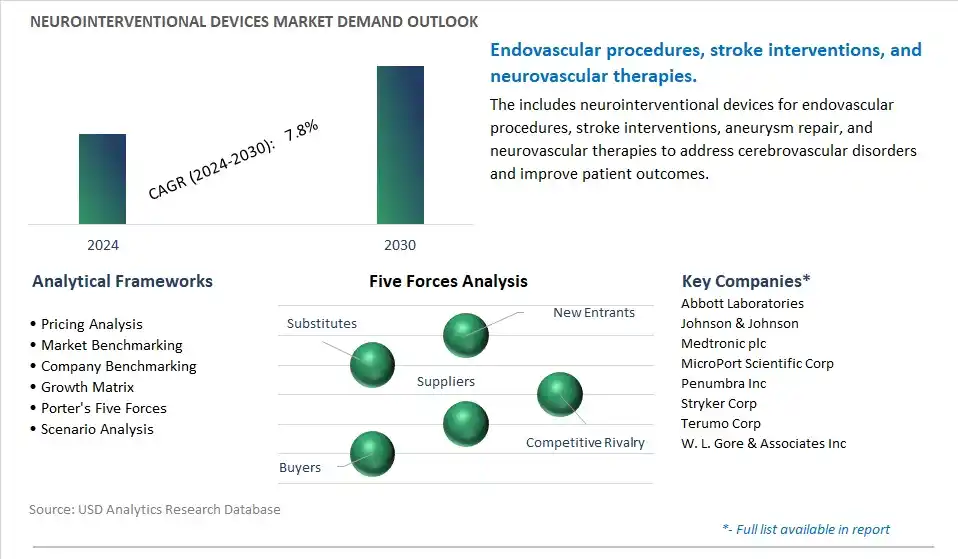

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossAbbott Laboratories, Johnson & Johnson, Medtronic plc, MicroPort Scientific Corp, Penumbra Inc, Stryker Corp, Terumo Corp, W. L. Gore & Associates Inc

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Abbott Laboratories

Johnson & Johnson

Medtronic plc

MicroPort Scientific Corp

Penumbra Inc

Stryker Corp

Terumo Corp

W. L. Gore & Associates Inc

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Neurointerventional Devices Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Neurointerventional Devices Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Neurointerventional Devices Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Neurointerventional Devices Market Size Outlook, $ Million, 2021 to 2030

3.2 Neurointerventional Devices Market Outlook by Type, $ Million, 2021 to 2030

3.3 Neurointerventional Devices Market Outlook by Product, $ Million, 2021 to 2030

3.4 Neurointerventional Devices Market Outlook by Application, $ Million, 2021 to 2030

3.5 Neurointerventional Devices Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Neurointerventional Devices Industry

4.2 Key Market Trends in Neurointerventional Devices Industry

4.3 Potential Opportunities in Neurointerventional Devices Industry

4.4 Key Challenges in Neurointerventional Devices Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Neurointerventional Devices Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Neurointerventional Devices Market Outlook by Segments

7.1 Neurointerventional Devices Market Outlook by Segments, $ Million, 2021- 2030

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

8 North America Neurointerventional Devices Market Analysis and Outlook To 2030

8.1 Introduction to North America Neurointerventional Devices Markets in 2024

8.2 North America Neurointerventional Devices Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Neurointerventional Devices Market size Outlook by Segments, 2021-2030

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

9 Europe Neurointerventional Devices Market Analysis and Outlook To 2030

9.1 Introduction to Europe Neurointerventional Devices Markets in 2024

9.2 Europe Neurointerventional Devices Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Neurointerventional Devices Market Size Outlook by Segments, 2021-2030

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

10 Asia Pacific Neurointerventional Devices Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Neurointerventional Devices Markets in 2024

10.2 Asia Pacific Neurointerventional Devices Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Neurointerventional Devices Market size Outlook by Segments, 2021-2030

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

11 South America Neurointerventional Devices Market Analysis and Outlook To 2030

11.1 Introduction to South America Neurointerventional Devices Markets in 2024

11.2 South America Neurointerventional Devices Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Neurointerventional Devices Market size Outlook by Segments, 2021-2030

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

12 Middle East and Africa Neurointerventional Devices Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Neurointerventional Devices Markets in 2024

12.2 Middle East and Africa Neurointerventional Devices Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Neurointerventional Devices Market size Outlook by Segments, 2021-2030

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Abbott Laboratories

Johnson & Johnson

Medtronic plc

MicroPort Scientific Corp

Penumbra Inc

Stryker Corp

Terumo Corp

W. L. Gore & Associates Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Stents

Embolic Coils

Catheter

Wires

Others

By Indication

Brain Aneurysm

Stroke

Others

By Application

Hospitals

Ambulatory Surgical Centers

Others

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

The global Neurointerventional Devices Market is one of the lucrative growth markets, poised to register a 7.8% growth (CAGR) between 2024 and 2030.

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

Abbott Laboratories, Johnson & Johnson, Medtronic plc, MicroPort Scientific Corp, Penumbra Inc, Stryker Corp, Terumo Corp, W. L. Gore & Associates Inc

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2030; Currency: USD; Volume