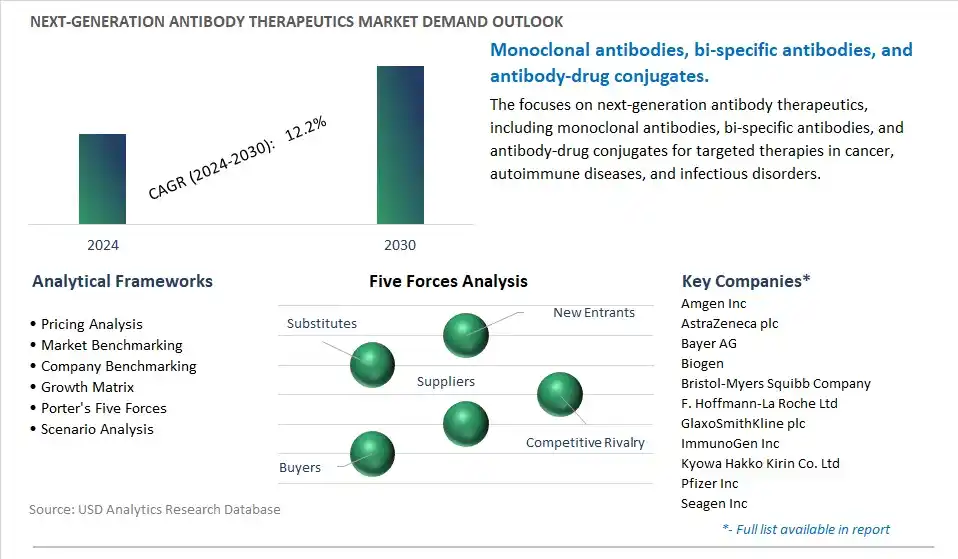

Next Generation Antibody Therapeutics Market is estimated to increase at a Compounded Annual Growth Rate of 12.2% CAGR over the forecast period from 2024 to 2030

The Next Generation Antibody Therapeutics Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Therapeutic Area (Oncology, Autoimmune/Inflammatory), By Technology (Antibody-Drug Conjugates (ADCs), Bispecific Antibodies (BsAbs), Fc-Engineered Antibodies, Antibody Fragments and Antibody-Like Proteins (AF & ALPs), Biosimilar Antibody Products).

An Introduction to Next Generation Antibody Therapeutics Market in 2024

In 2024, the market for next-generation antibody therapeutics continues to advance, offering innovative approaches to treating cancer, autoimmune diseases, infectious diseases, and other medical conditions. Next-generation antibody therapeutics encompass a diverse range of antibody-based drugs, including monoclonal antibodies (mAbs), bispecific antibodies, antibody-drug conjugates (ADCs), and engineered antibody fragments, designed to target specific antigens or cell surface receptors implicated in disease pathogenesis. These advanced antibody formats offer advantages such as enhanced binding specificity, improved tissue penetration, reduced immunogenicity, and enhanced effector functions compared to traditional antibodies, enabling more potent and targeted therapeutic effects. Technological advancements in next-generation antibody therapeutics include the development of novel antibody engineering platforms, computational modeling techniques, and high-throughput screening assays for antibody discovery, optimization, and production. Moreover, the integration of personalized medicine approaches, biomarker-driven patient selection, and combination therapy strategies enhances the clinical utility and efficacy of next-generation antibody drugs across a wide range of therapeutic indications. With the growing demand for targeted therapies, precision medicine, and immunotherapy options, the market for next-generation antibody therapeutics is poised for continued growth and innovation, offering promising opportunities for improving patient outcomes and addressing unmet medical needs in diverse disease settings.

Market Trend: Advancements in Antibody Engineering and Design

A prominent trend in the next-generation antibody therapeutics market is the rapid advancements in antibody engineering and design, leading to the development of novel antibody-based therapies with enhanced efficacy, specificity, and safety profiles. Traditional monoclonal antibodies have revolutionized the treatment of various diseases, but limitations such as immunogenicity, suboptimal tissue penetration, and resistance mechanisms have spurred the need for next-generation approaches. This trend is characterized by innovations in antibody formats, such as bispecific antibodies, antibody-drug conjugates (ADCs), and multispecific antibodies, which offer improved targeting of disease pathways, enhanced therapeutic potency, and reduced off-target effects. Additionally, advancements in antibody discovery technologies, such as phage display, yeast display, and transgenic animal platforms, enable the generation of antibodies with superior binding affinity, selectivity, and biophysical properties. As pharmaceutical companies and biotechnology firms invest in next-generation antibody platforms and technologies, the market for next-generation antibody therapeutics is poised for significant growth and innovation, driven by the imperative to address unmet medical needs and improve patient outcomes across diverse therapeutic areas.

Market Driver: Growing Demand for Targeted and Personalized Therapies

The primary driver propelling the next-generation antibody therapeutics market is the growing demand for targeted and personalized therapies that offer improved efficacy, safety, and tolerability compared to conventional treatments. Next-generation antibody therapeutics enable precise modulation of disease pathways, selective targeting of tumor antigens, and tailored immune modulation, leading to better therapeutic outcomes and reduced systemic toxicity. This driver is fueled by advances in molecular profiling, biomarker identification, and patient stratification strategies, which enable the selection of patients most to benefit from specific antibody-based therapies. Additionally, the increasing prevalence of complex diseases, such as cancer, autoimmune disorders, and infectious diseases, underscores the need for innovative treatment approaches that address heterogeneous patient populations and overcome treatment resistance mechanisms. As healthcare systems prioritize value-based care, personalized medicine, and precision oncology initiatives, the market for next-generation antibody therapeutics is expected to experience sustained growth and investment, driven by the imperative to improve therapeutic outcomes and reduce healthcare costs through targeted interventions.

Market Opportunity: Development of Immunomodulatory Antibodies

An opportunity within the next-generation antibody therapeutics market lies in the development of immunomodulatory antibodies that harness the immune system to treat cancer, autoimmune diseases, and inflammatory disorders. Opportunities exist for pharmaceutical companies to explore novel antibody targets, pathways, and mechanisms of action involved in immune regulation, T-cell activation, and immune checkpoint inhibition. Immunomodulatory antibodies, such as immune checkpoint inhibitors, costimulatory agonists, and cytokine modulators, offer potential benefits in enhancing antitumor immunity, overcoming immunosuppression, and improving response rates to immunotherapy. Additionally, opportunities exist for combination therapies that synergistically target multiple immune checkpoints or pathways to overcome resistance and enhance durable responses in patients with refractory cancers or immune-mediated disorders. Collaborations between industry, academia, and regulatory agencies can drive innovation and development of immunomodulatory antibody therapies, ensuring rigorous preclinical evaluation, clinical translation, and regulatory approval of next-generation immunotherapies. As the field of cancer immunotherapy and immunology evolves, the market presents opportunities for differentiation, market expansion, and leadership in delivering transformative antibody-based therapies that harness the immune system to combat cancer and other immune-related diseases.

Next-Generation Antibody Therapeutics Market Share Analysis: Antibody-Drug Conjugates (ADCs)

The fast-growing segment within the next-generation antibody therapeutics market is antibody-drug conjugates (ADCs). This growth is driven by several key factors. Firstly, ADCs represent a novel class of targeted cancer therapies designed to selectively deliver cytotoxic drugs to tumor cells while sparing normal tissues, thereby maximizing therapeutic efficacy and minimizing systemic toxicity associated with conventional chemotherapy. The precise targeting mechanism of ADCs involves the conjugation of monoclonal antibodies (mAbs) with potent cytotoxic payloads via stable linkers, enabling specific recognition of tumor-associated antigens expressed on cancer cells and internalization of the ADC-drug complex into malignant cells, where the cytotoxic payload is released and exerts its anti-cancer effects through various mechanisms, including inhibition of DNA synthesis, microtubule disruption, and induction of apoptosis. Secondly, ADCs offer several advantages over traditional chemotherapy and monoclonal antibodies, including improved tumor selectivity, enhanced therapeutic index, prolonged circulation time, reduced off-target effects, and potential synergy with other cancer therapies, such as immune checkpoint inhibitors and targeted small molecule inhibitors. These attributes make ADCs promising candidates for the treatment of a wide range of solid tumors and hematological malignancies, including breast cancer, lymphoma, leukemia, lung cancer, and ovarian cancer, among others. Additionally, the growing pipeline of ADC candidates in clinical development, coupled with advancements in antibody engineering, linker chemistry, and payload optimization, drives innovation and expands the therapeutic landscape of ADC-based cancer therapies, with numerous ADCs entering late-stage clinical trials and receiving regulatory approvals for the treatment of various cancer types. Furthermore, strategic collaborations between pharmaceutical companies, biotechnology firms, academic institutions, and contract manufacturing organizations accelerate the development and commercialization of ADC-based therapeutics, facilitating the translation of preclinical research into clinically validated treatments and improving patient access to innovative cancer therapies. Moreover, the increasing prevalence of cancer worldwide, coupled with the unmet medical need for effective and well-tolerated treatment options, underscores the importance of ADCs as a promising strategy to address the challenges of cancer treatment and improve patient outcomes. Overall, the combination of scientific innovation, clinical demand, and industry investment positions antibody-drug conjugates as the fast-growing segment within the next-generation antibody therapeutics market.

Next Generation Antibody Therapeutics Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossAmgen Inc, AstraZeneca plc, Bayer AG, Biogen, Bristol-Myers Squibb Company, F. Hoffmann-La Roche Ltd, GlaxoSmithKline plc, ImmunoGen Inc, Kyowa Hakko Kirin Co. Ltd, Pfizer Inc, Seagen Inc, Xencor Inc

Next Generation Antibody Therapeutics Market Segmentation

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Next Generation Antibody Therapeutics Market Companies

Amgen Inc

AstraZeneca plc

Bayer AG

Biogen

Bristol-Myers Squibb Company

F. Hoffmann-La Roche Ltd

GlaxoSmithKline plc

ImmunoGen Inc

Kyowa Hakko Kirin Co. Ltd

Pfizer Inc

Seagen Inc

Xencor Inc

Reasons to Buy the Next Generation Antibody Therapeutics Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Next Generation Antibody Therapeutics Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Next Generation Antibody Therapeutics Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Next Generation Antibody Therapeutics Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Next Generation Antibody Therapeutics Market Size Outlook, $ Million, 2021 to 2030

3.2 Next Generation Antibody Therapeutics Market Outlook by Type, $ Million, 2021 to 2030

3.3 Next Generation Antibody Therapeutics Market Outlook by Product, $ Million, 2021 to 2030

3.4 Next Generation Antibody Therapeutics Market Outlook by Application, $ Million, 2021 to 2030

3.5 Next Generation Antibody Therapeutics Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Next Generation Antibody Therapeutics Industry

4.2 Key Market Trends in Next Generation Antibody Therapeutics Industry

4.3 Potential Opportunities in Next Generation Antibody Therapeutics Industry

4.4 Key Challenges in Next Generation Antibody Therapeutics Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Next Generation Antibody Therapeutics Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Next Generation Antibody Therapeutics Market Outlook by Segments

7.1 Next Generation Antibody Therapeutics Market Outlook by Segments, $ Million, 2021- 2030

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

8 North America Next Generation Antibody Therapeutics Market Analysis and Outlook To 2030

8.1 Introduction to North America Next Generation Antibody Therapeutics Markets in 2024

8.2 North America Next Generation Antibody Therapeutics Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Next Generation Antibody Therapeutics Market size Outlook by Segments, 2021-2030

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

9 Europe Next Generation Antibody Therapeutics Market Analysis and Outlook To 2030

9.1 Introduction to Europe Next Generation Antibody Therapeutics Markets in 2024

9.2 Europe Next Generation Antibody Therapeutics Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Next Generation Antibody Therapeutics Market Size Outlook by Segments, 2021-2030

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

10 Asia Pacific Next Generation Antibody Therapeutics Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Next Generation Antibody Therapeutics Markets in 2024

10.2 Asia Pacific Next Generation Antibody Therapeutics Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Next Generation Antibody Therapeutics Market size Outlook by Segments, 2021-2030

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

11 South America Next Generation Antibody Therapeutics Market Analysis and Outlook To 2030

11.1 Introduction to South America Next Generation Antibody Therapeutics Markets in 2024

11.2 South America Next Generation Antibody Therapeutics Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Next Generation Antibody Therapeutics Market size Outlook by Segments, 2021-2030

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

12 Middle East and Africa Next Generation Antibody Therapeutics Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Next Generation Antibody Therapeutics Markets in 2024

12.2 Middle East and Africa Next Generation Antibody Therapeutics Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Next Generation Antibody Therapeutics Market size Outlook by Segments, 2021-2030

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Amgen Inc

AstraZeneca plc

Bayer AG

Biogen

Bristol-Myers Squibb Company

F. Hoffmann-La Roche Ltd

GlaxoSmithKline plc

ImmunoGen Inc

Kyowa Hakko Kirin Co. Ltd

Pfizer Inc

Seagen Inc

Xencor Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Therapeutic Area

Oncology

Autoimmune/Inflammatory

By Technology

Antibody-Drug Conjugates (ADCs)

Bispecific Antibodies (BsAbs)

Fc-Engineered Antibodies

Antibody Fragments and Antibody-Like Proteins (AF & ALPs)

Biosimilar Antibody Products

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)