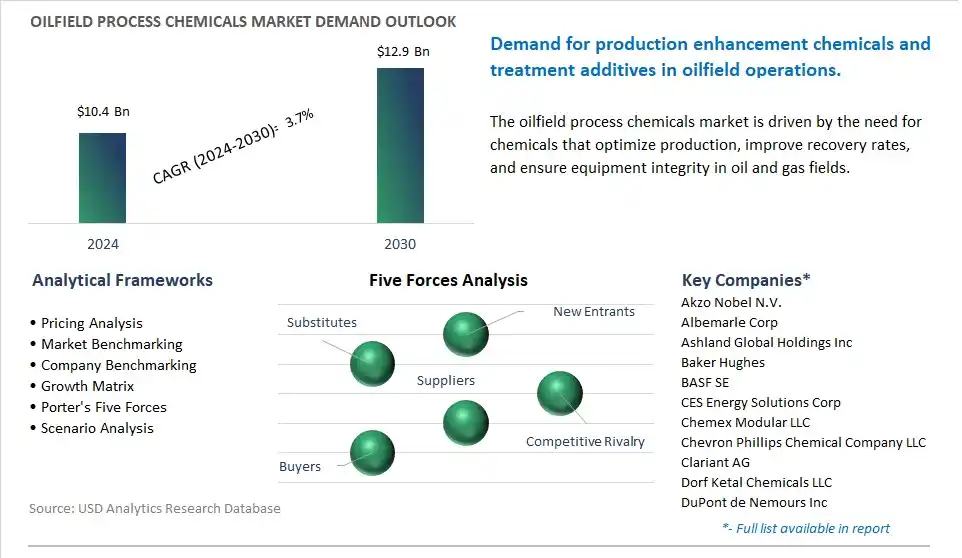

The global Oilfield Process Chemicals Market is poised to register a 3.7% CAGR from $10.4 Billion in 2024 to $12.9 Billion in 2030.

The global Oilfield Process Chemicals Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Drilling Fluids, Cementing Chemicals, Workover and Completion Chemicals, Enhanced Oil Recovery Chemicals, Stimulation Chemicals, Production Chemicals), By Application (Drilling Fluid, Well Stimulation, Enhanced Oil Recovery (EOR), Cementing, Workover and Completion).

An Introduction to Global Oilfield Process Chemicals Market in 2024

The future of oilfield process chemicals is shaped by several key trends, including increasing demand for specialty chemicals in oil and gas production, advancements in chemical formulation and application technologies, and growing emphasis on production optimization, asset integrity, and environmental sustainability in the oilfield industry. Oilfield process chemicals encompass a wide range of specialty chemicals used in various stages of upstream, midstream, and downstream operations such as corrosion inhibitors, scale inhibitors, demulsifiers, and biocides. With the rise of mature fields, enhanced oil recovery techniques, and complex reservoir conditions, there's a growing need for process chemicals that offer effective solutions to challenges such as corrosion, scale deposition, emulsion breaking, and microbial contamination while minimizing environmental impact and operational costs. Moreover, advancements in chemical synthesis, such as green chemistry principles, molecular modeling, and high-throughput screening, are driving the development of innovative chemical formulations with enhanced performance attributes, compatibility with reservoir fluids, and biodegradability for specific applications in oil and gas production. Additionally, the integration of process chemicals into digital oilfield solutions such as predictive analytics, remote monitoring, and autonomous control systems is enabling the optimization of production processes, asset integrity management, and environmental compliance in the oilfield industry. Collaboration between chemical suppliers, oilfield operators, technology providers, and regulatory agencies is essential to drive innovation, ensure chemical performance, and address market demands in the oilfield process chemicals industry.

Oilfield Process Chemicals Market Competitive Landscape

The market report analyses the leading companies in the industry including Akzo Nobel N.V., Albemarle Corp, Ashland Global Holdings Inc, Baker Hughes, BASF SE, CES Energy Solutions Corp, Chemex Modular LLC, Chevron Phillips Chemical Company LLC, Clariant AG, Dorf Ketal Chemicals LLC, DuPont de Nemours Inc, Ecolab Inc, Gulf Coast Chemical, Halliburton Company, Huntsman International, Lamberti S.p.A., Newpark Resources Inc, Schlumberger NV, SICHEM S.p.A., Solvay S.A., Stepan Company, The Dow Chemical company, The Lubrizol Corp.

Oilfield Process Chemicals Market Dynamics

Oilfield Process Chemicals Market Trend: Adoption of Digitalization and Automation in Oilfield Operations

A significant trend in the oilfield process chemicals market is the increasing adoption of digitalization and automation in oilfield operations. With advancements in technology and data analytics, oilfield operators are increasingly leveraging digital solutions to optimize production processes, enhance efficiency, and reduce operational costs. Oilfield process chemicals play a critical role in various processes such as drilling, production, well stimulation, and enhanced oil recovery. The integration of digital technologies allows for real-time monitoring, predictive maintenance, and optimization of chemical usage, leading to improved performance and resource utilization. This trend is driven by the need for operational excellence, asset integrity, and cost optimization in the oil and gas industry. As companies embrace digital transformation initiatives to remain competitive and maximize returns from oilfield assets, the demand for process chemicals that complement digital solutions is expected to grow.

Oilfield Process Chemicals Market Driver: Increasing Oil and Gas Production Activities

A major driver of the oilfield process chemicals market is the increasing oil and gas production activities worldwide. Despite the shift towards renewable energy sources, oil and gas remain essential components of the global energy mix, driving continued exploration, development, and production activities in various regions. Oilfield process chemicals are essential for optimizing production processes, mitigating operational challenges, and maximizing recovery rates in oil and gas reservoirs. The driver behind this demand is the growing energy demand, population growth, and industrialization, particularly in emerging economies. Additionally, advancements in drilling technologies, such as horizontal drilling and hydraulic fracturing, have unlocked new reserves and increased the complexity of oilfield operations, driving the need for specialized process chemicals. As oilfield operators strive to maximize production efficiency and recoverable reserves, the demand for process chemicals to support production activities is expected to remain strong.

Oilfield Process Chemicals Market Opportunity: Development of Environmentally Friendly and Sustainable Chemical Solutions

An opportunity within the oilfield process chemicals market lies in the development of environmentally friendly and sustainable chemical solutions. With increasing regulatory scrutiny and stakeholder pressure to reduce environmental impact, there's a growing demand for process chemicals that are safe, biodegradable, and non-toxic. Oilfield operators are seeking chemical solutions that minimize environmental footprint, protect worker health, and comply with regulatory requirements. Opportunities exist for the development of eco-friendly alternatives to traditional chemical formulations, such as bio-based surfactants, green solvents, and low-emission corrosion inhibitors. By investing in research and development, innovation in chemical formulations, and collaboration with environmental agencies, companies can capitalize on opportunities to provide sustainable chemical solutions that meet the evolving needs of oilfield operators. Additionally, there's an opportunity to differentiate in the market by offering comprehensive chemical management services, including chemical monitoring, recycling, and disposal solutions, to support environmental stewardship and compliance initiatives in the oil and gas industry.

Oilfield Process Chemicals Market Share Analysis: The Production Chemicals Segment generated the highest revenue in 2024

The Production Chemicals segment is the largest in the Oilfield Process Chemicals Market, primarily due to its critical role in maintaining efficient and reliable oil and gas production operations. Production chemicals encompass a wide range of specialty chemicals designed to address various challenges encountered during the production phase, including corrosion inhibition, scale control, emulsion breaking, wax and asphaltene inhibition, and hydrate management. These chemicals are essential for optimizing production rates, extending asset lifespan, and ensuring the integrity and safety of production equipment and infrastructure. Further, the complexity of oilfield production environments, including reservoir characteristics, fluid properties, and operating conditions, necessitates tailored chemical solutions to mitigate production challenges effectively. Additionally, stringent environmental and regulatory requirements mandate the use of environmentally friendly and biodegradable production chemicals, further driving innovation and investment in this segment. Furthermore, the increasing adoption of advanced production techniques, such as unconventional oil and gas production and deepwater operations, amplifies the demand for specialized production chemicals to address unique production challenges. As oil and gas producers prioritize efficiency, sustainability, and operational excellence, the demand for production chemicals is expected to remain robust, solidifying the Production Chemicals segment as the largest segment in the Oilfield Process Chemicals Market.

Oilfield Process Chemicals Market Share Analysis: The Enhanced Oil Recovery (EOR) segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Enhanced Oil Recovery (EOR) segment is the fastest-growing segment in the Oilfield Process Chemicals Market. Enhanced Oil Recovery techniques, including thermal, chemical, and microbial methods, are increasingly employed to extract additional hydrocarbons from reservoirs beyond primary and secondary recovery stages. Chemical EOR methods, in particular, rely on the injection of specialized chemicals into reservoirs to alter fluid properties, improve sweep efficiency, and mitigate reservoir heterogeneities, thereby enhancing oil recovery rates. Chemical EOR processes involve the injection of polymers, surfactants, alkalis, and other specialty chemicals tailored to specific reservoir conditions and production challenges. Further, the growing emphasis on optimizing hydrocarbon production, maximizing asset value, and extending reservoir life drives the adoption of advanced chemical EOR techniques globally. Additionally, advancements in chemical formulation technologies, reservoir characterization, and modeling tools enable the development of customized chemical EOR solutions to address reservoir-specific challenges effectively. Furthermore, favorable government incentives, technological advancements, and increasing investments in mature oilfields and unconventional reservoirs further accelerate the growth of the Chemical EOR segment in the Oilfield Process Chemicals Market. As oil and gas operators seek innovative solutions to enhance oil recovery rates and maximize hydrocarbon reserves, the demand for specialized chemicals for EOR applications is expected to experience sustained acceleration, positioning the Chemical EOR segment as a key driver of growth in the market.

Oilfield Process Chemicals Market Report Segmentation

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Oilfield Process Chemicals Companies Profiled in the Market Study

Akzo Nobel N.V.

Albemarle Corp

Ashland Global Holdings Inc

Baker Hughes

BASF SE

CES Energy Solutions Corp

Chemex Modular LLC

Chevron Phillips Chemical Company LLC

Clariant AG

Dorf Ketal Chemicals LLC

DuPont de Nemours Inc

Ecolab Inc

Gulf Coast Chemical

Halliburton Company

Huntsman International

Lamberti S.p.A.

Newpark Resources Inc

Schlumberger NV

SICHEM S.p.A.

Solvay S.A.

Stepan Company

The Dow Chemical company

The Lubrizol Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Oilfield Process Chemicals Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Oilfield Process Chemicals Market Size Outlook, $ Million, 2021 to 2030

3.2 Oilfield Process Chemicals Market Outlook by Type, $ Million, 2021 to 2030

3.3 Oilfield Process Chemicals Market Outlook by Product, $ Million, 2021 to 2030

3.4 Oilfield Process Chemicals Market Outlook by Application, $ Million, 2021 to 2030

3.5 Oilfield Process Chemicals Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Oilfield Process Chemicals Industry

4.2 Key Market Trends in Oilfield Process Chemicals Industry

4.3 Potential Opportunities in Oilfield Process Chemicals Industry

4.4 Key Challenges in Oilfield Process Chemicals Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Oilfield Process Chemicals Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Oilfield Process Chemicals Market Outlook by Segments

7.1 Oilfield Process Chemicals Market Outlook by Segments, $ Million, 2021- 2030

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

8 North America Oilfield Process Chemicals Market Analysis and Outlook To 2030

8.1 Introduction to North America Oilfield Process Chemicals Markets in 2024

8.2 North America Oilfield Process Chemicals Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Oilfield Process Chemicals Market size Outlook by Segments, 2021-2030

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

9 Europe Oilfield Process Chemicals Market Analysis and Outlook To 2030

9.1 Introduction to Europe Oilfield Process Chemicals Markets in 2024

9.2 Europe Oilfield Process Chemicals Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Oilfield Process Chemicals Market Size Outlook by Segments, 2021-2030

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

10 Asia Pacific Oilfield Process Chemicals Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Oilfield Process Chemicals Markets in 2024

10.2 Asia Pacific Oilfield Process Chemicals Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Oilfield Process Chemicals Market size Outlook by Segments, 2021-2030

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

11 South America Oilfield Process Chemicals Market Analysis and Outlook To 2030

11.1 Introduction to South America Oilfield Process Chemicals Markets in 2024

11.2 South America Oilfield Process Chemicals Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Oilfield Process Chemicals Market size Outlook by Segments, 2021-2030

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

12 Middle East and Africa Oilfield Process Chemicals Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Oilfield Process Chemicals Markets in 2024

12.2 Middle East and Africa Oilfield Process Chemicals Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Oilfield Process Chemicals Market size Outlook by Segments, 2021-2030

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Akzo Nobel N.V.

Albemarle Corp

Ashland Global Holdings Inc

Baker Hughes

BASF SE

CES Energy Solutions Corp

Chemex Modular LLC

Chevron Phillips Chemical Company LLC

Clariant AG

Dorf Ketal Chemicals LLC

DuPont de Nemours Inc

Ecolab Inc

Gulf Coast Chemical

Halliburton Company

Huntsman International

Lamberti S.p.A.

Newpark Resources Inc

Schlumberger NV

SICHEM S.p.A.

Solvay S.A.

Stepan Company

The Dow Chemical company

The Lubrizol Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Drilling Fluids

Cementing Chemicals

Workover and Completion Chemicals

Enhanced Oil Recovery Chemicals

Stimulation Chemicals

Production Chemicals

By Application

Drilling Fluid

Well Stimulation

Enhanced Oil Recovery (EOR)

Cementing

Workover and Completion

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)