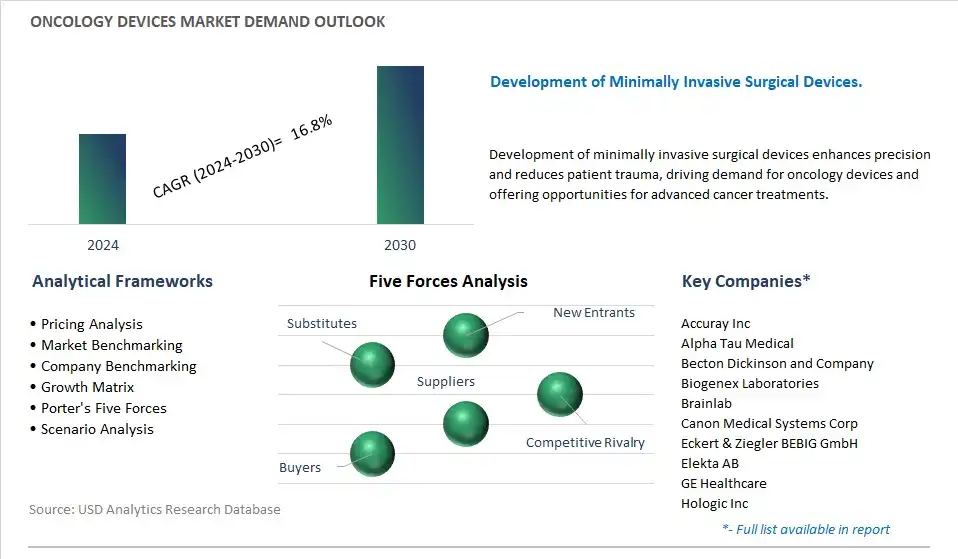

Oncology Devices Market is estimated to increase at a growth rate of 16.8% CAGR over the forecast period from 2024 to 2030.

The global Oncology Devices Marketstudy analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Device (Brachytherapy Devices, Endoscopic Devices), By Therapy (Chemotherapy, Hormone Therapy, Biotherapy/Immunotherapy, Radiation Therapy), By End-user (Hospitals, Cancer Research Institutes, Others).

An introduction to Oncology Devices Market in 2024

Supporting cancer diagnosis, treatment, and supportive care, the Oncology Devices market offers a diverse array of medical devices and equipment for oncology clinics, hospitals, and research laboratories. Oncology devices include diagnostic imaging systems (e.g., PET-CT, MRI), radiation therapy equipment (e.g., linear accelerators, brachytherapy systems), surgical instruments (e.g., biopsy needles, electrosurgical devices), and supportive care devices (e.g., infusion pumps, central venous catheters) designed to improve patient outcomes and quality of life across the cancer care continuum. The market's growth is driven by technological advancements in oncology devices, increasing incidence of cancer, and investments in cancer care infrastructure and supportive technologies worldwide.

Oncology Devices market Trend: Advancements in Minimally Invasive Surgical Techniques

A significant trend in the Oncology Devices market is the continual advancements in minimally invasive surgical techniques. As surgical oncology evolves, there is a notable shift towards minimally invasive procedures, such as laparoscopic surgery, robotic-assisted surgery, and image-guided interventions. These advanced surgical techniques offer benefits such as reduced postoperative pain, shorter hospital stays, faster recovery times, and improved cosmetic outcomes for cancer patients. This trend reflects a broader emphasis on enhancing patient outcomes, reducing healthcare costs, and improving quality of life through less invasive approaches to cancer treatment. As a result, there is increasing demand for oncology devices designed specifically for minimally invasive procedures, driving innovation in surgical instrumentation, imaging technologies, and surgical navigation systems tailored for oncological applications.

Oncology Devices market Driver: Growing Incidence of Cancer and Rising Demand for Oncological Procedures

The primary driver propelling the Oncology Devices market is the growing incidence of cancer and the rising demand for oncological procedures. With cancer continuing to be a leading cause of morbidity and mortality worldwide, there is significant demand for oncology devices used in the diagnosis, treatment, and management of various malignancies. From diagnostic imaging equipment and radiation therapy systems to surgical instruments and implantable devices, oncology devices play a critical role in the multidisciplinary approach to cancer care. The increasing prevalence of cancer, coupled with advancements in early detection, screening programs, and treatment modalities, is driving the adoption of oncology devices across healthcare settings, including hospitals, ambulatory surgery centers, and specialty clinics. The growing demand for oncological procedures and interventions is fueling market growth for a wide range of oncology devices, creating opportunities for device manufacturers, healthcare providers, and medical technology companies to innovate and expand their product portfolios to meet the evolving needs of cancer patients and healthcare professionals.

Oncology Devices market Opportunity: Development of Personalized Oncology Devices and Patient-Specific Implants

An exciting opportunity in the Oncology Devices market lies in the development of personalized oncology devices and patient-specific implants. With the advent of precision medicine and personalized oncology approaches, there is increasing recognition of the importance of tailoring cancer treatments to individual patient characteristics, tumor biology, and genetic profiles. Contract medical device manufacturers and technology companies can capitalize on this opportunity by leveraging advanced manufacturing techniques, such as 3D printing and additive manufacturing, to create customized oncology devices, surgical instruments, and patient-specific implants optimized for individual patient anatomy and treatment requirements. By offering personalized oncology devices, such as customized surgical guides, implantable prostheses, and brachytherapy applicators, manufacturers can enhance treatment precision, improve therapeutic outcomes, and minimize complications for cancer patients undergoing surgical interventions or radiation therapy. Moreover, personalized oncology devices have the potential to streamline surgical workflows, reduce intraoperative variability, and optimize resource utilization in oncological procedures, contributing to the advancement of personalized cancer care and the overall improvement of patient outcomes in oncology practice.

Oncology Devices Market Market Segmentation

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Oncology Devices Market Companies

Accuray Inc

Alpha Tau Medical

Becton Dickinson and Company

Biogenex Laboratories

Brainlab

Canon Medical Systems Corp

Eckert & Ziegler BEBIG GmbH

Elekta AB

GE Healthcare

Hologic Inc

IBA AG

IBA Group

IsoRay

Medtronic PLC

Mevion Medical Systems

Mirada Medical Ltd

Nanobiotix

Navidea Biopharmaceuticals Inc

Oncura Inc

PerkinElmer

Philips Healthcare

RaySearch Laboratories

RefleXion Medical

Roche Diagnostics

Siemens Healthineers

Theragenics Corp

Varian Medical Systems Inc

ViewRay Inc

Vision RT

Reasons to Buy the Oncology Devices Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Oncology Devices Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Oncology Devices Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Oncology Devices Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Oncology Devices Market Size Outlook, $ Million, 2021 to 2030

3.2 Oncology Devices Market Outlook by Type, $ Million, 2021 to 2030

3.3 Oncology Devices Market Outlook by Product, $ Million, 2021 to 2030

3.4 Oncology Devices Market Outlook by Application, $ Million, 2021 to 2030

3.5 Oncology Devices Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Oncology Devices Industry

4.2 Key Market Trends in Oncology Devices Industry

4.3 Potential Opportunities in Oncology Devices Industry

4.4 Key Challenges in Oncology Devices Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Oncology Devices Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Oncology Devices Market Outlook by Segments

7.1 Oncology Devices Market Outlook by Segments, $ Million, 2021- 2030

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

8 North America Oncology Devices Market Analysis and Outlook To 2030

8.1 Introduction to North America Oncology Devices Markets in 2024

8.2 North America Oncology Devices Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Oncology Devices Market size Outlook by Segments, 2021-2030

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

9 Europe Oncology Devices Market Analysis and Outlook To 2030

9.1 Introduction to Europe Oncology Devices Markets in 2024

9.2 Europe Oncology Devices Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Oncology Devices Market Size Outlook by Segments, 2021-2030

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

10 Asia Pacific Oncology Devices Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Oncology Devices Markets in 2024

10.2 Asia Pacific Oncology Devices Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Oncology Devices Market size Outlook by Segments, 2021-2030

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

11 South America Oncology Devices Market Analysis and Outlook To 2030

11.1 Introduction to South America Oncology Devices Markets in 2024

11.2 South America Oncology Devices Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Oncology Devices Market size Outlook by Segments, 2021-2030

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

12 Middle East and Africa Oncology Devices Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Oncology Devices Markets in 2024

12.2 Middle East and Africa Oncology Devices Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Oncology Devices Market size Outlook by Segments, 2021-2030

By Device

Brachytherapy Devices

Endoscopic Devices

By Therapy

Chemotherapy

Hormone Therapy

Biotherapy/Immunotherapy

Radiation Therapy

By End-User

Hospitals

Cancer Research Institutes

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Accuray Inc

Alpha Tau Medical

Becton Dickinson and Company

Biogenex Laboratories

Brainlab

Canon Medical Systems Corp

Eckert & Ziegler BEBIG GmbH

Elekta AB

GE Healthcare

Hologic Inc

IBA AG

IBA Group

IsoRay

Medtronic PLC

Mevion Medical Systems

Mirada Medical Ltd

Nanobiotix

Navidea Biopharmaceuticals Inc

Oncura Inc

PerkinElmer

Philips Healthcare

RaySearch Laboratories

RefleXion Medical

Roche Diagnostics

Siemens Healthineers

Theragenics Corp

Varian Medical Systems Inc

ViewRay Inc

Vision RT

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise