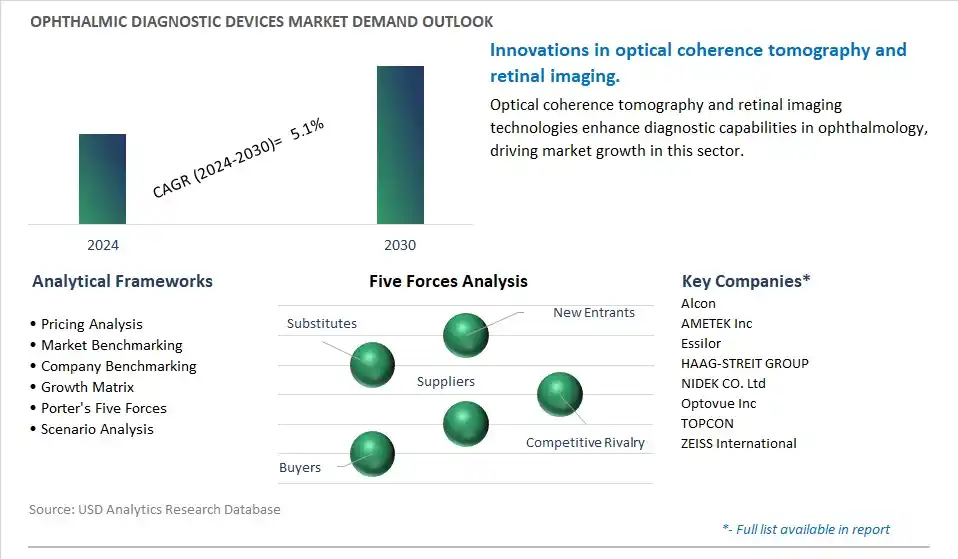

Ophthalmic Diagnostic Devices Market is estimated to increase at a growth rate of 5.1% CAGR over the forecast period from 2024 to 2030.

The global Ophthalmic Diagnostic Devices Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Product (Optical Coherence Tomography, Aberrometer & Topography Systems, Fundus Camera, Ophthalmic Ultrasound, Others), By End-User (Hospitals, Ophthalmic Clinics, Others).

An Introduction to Ophthalmic Diagnostic Devices Market in 2024

Ophthalmic Diagnostic Devices play a critical role in the early detection, diagnosis, and monitoring of various eye conditions and vision disorders, driving significant growth and innovation in the Ophthalmic Diagnostic Devices Market in 2024. With the global burden of eye diseases on the rise, fueled by aging populations and lifestyle factors, there is a growing demand for advanced diagnostic tools capable of assessing ocular health and visual function with precision and accuracy. The market is characterized by a diverse array of diagnostic devices, including slit lamps, fundus cameras, optical coherence tomography (OCT) systems, and visual field analyzers, offering comprehensive assessments of anterior and posterior segment structures, retinal morphology, and visual field integrity. Moreover, there is increasing adoption of handheld and portable diagnostic devices, teleophthalmology solutions, and AI-enabled imaging technologies, enabling remote monitoring, teleconsultation, and decentralized eye care delivery models. As advancements in ophthalmic imaging, biometry, and artificial intelligence continue to drive innovation, the Ophthalmic Diagnostic Devices Market holds promise for revolutionizing the diagnosis and management of eye diseases and vision disorders, facilitating early intervention and preserving sight for patients worldwide.

Ophthalmic Diagnostic Devices Market Competitive Landscape

The global Ophthalmic Diagnostic Devices Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Ophthalmic Diagnostic Devices Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Ophthalmic Diagnostic Devices Industry include- Alcon, AMETEK Inc, Essilor, HAAG-STREIT GROUP, NIDEK CO. Ltd, Optovue Inc, TOPCON, ZEISS International.

Ophthalmic Diagnostic Devices Market Trend: Integration of Artificial Intelligence (AI) and Machine Learning

In the Ophthalmic Diagnostic Devices market, a prominent trend is the integration of artificial intelligence (AI) and machine learning algorithms into diagnostic devices. These technologies enable automated image analysis, pattern recognition, and disease detection, enhancing the accuracy and efficiency of diagnostic procedures. AI-powered diagnostic devices can assist ophthalmologists in detecting early signs of eye diseases, such as diabetic retinopathy and age-related macular degeneration, leading to timely interventions and improved patient outcomes. Moreover, the incorporation of AI algorithms into diagnostic devices facilitates teleophthalmology initiatives, allowing for remote screening and diagnosis, particularly in underserved regions with limited access to eye care specialists.

Ophthalmic Diagnostic Devices Market Driver: Aging Population and Rising Prevalence of Eye Disorders

The primary market driver for Ophthalmic Diagnostic Devices is the aging population and the associated increase in the prevalence of eye disorders. As the global population ages, the incidence of age-related eye diseases, such as cataracts, glaucoma, and macular degeneration, is rising significantly, driving the demand for advanced diagnostic tools for early detection and management. Ophthalmic diagnostic devices play a crucial role in the early diagnosis, monitoring, and treatment planning of various eye conditions, supporting ophthalmologists in delivering personalized and timely care to patients. The growing burden of eye diseases worldwide, coupled with the need for comprehensive eye health assessments, fuels market demand for innovative diagnostic solutions that enable efficient and accurate diagnosis of ophthalmic conditions.

Ophthalmic Diagnostic Devices Market Opportunity: Development of Portable and Point-of-Care Diagnostic Devices

An emerging opportunity in the Ophthalmic Diagnostic Devices market lies in the development of portable and point-of-care diagnostic devices that offer convenience, accessibility, and cost-effectiveness. Portable diagnostic devices enable eye screenings and examinations to be conducted outside traditional clinical settings, such as in community health centers, mobile clinics, and remote areas with limited healthcare infrastructure. These devices empower primary care providers, optometrists, and community health workers to perform basic eye assessments, detect common eye conditions, and refer patients for further evaluation or treatment as needed. Moreover, point-of-care diagnostic devices offer rapid and on-the-spot results, reducing patient waiting times and facilitating timely interventions. By leveraging technological advancements in miniaturization, connectivity, and battery efficiency, manufacturers can develop compact and user-friendly ophthalmic diagnostic devices that expand access to eye care services, particularly in resource-limited settings, rural areas, and underserved populations, thereby addressing unmet needs and improving eye health outcomes globally.

Ophthalmic Diagnostic Devices Market Share Analysis: Optical Coherence Tomography (OCT) for Ophthalmic Clinics is the fastest growing market segment over the forecast period to 2030

Among the various ophthalmic diagnostic devices, Optical Coherence Tomography (OCT) stands out as the fastest-growing segment, particularly in ophthalmic clinics. This growth is driven by the widespread adoption of OCT technology due to its non-invasive and high-resolution imaging capabilities, which enable detailed visualization of the various layers of the eye. OCT allows clinicians to assess retinal thickness, detect abnormalities in the macula and optic nerve, and monitor disease progression in conditions such as macular degeneration, diabetic retinopathy, and glaucoma. Furthermore, advancements in OCT technology, such as spectral-domain OCT and swept-source OCT, have further improved image resolution, scan speed, and depth penetration, enhancing diagnostic accuracy and clinical utility. In ophthalmic clinics, OCT has become an indispensable tool for comprehensive eye examinations, aiding in early detection, diagnosis, and management of a wide range of ocular diseases. Moreover, the growing prevalence of age-related eye disorders and the increasing demand for advanced diagnostic techniques contribute to the continued expansion of OCT usage in ophthalmic clinics. As the field of ophthalmic imaging continues to evolve and innovate, OCT is expected to maintain its position as a cornerstone technology in ophthalmic diagnostics, driving improved patient care and outcomes in the management of ocular conditions.

Ophthalmic Diagnostic Devices Market Segmentation

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Ophthalmic Diagnostic Devices Companies

Alcon

AMETEK Inc

Essilor

HAAG-STREIT GROUP

NIDEK CO. Ltd

Optovue Inc

TOPCON

ZEISS International

* List not Exhaustive

Reasons to Buy the Ophthalmic Diagnostic Devices Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Ophthalmic Diagnostic Devices Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Ophthalmic Diagnostic Devices Industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Ophthalmic Diagnostic Devices Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Ophthalmic Diagnostic Devices Market Size Outlook, $ Million, 2021 to 2030

3.2 Ophthalmic Diagnostic Devices Market Outlook by Type, $ Million, 2021 to 2030

3.3 Ophthalmic Diagnostic Devices Market Outlook by Product, $ Million, 2021 to 2030

3.4 Ophthalmic Diagnostic Devices Market Outlook by Application, $ Million, 2021 to 2030

3.5 Ophthalmic Diagnostic Devices Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Ophthalmic Diagnostic Devices Industry

4.2 Key Market Trends in Ophthalmic Diagnostic Devices Industry

4.3 Potential Opportunities in Ophthalmic Diagnostic Devices Industry

4.4 Key Challenges in Ophthalmic Diagnostic Devices Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Ophthalmic Diagnostic Devices Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Ophthalmic Diagnostic Devices Market Outlook by Segments

7.1 Ophthalmic Diagnostic Devices Market Outlook by Segments, $ Million, 2021- 2030

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

8 North America Ophthalmic Diagnostic Devices Market Analysis and Outlook To 2030

8.1 Introduction to North America Ophthalmic Diagnostic Devices Markets in 2024

8.2 North America Ophthalmic Diagnostic Devices Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Ophthalmic Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

9 Europe Ophthalmic Diagnostic Devices Market Analysis and Outlook To 2030

9.1 Introduction to Europe Ophthalmic Diagnostic Devices Markets in 2024

9.2 Europe Ophthalmic Diagnostic Devices Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Ophthalmic Diagnostic Devices Market Size Outlook by Segments, 2021-2030

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

10 Asia Pacific Ophthalmic Diagnostic Devices Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Ophthalmic Diagnostic Devices Markets in 2024

10.2 Asia Pacific Ophthalmic Diagnostic Devices Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Ophthalmic Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

11 South America Ophthalmic Diagnostic Devices Market Analysis and Outlook To 2030

11.1 Introduction to South America Ophthalmic Diagnostic Devices Markets in 2024

11.2 South America Ophthalmic Diagnostic Devices Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Ophthalmic Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

12 Middle East and Africa Ophthalmic Diagnostic Devices Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Ophthalmic Diagnostic Devices Markets in 2024

12.2 Middle East and Africa Ophthalmic Diagnostic Devices Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Ophthalmic Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Optical Coherence Tomography

Aberrometer & Topography Systems

Fundus Camera

Ophthalmic Ultrasound

Others

By End-User

Hospitals

Ophthalmic Clinics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Alcon

AMETEK Inc

Essilor

HAAG-STREIT GROUP

NIDEK CO. Ltd

Optovue Inc

TOPCON

ZEISS International

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise