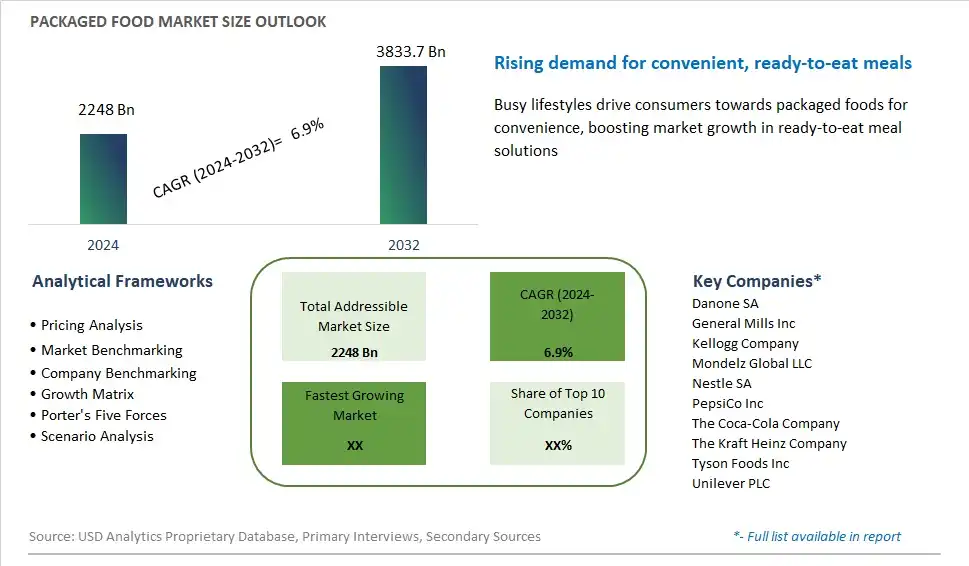

Global Packaged Food Market Size is valued at $2,248 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.9% to reach $3,833.7 Billion by 2032.

The global Packaged Food Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Dairy Products, Confectionery, Beverage, Bakery, Snacks, Meat, Poultry and Seafood, Breakfast Cereals, Ready Meals, Others), By Packaging (Plastic, Tetra Pack, Metal Cans, Others), By Distribution Channel (Supermarket/Hypermarket, Convenience Stores, Online Retail Stores, Others)

An Introduction to Packaged Food Market

The packaged foods market in 2024 is witnessing robust growth, driven by increasing consumer demand for convenience, variety, and long shelf life. This market encompasses a wide range of products, including canned goods, frozen meals, snacks, and pantry staples, catering to diverse dietary preferences and lifestyles. The trend towards convenience and ready-to-eat solutions has significantly boosted demand for packaged foods, especially among busy professionals and families. Health-conscious consumers are also seeking healthier packaged food options, such as those with natural ingredients, minimal processing, and fortified nutrients. Innovations in packaging technology, including eco-friendly and sustainable materials, are enhancing the appeal and accessibility of packaged foods. As consumers continue to prioritize convenience, nutrition, and sustainability, the packaged foods market is set for sustained growth and innovation, offering a wide array of products that meet evolving consumer needs.

Packaged Food Competitive Landscape

The market report analyses the leading companies in the industry including Danone SA, General Mills Inc, Kellogg Company, Mondelz Global LLC, Nestle SA, PepsiCo Inc, The Coca-Cola Company, The Kraft Heinz Company, Tyson Foods Inc, Unilever PLC, and Others.

Packaged Food Market Dynamics

Packaged Foods Market Trend: Shift Towards Convenience and Healthy Eating

Packaged foods are witnessing a prominent trend towards convenience and healthy eating, driven by evolving consumer lifestyles and dietary preferences. This trend reflects a growing demand for ready-to-eat and easy-to-prepare meals and snacks that offer convenience without compromising on quality or nutrition. Consumers are increasingly seeking packaged foods that are minimally processed, free from artificial additives, and enriched with functional ingredients to support health and well-being. As busy schedules and on-the-go lifestyles become more prevalent, the market for packaged foods is evolving to meet the needs of health-conscious consumers seeking convenient yet nutritious options.

Market Driver: Changing Consumer Preferences and Busy Lifestyles

The rapid expansion of the packaged foods market is primarily driven by changing consumer preferences and the prevalence of busy lifestyles. With hectic schedules and limited time for meal preparation, consumers are turning to packaged foods as convenient solutions for quick and easy meals and snacks. Packaged foods offer the convenience of on-the-go consumption, allowing consumers to enjoy satisfying meals and snacks without the need for extensive cooking or preparation. Moreover, the increasing demand for healthier options, including organic, natural, and functional foods, is driving innovation in the packaged foods sector, as brands seek to cater to health-conscious consumers seeking convenient yet nutritious options.

Market Opportunity: Innovation in Product Formulation and Packaging

One significant opportunity within the packaged foods market lies in innovation in product formulation and packaging to meet the evolving needs and preferences of consumers. Brands can differentiate themselves by offering a wider range of healthier options, including plant-based, gluten-free, and low-sodium alternatives, to cater to diverse dietary preferences and restrictions. Additionally, incorporating functional ingredients such as probiotics, antioxidants, and superfoods can enhance the nutritional value and health benefits of packaged foods, appealing to health-conscious consumers seeking functional benefits. Furthermore, exploring innovative packaging formats such as portion-controlled packs, resealable pouches, and eco-friendly materials can enhance convenience, freshness, and sustainability, providing added value to consumers and driving brand loyalty. As the market for packaged foods continues to evolve, brands that prioritize innovation, differentiation, and consumer-centric strategies are well-positioned to capitalize on the growing demand for convenient, nutritious, and sustainable food options.

Packaged Foods Market Share Analysis: Tetra Pack market is poised to register the fastest growth rae over the forecast period to 2032

In the Packaged Foods Market by packaging, the Tetra Pack segment is the fastest-growing. This rapid growth can be attributed to several factors. Firstly, Tetra Pack packaging offers several advantages over other packaging materials. It is lightweight, which reduces transportation costs and carbon emissions, making it a more environmentally friendly option. Additionally, Tetra Pack is convenient and versatile, allowing for easy storage, handling, and pouring of packaged foods such as juices, soups, sauces, and dairy products. Its ability to preserve the freshness and flavor of the contents for an extended period without the need for refrigeration makes it popular among consumers seeking convenience and shelf-stable options. Furthermore, Tetra Pack's innovation in sustainable packaging solutions, such as using renewable materials and reducing plastic usage, aligns with the growing consumer demand for eco-friendly and socially responsible products. With its practicality, sustainability, and consumer appeal, the Tetra Pack segment in the packaged foods market is poised for continued expansion in the coming years.

Packaged Foods Market Share Analysis: Supermarket/Hypermarket held the dominant market share in 2024

The Supermarket/Hypermarket segment is the largest in the Packaged Foods Market by distribution channel. This dominance is primarily attributed to several factors. Firstly, supermarkets and hypermarkets offer various packaged foods under one roof, providing consumers with convenience and choice. Their extensive shelf space and strategic placement within shopping centers attract a large number of shoppers, resulting in high visibility and accessibility for packaged food products. Additionally, supermarkets and hypermarkets often carry a diverse range of packaged foods, including both branded and private-label options, catering to different consumer preferences and budgets. Further, the trust and reliability of established supermarkets and hypermarket chains further contribute to their popularity as preferred shopping destinations for packaged foods. Furthermore, the ability to inspect and select products in person, combined with promotional offers and discounts, enhances the shopping experience and encourages impulse purchases. With its wide reach, diverse offerings, and consumer trust, the Supermarket/Hypermarket segment maintains its position as the largest in the packaged foods market.

Packaged Food Market Segmentation

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Packaged Food Companies Profiled in the Study

Danone SA

General Mills Inc

Kellogg Company

Mondelz Global LLC

Nestle SA

PepsiCo Inc

The Coca-Cola Company

The Kraft Heinz Company

Tyson Foods Inc

Unilever PLC

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Packaged Food Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Packaged Food Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Packaged Food Market Share by Company, 2023

4.1.2. Product Offerings of Leading Packaged Food Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Packaged Food Market Drivers

6.2. Packaged Food Market Challenges

6.6. Packaged Food Market Opportunities

6.4. Packaged Food Market Trends

Chapter 7. Global Packaged Food Market Outlook Trends

7.1. Global Packaged Food Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Packaged Food Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Packaged Food Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Chapter 8. Global Packaged Food Regional Analysis and Outlook

8.1. Global Packaged Food Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Packaged Food Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Packaged Food Regional Analysis and Outlook

8.2.2. Canada Packaged Food Regional Analysis and Outlook

8.2.3. Mexico Packaged Food Regional Analysis and Outlook

8.3. Europe Packaged Food Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Packaged Food Regional Analysis and Outlook

8.3.2. France Packaged Food Regional Analysis and Outlook

8.3.3. United Kingdom Packaged Food Regional Analysis and Outlook

8.3.4. Spain Packaged Food Regional Analysis and Outlook

8.3.5. Italy Packaged Food Regional Analysis and Outlook

8.3.6. Russia Packaged Food Regional Analysis and Outlook

8.3.7. Rest of Europe Packaged Food Regional Analysis and Outlook

8.4. Asia Pacific Packaged Food Revenue (USD Million) by Country (2021-2032)

8.4.1. China Packaged Food Regional Analysis and Outlook

8.4.2. Japan Packaged Food Regional Analysis and Outlook

8.4.3. India Packaged Food Regional Analysis and Outlook

8.4.4. South Korea Packaged Food Regional Analysis and Outlook

8.4.5. Australia Packaged Food Regional Analysis and Outlook

8.4.6. South East Asia Packaged Food Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Packaged Food Regional Analysis and Outlook

8.5. South America Packaged Food Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Packaged Food Regional Analysis and Outlook

8.5.2. Argentina Packaged Food Regional Analysis and Outlook

8.5.3. Rest of South America Packaged Food Regional Analysis and Outlook

8.6. Middle East and Africa Packaged Food Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Packaged Food Regional Analysis and Outlook

8.6.2. Africa Packaged Food Regional Analysis and Outlook

Chapter 9. North America Packaged Food Analysis and Outlook

9.1. North America Packaged Food Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Packaged Food Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Packaged Food Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Packaged Food Revenue (USD Million) by Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Chapter 10. Europe Packaged Food Analysis and Outlook

10.1. Europe Packaged Food Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Packaged Food Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Packaged Food Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Packaged Food Revenue (USD Million) by Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Chapter 11. Asia Pacific Packaged Food Analysis and Outlook

11.1. Asia Pacific Packaged Food Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Packaged Food Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Packaged Food Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Packaged Food Revenue (USD Million) by Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Chapter 12. South America Packaged Food Analysis and Outlook

12.1. South America Packaged Food Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Packaged Food Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Packaged Food Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Packaged Food Revenue (USD Million) by Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Chapter 13. Middle East and Africa Packaged Food Analysis and Outlook

13.1. Middle East and Africa Packaged Food Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Packaged Food Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Packaged Food Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Packaged Food Revenue (USD Million) by Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Chapter 14. Packaged Food Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Danone SA

General Mills Inc

Kellogg Company

Mondelz Global LLC

Nestle SA

PepsiCo Inc

The Coca-Cola Company

The Kraft Heinz Company

Tyson Foods Inc

Unilever PLC

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Packaged Food Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Packaged Food Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Packaged Food Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Packaged Food Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Packaged Food Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Packaged Food Market Share (%) By Regions (2021-2032)

Table 12 North America Packaged Food Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Packaged Food Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Packaged Food Revenue (USD Million) By Country (2021-2032)

Table 15 South America Packaged Food Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Packaged Food Revenue (USD Million) By Region (2021-2032)

Table 17 North America Packaged Food Revenue (USD Million) By Type (2021-2032)

Table 18 North America Packaged Food Revenue (USD Million) By Application (2021-2032)

Table 19 North America Packaged Food Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Packaged Food Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Packaged Food Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Packaged Food Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Packaged Food Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Packaged Food Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Packaged Food Revenue (USD Million) By Product (2021-2032)

Table 26 South America Packaged Food Revenue (USD Million) By Type (2021-2032)

Table 27 South America Packaged Food Revenue (USD Million) By Application (2021-2032)

Table 28 South America Packaged Food Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Packaged Food Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Packaged Food Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Packaged Food Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Packaged Food Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Packaged Food Market Share (%) By Regions (2023)

Figure 6. North America Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 12. France Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 12. China Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 14. India Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Packaged Food Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Packaged Food Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Packaged Food Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Packaged Food Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Packaged Food Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Packaged Food Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Packaged Food Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Packaged Food Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Packaged Food Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Packaged Food Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Packaged Food Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Packaged Food Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Packaged Food Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Packaged Food Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Packaged Food Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Packaged Food Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Packaged Food Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Packaged Food Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Packaged Food Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Packaged Food Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Packaged Food Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Packaged Food Revenue (USD Million) By Product (2021-2032)

By Product

Dairy Products

Confectionery

Beverage

Bakery

Snacks

Meat

Poultry and Seafood

Breakfast Cereals

Ready Meals

Others

By Packaging

Plastic

Tetra Pack

Metal Cans

Others

By Distribution Channel

Supermarket/Hypermarket

Convenience Stores

Online Retail Stores

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)