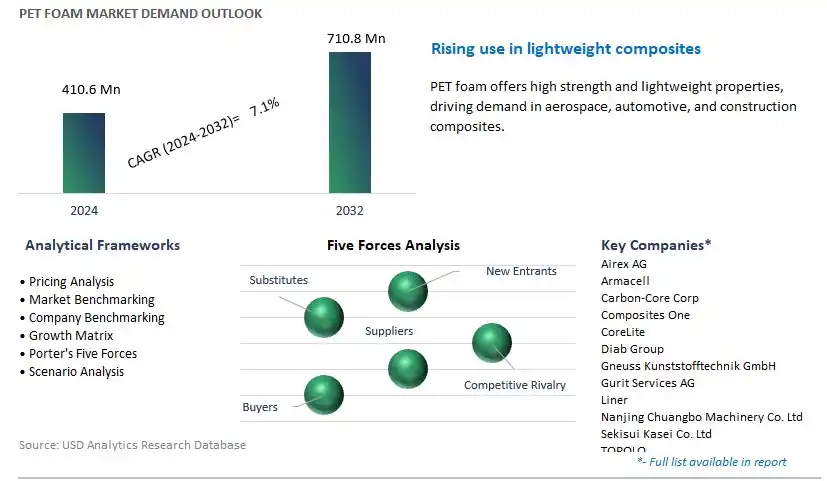

Global PET Foam Market Size is valued at $410.6 Million in 2024 and is forecast to register a growth rate (CAGR) of 7.1% to reach $710.8 Million by 2032.

The global PET Foam Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Raw Material (Virgin PET, Recycled PET), By Grade (Low-density, High-density), By Application (Wind Energy, Transportation, Marine, Building & Construction, Packaging, Others).

An Introduction to PET Foam Market in 2024

PET (polyethylene terephthalate) foam is a lightweight and recyclable foam material made from PET resin, widely used as a core material in sandwich structures for applications such as aerospace, automotive, marine, and wind energy. In 2024, the market for PET foam s to grow as industries seek lightweight and high-performance materials to reduce fuel consumption, increase energy efficiency, and improve sustainability in manufacturing processes. PET foam offers advantages such as high strength-to-weight ratio, excellent fatigue resistance, thermal stability, and resistance to moisture and chemicals. These properties make it ideal for use as a core material in composite structures, sandwich panels, and laminates, providing structural support, insulation, and impact resistance. PET foam is used in applications such as aircraft interiors, automotive components, wind turbine blades, and boat hulls, where lightweight construction and superior mechanical properties are essential. The demand for PET foam is driven by factors such as the growth of the aerospace and automotive industries, increasing demand for renewable energy sources, and the emphasis on lightweighting and sustainability in product design and manufacturing. Market trends include the development of bio-based and recyclable PET foam formulations, the optimization of foam structures and properties for specific applications and performance requirements, and the adoption of advanced manufacturing techniques such as continuous production processes and additive manufacturing for cost-effective and customized solutions.

PET Foam Market Competitive Landscape

The market report analyses the leading companies in the industry including Airex AG, Armacell, Carbon-Core Corp, Composites One, CoreLite, Diab Group, Gneuss Kunststofftechnik GmbH, Gurit Services AG, Liner, Nanjing Chuangbo Machinery Co. Ltd, Sekisui Kasei Co. Ltd, TOPOLO, USEON Technology Ltd, and others.

PET Foam Market Dynamics

Market Trend: Growing Demand for Lightweight and Sustainable Materials

A prominent market trend in PET foam is the growing demand for lightweight and sustainable materials across various industries. As industries seek to reduce the weight of their products for improved fuel efficiency, performance, and environmental sustainability, there is a rising need for lightweight materials such as PET foam. PET foam offers advantages such as high strength-to-weight ratio, excellent thermal insulation properties, and recyclability, making it suitable for applications in aerospace, automotive, marine, wind energy, and construction sectors. This trend towards lightweight and sustainable materials reflects the industry's commitment to innovation and sustainability in product development and manufacturing processes.

Market Driver: Increased Adoption in Composite Manufacturing

A key driver for the PET foam market is the increased adoption of PET foam in composite manufacturing processes. With advancements in composite materials technology and growing demand for high-performance composites, PET foam serves as a core material in sandwich panel constructions for various applications. PET foam cores provide structural support, insulation, and impact resistance while reducing overall weight in composite structures such as boat hulls, wind turbine blades, automotive parts, and building panels. The expanding use of composites in lightweight and high-strength applications drives the demand for PET foam as a core material in composite manufacturing.

Market Opportunity: Development of Advanced PET Foam Formulations

A significant market opportunity for PET foam lies in the development of advanced formulations tailored to meet specific application needs and performance requirements. Manufacturers have the opportunity to innovate and formulate PET foam with enhanced properties such as improved mechanical strength, thermal stability, fire resistance, and compatibility with different resin systems. Additionally, there is potential to offer PET foam with customized densities, thicknesses, and surface finishes to address the diverse needs of different industries and applications. By leveraging the opportunity presented by advanced PET foam formulations, suppliers can differentiate their products, capture market share in specialized segments, and provide tailored solutions for customers seeking lightweight and high-performance materials for their projects.

PET Foam Market Share Analysis: Virgin PET generated the highest revenue in 2024

In the PET Foam Market, the largest segment is Virgin PET. The large revenue share is primarily driven by the widespread use and demand for virgin PET foam across various industries. Virgin PET foam offers superior mechanical properties, thermal stability, and processing advantages compared to recycled PET foam. It is commonly used in applications where stringent performance requirements and quality standards are essential, such as aerospace, automotive, marine, and wind energy sectors. Virgin PET foam exhibits excellent strength-to-weight ratio, dimensional stability, and resistance to moisture absorption, making it suitable for structural and lightweighting applications in composite materials. Moreover, virgin PET foam is preferred for its consistency in material properties and purity, ensuring reliable performance and ease of processing during manufacturing processes. Additionally, the growing demand for sustainable and eco-friendly materials in various industries further drives the adoption of virgin PET foam, as it can be recycled and reused to minimize environmental impact. Furthermore, advancements in PET foam manufacturing technologies and material formulations continue to expand the application possibilities and market penetration of virgin PET foam, reinforcing its position as the largest segment in the PET Foam Market. Hence, with its superior properties, reliability, and versatility, Virgin PET foam is the largest and most significant segment in the PET Foam Market.

PET Foam Market Share Analysis: Low-Density Grade is poised to register the fastest CAGR over the forecast period

In the PET Foam Market, the fastest-growing segment is the Low-Density Grade. The market growth is driven by increasing demand for low-density PET foam across various industries. Low-density PET foam offers potential advantages over high-density foam, including lightweight properties, enhanced flexibility, and improved impact resistance. These characteristics make it particularly suitable for applications where weight reduction, insulation, and cushioning properties are essential, such as in the transportation, marine, and wind energy sectors. Additionally, the low-density grade of PET foam provides excellent buoyancy and flotation capabilities, making it ideal for marine applications such as boat hulls, decks, and buoys. Moreover, the construction industry is increasingly adopting low-density PET foam for insulation panels, roofing materials, and structural components due to its thermal insulation properties and ease of installation. Furthermore, advancements in manufacturing processes and material formulations have led to the development of high-performance low-density PET foams with improved mechanical properties and processing efficiency, further driving their adoption across various end-use industries. Hence, with its versatility, lightweight properties, and expanding application opportunities, the Low-Density Grade is the fastest-growing segment in the PET Foam Market.

PET Foam Market Share Analysis: Building & Construction generated the highest revenue in 2024

In the PET Foam Market, the largest segment is Building & Construction. The large revenue share is primarily driven by the extensive use and demand for PET foam in building and construction applications. PET foam offers a range of properties that make it highly suitable for various construction applications, including insulation panels, roofing materials, composite panels, and structural components. PET foam provides excellent thermal insulation properties, helping to improve energy efficiency and reduce heating and cooling costs in buildings. Additionally, PET foam is lightweight yet strong, contributing to the structural integrity of construction elements while minimizing overall weight. Moreover, PET foam is resistant to moisture, chemicals, and environmental degradation, ensuring long-term durability and performance in harsh weather conditions. Furthermore, the growing emphasis on sustainable and eco-friendly construction practices drives the adoption of PET foam, as it can be recycled and reused to minimize environmental impact. The versatility, performance, and sustainability of PET foam make it a preferred choice for architects, builders, and contractors in the construction industry, thereby driving its dominance as the largest segment in the PET Foam Market.

PET Foam Market

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

PET Foam Companies Profiled in the Study

Airex AG

Armacell

Carbon-Core Corp

Composites One

CoreLite

Diab Group

Gneuss Kunststofftechnik GmbH

Gurit Services AG

Liner

Nanjing Chuangbo Machinery Co. Ltd

Sekisui Kasei Co. Ltd

TOPOLO

USEON Technology Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 PET Foam Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global PET Foam Market Size Outlook, $ Million, 2021 to 2032

3.2 PET Foam Market Outlook by Type, $ Million, 2021 to 2032

3.3 PET Foam Market Outlook by Product, $ Million, 2021 to 2032

3.4 PET Foam Market Outlook by Application, $ Million, 2021 to 2032

3.5 PET Foam Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of PET Foam Industry

4.2 Key Market Trends in PET Foam Industry

4.3 Potential Opportunities in PET Foam Industry

4.4 Key Challenges in PET Foam Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global PET Foam Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global PET Foam Market Outlook by Segments

7.1 PET Foam Market Outlook by Segments, $ Million, 2021- 2032

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

8 North America PET Foam Market Analysis and Outlook To 2032

8.1 Introduction to North America PET Foam Markets in 2024

8.2 North America PET Foam Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America PET Foam Market size Outlook by Segments, 2021-2032

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

9 Europe PET Foam Market Analysis and Outlook To 2032

9.1 Introduction to Europe PET Foam Markets in 2024

9.2 Europe PET Foam Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe PET Foam Market Size Outlook by Segments, 2021-2032

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

10 Asia Pacific PET Foam Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific PET Foam Markets in 2024

10.2 Asia Pacific PET Foam Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific PET Foam Market size Outlook by Segments, 2021-2032

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

11 South America PET Foam Market Analysis and Outlook To 2032

11.1 Introduction to South America PET Foam Markets in 2024

11.2 South America PET Foam Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America PET Foam Market size Outlook by Segments, 2021-2032

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

12 Middle East and Africa PET Foam Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa PET Foam Markets in 2024

12.2 Middle East and Africa PET Foam Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa PET Foam Market size Outlook by Segments, 2021-2032

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Airex AG

Armacell

Carbon-Core Corp

Composites One

CoreLite

Diab Group

Gneuss Kunststofftechnik GmbH

Gurit Services AG

Liner

Nanjing Chuangbo Machinery Co. Ltd

Sekisui Kasei Co. Ltd

TOPOLO

USEON Technology Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Raw Material

Virgin PET

Recycled PET

By Grade

Low-density

High-density

By Application

Wind Energy

Transportation

Marine

Building & Construction

Packaging

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)