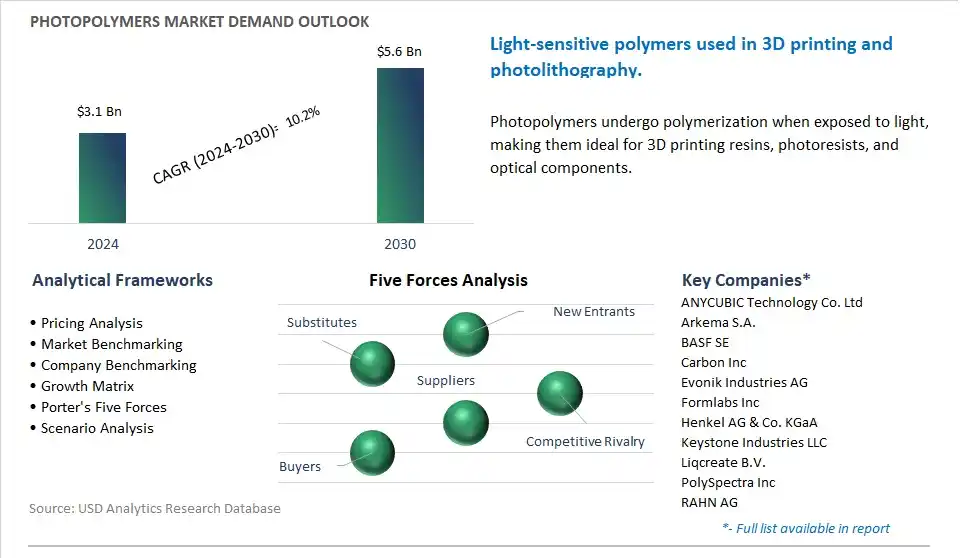

The global Photopolymers Market is poised to register a 10.2% CAGR from $3.1 Billion in 2024 to $5.6 Billion in 2030.

The global Photopolymers Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Performance (Low Performance, Mid Performance, High Performance), By Technology (Stereolithography (SLA), Digital Light Processing (DLP), Continuous Digital Light Processing (cDLP)), By Application (Dental, Medical, Audiology, Jewelry, Automotive, Prototyping, Others).

An Introduction to Global Photopolymers Market in 2024

The key trend shaping the future of the photopolymers industry is the increasing adoption of additive manufacturing (AM) technologies such as stereolithography (SLA), digital light processing (DLP), and continuous liquid interface production (CLIP) for rapid prototyping, tooling, and production of complex parts and components across various industries. Photopolymers are light-sensitive materials that undergo polymerization when exposed to ultraviolet (UV) light, forming three-dimensional (3D) structures layer by layer in AM processes. With the growing demand for customized, on-demand manufacturing solutions and the need for faster time-to-market, there is a rising interest in photopolymer-based AM technologies that offer high-resolution, surface finish, and material properties suitable for a wide range of applications. Manufacturers are investing in the development of advanced photopolymer formulations, curing methods, and post-processing techniques to improve mechanical strength, thermal stability, and functional performance of printed parts, meeting the diverse needs and requirements of end-users in industries such as aerospace, automotive, healthcare, and consumer goods. Additionally, there is a trend towards the use of bio-based and sustainable photopolymers derived from renewable feedstocks such as plant oils, starches, or proteins, addressing concerns over environmental impact and resource depletion. Furthermore, with the integration of digital design tools, simulation software, and automated manufacturing workflows, there is a growing interest in digital manufacturing platforms that enable seamless design iteration, process optimization, and scalability in photopolymer-based AM processes. As industries continue to embrace digitalization and additive manufacturing for product innovation and supply chain resilience, the demand for photopolymers is expected to grow, driving market expansion and technological innovation in the 3D printing and AM industries.

Photopolymers Market Competitive Landscape

The market report analyses the leading companies in the industry including ANYCUBIC Technology Co. Ltd, Arkema S.A., BASF SE, Carbon Inc, Evonik Industries AG, Formlabs Inc, Henkel AG & Co. KGaA, Keystone Industries LLC, Liqcreate B.V., PolySpectra Inc, RAHN AG, Stratasys Ltd.

Photopolymers Market Dynamics

Photopolymers Market Trend: Growing Demand for 3D Printing Applications

One prominent trend in the photopolymers market is the growing demand for 3D printing applications across various industries. As additive manufacturing continues to gain traction for prototyping, product development, and manufacturing processes, there is an increasing need for photopolymer resins that offer high precision, speed, and versatility. Manufacturers are innovating to develop photopolymers tailored to meet the specific requirements of 3D printing technologies, such as stereolithography (SLA), digital light processing (DLP), and inkjet-based systems, driving market growth in the additive manufacturing sector.

Photopolymers Market Driver: Advancements in Material Science and Technology

A significant driver propelling the photopolymers market is the continuous advancements in material science and technology. As researchers and engineers explore new formulations, additives, and curing methods, photopolymer resins are becoming more diverse, customizable, and performance-driven. Innovations in UV-curable formulations, biocompatible materials, and functional additives are expanding the application scope of photopolymers across industries such as healthcare, automotive, aerospace, and consumer goods, driving demand for these materials worldwide.

Photopolymers Market Opportunity: Expansion in Healthcare and Medical Device Applications

An opportunity for the photopolymers market lies in the expansion of healthcare and medical device applications. With the increasing demand for personalized healthcare solutions, minimally invasive procedures, and patient-specific medical devices, there is a growing need for biocompatible photopolymers suitable for medical-grade 3D printing applications. Manufacturers focusing on developing photopolymers with biocompatibility, sterilizability, and regulatory compliance stand to capitalize on the burgeoning healthcare market, providing innovative solutions for surgical guides, dental implants, prosthetics, tissue engineering, and drug delivery systems.

Photopolymers Market Share Analysis: Low Performance generated the highest revenue in 2024

The largest segment in the Photopolymers Market is the Low Performance segment. low-performance photopolymers are widely used in various applications where cost-effectiveness and ease of processing are prioritized over high-performance characteristics. These photopolymers often have simpler formulations and lower material costs compared to mid-performance and high-performance alternatives, making them attractive for applications where cost considerations are critical, such as in signage, packaging, and consumer goods. Additionally, low-performance photopolymers exhibit relatively lower mechanical properties, such as tensile strength and impact resistance, compared to mid-performance and high-performance variants. However, they still offer sufficient performance for many applications where moderate durability and functional requirements are sufficient. Further, low-performance photopolymers are commonly used in entry-level 3D printing and rapid prototyping applications, where affordability and accessibility are essential considerations for users. Furthermore, the versatility and ease of processing of low-performance photopolymers make them suitable for a wide range of printing and coating processes, including screen printing, flexography, and inkjet printing, further contributing to their widespread adoption. Over the forecast period, the combination of cost-effectiveness, versatility, and suitability for various applications positions the Low Performance segment as the largest in the Photopolymers Market.

Photopolymers Market Share Analysis: Digital Light Processing (DLP) technology segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Photopolymers Market is the Digital Light Processing (DLP) technology segment. Diverse factors contribute to the rapid growth of DLP technology in the photopolymers market. DLP technology offers potential advantages over traditional photopolymerization methods, such as stereolithography (SLA). DLP printers utilize a digital light projector to expose entire layers of photopolymer resin simultaneously, resulting in faster build times compared to sequential layer-by-layer exposure in SLA systems. This parallel exposure capability enables DLP printers to achieve higher throughput and productivity, making them well-suited for applications requiring rapid prototyping, small-batch production, and on-demand manufacturing. Additionally, DLP technology allows for precise control over exposure parameters, such as light intensity and exposure time, resulting in enhanced printing accuracy and surface finish. Further, advancements in DLP hardware and software, including higher resolution projectors, faster curing resins, and improved slicing algorithms, have further improved the performance and capabilities of DLP printers, driving their adoption across various industries, including automotive, aerospace, healthcare, and consumer goods. Furthermore, the versatility of DLP technology enables the fabrication of complex geometries, intricate details, and fine features with high resolution and dimensional accuracy, expanding its applications beyond traditional prototyping to include functional parts, end-use products, and custom manufacturing solutions. Over the forecast period, the combination of speed, precision, versatility, and scalability makes DLP technology the fastest-growing segment in the Photopolymers Market, driving its widespread adoption and market expansion.

Photopolymers Market Share Analysis: Medical application segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Photopolymers Market is the Medical application segment. Diverse factors contribute to the rapid growth of photopolymers in medical applications. advancements in additive manufacturing technologies, such as stereolithography (SLA) and digital light processing (DLP), have revolutionized the medical industry by enabling the production of customized and patient-specific medical devices and implants. Photopolymers offer unique advantages in medical applications due to their biocompatibility, precision, and ability to produce intricate and complex geometries with high resolution. In dentistry, photopolymer resins are used for producing dental models, surgical guides, crowns, bridges, and orthodontic appliances with exceptional accuracy and fit. Additionally, in the medical field, photopolymers are utilized for manufacturing hearing aid shells, prosthetic limbs, patient-specific surgical guides, and anatomical models for surgical planning and training purposes. Further, the growing demand for minimally invasive surgical procedures, personalized healthcare solutions, and rapid prototyping in medical device development drives the adoption of photopolymers across various medical specialties. Furthermore, regulatory approvals, advancements in material formulations, and increasing collaborations between medical device manufacturers and 3D printing companies further accelerate the adoption of photopolymers in medical applications. Over the forecast period, the combination of technological advancements, regulatory support, and the need for personalized and patient-specific medical solutions fuels the rapid growth of the Medical application segment in the Photopolymers Market.

Photopolymers Market Report Segmentation

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Photopolymers Companies Profiled in the Market Study

ANYCUBIC Technology Co. Ltd

Arkema S.A.

BASF SE

Carbon Inc

Evonik Industries AG

Formlabs Inc

Henkel AG & Co. KGaA

Keystone Industries LLC

Liqcreate B.V.

PolySpectra Inc

RAHN AG

Stratasys Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Photopolymers Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Photopolymers Market Size Outlook, $ Million, 2021 to 2030

3.2 Photopolymers Market Outlook by Type, $ Million, 2021 to 2030

3.3 Photopolymers Market Outlook by Product, $ Million, 2021 to 2030

3.4 Photopolymers Market Outlook by Application, $ Million, 2021 to 2030

3.5 Photopolymers Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Photopolymers Industry

4.2 Key Market Trends in Photopolymers Industry

4.3 Potential Opportunities in Photopolymers Industry

4.4 Key Challenges in Photopolymers Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Photopolymers Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Photopolymers Market Outlook by Segments

7.1 Photopolymers Market Outlook by Segments, $ Million, 2021- 2030

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

8 North America Photopolymers Market Analysis and Outlook To 2030

8.1 Introduction to North America Photopolymers Markets in 2024

8.2 North America Photopolymers Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Photopolymers Market size Outlook by Segments, 2021-2030

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

9 Europe Photopolymers Market Analysis and Outlook To 2030

9.1 Introduction to Europe Photopolymers Markets in 2024

9.2 Europe Photopolymers Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Photopolymers Market Size Outlook by Segments, 2021-2030

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

10 Asia Pacific Photopolymers Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Photopolymers Markets in 2024

10.2 Asia Pacific Photopolymers Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Photopolymers Market size Outlook by Segments, 2021-2030

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

11 South America Photopolymers Market Analysis and Outlook To 2030

11.1 Introduction to South America Photopolymers Markets in 2024

11.2 South America Photopolymers Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Photopolymers Market size Outlook by Segments, 2021-2030

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

12 Middle East and Africa Photopolymers Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Photopolymers Markets in 2024

12.2 Middle East and Africa Photopolymers Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Photopolymers Market size Outlook by Segments, 2021-2030

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ANYCUBIC Technology Co. Ltd

Arkema S.A.

BASF SE

Carbon Inc

Evonik Industries AG

Formlabs Inc

Henkel AG & Co. KGaA

Keystone Industries LLC

Liqcreate B.V.

PolySpectra Inc

RAHN AG

Stratasys Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Performance

Low Performance

Mid Performance

High Performance

By Technology

Stereolithography (SLA)

Digital Light Processing (DLP)

Continuous Digital Light Processing (cDLP)

By Application

Dental

Medical

Audiology

Jewelry

Automotive

Prototyping

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)