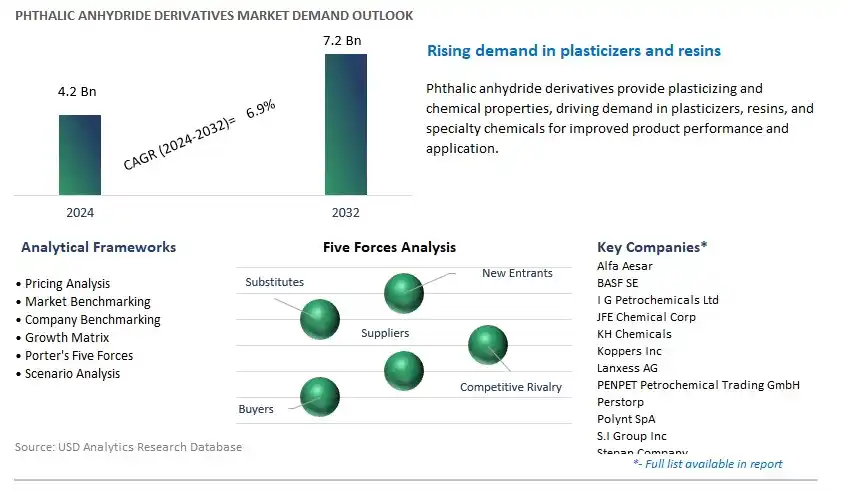

Global Phthalic Anhydride Derivatives Market Size is valued at $4.2 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.9% to reach $7.2 Billion by 2032.

The global Phthalic Anhydride Derivatives Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Derivative (Unsaturated Polyester Resins, Alkyd Resin, Plasticizer, Other), By End-User (Construction, Automotive, Electronics, Aerospace, Others).

An Introduction to Phthalic Anhydride Derivatives Market in 2024

In 2024, the market for phthalic anhydride derivatives witnesses steady growth, driven by their diverse applications in the production of plasticizers, polyester resins, and specialty chemicals. Phthalic anhydride derivatives, including phthalate esters and phthalic acid derivatives, serve as crucial intermediates in the synthesis of polymers and additives used in various industries, including automotive, construction, and consumer goods. Despite increasing regulatory scrutiny and consumer awareness regarding the environmental and health impacts of certain phthalate compounds, demand remains resilient due to the widespread use of phthalic anhydride derivatives in essential applications such as PVC manufacturing, coatings, and adhesives. Further, ongoing efforts to develop safer and more sustainable alternatives, along with technological innovations in chemical synthesis and purification processes, are expected to drive market evolution and maintain the relevance of phthalic anhydride derivatives in the global chemical industry.

Phthalic Anhydride Derivatives Market Competitive Landscape

The market report analyses the leading companies in the industry including Alfa Aesar, BASF SE, I G Petrochemicals Ltd, JFE Chemical Corp, KH Chemicals, Koppers Inc, Lanxess AG, PENPET Petrochemical Trading GmbH, Perstorp, Polynt SpA, S.I Group Inc, Stepan Company, The Chemical Company, Thirumalai Chemicals Ltd, Tokyo Chemical Industry, and others.

Phthalic Anhydride Derivatives Market Dynamics

Market Trend: Shift Towards Sustainable and Eco-Friendly Chemical Solutions

One prominent market trend in the phthalic anhydride derivatives industry is the shift towards sustainable and eco-friendly chemical solutions, driven by increasing environmental awareness, regulatory pressures, and consumer demand for greener alternatives. Phthalic anhydride derivatives, commonly used in the production of plasticizers, resins, and dyes, are facing scrutiny due to their association with environmental and health concerns. This trend is prompting manufacturers to explore and develop new derivatives with improved sustainability profiles, such as bio-based alternatives, renewable feedstocks, and low-toxicity formulations, to meet regulatory requirements, address consumer preferences, and support sustainable development initiatives.

Market Driver: Growing Demand from End-Use Industries and Applications

A key market driver for phthalic anhydride derivatives is the growing demand from end-use industries and applications such as plastics, coatings, construction, automotive, and textiles. Phthalic anhydride derivatives serve as essential building blocks in the production of a wide range of materials and products, including polyvinyl chloride (PVC) plasticizers, alkyd resins, polyester fibers, and synthetic lubricants, among others. The expanding global population, urbanization, and industrialization drive the demand for these derivative products, creating opportunities for manufacturers to meet the diverse needs of customers and industries worldwide.

Market Opportunity: Innovation in Specialty Derivative Products

An opportunity for market growth lies in the innovation and development of specialty phthalic anhydride derivative products tailored to specific application requirements and market segments. Companies specializing in phthalic anhydride derivatives can capitalize on this opportunity by investing in research and development to create value-added products with enhanced performance characteristics, such as improved durability, flexibility, flame retardancy, or biodegradability. Furthermore, targeting niche markets such as bioplastics, specialty coatings, high-performance polymers, or pharmaceutical excipients presents opportunities to differentiate products, command premium pricing, and capture opportunities in segments with higher growth potential. By offering innovative and specialized derivative products, manufacturers can address evolving market needs, expand their product portfolio, and maintain competitiveness in the dynamic chemical industry landscape.

Phthalic Anhydride Derivatives Market Share Analysis: Unsaturated Polyester Resins segment generated the highest revenue in 2024

Unsaturated polyester resins emerge as the largest segment in the phthalic anhydride derivatives market. These resins are extensively utilized in various industries such as construction, automotive, marine, and aerospace for manufacturing fiberglass-reinforced composites, laminates, and coatings. The versatility of unsaturated polyester resins makes them indispensable in applications requiring high strength-to-weight ratios, corrosion resistance, and dimensional stability. The booming construction sector, driven by urbanization, infrastructure development, and the growing demand for lightweight and durable materials, significantly contributes to the dominance of this segment. Moreover, the automotive industry's shift towards lightweight materials to enhance fuel efficiency and reduce emissions further propels the demand for unsaturated polyester resins in composite manufacturing. Additionally, ongoing research and development efforts aimed at enhancing the properties and sustainability of these resins continue to drive their adoption across various end-user industries, solidifying their position as the largest segment in the phthalic anhydride derivatives market.

Phthalic Anhydride Derivatives Market Share Analysis: Electronics is poised to register the fastest CAGR over the forecast period

The electronics segment is the fastest-growing segment in the phthalic anhydride derivatives market. With the proliferation of electronic devices and the rapid advancement of technology, there is an escalating demand for high-performance materials to meet the evolving needs of the electronics industry. Phthalic anhydride derivatives find extensive applications in the manufacturing of various electronic components, including printed circuit boards (PCBs), semiconductor encapsulants, insulating materials, and connectors. The increasing integration of electronics into diverse sectors such as automotive, healthcare, consumer electronics, and telecommunications further drives the demand for these derivatives. Moreover, the rise of emerging technologies like 5G, Internet of Things (IoT), artificial intelligence, and electric vehicles necessitates the production of advanced electronic devices and components, thereby fuelling the growth of the electronics segment in the phthalic anhydride derivatives market. Additionally, ongoing innovations in electronic materials and the quest for more efficient and sustainable solutions contribute to the segment's rapid expansion, making it a key driver of growth in the overall market.

Phthalic Anhydride Derivatives Market

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Phthalic Anhydride Derivatives Companies Profiled in the Study

Alfa Aesar

BASF SE

I G Petrochemicals Ltd

JFE Chemical Corp

KH Chemicals

Koppers Inc

Lanxess AG

PENPET Petrochemical Trading GmbH

Perstorp

Polynt SpA

S.I Group Inc

Stepan Company

The Chemical Company

Thirumalai Chemicals Ltd

Tokyo Chemical Industry

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Phthalic Anhydride Derivatives Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Phthalic Anhydride Derivatives Market Size Outlook, $ Million, 2021 to 2032

3.2 Phthalic Anhydride Derivatives Market Outlook by Type, $ Million, 2021 to 2032

3.3 Phthalic Anhydride Derivatives Market Outlook by Product, $ Million, 2021 to 2032

3.4 Phthalic Anhydride Derivatives Market Outlook by Application, $ Million, 2021 to 2032

3.5 Phthalic Anhydride Derivatives Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Phthalic Anhydride Derivatives Industry

4.2 Key Market Trends in Phthalic Anhydride Derivatives Industry

4.3 Potential Opportunities in Phthalic Anhydride Derivatives Industry

4.4 Key Challenges in Phthalic Anhydride Derivatives Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Phthalic Anhydride Derivatives Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Phthalic Anhydride Derivatives Market Outlook by Segments

7.1 Phthalic Anhydride Derivatives Market Outlook by Segments, $ Million, 2021- 2032

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

8 North America Phthalic Anhydride Derivatives Market Analysis and Outlook To 2032

8.1 Introduction to North America Phthalic Anhydride Derivatives Markets in 2024

8.2 North America Phthalic Anhydride Derivatives Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Phthalic Anhydride Derivatives Market size Outlook by Segments, 2021-2032

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

9 Europe Phthalic Anhydride Derivatives Market Analysis and Outlook To 2032

9.1 Introduction to Europe Phthalic Anhydride Derivatives Markets in 2024

9.2 Europe Phthalic Anhydride Derivatives Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Phthalic Anhydride Derivatives Market Size Outlook by Segments, 2021-2032

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

10 Asia Pacific Phthalic Anhydride Derivatives Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Phthalic Anhydride Derivatives Markets in 2024

10.2 Asia Pacific Phthalic Anhydride Derivatives Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Phthalic Anhydride Derivatives Market size Outlook by Segments, 2021-2032

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

11 South America Phthalic Anhydride Derivatives Market Analysis and Outlook To 2032

11.1 Introduction to South America Phthalic Anhydride Derivatives Markets in 2024

11.2 South America Phthalic Anhydride Derivatives Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Phthalic Anhydride Derivatives Market size Outlook by Segments, 2021-2032

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

12 Middle East and Africa Phthalic Anhydride Derivatives Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Phthalic Anhydride Derivatives Markets in 2024

12.2 Middle East and Africa Phthalic Anhydride Derivatives Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Phthalic Anhydride Derivatives Market size Outlook by Segments, 2021-2032

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Alfa Aesar

BASF SE

I G Petrochemicals Ltd

JFE Chemical Corp

KH Chemicals

Koppers Inc

Lanxess AG

PENPET Petrochemical Trading GmbH

Perstorp

Polynt SpA

S.I Group Inc

Stepan Company

The Chemical Company

Thirumalai Chemicals Ltd

Tokyo Chemical Industry

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Derivative

Unsaturated Polyester Resins

Alkyd Resin

Plasticizer

Other

By End-User

Construction

Automotive

Electronics

Aerospace

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)