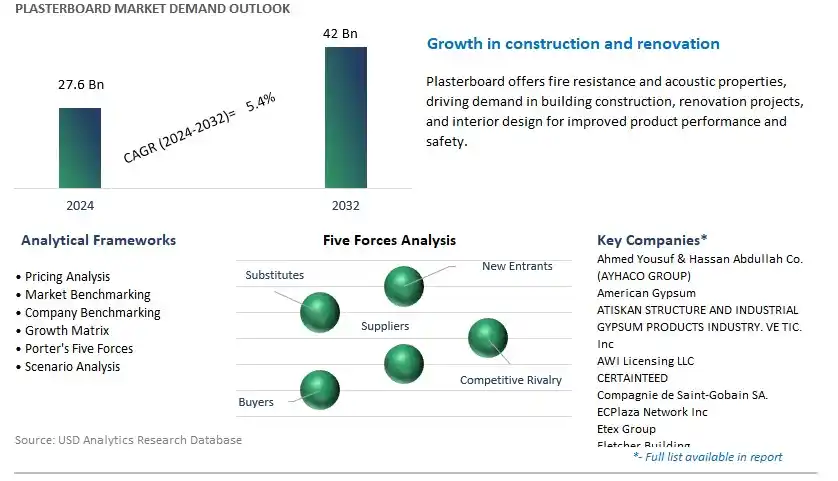

Global Plasterboard Market Size is valued at $27.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.4% to reach $42 Billion by 2032.

The global Plasterboard Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Standard, Fire-resistant, Sound-insulated, Moisture-resistant, Thermal, Others), By Form (Tapered, Square-edged), By End-User (Residential, Non-residential).

An Introduction to Plasterboard Market in 2024

The plasterboard market experiences steady growth in 2024, driven by the construction industry's demand for versatile, cost-effective, and sustainable interior building materials. Plasterboard, also known as drywall or gypsum board, is a widely used construction material composed of gypsum plaster sandwiched between layers of paper or fiberglass. It offers numerous advantages such as ease of installation, fire resistance, sound insulation, and smooth surface finish, making it a preferred choice for wall and ceiling applications in residential, commercial, and industrial buildings. Additionally, the increasing emphasis on energy efficiency and green building practices further propels the adoption of plasterboard, as it can contribute to improved thermal performance and indoor air quality when manufactured using sustainable practices and recycled materials. With urbanization and infrastructure development driving construction activity worldwide, the demand for plasterboard is expected to remain strong, supported by ongoing innovation in product design, manufacturing processes, and environmental stewardship.

Plasterboard Market Competitive Landscape

The market report analyses the leading companies in the industry including Ahmed Yousuf & Hassan Abdullah Co. (AYHACO GROUP), American Gypsum, ATISKAN STRUCTURE AND INDUSTRIAL GYPSUM PRODUCTS INDUSTRY. VE TIC. Inc, AWI Licensing LLC, CERTAINTEED, Compagnie de Saint-Gobain SA., ECPlaza Network Inc, Etex Group, Fletcher Building, Georgia-Pacific, Gyprock, Gypsemna, Gyptec Iberica, Jason Plasterboard Co. Ltd, JN Linrose, LafargeHolcim, Mada Gypsum, National Gypsum Services Company, USG Boral, and others.

Plasterboard Market Dynamics

Market Trend: Sustainable Construction Practices and Green Building Standards

One prominent market trend in the plasterboard industry is the increasing focus on sustainable construction practices and adherence to green building standards, driven by environmental concerns, regulatory requirements, and consumer demand for eco-friendly building materials. Plasterboard, also known as drywall or gypsum board, is witnessing heightened demand as a sustainable alternative to traditional construction materials due to its recyclability, energy efficiency, and low environmental impact. This trend is fueled by the adoption of green building certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method), which incentivize the use of plasterboard and other sustainable construction products to minimize resource consumption, reduce waste generation, and improve indoor air quality in buildings.

Market Driver: Urbanization and Population Growth

A key market driver for plasterboard is urbanization and population growth, which drive the demand for affordable housing, commercial buildings, and infrastructure development in urban centers worldwide. As cities expand and populations increase, there is a growing need for construction materials that offer efficiency, speed of installation, and versatility in building design and renovation projects. Plasterboard, with its lightweight, fire-resistant, and sound-insulating properties, addresses these requirements and is widely used in residential, commercial, and institutional construction applications. Furthermore, the shift towards multi-story and high-density building projects in urban areas drives the demand for plasterboard as a cost-effective and space-efficient solution for interior partitioning, ceiling systems, and wall linings, sustaining market growth and adoption.

Market Opportunity: Innovation in Product Design and Performance

An opportunity for market growth lies in the innovation and development of plasterboard products that offer enhanced performance, functionality, and sustainability features to meet evolving market demands and regulatory requirements. Companies specializing in plasterboard manufacturing can capitalize on this opportunity by investing in research and development to engineer products with improved acoustic insulation, thermal efficiency, moisture resistance, and impact resistance properties. Additionally, developing plasterboard solutions with integrated technologies such as smart sensors for building monitoring, energy management systems, and fire detection presents opportunities to offer value-added solutions and differentiate products in the competitive market landscape. By embracing innovation and sustainability, plasterboard manufacturers can address market trends, drive product differentiation, and capture opportunities in the dynamic construction industry.

Plasterboard Market Share Analysis: Standard segment generated the highest revenue in 2024

Standard plasterboard is the largest segment in the Plasterboard market. Standard plasterboard is the most commonly used type of plasterboard in construction projects worldwide. It offers versatility, affordability, and ease of installation, making it the preferred choice for a wide range of applications in residential, commercial, and industrial buildings. Standard plasterboard provides basic properties such as fire resistance, sound insulation, and thermal insulation, meeting the standard requirements of most construction projects. Additionally, its availability in various sizes and thicknesses allows for flexibility in design and construction, further contributing to its widespread use. Moreover, as construction activities continue to grow globally, particularly in emerging economies, the demand for standard plasterboard remains robust. The construction of new residential and commercial buildings, as well as renovation and refurbishment projects, drives the consumption of standard plasterboard, solidifying its position as the largest segment in the Plasterboard market.

Plasterboard Market Share Analysis: Tapered is poised to register the fastest CAGR over the forecast period

The tapered form of plasterboard is the fastest-growing segment in the Plasterboard. Tapered plasterboard, also known as tapered edge or tapered edge board, offers distinct advantages over square-edged plasterboard in terms of installation efficiency and aesthetics. Tapered edges allow for seamless joints between adjacent boards, reducing the need for extensive joint compound and sanding during the finishing process. This results in faster and more cost-effective installation, making tapered plasterboard the preferred choice for professional drywall installers and contractors. Additionally, the tapered edge design creates smoother transitions between boards, minimizing visible seams and imperfections in the finished wall or ceiling surface. As construction projects increasingly prioritize speed, efficiency, and quality of finish, the demand for tapered plasterboard is on the rise. Moreover, the growing trend towards modern interior design styles, which often feature clean lines and minimalistic aesthetics, further fuels the preference for tapered plasterboard. As a result, the tapered segment is experiencing rapid growth in the Plasterboard market, catering to the evolving needs of construction professionals and designers alike.

Plasterboard Market Share Analysis: Residential segment generated the highest revenue in 2024

The residential segment is the largest segment in the Plasterboard market. Residential construction projects, including single-family homes, multi-family dwellings, and residential renovations, constitute a substantial portion of the overall construction industry. Plasterboard is a fundamental building material extensively used in residential construction for interior wall and ceiling applications. Its versatility, affordability, and ease of installation make it the preferred choice for builders, contractors, and homeowners alike. Additionally, the growing global population, urbanization trends, and increasing disposable incomes drive demand for new residential construction and renovation projects, consequently boosting the consumption of plasterboard. Moreover, as homeowners increasingly prioritize comfort, energy efficiency, and aesthetic appeal, there is a growing demand for innovative plasterboard solutions that offer enhanced thermal and acoustic insulation properties. As a result, the residential segment remains robust, solidifying its position as the largest segment in the Plasterboard market.

Plasterboard Market

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residentialCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Plasterboard Companies Profiled in the Study

Ahmed Yousuf & Hassan Abdullah Co. (AYHACO GROUP)

American Gypsum

ATISKAN STRUCTURE AND INDUSTRIAL GYPSUM PRODUCTS INDUSTRY. VE TIC. Inc

AWI Licensing LLC

CERTAINTEED

Compagnie de Saint-Gobain SA.

ECPlaza Network Inc

Etex Group

Fletcher Building

Georgia-Pacific

Gyprock

Gypsemna

Gyptec Iberica

Jason Plasterboard Co. Ltd

JN Linrose

LafargeHolcim

Mada Gypsum

National Gypsum Services Company

USG Boral

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Plasterboard Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Plasterboard Market Size Outlook, $ Million, 2021 to 2032

3.2 Plasterboard Market Outlook by Type, $ Million, 2021 to 2032

3.3 Plasterboard Market Outlook by Product, $ Million, 2021 to 2032

3.4 Plasterboard Market Outlook by Application, $ Million, 2021 to 2032

3.5 Plasterboard Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Plasterboard Industry

4.2 Key Market Trends in Plasterboard Industry

4.3 Potential Opportunities in Plasterboard Industry

4.4 Key Challenges in Plasterboard Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Plasterboard Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Plasterboard Market Outlook by Segments

7.1 Plasterboard Market Outlook by Segments, $ Million, 2021- 2032

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

8 North America Plasterboard Market Analysis and Outlook To 2032

8.1 Introduction to North America Plasterboard Markets in 2024

8.2 North America Plasterboard Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Plasterboard Market size Outlook by Segments, 2021-2032

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

9 Europe Plasterboard Market Analysis and Outlook To 2032

9.1 Introduction to Europe Plasterboard Markets in 2024

9.2 Europe Plasterboard Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Plasterboard Market Size Outlook by Segments, 2021-2032

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

10 Asia Pacific Plasterboard Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Plasterboard Markets in 2024

10.2 Asia Pacific Plasterboard Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Plasterboard Market size Outlook by Segments, 2021-2032

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

11 South America Plasterboard Market Analysis and Outlook To 2032

11.1 Introduction to South America Plasterboard Markets in 2024

11.2 South America Plasterboard Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Plasterboard Market size Outlook by Segments, 2021-2032

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

12 Middle East and Africa Plasterboard Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Plasterboard Markets in 2024

12.2 Middle East and Africa Plasterboard Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Plasterboard Market size Outlook by Segments, 2021-2032

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Ahmed Yousuf & Hassan Abdullah Co. (AYHACO GROUP)

American Gypsum

ATISKAN STRUCTURE AND INDUSTRIAL GYPSUM PRODUCTS INDUSTRY. VE TIC. Inc

AWI Licensing LLC

CERTAINTEED

Compagnie de Saint-Gobain SA.

ECPlaza Network Inc

Etex Group

Fletcher Building

Georgia-Pacific

Gyprock

Gypsemna

Gyptec Iberica

Jason Plasterboard Co. Ltd

JN Linrose

LafargeHolcim

Mada Gypsum

National Gypsum Services Company

USG Boral

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Standard

Fire-resistant

Sound-insulated

Moisture-resistant

Thermal

Others

By Form

Tapered

Square-edged

By End-User

Residential

Non-residential

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)