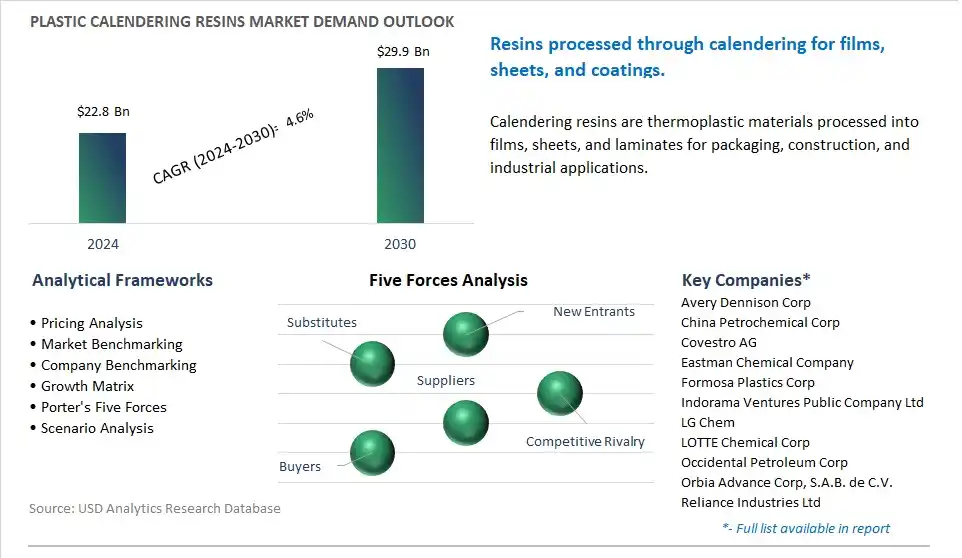

The global Plastic Calendering Resins Market is poised to register a 4.6% CAGR from $22.8 Billion in 2024 to $29.9 Billion in 2030.

The global Plastic Calendering Resins Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (PVC, PET, PP, PETG, Others), By End-User (Food & Beverages, Automotive, Healthcare, Electronics, Construction & Buildings, Furniture, Others).

An Introduction to Global Plastic Calendering Resins Market in 2024

The key trend shaping the future of the plastic calendering resins industry is the increasing demand for high-performance, cost-effective materials for the production of flexible films, sheets, and laminates used in packaging, construction, automotive, and industrial applications. Plastic calendering resins are thermoplastic materials that undergo a calendering process to produce flat or textured surfaces with precise thickness and uniformity, offering excellent mechanical properties, chemical resistance, and surface finish. With growing requirements for lightweight, durable, and visually appealing plastic products, there is a rising need for calendering resins that offer superior processability, thermal stability, and barrier properties to meet the diverse needs of end-users across different sectors. Manufacturers are investing in the development of innovative calendering resin formulations based on polymers such as polyvinyl chloride (PVC), polyethylene (PE), polypropylene (PP), and thermoplastic elastomers (TPE) to address specific application requirements such as food packaging, automotive interiors, roofing membranes, and medical films. Additionally, there is a trend towards the use of sustainable and recyclable calendering resins that comply with regulatory standards, industry certifications, and customer preferences for eco-friendly materials, addressing concerns over plastic waste and environmental sustainability. Furthermore, with increasing competition and technological advancements in the plastics industry, there is a growing emphasis on product differentiation, customization, and value-added services to meet the evolving needs and preferences of customers in a dynamic market environment. As industries continue to innovate and adapt to changing market dynamics, the demand for high-quality calendering resins tailored to specific performance requirements and processing conditions is expected to grow, driving market expansion and technological innovation in the plastics compounding and processing sector.

Plastic Calendering Resins Market Competitive Landscape

The market report analyses the leading companies in the industry including Avery Dennison Corp, China Petrochemical Corp, Covestro AG, Eastman Chemical Company, Formosa Plastics Corp, Indorama Ventures Public Company Ltd, LG Chem, LOTTE Chemical Corp, Occidental Petroleum Corp, Orbia Advance Corp, S.A.B. de C.V., Reliance Industries Ltd, SABIC, Shin-Etsu Chemical Co. Ltd, SK chemicals, Westlake Corp.

Plastic Calendering Resins Market Dynamics

Plastic Calendering Resins Market Trend: Increasing Demand for Sustainable and Recyclable Resins

A prominent trend in the plastic calendering resins market is the increasing demand for sustainable and recyclable resins. With growing awareness of environmental issues and regulatory pressures to reduce plastic waste, there is a shifting preference towards resins that offer improved sustainability profiles. Manufacturers are investing in research and development to develop bio-based, biodegradable, and recyclable plastic calendering resins that can replace traditional petroleum-based counterparts. Additionally, there is a trend towards the development of resins with enhanced properties such as improved mechanical strength, barrier properties, and heat resistance, to meet the diverse needs of end-users across industries such as packaging, automotive, construction, and consumer goods.

Plastic Calendering Resins Market Driver: Growth in Packaging and Construction Industries

The primary driver fueling the plastic calendering resins market is the growth in the packaging and construction industries. Plastic calendering resins are extensively used in the manufacturing of various products such as packaging films, sheets, profiles, and laminates, due to their versatility, cost-effectiveness, and ease of processing. With the expansion of the global packaging market, driven by factors such as population growth, urbanization, e-commerce trends, and changing consumer preferences, there is a significant increase in the demand for plastic packaging materials. Similarly, the construction industry is witnessing robust growth, particularly in emerging economies, driven by infrastructure development projects, urbanization trends, and investments in residential and commercial construction. Plastic calendering resins find wide applications in the construction sector for manufacturing roofing membranes, flooring materials, wall claddings, and insulation products. The burgeoning demand for packaging and construction materials is driving the consumption of plastic calendering resins, thereby fueling market growth.

Plastic Calendering Resins Market Opportunity: Development of High-Performance Specialty Resins

An opportunity for the plastic calendering resins market lies in the development of high-performance specialty resins tailored to meet specific application requirements. As industries such as automotive, aerospace, electronics, and healthcare demand materials with superior properties such as flame resistance, chemical resistance, UV stability, and thermal conductivity, there is a growing need for specialty resins that can withstand harsh operating conditions and stringent performance standards. Manufacturers aim to capitalize on this opportunity by investing in research and development to innovate and commercialize specialty resins with advanced properties, formulations, and processing characteristics. By offering tailored solutions to niche markets and addressing unmet needs, manufacturers aim to gain market shares in the market, command premium pricing, and capture new growth opportunities. Additionally, partnerships and collaborations with end-users and value chain partners can help accelerate product development and market penetration, enabling companies to stay ahead of the competition and unlock the full potential of the plastic calendering resins market.

Plastic Calendering Resins Market Share Analysis: PVC (Polyvinyl Chloride) generated the highest revenue in 2024

The largest segment in the Plastic Calendering Resins Market is the PVC (Polyvinyl Chloride) category. PVC is one of the most widely used thermoplastic polymers in the world due to its versatility, durability, and cost-effectiveness. PVC calendering resins are extensively utilized in various industries for manufacturing a wide range of products, including vinyl films, sheets, flooring, pipes, profiles, and packaging materials. PVC offers excellent properties such as chemical resistance, weatherability, flame retardancy, and electrical insulation, making it suitable for diverse applications in construction, automotive, packaging, healthcare, and consumer goods sectors. Additionally, PVC can be easily processed using calendering techniques to produce flexible or rigid products with precise dimensions, smooth surface finish, and tailored properties to meet specific end-use requirements. Further, PVC has a long history of use and established market infrastructure, including manufacturing facilities, distribution networks, and regulatory standards, which contribute to its dominance in the plastic calendering resins market. Furthermore, PVC remains competitive compared to other plastic resins due to its relatively low cost, wide availability of raw materials, and recyclability, making it a preferred choice for manufacturers seeking cost-effective and sustainable solutions. Accordingly, the PVC segment is the largest in the Plastic Calendering Resins Market due to its widespread use, versatility, and established market presence across multiple industries.

Plastic Calendering Resins Market Share Analysis: Healthcare segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Plastic Calendering Resins Market is the Healthcare sector. This is driving increased demand for plastic calendering resins in the healthcare industry. There is a growing need for medical-grade plastic materials for manufacturing a wide range of healthcare products, including medical devices, equipment components, packaging materials, and disposable supplies. Plastic calendering resins offer advantages such as flexibility, clarity, sterilizability, and biocompatibility, making them suitable for use in medical applications such as IV bags, blood bags, tubing, catheters, diagnostic components, and packaging for pharmaceuticals and medical devices. Additionally, the COVID-19 pandemic has further accelerated the demand for healthcare products and medical supplies, driving investments in medical-grade plastic materials and production capacity to meet the surge in demand for healthcare products worldwide. Further, advancements in plastic calendering technology, such as cleanroom manufacturing, precision processing, and compliance with regulatory standards for medical devices and packaging, have enabled manufacturers to produce high-quality and regulatory-compliant healthcare products efficiently and cost-effectively. Furthermore, demographic trends such as aging populations and increasing healthcare expenditures are driving the growth of the healthcare industry, creating opportunities for the expansion of the market for plastic calendering resins in healthcare applications. Accordingly, the Healthcare sector is the fastest-growing in the Plastic Calendering Resins Market as the healthcare industry increasingly relies on plastic calendering technology to meet evolving healthcare needs and regulatory requirements.

Plastic Calendering Resins Market Report Segmentation

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Plastic Calendering Resins Companies Profiled in the Market Study

Avery Dennison Corp

China Petrochemical Corp

Covestro AG

Eastman Chemical Company

Formosa Plastics Corp

Indorama Ventures Public Company Ltd

LG Chem

LOTTE Chemical Corp

Occidental Petroleum Corp

Orbia Advance Corp, S.A.B. de C.V.

Reliance Industries Ltd

SABIC

Shin-Etsu Chemical Co. Ltd

SK chemicals

Westlake Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Plastic Calendering Resins Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Plastic Calendering Resins Market Size Outlook, $ Million, 2021 to 2030

3.2 Plastic Calendering Resins Market Outlook by Type, $ Million, 2021 to 2030

3.3 Plastic Calendering Resins Market Outlook by Product, $ Million, 2021 to 2030

3.4 Plastic Calendering Resins Market Outlook by Application, $ Million, 2021 to 2030

3.5 Plastic Calendering Resins Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Plastic Calendering Resins Industry

4.2 Key Market Trends in Plastic Calendering Resins Industry

4.3 Potential Opportunities in Plastic Calendering Resins Industry

4.4 Key Challenges in Plastic Calendering Resins Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Plastic Calendering Resins Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Plastic Calendering Resins Market Outlook by Segments

7.1 Plastic Calendering Resins Market Outlook by Segments, $ Million, 2021- 2030

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

8 North America Plastic Calendering Resins Market Analysis and Outlook To 2030

8.1 Introduction to North America Plastic Calendering Resins Markets in 2024

8.2 North America Plastic Calendering Resins Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Plastic Calendering Resins Market size Outlook by Segments, 2021-2030

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

9 Europe Plastic Calendering Resins Market Analysis and Outlook To 2030

9.1 Introduction to Europe Plastic Calendering Resins Markets in 2024

9.2 Europe Plastic Calendering Resins Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Plastic Calendering Resins Market Size Outlook by Segments, 2021-2030

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

10 Asia Pacific Plastic Calendering Resins Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Plastic Calendering Resins Markets in 2024

10.2 Asia Pacific Plastic Calendering Resins Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Plastic Calendering Resins Market size Outlook by Segments, 2021-2030

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

11 South America Plastic Calendering Resins Market Analysis and Outlook To 2030

11.1 Introduction to South America Plastic Calendering Resins Markets in 2024

11.2 South America Plastic Calendering Resins Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Plastic Calendering Resins Market size Outlook by Segments, 2021-2030

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

12 Middle East and Africa Plastic Calendering Resins Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Plastic Calendering Resins Markets in 2024

12.2 Middle East and Africa Plastic Calendering Resins Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Plastic Calendering Resins Market size Outlook by Segments, 2021-2030

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Avery Dennison Corp

China Petrochemical Corp

Covestro AG

Eastman Chemical Company

Formosa Plastics Corp

Indorama Ventures Public Company Ltd

LG Chem

LOTTE Chemical Corp

Occidental Petroleum Corp

Orbia Advance Corp, S.A.B. de C.V.

Reliance Industries Ltd

SABIC

Shin-Etsu Chemical Co. Ltd

SK chemicals

Westlake Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

PVC

PET

PP

PETG

Others

By End-User

Food & Beverages

Automotive

Healthcare

Electronics

Construction & Buildings

Furniture

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)