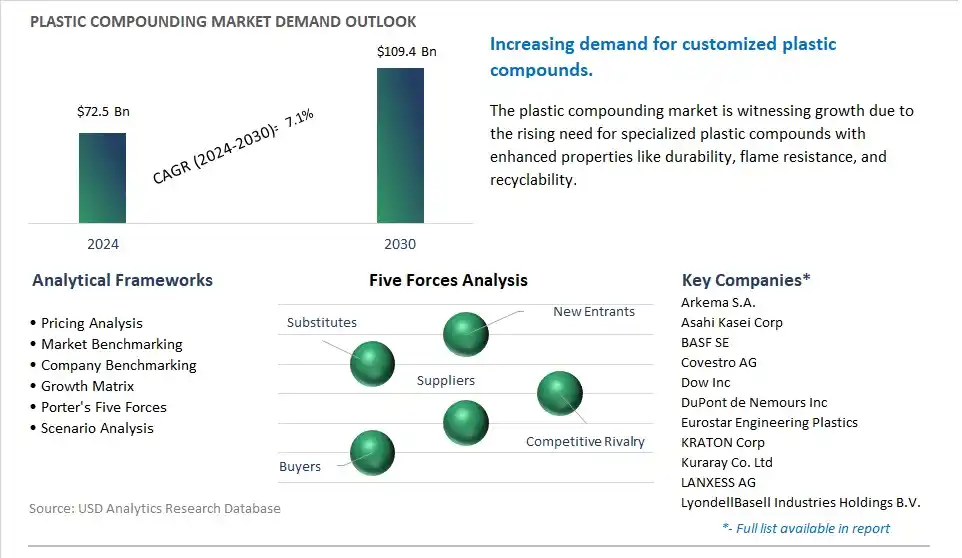

The global Plastic Compounding Market is poised to register a 7.1% CAGR from $72.5 Billion in 2024 to $109.4 Billion in 2030.

The global Plastic Compounding Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Source (Fossil-based, Bio-based, Recycled), By Product (Polyethylene (PE), Polypropylene (PP), Thermoplastic Vulcanizates (TPV), Thermoplastic Polyolefins (TPO), Polyvinyl Chloride (PVC), Polystyrene (PS), Polyethylene Terephthalate (PET), Polybutylene Terephthalate (PBT), Polyamide (PA), Polycarbonate (PC), Polyurethane (PU), Polymethyl Methacrylate (PMMA), Acrylonitrile Butadiene Styrene (ABS), Others), By Application (Automotive, Building & construction, Electrical & electronics, Packaging, Consumer goods, Industrial machinery, Medical devices, Optical media, Aerospace, Others).

An Introduction to Global Plastic Compounding Market in 2024

The key trend shaping the future of the plastic compounding industry is the increasing demand for specialized, customized, and sustainable polymer compounds to meet the diverse needs of end-users across various sectors such as automotive, electronics, packaging, and construction. Plastic compounding involves the blending of base polymers with additives, fillers, reinforcements, and colorants to create materials with specific performance attributes such as strength, flexibility, flame retardancy, and UV resistance. With growing requirements for lightweight, durable, and high-performance materials, there is a rising need for plastic compounds that offer enhanced properties and functionalities tailored to meet the evolving demands of different applications. Manufacturers are investing in the development of advanced compounding technologies such as twin-screw extrusion, melt blending, and reactive compounding to optimize material performance, process efficiency, and product consistency. Additionally, there is a trend towards the use of sustainable additives, bio-based fillers, and recycled polymers in plastic compounding to reduce environmental impact, improve resource efficiency, and support circular economy initiatives. Furthermore, with increasing regulatory scrutiny and consumer awareness of health and environmental issues, there is a growing interest in compounding solutions that comply with stringent safety standards, regulatory requirements, and industry certifications, ensuring product quality, reliability, and sustainability. As industries continue to innovate and differentiate their products through material science and engineering solutions, the demand for customized plastic compounds with tailored properties and performance characteristics is expected to grow, driving market expansion and technological innovation in the plastics compounding sector.

Plastic Compounding Market Competitive Landscape

The market report analyses the leading companies in the industry including Arkema S.A., Asahi Kasei Corp, BASF SE, Covestro AG, Dow Inc, DuPont de Nemours Inc, Eurostar Engineering Plastics, KRATON Corp, Kuraray Co. Ltd, LANXESS AG, LyondellBasell Industries Holdings B.V., Polyvisions Inc, Ravago Group, RTP Company, S&E Specialty Polymers LLC, SABIC, SO.F.TER. Srl, Solvay S.A., Teijin Ltd, Washington Penn.

Plastic Compounding Market Dynamics

Plastic Compounding Market Trend: Increasing Demand for Sustainable and Specialty Compounds

A prominent trend in the plastic compounding market is the increasing demand for sustainable and specialty compounds. With growing concerns about environmental sustainability and regulatory pressures to reduce carbon footprint, there is a rising preference for compounds made from recycled or biodegradable materials. Manufacturers are also focusing on developing specialty compounds with enhanced properties such as flame retardancy, thermal stability, UV resistance, and conductivity to meet the specific requirements of various industries such as automotive, electrical and electronics, construction, and healthcare. Furthermore, innovations in compounding technologies, such as reactive extrusion and nano-composites, are driving the development of advanced compounds with improved performance characteristics, opening up new opportunities in the market.

Plastic Compounding Market Driver: Growth in End-Use Industries and Replacement of Traditional Materials

The primary driver fueling the plastic compounding market is the growth in end-use industries and the replacement of traditional materials with engineered thermoplastics. Industries such as automotive, consumer goods, packaging, electrical and electronics, and construction are increasingly adopting plastic compounds due to their superior properties, cost-effectiveness, and design flexibility. The automotive industry, in particular, is witnessing a significant surge in the use of lightweight and high-performance plastics to meet stringent fuel efficiency and emissions standards. Similarly, the packaging industry is transitioning from conventional materials like glass and metal to plastic compounds for their lightweight, durability, and barrier properties. Additionally, the replacement of traditional materials such as wood, metal, and rubber with plastic compounds in various applications is further driving market growth.

Plastic Compounding Market Opportunity: Development of Customized and Functional Compounds

An opportunity for the plastic compounding market lies in the development of customized and functional compounds tailored to meet specific customer requirements and application needs. As end-users demand materials with unique properties and performance characteristics, there is a growing need for compounds that offer enhanced functionality, aesthetics, and sustainability. Manufacturers aim to capitalize on this opportunity by offering customized compounding solutions that address niche markets and niche applications, such as medical devices, aerospace components, and electronic enclosures. By leveraging their expertise in material science, formulation development, and compounding technologies, companies can collaborate closely with customers to co-develop specialized compounds that deliver superior performance, durability, and cost-effectiveness. Furthermore, partnerships with raw material suppliers, additive manufacturers, and equipment providers can enhance innovation capabilities and expand the product portfolio, enabling companies to capture a larger share of the plastic compounding market.

Plastic Compounding Market Share Analysis: Fossil-based generated the highest revenue in 2024

The largest segment in the Plastic Compounding Market is the Fossil-based category. Fossil-based sources, primarily derived from petrochemical feedstocks such as crude oil and natural gas, have historically been the primary source of raw materials for plastic compounding due to their abundance, cost-effectiveness, and well-established infrastructure for polymer production and processing. Fossil-based plastics offer a wide range of properties, including versatility, durability, and processability, making them suitable for diverse applications in industries such as packaging, automotive, construction, electronics, and consumer goods. Additionally, fossil-based plastics can be easily compounded with additives, fillers, and reinforcements to enhance their performance, functionality, and sustainability. Further, advancements in polymer science and compounding technologies have enabled manufacturers to develop innovative formulations and blends of fossil-based plastics with improved properties such as strength, impact resistance, flame retardancy, and chemical resistance, further driving their adoption in various applications. Furthermore, despite growing concerns about environmental sustainability and plastic pollution, fossil-based plastics continue to dominate the market due to their established market presence, performance advantages, and cost competitiveness compared to alternative sources such as bio-based and recycled plastics. Accordingly, the Fossil-based segment is the largest in the Plastic Compounding Market, reflecting the widespread use and reliance on fossil-based plastics in the global economy.

Plastic Compounding Market Share Analysis: Thermoplastic Polyolefins (TPO) segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Plastic Compounding Market is the Thermoplastic Polyolefins (TPO) category. This is driving increased demand for TPO compounds in various industries. TPO compounds offer a unique combination of properties that make them suitable for a wide range of applications, including automotive, construction, packaging, and consumer goods. TPOs exhibit excellent mechanical properties such as high impact strength, stiffness, and toughness, as well as resistance to chemicals, weathering, and UV radiation, making them ideal for outdoor and automotive applications requiring durability and weatherability. Additionally, TPO compounds can be easily processed using conventional thermoplastic processing techniques such as injection molding, extrusion, and blow molding, enabling manufacturers to produce complex parts and components with high efficiency and cost-effectiveness. Further, regulatory trends favoring lightweight materials, fuel efficiency, and sustainability in automotive and construction industries are driving the adoption of TPO compounds as alternatives to traditional materials such as metals, rubber, and PVC. Furthermore, advancements in TPO formulation technology, including the development of reinforced and filled TPO grades with enhanced properties such as flame retardancy, dimensional stability, and surface aesthetics, are expanding the application scope and market opportunities for TPO compounds. Accordingly, the Thermoplastic Polyolefins (TPO) segment is the fastest-growing in the Plastic Compounding Market as industries increasingly recognize the performance, versatility, and sustainability benefits of TPO compounds for addressing evolving market needs and regulatory requirements.

Plastic Compounding Market Share Analysis: Electrical & Electronics segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Plastic Compounding Market is the Electrical & Electronics category. This is driving increased demand for plastic compounds in the electrical and electronics industry. The proliferation of electronic devices, including smartphones, tablets, laptops, and wearable technologies, has led to a surge in demand for high-performance plastic compounds with properties such as electrical insulation, heat resistance, flame retardancy, and dimensional stability. Plastics offer advantages over traditional materials such as metal and ceramics in terms of weight reduction, design flexibility, and cost-effectiveness, making them ideal for use in electrical and electronic applications. Additionally, the transition towards miniaturization, integration, and connectivity in electronic devices requires materials with improved properties such as high flowability, moldability, and surface finish, which can be achieved through advanced plastic compounding technologies. Further, regulatory initiatives aimed at reducing hazardous substances, such as RoHS and REACH directives, are driving the adoption of environmentally friendly and compliant plastic compounds in electrical and electronic products. Furthermore, emerging trends such as electric mobility, renewable energy, and smart infrastructure are creating opportunities for plastics in new applications such as electric vehicle components, solar panels, and smart grids, further fueling the growth of the electrical and electronics segment in the plastic compounding market. Accordingly, the Electrical & Electronics segment is the fastest-growing in the Plastic Compounding Market as the industry continues to innovate and adopt plastic compounds to meet the evolving requirements of modern electronic devices and systems.

Plastic Compounding Market Report Segmentation

By Source

Fossil-based

Bio-based

Recycled

By Product

Polyethylene (PE)

Polypropylene (PP)

Thermoplastic Vulcanizates (TPV)

Thermoplastic Polyolefins (TPO)

Polyvinyl Chloride (PVC)

Polystyrene (PS)

Polyethylene Terephthalate (PET)

Polybutylene Terephthalate (PBT)

Polyamide (PA)

Polycarbonate (PC)

Polyurethane (PU)

Polymethyl Methacrylate (PMMA)

Acrylonitrile Butadiene Styrene (ABS)

Others

By Application

Automotive

Building & construction

Electrical & electronics

Packaging

Consumer goods

Industrial machinery

Medical devices

Optical media

Aerospace

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Plastic Compounding Companies Profiled in the Market Study

Arkema S.A.

Asahi Kasei Corp

BASF SE

Covestro AG

Dow Inc

DuPont de Nemours Inc

Eurostar Engineering Plastics

KRATON Corp

Kuraray Co. Ltd

LANXESS AG

LyondellBasell Industries Holdings B.V.

Polyvisions Inc

Ravago Group

RTP Company

S&E Specialty Polymers LLC

SABIC

SO.F.TER. Srl

Solvay S.A.

Teijin Ltd

Washington Penn

*- List Not Exhaustive