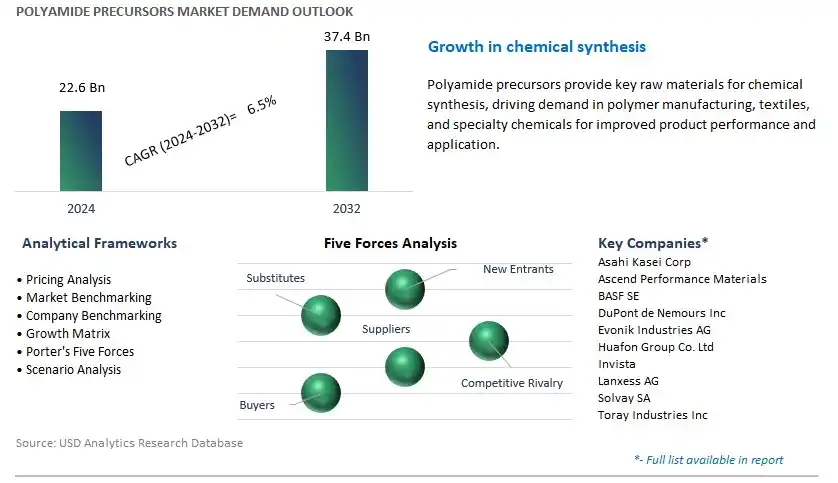

Global Polyamide Precursors Market Size is valued at $22.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.5% to reach $37.4 Billion by 2032.

The global Polyamide Precursors Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Adipic Acid (ADA), Caprolactam (CPL), Hexamethylenediamine (HMDA), Others), By End-User (Automotive, Electrical and Electronics, Textile, Packaging, Others).

An Introduction to Polyamide Precursors Market in 2024

The polyamide precursors market experiences significant growth in 2024, driven by the expanding demand for raw materials used in the production of polyamide resins, fibers, and engineering plastics. Polyamide precursors, also known as nylon intermediates, are key chemical compounds synthesized from petrochemical feedstocks such as adipic acid and hexamethylene diamine, which serve as building blocks for various polyamide formulations. They play a crucial role in the polymerization process, determining the properties and performance characteristics of the final polyamide products, including tensile strength, impact resistance, and thermal stability. With the increasing use of polyamides in automotive, aerospace, textiles, and consumer goods industries, the demand for high-quality precursors s to rise, supported by the growing production of nylon fibers, resins, and specialty polymers worldwide. Further, technological advancements in precursor synthesis, process optimization, and sustainability initiatives contribute to market expansion, offering opportunities for manufacturers to innovate and differentiate their product offerings in response to evolving market trends and customer requirements.

Polyamide Precursors Market Competitive Landscape

The market report analyses the leading companies in the industry including Asahi Kasei Corp, Ascend Performance Materials, BASF SE, DuPont de Nemours Inc, Evonik Industries AG, Huafon Group Co. Ltd, Invista, Lanxess AG, Solvay SA, Toray Industries Inc, and others.

Polyamide Precursors Market Dynamics

Market Trend: Demand for High-Performance Materials in Advanced Manufacturing

One prominent market trend in the polyamide precursors industry is the increasing demand for high-performance materials in advanced manufacturing processes, driven by trends in aerospace, automotive, electronics, and medical industries. Polyamide precursors, essential raw materials for producing polyamide fibers, resins, and engineered plastics, are witnessing heightened demand as manufacturers seek materials with superior mechanical properties, chemical resistance, and thermal stability for critical applications. This trend is fueled by the need for lightweight, durable, and high-strength materials to meet performance requirements in aerospace components, automotive parts, electronic enclosures, and medical devices, driving the adoption of polyamide precursors in various industrial sectors worldwide.

Market Driver: Technological Advancements and Material Innovation

A key market driver for polyamide precursors is technological advancements and material innovation, which drive the development of novel formulations, processing techniques, and application-specific solutions to meet evolving market demands and performance requirements. As industries embrace digitalization, additive manufacturing, and advanced materials science, there is a growing emphasis on engineering plastics with tailored properties such as improved strength-to-weight ratio, chemical resistance, and processability. Polyamide precursors play a vital role in enabling these advancements by serving as building blocks for engineering polymers such as nylon 6, nylon 66, and specialty polyamides, which find applications in a wide range of industries and end-use applications. Furthermore, the ongoing research and development efforts in polyamide chemistry, polymer processing, and additive manufacturing technologies drive continuous innovation and market growth in the polyamide precursors industry.

Market Opportunity: Customization and Tailored Solutions for Specific Applications

An opportunity for market growth lies in the customization and development of tailored polyamide precursor formulations to address specific performance requirements and application needs in diverse industries. Companies specializing in polyamide precursor production can capitalize on this opportunity by offering a wide range of product grades, compositions, and processing aids optimized for specific end-use applications such as injection molding, extrusion, 3D printing, and fiber spinning. Additionally, developing specialty polyamide precursors with enhanced properties such as flame retardancy, electrical conductivity, and bio-compatibility presents opportunities to target niche markets and emerging applications in sectors such as automotive, electronics, healthcare, and consumer goods. By providing customized solutions and value-added services, manufacturers can differentiate their products, strengthen customer relationships, and capture opportunities in the dynamic and evolving market for polyamide precursors.

Polyamide Precursors Market Share Analysis: Caprolactam (CPL) segment generated the highest revenue in 2024

Caprolactam is the largest segment in the Polyamide Precursors market. Caprolactam is a key precursor in the production of polyamide 6 (PA 6), one of the most widely used engineering thermoplastics globally. PA 6 offers exceptional mechanical properties, chemical resistance, and thermal stability, making it suitable for various applications across industries such as automotive, electrical and electronics, consumer goods, and packaging. As a result, the demand for caprolactam as a raw material for PA 6 production remains robust, driving its dominance in the Polyamide Precursors market. Additionally, technological advancements and innovations in caprolactam production processes, such as the development of environmentally friendly and cost-effective production methods, further contribute to its widespread adoption. Moreover, the growing demand for lightweight and high-performance materials in industries such as automotive and electronics fuels the consumption of caprolactam, solidifying its position as the largest segment in the Polyamide Precursors market.

Polyamide Precursors Market Share Analysis: Electrical and Electronics is poised to register the fastest CAGR over the forecast period

The electrical and electronics sector is the fastest-growing segment in the Polyamide Precursors. Polyamide precursors, particularly caprolactam and adipic acid, are essential raw materials used in the production of engineering plastics such as polyamide 6 (PA 6) and polyamide 66 (PA 66), which find extensive applications in the electrical and electronics industry. These materials offer excellent mechanical properties, chemical resistance, and thermal stability, making them ideal for manufacturing various components and parts used in electronic devices, electrical equipment, and wiring systems. With the rapid advancements in technology and the increasing adoption of electronic devices across various sectors, including consumer electronics, telecommunications, automotive electronics, and industrial automation, the demand for polyamide precursors in the electrical and electronics sector is witnessing significant growth. Moreover, the trend towards miniaturization, lightweighting, and high-performance materials in electronics further drives the consumption of polyamide precursors. As the demand for advanced electronic products continues to rise globally, particularly in emerging markets, the electrical and electronics segment is expected to experience rapid growth, making it the fastest-growing segment in the Polyamide Precursors market.

Polyamide Precursors Market

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Polyamide Precursors Companies Profiled in the Study

Asahi Kasei Corp

Ascend Performance Materials

BASF SE

DuPont de Nemours Inc

Evonik Industries AG

Huafon Group Co. Ltd

Invista

Lanxess AG

Solvay SA

Toray Industries Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Polyamide Precursors Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Polyamide Precursors Market Size Outlook, $ Million, 2021 to 2032

3.2 Polyamide Precursors Market Outlook by Type, $ Million, 2021 to 2032

3.3 Polyamide Precursors Market Outlook by Product, $ Million, 2021 to 2032

3.4 Polyamide Precursors Market Outlook by Application, $ Million, 2021 to 2032

3.5 Polyamide Precursors Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Polyamide Precursors Industry

4.2 Key Market Trends in Polyamide Precursors Industry

4.3 Potential Opportunities in Polyamide Precursors Industry

4.4 Key Challenges in Polyamide Precursors Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Polyamide Precursors Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Polyamide Precursors Market Outlook by Segments

7.1 Polyamide Precursors Market Outlook by Segments, $ Million, 2021- 2032

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

8 North America Polyamide Precursors Market Analysis and Outlook To 2032

8.1 Introduction to North America Polyamide Precursors Markets in 2024

8.2 North America Polyamide Precursors Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Polyamide Precursors Market size Outlook by Segments, 2021-2032

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

9 Europe Polyamide Precursors Market Analysis and Outlook To 2032

9.1 Introduction to Europe Polyamide Precursors Markets in 2024

9.2 Europe Polyamide Precursors Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Polyamide Precursors Market Size Outlook by Segments, 2021-2032

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

10 Asia Pacific Polyamide Precursors Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Polyamide Precursors Markets in 2024

10.2 Asia Pacific Polyamide Precursors Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Polyamide Precursors Market size Outlook by Segments, 2021-2032

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

11 South America Polyamide Precursors Market Analysis and Outlook To 2032

11.1 Introduction to South America Polyamide Precursors Markets in 2024

11.2 South America Polyamide Precursors Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Polyamide Precursors Market size Outlook by Segments, 2021-2032

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

12 Middle East and Africa Polyamide Precursors Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Polyamide Precursors Markets in 2024

12.2 Middle East and Africa Polyamide Precursors Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Polyamide Precursors Market size Outlook by Segments, 2021-2032

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Asahi Kasei Corp

Ascend Performance Materials

BASF SE

DuPont de Nemours Inc

Evonik Industries AG

Huafon Group Co. Ltd

Invista

Lanxess AG

Solvay SA

Toray Industries Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Adipic Acid (ADA)

Caprolactam (CPL)

Hexamethylenediamine (HMDA)

Others

By End-User

Automotive

Electrical and Electronics

Textile

Packaging

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)