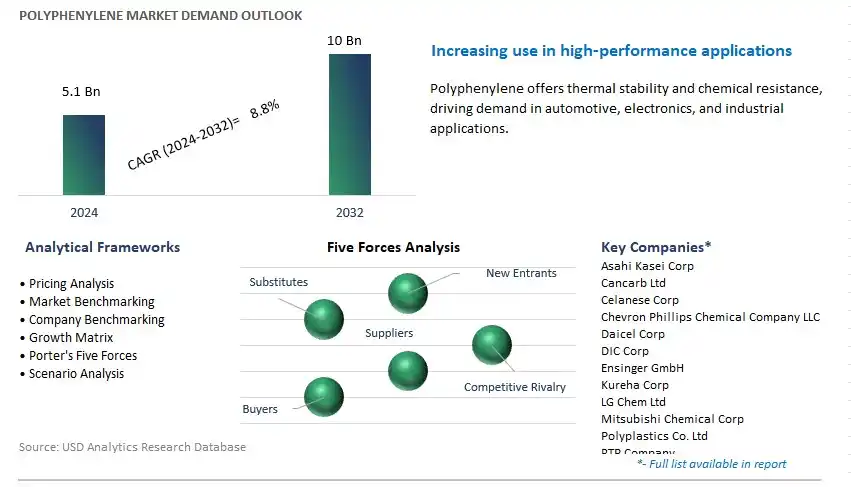

Global Polyphenylene Market Size is valued at $5.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 8.8% to reach $10 Billion by 2032.

The global Polyphenylene Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Polyphenylene Sulfide (PPS), Polyphenylene Ether/Oxide (PPE/PPO), Others), By End-User (Automotive, Electrical & Electronics, Industrial, Coatings, Others), By Application (Composites, Engineering Plastics, High Performance Lubricants, Filter Bags, Others).

An Introduction to Polyphenylene Market in 2024

Polyphenylene (PPS) is a high-performance thermoplastic polymer known for its exceptional heat resistance, chemical resistance, flame retardancy, and mechanical properties, making it a preferred material choice for various automotive, aerospace, electrical, and industrial applications. In 2024, the market for polyphenylene s to grow as industries seek lightweight, durable, and reliable materials for high-temperature and chemically aggressive environments in a global market landscape. Polyphenylene offers advantages such as high thermal stability, dimensional stability, creep resistance, and resistance to harsh chemicals and solvents, allowing for long-term performance and reliability in demanding applications. This polymer is used in automotive components such as fuel system parts, sensors, and connectors for its resistance to fuels, oils, and automotive fluids, as well as in electrical and electronic applications such as connectors, sockets, and circuit breakers for its electrical properties and flame retardancy. In aerospace and industrial applications, polyphenylene is used in components such as pumps, valves, and seals for its wear resistance and dimensional stability. The demand for polyphenylene is driven by factors such as the growth of automotive electrification and lightweighting trends, increasing demand for high-temperature and chemically resistant materials in aerospace and industrial sectors, and the expansion of electronics and semiconductor industries. Market trends include the development of advanced PPS grades with improved flowability, impact resistance, and processing stability, the optimization of polymer compounding and molding techniques for enhanced part quality and productivity, and the integration of advanced testing and simulation tools for predictive material design and performance optimization.

Polyphenylene Market Competitive Landscape

The market report analyses the leading companies in the industry including Asahi Kasei Corp, Cancarb Ltd, Celanese Corp, Chevron Phillips Chemical Company LLC, Daicel Corp, DIC Corp, Ensinger GmbH, Kureha Corp, LG Chem Ltd, Mitsubishi Chemical Corp, Polyplastics Co. Ltd, RTP Company, Ryan Plastics Ltd, Solvay SA, Songhan Plastic Technology Co. Ltd, Teijin Ltd, Toray Industries Inc, Tosoh Corp, Zhejiang Xinhecheng Special Materials Co. Ltd, and others.

Polyphenylene Market Dynamics

Market Trend: Increasing Demand for High-Performance Engineering Plastics

A significant trend in the polyphenylene market is the increasing demand for high-performance engineering plastics across various industries. Polyphenylenes, including polyphenylene sulfide (PPS) and polyphenylene ether (PPE), are valued for their exceptional thermal stability, mechanical strength, chemical resistance, and flame-retardant properties. This trend is driven by the need for materials capable of withstanding extreme temperatures, harsh chemicals, and demanding operating conditions in sectors such as automotive, aerospace, electronics, and industrial manufacturing. As manufacturers seek lightweight and durable alternatives to traditional metals and thermoset plastics, the demand for polyphenylene-based materials continues to rise, spurring innovation in material formulations, processing technologies, and application development to meet the stringent requirements of high-performance end-users.

Market Driver: Growth in Electric Vehicles and Electrical Components

A key driver propelling the polyphenylene market is the growth in electric vehicles (EVs) and electrical components. Polyphenylene materials, particularly PPS and PPE, are widely used in the automotive industry for electrical insulation, connectors, sensors, and battery components in EVs and hybrid vehicles. With the increasing adoption of EVs worldwide, driven by environmental regulations, government incentives, and consumer demand for sustainable transportation solutions, there is a robust demand for materials that offer excellent electrical properties, thermal stability, and flame resistance to ensure the safety and reliability of electric drivetrains and power electronics. Moreover, the electrification trend extends beyond the automotive sector to various applications in renewable energy, electronics, and power distribution, providing further opportunities for growth and market expansion in the polyphenylene segment.

Market Opportunity: Penetration into Healthcare and Medical Devices

An opportunity for growth in the polyphenylene market lies in penetration into healthcare and medical devices. Polyphenylene materials, due to their biocompatibility, sterilizability, and resistance to chemicals and bodily fluids, hold promise for various medical applications, including surgical instruments, diagnostic equipment, implantable devices, and medical packaging. As the demand for advanced medical devices and personalized healthcare solutions continues to rise, driven by aging populations and increasing healthcare expenditures, there is a growing need for materials that can meet stringent regulatory requirements and deliver reliable performance in medical applications. By leveraging their inherent properties and collaborating with medical device manufacturers and healthcare providers, polyphenylene suppliers can explore opportunities to expand their presence in the medical sector, contributing to advancements in healthcare technology and improving patient outcomes.

Polyphenylene Market Share Analysis: Polyphenylene Sulfide (PPS) segment generated the highest revenue in 2024

Polyphenylene Sulfide (PPS) is the largest segment within the polyphenylene market. In particular, PPS exhibits exceptional properties such as high thermal stability, chemical resistance, flame retardancy, and mechanical strength, making it a preferred choice across various industries. Its ability to withstand harsh environments and extreme temperatures makes it particularly suitable for automotive, electrical and electronics, and industrial applications. In the automotive sector, PPS is widely used in components such as fuel system parts, electrical connectors, and under-the-hood applications due to its heat resistance and dimensional stability. Moreover, the increasing demand for lightweight materials to improve fuel efficiency and reduce emissions further boosts the adoption of PPS in automotive manufacturing. Additionally, the electrical and electronics industry relies on PPS for its excellent electrical insulation properties, contributing to the growing demand for consumer electronics, appliances, and electrical components. As industries continue to prioritize performance, reliability, and sustainability, the dominance of PPS in the polyphenylene market is expected to persist, driven by its diverse applications and superior properties.

Polyphenylene Market Share Analysis: Electrical & Electronics is poised to register the fastest CAGR over the forecast period

The Electrical & Electronics segment is the fastest-growing within the polyphenylene market. In particular, the proliferation of electronic devices, advancements in technology, and the increasing digitization of industries fuel the demand for high-performance materials like polyphenylene. Polyphenylene's exceptional electrical insulation properties, thermal stability, and chemical resistance make it indispensable in a wide range of electrical and electronic applications, including connectors, sockets, switches, and circuit boards. Additionally, the growing adoption of electric vehicles (EVs), renewable energy systems, and smart devices further boosts the demand for polyphenylene in the Electrical & Electronics sector. Moreover, stringent regulations regarding energy efficiency and safety standards in electronics manufacturing drive the preference for durable and reliable materials like polyphenylene. As the demand for innovative electronic products continues to rise globally, the Electrical & Electronics segment is poised for significant growth, solidifying its position as the fastest-growing segment in the polyphenylene market.

Polyphenylene Market Share Analysis: Engineering Plastics segment generated the highest revenue in 2024

Within the Polyphenylene market, the Engineering Plastics segment is the largest. Engineering plastics, including polyphenylene, are extensively utilized in a wide range of applications due to their exceptional mechanical properties, thermal stability, chemical resistance, and dimensional stability. Polyphenylene-based engineering plastics find extensive usage in automotive components, electrical and electronic devices, industrial machinery, and consumer goods. Their ability to replace traditional materials like metal and other plastics in demanding applications due to their lightweight nature and superior performance attributes contributes significantly to their widespread adoption. Moreover, the increasing focus on sustainability and the drive towards lightweighting in various industries further boost the demand for polyphenylene-based engineering plastics. As industries continue to seek innovative solutions to enhance product performance and efficiency, the Engineering Plastics segment is expected to maintain its dominance in the polyphenylene market, solidifying its position as the largest segment.

Polyphenylene Market

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Polyphenylene Companies Profiled in the Study

Asahi Kasei Corp

Cancarb Ltd

Celanese Corp

Chevron Phillips Chemical Company LLC

Daicel Corp

DIC Corp

Ensinger GmbH

Kureha Corp

LG Chem Ltd

Mitsubishi Chemical Corp

Polyplastics Co. Ltd

RTP Company

Ryan Plastics Ltd

Solvay SA

Songhan Plastic Technology Co. Ltd

Teijin Ltd

Toray Industries Inc

Tosoh Corp

Zhejiang Xinhecheng Special Materials Co. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Polyphenylene Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Polyphenylene Market Size Outlook, $ Million, 2021 to 2032

3.2 Polyphenylene Market Outlook by Type, $ Million, 2021 to 2032

3.3 Polyphenylene Market Outlook by Product, $ Million, 2021 to 2032

3.4 Polyphenylene Market Outlook by Application, $ Million, 2021 to 2032

3.5 Polyphenylene Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Polyphenylene Industry

4.2 Key Market Trends in Polyphenylene Industry

4.3 Potential Opportunities in Polyphenylene Industry

4.4 Key Challenges in Polyphenylene Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Polyphenylene Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Polyphenylene Market Outlook by Segments

7.1 Polyphenylene Market Outlook by Segments, $ Million, 2021- 2032

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

8 North America Polyphenylene Market Analysis and Outlook To 2032

8.1 Introduction to North America Polyphenylene Markets in 2024

8.2 North America Polyphenylene Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Polyphenylene Market size Outlook by Segments, 2021-2032

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

9 Europe Polyphenylene Market Analysis and Outlook To 2032

9.1 Introduction to Europe Polyphenylene Markets in 2024

9.2 Europe Polyphenylene Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Polyphenylene Market Size Outlook by Segments, 2021-2032

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

10 Asia Pacific Polyphenylene Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Polyphenylene Markets in 2024

10.2 Asia Pacific Polyphenylene Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Polyphenylene Market size Outlook by Segments, 2021-2032

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

11 South America Polyphenylene Market Analysis and Outlook To 2032

11.1 Introduction to South America Polyphenylene Markets in 2024

11.2 South America Polyphenylene Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Polyphenylene Market size Outlook by Segments, 2021-2032

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

12 Middle East and Africa Polyphenylene Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Polyphenylene Markets in 2024

12.2 Middle East and Africa Polyphenylene Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Polyphenylene Market size Outlook by Segments, 2021-2032

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Asahi Kasei Corp

Cancarb Ltd

Celanese Corp

Chevron Phillips Chemical Company LLC

Daicel Corp

DIC Corp

Ensinger GmbH

Kureha Corp

LG Chem Ltd

Mitsubishi Chemical Corp

Polyplastics Co. Ltd

RTP Company

Ryan Plastics Ltd

Solvay SA

Songhan Plastic Technology Co. Ltd

Teijin Ltd

Toray Industries Inc

Tosoh Corp

Zhejiang Xinhecheng Special Materials Co. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Polyphenylene Sulfide (PPS)

Polyphenylene Ether/Oxide (PPE/PPO)

Others

By End-User

Automotive

Electrical & Electronics

Industrial

Coatings

Others

By Application

Composites

Engineering Plastics

High Performance Lubricants

Filter Bags

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)