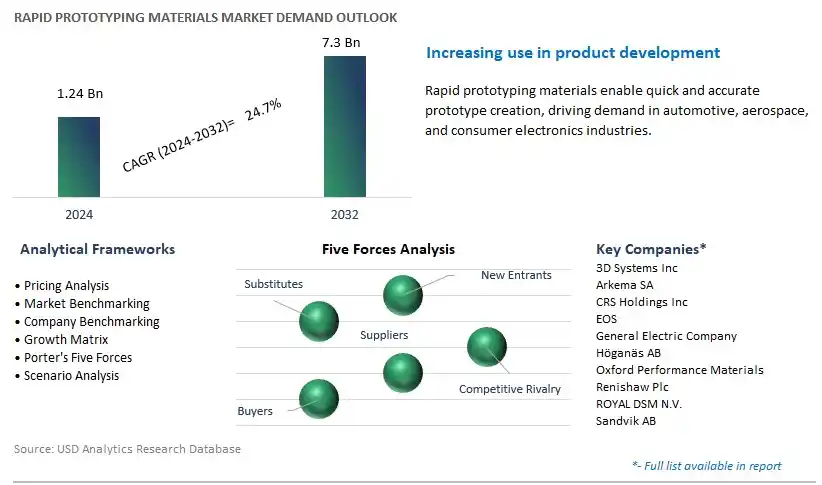

Global Rapid Prototyping Materials Market Size is valued at $1.24 Billion in 2024 and is forecast to register a growth rate (CAGR) of 24.7% to reach $7.3 Billion by 2032.

The global Rapid Prototyping Materials Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Polymers, Metals, Ceramics), By Form (Filament, Ink, Powder), By End-User (Aerospace & Defense, Healthcare, Transportation, Consumer Goods & Electronics, Manufacturing & Construction), By Function (Conceptual Model, Functional Prototype).

An Introduction to Rapid Prototyping Materials Market in 2024

In 2024, the rapid prototyping materials market is witnessing robust growth driven by the increasing adoption of additive manufacturing technologies such as 3D printing across diverse industries such as automotive, aerospace, healthcare, and consumer goods. Rapid prototyping materials encompass a wide range of polymers, metals, ceramics, and composites used to produce functional prototypes, concept models, and production tooling with speed, accuracy, and cost-effectiveness. The automotive and aerospace industries are major drivers of demand for rapid prototyping materials, with applications ranging from design validation and functional testing to customized parts production and spare parts manufacturing, benefiting from the ability to iterate designs rapidly and reduce time-to-market. Further, the healthcare sector utilizes rapid prototyping materials for medical device development, surgical planning, and patient-specific implants, contributing to personalized healthcare solutions and improved patient outcomes. Additionally, the consumer goods industry leverages additive manufacturing for product customization, small-batch production, and supply chain optimization, enabling innovative product designs and on-demand manufacturing capabilities. With advancements in material science, additive manufacturing technologies, and design software, the rapid prototyping materials market is poised for d growth, driven by innovations in material formulations, process optimization, and end-user applications.

Rapid Prototyping Materials Market Competitive Landscape

The market report analyses the leading companies in the industry including 3D Systems Inc, Arkema SA, CRS Holdings Inc, EOS, General Electric Company, Höganäs AB, Oxford Performance Materials, Renishaw Plc, ROYAL DSM N.V., Sandvik AB, and others.

Rapid Prototyping Materials Market Dynamics

Market Trend: Advancements in Additive Manufacturing Technologies

One prominent market trend in rapid prototyping materials is the continuous advancements in additive manufacturing technologies. As 3D printing capabilities evolve, there is a growing demand for innovative materials that can meet the complex requirements of rapid prototyping across various industries. Manufacturers are increasingly focusing on developing new materials with improved properties such as enhanced strength, durability, flexibility, and heat resistance to address the evolving needs of prototyping applications. This trend is driving the exploration and adoption of novel materials compatible with advanced additive manufacturing processes, including fused deposition modeling (FDM), stereolithography (SLA), selective laser sintering (SLS), and multi-material printing.

Market Driver: Demand for Faster Product Development Cycles

A key market driver for rapid prototyping materials is the demand for faster product development cycles in industries such as automotive, aerospace, consumer goods, and healthcare. In today's competitive market landscape, companies are under pressure to accelerate their time-to-market while maintaining product quality and innovation. Rapid prototyping offers a cost-effective and efficient solution to iterate designs, test functionalities, and validate concepts in a shorter time frame. As a result, there is a growing need for materials that can enable rapid prototyping processes to produce functional prototypes with high precision, accuracy, and repeatability. The imperative to reduce lead times and gain a competitive edge is thus fueling the demand for advanced rapid prototyping materials that can streamline the product development workflow.

Market Opportunity: Customization and Personalization in Manufacturing

An emerging opportunity in the rapid prototyping materials market lies in catering to the increasing demand for customization and personalization in manufacturing. Consumers today seek products that are tailored to their individual preferences and needs, driving manufacturers to adopt flexible production methods such as additive manufacturing to accommodate customization requirements. Rapid prototyping materials play a crucial role in enabling the production of customized parts, components, and products with complex geometries, intricate designs, and personalized features. By offering a diverse range of materials that can support customization and personalization, manufacturers can capitalize on this opportunity to tap into niche markets, enhance customer satisfaction, and differentiate their offerings in the highly competitive landscape. Additionally, the rise of digital manufacturing technologies and the advent of Industry 4.0 present opportunities for integrating rapid prototyping materials into digital workflows for on-demand manufacturing and mass customization.

Rapid Prototyping Materials Market Share Analysis: Polymers segment generated the highest revenue in 2024

Polymers emerge as the largest segment in the Rapid Prototyping Materials market due to their widespread adoption, versatility, and cost-effectiveness in various prototyping applications. Polymers offer a diverse range of properties, including flexibility, durability, and ease of processing, making them suitable for rapid prototyping across industries such as automotive, aerospace, consumer goods, and healthcare. Rapid prototyping with polymers enables engineers and designers to quickly iterate and validate designs, reducing time-to-market and development costs. Additionally, polymers are available in a variety of formulations and grades, allowing for customization of mechanical, thermal, and aesthetic properties to meet specific prototyping requirements. Furthermore, advancements in polymer additive manufacturing technologies, such as stereolithography (SLA), fused deposition modeling (FDM), and selective laser sintering (SLS), have expanded the capabilities and applications of polymer-based rapid prototyping, further driving their dominance in the market. As industries continue to prioritize innovation, product development, and prototyping efficiency, the demand for polymers in rapid prototyping materials is expected to remain strong, solidifying their position as the largest segment in the Rapid Prototyping Materials market.

Rapid Prototyping Materials Market Share Analysis: Powder segment generated the highest revenue in 2024

The powder segment is the fastest-growing segment in the Rapid Prototyping Materials market, driven by the increasing adoption of powder-based additive manufacturing technologies such as selective laser sintering (SLS) and binder jetting. Powder-based prototyping offers potential advantages, including high resolution, intricate detailing, and the ability to produce complex geometries without the need for support structures. Additionally, powder-based materials enable the fabrication of functional prototypes with a wide range of mechanical, thermal, and chemical properties, catering to diverse prototyping needs across industries such as aerospace, automotive, healthcare, and consumer goods. Moreover, advancements in powder materials, including metal alloys, polymers, and ceramics, have expanded the applications of powder-based prototyping to include end-use parts production, tooling, and rapid manufacturing. As industries continue to adopt additive manufacturing for rapid prototyping and production, the demand for powder-based materials is expected to experience rapid growth, solidifying powder as the fastest-growing segment in the Rapid Prototyping Materials market.

Rapid Prototyping Materials Market Share Analysis: Consumer Goods & Electronics segment generated the highest revenue in 2024

The consumer goods & electronics segment is the largest segment in the Rapid Prototyping Materials market due to the widespread adoption of rapid prototyping technologies in product development and innovation within the consumer electronics, appliances, and consumer goods industries. This segment encompasses a wide range of applications, including the development of smartphones, wearable devices, home appliances, toys, and other consumer products. Rapid prototyping enables manufacturers to quickly iterate and refine designs, test functionalities, and introduce new products to market faster, addressing evolving consumer preferences and market trends. Additionally, the consumer goods & electronics industry demands materials with specific properties such as high strength, heat resistance, and aesthetic appeal, which can be achieved through various rapid prototyping technologies and materials. With the continuous advancements in additive manufacturing technologies and the growing demand for customized and personalized products, the consumer goods & electronics segment is expected to maintain its dominance in the Rapid Prototyping Materials market.

Rapid Prototyping Materials Market Share Analysis: Functional Prototype is poised to register the fastest CAGR over the forecast period

The functional prototype segment is the fastest-growing segment in the Rapid Prototyping Materials market, fuelled by the increasing demand for functional testing and validation of product designs across industries. Functional prototypes are physical representations of end-use parts or products that closely mimic the intended functionality and performance characteristics. These prototypes allow engineers and designers to evaluate the feasibility, functionality, and performance of a design in real-world conditions, enabling early detection of design flaws, optimization of features, and validation of product specifications. Additionally, functional prototypes serve as valuable tools for communication and collaboration between cross-functional teams, stakeholders, and clients, facilitating informed decision-making and accelerating the product development process. As industries increasingly adopt additive manufacturing technologies for functional prototyping to reduce time-to-market, minimize development costs, and enhance product quality, the demand for rapid prototyping materials suitable for functional prototypes is expected to experience rapid growth, solidifying functional prototypes as the fastest-growing segment in the Rapid Prototyping Materials market.

Rapid Prototyping Materials Market

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional PrototypeCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Rapid Prototyping Materials Companies Profiled in the Study

3D Systems Inc

Arkema SA

CRS Holdings Inc

EOS

General Electric Company

Höganäs AB

Oxford Performance Materials

Renishaw Plc

ROYAL DSM N.V.

Sandvik AB

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Rapid Prototyping Materials Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Rapid Prototyping Materials Market Size Outlook, $ Million, 2021 to 2032

3.2 Rapid Prototyping Materials Market Outlook by Type, $ Million, 2021 to 2032

3.3 Rapid Prototyping Materials Market Outlook by Product, $ Million, 2021 to 2032

3.4 Rapid Prototyping Materials Market Outlook by Application, $ Million, 2021 to 2032

3.5 Rapid Prototyping Materials Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Rapid Prototyping Materials Industry

4.2 Key Market Trends in Rapid Prototyping Materials Industry

4.3 Potential Opportunities in Rapid Prototyping Materials Industry

4.4 Key Challenges in Rapid Prototyping Materials Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Rapid Prototyping Materials Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Rapid Prototyping Materials Market Outlook by Segments

7.1 Rapid Prototyping Materials Market Outlook by Segments, $ Million, 2021- 2032

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

8 North America Rapid Prototyping Materials Market Analysis and Outlook To 2032

8.1 Introduction to North America Rapid Prototyping Materials Markets in 2024

8.2 North America Rapid Prototyping Materials Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Rapid Prototyping Materials Market size Outlook by Segments, 2021-2032

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

9 Europe Rapid Prototyping Materials Market Analysis and Outlook To 2032

9.1 Introduction to Europe Rapid Prototyping Materials Markets in 2024

9.2 Europe Rapid Prototyping Materials Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Rapid Prototyping Materials Market Size Outlook by Segments, 2021-2032

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

10 Asia Pacific Rapid Prototyping Materials Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Rapid Prototyping Materials Markets in 2024

10.2 Asia Pacific Rapid Prototyping Materials Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Rapid Prototyping Materials Market size Outlook by Segments, 2021-2032

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

11 South America Rapid Prototyping Materials Market Analysis and Outlook To 2032

11.1 Introduction to South America Rapid Prototyping Materials Markets in 2024

11.2 South America Rapid Prototyping Materials Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Rapid Prototyping Materials Market size Outlook by Segments, 2021-2032

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

12 Middle East and Africa Rapid Prototyping Materials Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Rapid Prototyping Materials Markets in 2024

12.2 Middle East and Africa Rapid Prototyping Materials Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Rapid Prototyping Materials Market size Outlook by Segments, 2021-2032

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

3D Systems Inc

Arkema SA

CRS Holdings Inc

EOS

General Electric Company

Höganäs AB

Oxford Performance Materials

Renishaw Plc

ROYAL DSM N.V.

Sandvik AB

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Polymers

Metals

Ceramics

By Form

Filament

Ink

Powder

By End-User

Aerospace & Defense

Healthcare

Transportation

Consumer Goods & Electronics

Manufacturing & Construction

By Function

Conceptual Model

Functional Prototype

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)