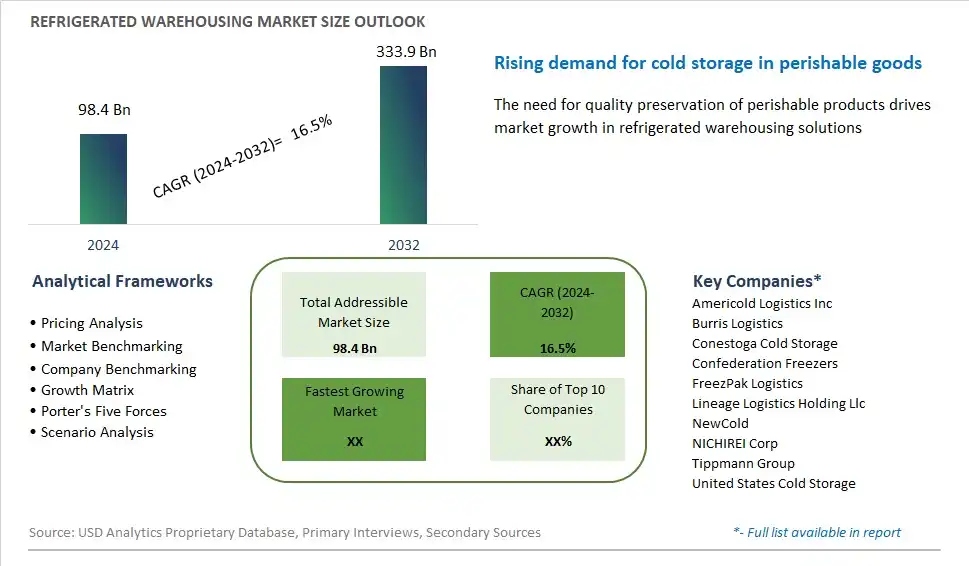

Global Refrigerated Warehousing Market Size is valued at $98.4 Billion in 2024 and is forecast to register a growth rate (CAGR) of 16.5% to reach $333.9 Billion by 2032.

The global Refrigerated Warehousing Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Private & Semi-Private, Public), By Temperature Range (Chilled (0°C to 15°C), Frozen (-18°C to -25°C), Deep-frozen (Below -25°C)), By Application (Fruits & Vegetables, Dairy Products, Meat, Seafood, Pharmaceuticals, Others)

An Introduction to Refrigerated Warehousing Market

Refrigerated warehousing facilities are storage facilities equipped with refrigeration systems to maintain temperature-controlled environments for the storage of perishable goods such as fresh produce, frozen foods, and pharmaceuticals in 2024. These facilities play a crucial role in the cold chain, providing temporary storage for temperature-sensitive products before distribution to retailers, wholesalers, and consumers. Refrigerated warehousing facilities are equipped with temperature monitoring systems, humidity control, and security measures to ensure product integrity, safety, and compliance with regulatory requirements. With the growth of e-commerce, online grocery delivery, and global trade in perishable goods, the market for refrigerated warehousing is expanding, driven by investments in cold storage infrastructure, automation, and energy efficiency that enable manufacturers, distributors, and logistics providers to meet the growing demand for refrigerated storage capacity, maintain product quality, and optimize supply chain efficiency.

Refrigerated Warehousing Competitive Landscape

The market report analyses the leading companies in the industry including Americold Logistics Inc, Burris Logistics, Conestoga Cold Storage, Confederation Freezers, FreezPak Logistics, Lineage Logistics Holding Llc, NewCold, NICHIREI Corp, Tippmann Group, United States Cold Storage, and Others.

Refrigerated Warehousing Market Dynamics

Refrigerated Warehousing Market Trend: Increased Demand for Cold Storage Facilities

One prominent market trend in refrigerated warehousing is the increased demand for cold storage facilities. With the growth of e-commerce, globalization, and the food industry, there's a rising need for temperature-controlled storage solutions to accommodate perishable goods such as fresh produce, frozen foods, pharmaceuticals, and vaccines. This trend is driven by evolving consumer preferences for fresh and high-quality products, as well as regulatory requirements for maintaining the cold chain integrity throughout the supply chain. As a result, the demand for refrigerated warehousing services is on the rise, with businesses seeking reliable facilities equipped with advanced refrigeration systems, temperature monitoring technology, and efficient logistics capabilities to ensure product safety and compliance with industry standards.

Market Driver: Expansion of the Cold Chain Logistics Network

A key driver propelling the market for refrigerated warehousing is the expansion of the cold chain logistics network to support the growing demand for temperature-controlled storage and distribution services. As companies seek to reach new markets, streamline their supply chains, and improve operational efficiency, there's a growing reliance on refrigerated warehousing facilities strategically located near key transportation hubs, ports, and production centers. Moreover, the increasing complexity of supply chain operations, along with the need for just-in-time inventory management and quick order fulfillment, drives the demand for flexible and scalable cold storage solutions. This expansion of the cold chain logistics network is fueled by investments in infrastructure, technology, and automation to meet the diverse needs of various industries, including food and beverage, pharmaceuticals, healthcare, and biotechnology.

Market Opportunity: Integration of Digitalization and Smart Technologies

An opportunity within the refrigerated warehousing market lies in the integration of digitalization and smart technologies to enhance operational efficiency, visibility, and sustainability. With the advent of Industry 4.0 and the Internet of Things (IoT), there's a vast potential to optimize cold storage operations through real-time data monitoring, predictive analytics, and automation. By leveraging IoT sensors, RFID tags, and cloud-based platforms, refrigerated warehousing providers can gain insights into temperature conditions, inventory levels, and equipment performance, enabling proactive maintenance, inventory optimization, and energy management. Furthermore, there's an opportunity to implement blockchain technology to enhance transparency, traceability, and food safety across the cold chain, ensuring compliance with regulatory requirements and meeting consumer demands for product authenticity and quality assurance. By embracing digitalization and smart technologies, refrigerated warehousing companies can improve their competitiveness, attract new customers, and unlock new revenue streams in the dynamic and evolving cold storage industry.

Refrigerated Warehousing Market Share Analysis: Private & Semi-Private held the dominant market share in 2024

The private and semi-private segment holds the largest share in the refrigerated warehousing market due to the specialized storage needs and stringent quality control requirements of industries such as food and pharmaceuticals. Private and semi-private refrigerated warehouses are owned or operated by companies for their exclusive use or shared among a limited number of clients, offering customized storage solutions tailored to their specific needs. These facilities provide controlled temperature and humidity environments to preserve the freshness, quality, and safety of perishable goods, including dairy, meat, seafood, fruits, vegetables, and pharmaceutical products. Further, private and semi-private refrigerated warehouses offer enhanced security, traceability, and confidentiality of stored goods, making them preferred by companies with sensitive or high-value products. Additionally, as regulations and food safety standards become more stringent, especially in developed economies, companies increasingly opt for private and semi-private refrigerated warehousing solutions to ensure compliance and mitigate risks associated with product spoilage or contamination. As a result, the private and semi-private segment maintains its dominance in the refrigerated warehousing market, catering to the evolving needs of industries requiring specialized cold chain logistics solutions.

Refrigerated Warehousing Market Share Analysis: Deep-frozen market is poised to register the fastest growth rae over the forecast period to 2032

The deep-frozen segment is experiencing rapid growth in the refrigerated warehousing market due to the increasing demand for storage facilities capable of maintaining ultra-low temperatures required for preserving highly perishable goods, including specialty frozen foods, pharmaceuticals, and biologics. Deep-frozen warehouses provide storage environments below -25°C, ensuring the long-term preservation of products and preventing degradation or spoilage. With the rising popularity of convenience foods, ready-to-eat meals, and frozen desserts, as well as the expansion of the pharmaceutical industry and the growing demand for biopharmaceutical products requiring stringent temperature control, the need for deep-frozen storage facilities is escalating. Additionally, advancements in cold chain logistics, refrigeration technology, and energy efficiency are driving the development of specialized deep-frozen warehousing solutions, further fueling the growth of this segment. As companies strive to ensure product quality, safety, and regulatory compliance, the deep-frozen segment is expected to continue its rapid expansion, offering opportunities for innovation and investment in the refrigerated warehousing market.

Refrigerated Warehousing Market Share Analysis: Meat held the dominant market share in 2024

The meat segment dominates the refrigerated warehousing market due to the substantial volume and specialized storage requirements of meat products, including beef, poultry, pork, and processed meats. Meat products are highly perishable and require strict temperature control and hygiene standards to maintain freshness, prevent spoilage, and ensure food safety. Refrigerated warehouses equipped with temperature-controlled environments provide optimal conditions for storing meat products at temperatures below 0°C to preserve their quality and extend shelf life. Additionally, the global demand for meat products continues to rise, driven by population growth, urbanization, and changing dietary preferences, particularly in emerging economies. As a result, meat companies and retailers rely heavily on refrigerated warehousing facilities to store, distribute, and deliver meat products efficiently and effectively. With increasing consumer awareness of food safety and quality standards, the meat segment is expected to maintain its dominance in the refrigerated warehousing market, driving continued growth and investment in cold chain logistics infrastructure.

Refrigerated Warehousing Market Segmentation

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Refrigerated Warehousing Companies Profiled in the Study

Americold Logistics Inc

Burris Logistics

Conestoga Cold Storage

Confederation Freezers

FreezPak Logistics

Lineage Logistics Holding Llc

NewCold

NICHIREI Corp

Tippmann Group

United States Cold Storage

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Refrigerated Warehousing Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Refrigerated Warehousing Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Refrigerated Warehousing Market Share by Company, 2023

4.1.2. Product Offerings of Leading Refrigerated Warehousing Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Refrigerated Warehousing Market Drivers

6.2. Refrigerated Warehousing Market Challenges

6.6. Refrigerated Warehousing Market Opportunities

6.4. Refrigerated Warehousing Market Trends

Chapter 7. Global Refrigerated Warehousing Market Outlook Trends

7.1. Global Refrigerated Warehousing Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Refrigerated Warehousing Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Refrigerated Warehousing Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Chapter 8. Global Refrigerated Warehousing Regional Analysis and Outlook

8.1. Global Refrigerated Warehousing Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Refrigerated Warehousing Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Refrigerated Warehousing Regional Analysis and Outlook

8.2.2. Canada Refrigerated Warehousing Regional Analysis and Outlook

8.2.3. Mexico Refrigerated Warehousing Regional Analysis and Outlook

8.3. Europe Refrigerated Warehousing Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Refrigerated Warehousing Regional Analysis and Outlook

8.3.2. France Refrigerated Warehousing Regional Analysis and Outlook

8.3.3. United Kingdom Refrigerated Warehousing Regional Analysis and Outlook

8.3.4. Spain Refrigerated Warehousing Regional Analysis and Outlook

8.3.5. Italy Refrigerated Warehousing Regional Analysis and Outlook

8.3.6. Russia Refrigerated Warehousing Regional Analysis and Outlook

8.3.7. Rest of Europe Refrigerated Warehousing Regional Analysis and Outlook

8.4. Asia Pacific Refrigerated Warehousing Revenue (USD Million) by Country (2021-2032)

8.4.1. China Refrigerated Warehousing Regional Analysis and Outlook

8.4.2. Japan Refrigerated Warehousing Regional Analysis and Outlook

8.4.3. India Refrigerated Warehousing Regional Analysis and Outlook

8.4.4. South Korea Refrigerated Warehousing Regional Analysis and Outlook

8.4.5. Australia Refrigerated Warehousing Regional Analysis and Outlook

8.4.6. South East Asia Refrigerated Warehousing Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Refrigerated Warehousing Regional Analysis and Outlook

8.5. South America Refrigerated Warehousing Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Refrigerated Warehousing Regional Analysis and Outlook

8.5.2. Argentina Refrigerated Warehousing Regional Analysis and Outlook

8.5.3. Rest of South America Refrigerated Warehousing Regional Analysis and Outlook

8.6. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Refrigerated Warehousing Regional Analysis and Outlook

8.6.2. Africa Refrigerated Warehousing Regional Analysis and Outlook

Chapter 9. North America Refrigerated Warehousing Analysis and Outlook

9.1. North America Refrigerated Warehousing Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Refrigerated Warehousing Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Refrigerated Warehousing Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Refrigerated Warehousing Revenue (USD Million) by Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Chapter 10. Europe Refrigerated Warehousing Analysis and Outlook

10.1. Europe Refrigerated Warehousing Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Refrigerated Warehousing Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Refrigerated Warehousing Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Refrigerated Warehousing Revenue (USD Million) by Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Chapter 11. Asia Pacific Refrigerated Warehousing Analysis and Outlook

11.1. Asia Pacific Refrigerated Warehousing Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Refrigerated Warehousing Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Refrigerated Warehousing Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Refrigerated Warehousing Revenue (USD Million) by Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Chapter 12. South America Refrigerated Warehousing Analysis and Outlook

12.1. South America Refrigerated Warehousing Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Refrigerated Warehousing Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Refrigerated Warehousing Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Refrigerated Warehousing Revenue (USD Million) by Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Chapter 13. Middle East and Africa Refrigerated Warehousing Analysis and Outlook

13.1. Middle East and Africa Refrigerated Warehousing Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) by Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Chapter 14. Refrigerated Warehousing Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Americold Logistics Inc

Burris Logistics

Conestoga Cold Storage

Confederation Freezers

FreezPak Logistics

Lineage Logistics Holding Llc

NewCold

NICHIREI Corp

Tippmann Group

United States Cold Storage

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Refrigerated Warehousing Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Refrigerated Warehousing Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Refrigerated Warehousing Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Refrigerated Warehousing Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Refrigerated Warehousing Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Refrigerated Warehousing Market Share (%) By Regions (2021-2032)

Table 12 North America Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Table 15 South America Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Table 17 North America Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Table 18 North America Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Table 19 North America Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Table 26 South America Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Table 27 South America Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Table 28 South America Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Refrigerated Warehousing Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Refrigerated Warehousing Market Share (%) By Regions (2023)

Figure 6. North America Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 12. France Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 12. China Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 14. India Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Refrigerated Warehousing Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Refrigerated Warehousing Revenue (USD Million) By Product (2021-2032)

By Type

Private & Semi-Private

Public

By Temperature Range

Chilled (0°C to 15°C)

Frozen (-18°C to -25°C)

Deep-frozen (Below -25°C)

By Application

Fruits & Vegetables

Dairy Products

Meat

Seafood

Pharmaceuticals

-Vaccines

-Blood Banking

-Others

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)