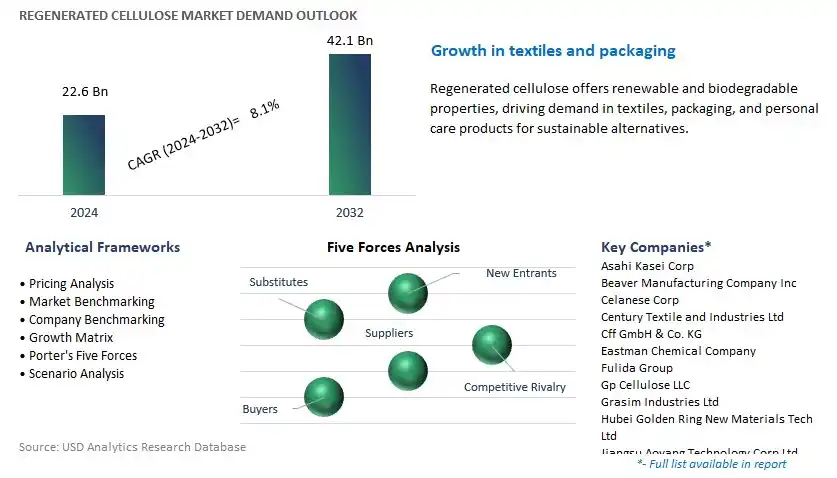

Global Regenerated Cellulose Market Size is valued at $22.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 8.1% to reach $42.1 Billion by 2032.

The global Regenerated Cellulose Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Fiber, Film), By Source (Wood-Pulp, Non-Wood Pulp, Recycled Pulp/De-inked Pulp), By Manufacturing Process (Viscose, Cuprammonium, N-methyl-morpholine-N-oxide (NMMO), Acetate), By End-User (Fabric, Automotive, Agriculture, Packaging, Others).

An Introduction to Regenerated Cellulose Market in 2024

In 2024, the regenerated cellulose market is experiencing significant growth driven by the increasing demand for sustainable fibers, films, and packaging materials in industries such as textiles, food packaging, and personal care. Regenerated cellulose, derived from natural sources such as wood pulp, cotton linters, and bamboo, offers properties such as biodegradability, moisture absorption, and softness, making it an attractive alternative to synthetic materials. The textile and apparel industry is a major consumer of regenerated cellulose fibers, with applications ranging from clothing and home textiles to nonwoven fabrics and industrial textiles, benefiting from their comfort, breathability, and eco-friendly credentials. Further, the food packaging sector utilizes regenerated cellulose films and coatings for applications such as flexible packaging, barrier films, and compostable wraps, contributing to sustainable packaging solutions and reducing plastic waste. Additionally, the personal care industry relies on regenerated cellulose for products such as wipes, diapers, and hygiene products, leveraging their softness, absorbency, and biodegradability. With a growing emphasis on sustainability, circular economy principles, and consumer awareness of environmental impact, the regenerated cellulose market is poised for d growth, driven by innovations in fiber production, processing technologies, and end-use applications.

Regenerated Cellulose Market Competitive Landscape

The market report analyses the leading companies in the industry including Asahi Kasei Corp, Beaver Manufacturing Company Inc, Celanese Corp, Century Textile and Industries Ltd, Cff GmbH & Co. KG, Eastman Chemical Company, Fulida Group, Gp Cellulose LLC, Grasim Industries Ltd, Hubei Golden Ring New Materials Tech Ltd, Jiangsu Aoyang Technology Corp Ltd, Kelheim Fibres GmbH, Kobo Products Inc, Lenzing AG, Sateri, Sniace S.A., Tangshan Sanyou Group. Ltd, Xinxiang Chemical Fiber Co. Ltd, and others.

Regenerated Cellulose Market Dynamics

Market Trend: Growing Demand for Sustainable Packaging Solutions

One prominent market trend in regenerated cellulose is the growing demand for sustainable packaging solutions. With increasing awareness of environmental issues and plastic pollution, there is a rising preference for eco-friendly packaging materials derived from renewable sources. Regenerated cellulose, commonly known as viscose or rayon, offers a sustainable alternative to traditional packaging materials such as plastic and paper. Its biodegradability, recyclability, and renewable nature make it an attractive choice for various packaging applications across industries such as food and beverage, cosmetics, and consumer goods. This trend is driven by consumer preferences for eco-friendly products and regulatory initiatives aimed at reducing single-use plastics and promoting sustainable packaging solutions.

Market Driver: Shift Towards Circular Economy and Waste Reduction

A key market driver for regenerated cellulose is the shift towards a circular economy and waste reduction initiatives. As governments, businesses, and consumers increasingly recognize the importance of waste management and resource conservation, there is a growing emphasis on circular economy principles that prioritize the reuse, recycling, and regeneration of materials. Regenerated cellulose fits into this framework by offering a closed-loop solution for packaging materials, where waste products can be regenerated into new cellulose-based products through recycling and upcycling processes. The drive towards waste reduction, circularity, and resource efficiency is propelling the demand for regenerated cellulose as a sustainable alternative to conventional packaging materials.

Market Opportunity: Innovation in Advanced Cellulose-Based Materials

An emerging opportunity in the regenerated cellulose market lies in innovation in advanced cellulose-based materials. While traditional viscose or rayon has been widely used for decades, advancements in materials science and technology have opened up new possibilities for developing novel cellulose-based materials with enhanced properties and functionalities. Opportunities exist to innovate cellulose-based materials with improved strength, durability, barrier properties, and biodegradability to meet the diverse requirements of modern packaging applications. By investing in research and development, companies can capitalize on the opportunity to create next-generation cellulose-based materials that offer superior performance, sustainability, and versatility, thereby expanding the market potential for regenerated cellulose in various industries beyond packaging.

Regenerated Cellulose Market Share Analysis: Fiber Type segment generated the highest revenue in 2024

The Fiber type segment is the largest segment within the Regenerated Cellulose Market. Regenerated cellulose fibers, such as viscose rayon and lyocell, are widely utilized in textile and apparel industries for their versatility, softness, and eco-friendly properties. Viscose rayon, the most common type of regenerated cellulose fiber, is extensively used in the production of clothing, home textiles, and non-woven fabrics due to its affordability and ease of processing. On the other hand, lyocell, a newer generation of regenerated cellulose fiber, offers enhanced strength, moisture absorption, and biodegradability, making it increasingly favored in sustainable fashion and textile applications. Moreover, the growing demand for eco-friendly and sustainable materials in the textile industry, coupled with increasing consumer awareness about the environmental impact of synthetic fibers, drives the adoption of regenerated cellulose fibers. As textile manufacturers and brands prioritize sustainability and circularity in their supply chains, the fiber type segment is expected to maintain its dominance in the regenerated cellulose market, driving continued growth and innovation in fiber technologies.

Regenerated Cellulose Market Share Analysis: Recycled Pulp/De-inked Pulp Source is poised to register the fastest CAGR over the forecast period

The Recycled Pulp/De-inked Pulp source segment is the fastest-growing segment within the Regenerated Cellulose Market. Recycled pulp, derived from post-consumer waste paper and de-inked pulp from recycled paper products, offers a sustainable and eco-friendly alternative to conventional wood-based and non-wood-based pulps. With increasing environmental concerns and regulations promoting circular economy principles, there's a growing emphasis on utilizing recycled materials in the production of regenerated cellulose fibers and films. Additionally, advancements in recycling technologies have improved the quality and availability of recycled pulp, making it viable for a wide range of applications across industries. Moreover, the growing demand for sustainable and ethically sourced materials in textile, packaging, and specialty paper industries further drives the adoption of recycled pulp in regenerated cellulose production. As companies and consumers alike prioritize environmental sustainability and resource efficiency, the recycled pulp/de-inked pulp source segment is poised to experience sustained growth, driving innovation and investment in recycling infrastructure and processes.

Regenerated Cellulose Market Share Analysis: Viscose Manufacturing Process segment generated the highest revenue in 2024

The Viscose manufacturing process segment is the largest segment within the Regenerated Cellulose Market. Viscose, also known as rayon, is one of the oldest and most widely used methods for producing regenerated cellulose fibers and films. The viscose process involves dissolving cellulose pulp in a solvent, typically sodium hydroxide, and carbon disulfide, to create a viscous solution that can be extruded into fibers or cast into films. Viscose fibers are prized for their softness, drapability, and affordability, making them popular in textile and apparel industries for a wide range of applications. Additionally, the viscose process offers versatility in terms of fiber properties and can be easily modified to produce specialty fibers with enhanced characteristics such as high absorbency, strength, or flame retardancy. Moreover, advancements in viscose production technology, including closed-loop systems and sustainable sourcing of raw materials, further cement its position as the preferred manufacturing process in the regenerated cellulose market. As the textile industry continues to expand globally, driven by changing consumer preferences and sustainability trends, the viscose manufacturing process segment is expected to maintain its dominance, driving continued growth and innovation in regenerated cellulose materials.

Regenerated Cellulose Market Share Analysis: Packaging is poised to register the fastest CAGR over the forecast period

The Packaging end-user segment is the fastest-growing segment within the Regenerated Cellulose Market. Regenerated cellulose materials, such as films and coatings derived from cellulose fibers or pulp, are increasingly favored in packaging applications due to their eco-friendly properties, versatility, and biodegradability. As the global packaging industry faces mounting pressure to reduce its environmental footprint and transition towards sustainable alternatives, regenerated cellulose is a promising solution. Cellulose-based packaging materials offer excellent barrier properties against moisture and gases, making them suitable for a wide range of applications including food packaging, cosmetics packaging, and pharmaceutical packaging. Additionally, consumer preferences for eco-friendly and recyclable packaging solutions further drive the adoption of regenerated cellulose materials in packaging applications. Moreover, regulatory initiatives promoting the use of sustainable materials and bans on single-use plastics contribute to the accelerated growth of the packaging segment in the regenerated cellulose market. As companies across industries strive to meet sustainability goals and address consumer demands for greener packaging options, the packaging end-user segment is poised to experience sustained growth, driving innovation and investment in cellulose-based packaging materials and technologies.

Regenerated Cellulose Market

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Regenerated Cellulose Companies Profiled in the Study

Asahi Kasei Corp

Beaver Manufacturing Company Inc

Celanese Corp

Century Textile and Industries Ltd

Cff GmbH & Co. KG

Eastman Chemical Company

Fulida Group

Gp Cellulose LLC

Grasim Industries Ltd

Hubei Golden Ring New Materials Tech Ltd

Jiangsu Aoyang Technology Corp Ltd

Kelheim Fibres GmbH

Kobo Products Inc

Lenzing AG

Sateri

Sniace S.A.

Tangshan Sanyou Group. Ltd

Xinxiang Chemical Fiber Co. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Regenerated Cellulose Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Regenerated Cellulose Market Size Outlook, $ Million, 2021 to 2032

3.2 Regenerated Cellulose Market Outlook by Type, $ Million, 2021 to 2032

3.3 Regenerated Cellulose Market Outlook by Product, $ Million, 2021 to 2032

3.4 Regenerated Cellulose Market Outlook by Application, $ Million, 2021 to 2032

3.5 Regenerated Cellulose Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Regenerated Cellulose Industry

4.2 Key Market Trends in Regenerated Cellulose Industry

4.3 Potential Opportunities in Regenerated Cellulose Industry

4.4 Key Challenges in Regenerated Cellulose Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Regenerated Cellulose Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Regenerated Cellulose Market Outlook by Segments

7.1 Regenerated Cellulose Market Outlook by Segments, $ Million, 2021- 2032

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

8 North America Regenerated Cellulose Market Analysis and Outlook To 2032

8.1 Introduction to North America Regenerated Cellulose Markets in 2024

8.2 North America Regenerated Cellulose Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Regenerated Cellulose Market size Outlook by Segments, 2021-2032

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

9 Europe Regenerated Cellulose Market Analysis and Outlook To 2032

9.1 Introduction to Europe Regenerated Cellulose Markets in 2024

9.2 Europe Regenerated Cellulose Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Regenerated Cellulose Market Size Outlook by Segments, 2021-2032

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

10 Asia Pacific Regenerated Cellulose Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Regenerated Cellulose Markets in 2024

10.2 Asia Pacific Regenerated Cellulose Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Regenerated Cellulose Market size Outlook by Segments, 2021-2032

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

11 South America Regenerated Cellulose Market Analysis and Outlook To 2032

11.1 Introduction to South America Regenerated Cellulose Markets in 2024

11.2 South America Regenerated Cellulose Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Regenerated Cellulose Market size Outlook by Segments, 2021-2032

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

12 Middle East and Africa Regenerated Cellulose Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Regenerated Cellulose Markets in 2024

12.2 Middle East and Africa Regenerated Cellulose Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Regenerated Cellulose Market size Outlook by Segments, 2021-2032

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Asahi Kasei Corp

Beaver Manufacturing Company Inc

Celanese Corp

Century Textile and Industries Ltd

Cff GmbH & Co. KG

Eastman Chemical Company

Fulida Group

Gp Cellulose LLC

Grasim Industries Ltd

Hubei Golden Ring New Materials Tech Ltd

Jiangsu Aoyang Technology Corp Ltd

Kelheim Fibres GmbH

Kobo Products Inc

Lenzing AG

Sateri

Sniace S.A.

Tangshan Sanyou Group. Ltd

Xinxiang Chemical Fiber Co. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Fiber

Film

By Source

Wood-Pulp

Non-Wood Pulp

Recycled Pulp/De-inked Pulp

By Manufacturing Process

Viscose

Cuprammonium

N-methyl-morpholine-N-oxide (NMMO)

Acetate

By End-User

Fabric

Automotive

Agriculture

Packaging

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)