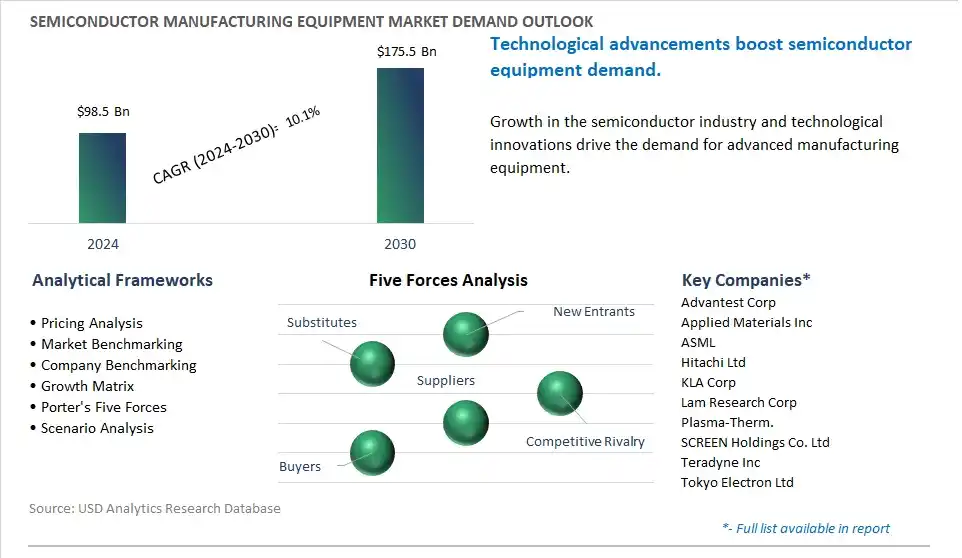

The global Semiconductor Manufacturing Equipment Market is poised to register a 10.1% CAGR from $98.5 Billion in 2024 to $175.5 Billion in 2030.

The global Semiconductor Manufacturing Equipment Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Front-end Equipment (Lithography, Wafer Surface Conditioning, Wafer Cleaning, Deposition, Others), By Back-end Equipment (Assembly and Packaging, Dicing, Metrology, Bonding, Wafer Testing/ IC Testing), By Fab Facility Equipment (Automation, Chemical Control, Gas Control, Others), By Product (Memory, Foundry, Logic, MPU, Discrete, Analog, MEMS, Others), By Dimension (2D ICs, 2.5D ICs, 3D ICs), By Supply Chain Participant (IDM Firms, OSAT Companies, Foundries).

An Introduction to Global Semiconductor Manufacturing Equipment Market in 2024

The future of semiconductor manufacturing equipment is shaped by key trends such as technological innovation, miniaturization, and the growing demand for advanced electronic devices. Semiconductor manufacturing equipment encompasses a wide range of tools and machinery used in the fabrication of integrated circuits (ICs) and semiconductor devices, including wafer processing, lithography, deposition, etching, and testing equipment. With the rapid evolution of semiconductor technology and the emergence of new applications such as artificial intelligence (AI), Internet of Things (IoT), and 5G connectivity, there is a constant demand for smaller, faster, and more energy-efficient semiconductor devices. As a result, semiconductor manufacturers are investing in next-generation manufacturing equipment capable of producing chips with higher transistor densities, improved performance, and enhanced functionality. Moreover, as the semiconductor industry transitions to advanced nodes such as 7nm, 5nm, and beyond, there is a need for cutting-edge lithography tools, process control systems, and metrology equipment to meet stringent specifications and yield requirements. Additionally, with the increasing complexity of semiconductor designs and the rise of heterogeneous integration, there is a growing demand for equipment that enables multi-chip packaging, 3D integration, and system-on-chip (SoC) integration to support the development of high-performance computing and advanced electronics. Furthermore, as industries such as automotive, healthcare, and telecommunications adopt semiconductor technology for autonomous vehicles, medical devices, and telecommunications infrastructure, there is a growing need for customized semiconductor manufacturing solutions tailored to specific application requirements. As semiconductor manufacturers invest in research and development to stay ahead of technological advancements and market demands, the semiconductor manufacturing equipment market will continue to evolve with innovations in process technology, equipment automation, and smart manufacturing solutions to enable the production of advanced semiconductor devices for the digital age.

Semiconductor Manufacturing Equipment Market Competitive Landscape

The market report analyses the leading companies in the industry including Advantest Corp, Applied Materials Inc, ASML, Hitachi Ltd, KLA Corp, Lam Research Corp, Plasma-Therm., SCREEN Holdings Co. Ltd, Teradyne Inc, Tokyo Electron Ltd.

Semiconductor Manufacturing Equipment Market Dynamics

Semiconductor Manufacturing Equipment Market Trend: Advancement in Semiconductor Technology and Manufacturing Processes

A significant trend in the market for semiconductor manufacturing equipment is the continuous advancement in semiconductor technology and manufacturing processes. With the rapid evolution of electronic devices, such as smartphones, tablets, IoT devices, and automotive electronics, there is a constant demand for smaller, faster, and more power-efficient semiconductors. Semiconductor manufacturers are investing in advanced equipment and technologies to keep pace with Moore's Law and meet the requirements of next-generation semiconductor devices. The trend drives the adoption of semiconductor manufacturing equipment that enables finer feature sizes, higher processing speeds, and enhanced functionality, thereby facilitating the production of cutting-edge semiconductor chips for various applications.

Semiconductor Manufacturing Equipment Market Driver: Increasing Demand for Semiconductor Devices in Various Industries

A primary driver for the market of semiconductor manufacturing equipment is the increasing demand for semiconductor devices in various industries. Semiconductors are essential components in electronic products used across sectors such as telecommunications, computing, automotive, healthcare, aerospace, and consumer electronics. The proliferation of connected devices, digitalization initiatives, and emerging technologies such as 5G, artificial intelligence (AI), Internet of Things (IoT), and electric vehicles drives the demand for semiconductor chips with higher performance, greater functionality, and lower power consumption. Semiconductor manufacturers invest in advanced equipment to ramp up production capacity, improve yields, and meet the growing demand for semiconductor devices worldwide.

Semiconductor Manufacturing Equipment Market Opportunity: Expansion into Emerging Technologies and Applications

An opportunity in the market for semiconductor manufacturing equipment lies in the expansion into emerging technologies and applications. As new technologies and applications emerge, such as AI, 5G, quantum computing, augmented reality (AR), and autonomous vehicles, there is a growing demand for specialized semiconductor devices tailored to meet the unique requirements of these applications. Semiconductor equipment manufacturers can seize this opportunity by developing and offering equipment optimized for manufacturing chips with specific features, such as high-speed processing, low latency, energy efficiency, and reliability. By aligning with the needs of emerging technologies and applications, semiconductor equipment suppliers can position themselves at the forefront of innovation, capture new market segments, and drive growth in the dynamic semiconductor industry.

Semiconductor Manufacturing Equipment Market Share Analysis: Lithography generated the highest revenue in 2024

Lithography equipment plays a critical role in semiconductor fabrication by transferring circuit patterns onto silicon wafers with precision and accuracy. As semiconductor technology advances, the demand for higher resolution and smaller feature sizes increases, driving the need for advanced lithography equipment capable of achieving finer patterning. Lithography equipment enables the production of complex integrated circuits, including microprocessors, memory chips, and other semiconductor devices used in various electronic products. Additionally, with the emergence of new applications such as artificial intelligence, autonomous vehicles, and 5G connectivity, there's a growing demand for semiconductor chips with advanced functionalities, further fueling the demand for lithography equipment. Given its indispensable role in semiconductor manufacturing and its continuous innovation to meet evolving industry requirements, lithography equipment remains the largest segment in the Semiconductor Manufacturing Equipment Market.

Semiconductor Manufacturing Equipment Market Share Analysis: Wafer Testing/IC Testing segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

As semiconductor devices become increasingly complex and integrated, the importance of thorough testing and quality assurance during the manufacturing process has grown significantly. Wafer testing/IC testing equipment plays a crucial role in ensuring the functionality, reliability, and performance of semiconductor chips before they are assembled into final products. With the rise of applications such as artificial intelligence, Internet of Things (IoT), and autonomous vehicles, there's a surging demand for semiconductor chips with higher processing power, improved efficiency, and enhanced reliability. This demand necessitates more advanced and efficient testing solutions to meet the stringent requirements of modern semiconductor devices. Additionally, with the growing complexity of semiconductor designs and the shrinking time-to-market windows, semiconductor manufacturers are investing in wafer testing/IC testing equipment to streamline their production processes and accelerate product development cycles. These factors contribute to the rapid growth of the Wafer Testing/IC Testing segment in the Semiconductor Manufacturing Equipment Market.

Semiconductor Manufacturing Equipment Market Share Analysis: Automation segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

Automation in fab facility equipment encompasses a wide range of technologies and systems designed to enhance efficiency, productivity, and precision throughout the semiconductor manufacturing process. As semiconductor fabrication becomes increasingly complex and demanding, there is a growing need for automation solutions to streamline operations, reduce manual intervention, and minimize errors. Automation technologies such as robotics, advanced control systems, and artificial intelligence are revolutionizing the semiconductor manufacturing landscape by enabling faster throughput, tighter process control, and improved yield rates. Additionally, automation enhances flexibility and scalability, allowing semiconductor manufacturers to adapt to changing market demands and rapidly introduce new products. With the relentless pursuit of higher performance, smaller form factors, and lower production costs in semiconductor devices, the demand for automation solutions in fab facility equipment is witnessing significant growth. Accordingly, the Automation segment is the fastest-growing segment in the Semiconductor Manufacturing Equipment Market.

Semiconductor Manufacturing Equipment Market Report Segmentation

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Semiconductor Manufacturing Equipment Companies Profiled in the Market Study

Advantest Corp

Applied Materials Inc

ASML

Hitachi Ltd

KLA Corp

Lam Research Corp

Plasma-Therm.

SCREEN Holdings Co. Ltd

Teradyne Inc

Tokyo Electron Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Semiconductor Manufacturing Equipment Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Semiconductor Manufacturing Equipment Market Size Outlook, $ Million, 2021 to 2030

3.2 Semiconductor Manufacturing Equipment Market Outlook by Type, $ Million, 2021 to 2030

3.3 Semiconductor Manufacturing Equipment Market Outlook by Product, $ Million, 2021 to 2030

3.4 Semiconductor Manufacturing Equipment Market Outlook by Application, $ Million, 2021 to 2030

3.5 Semiconductor Manufacturing Equipment Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Semiconductor Manufacturing Equipment Industry

4.2 Key Market Trends in Semiconductor Manufacturing Equipment Industry

4.3 Potential Opportunities in Semiconductor Manufacturing Equipment Industry

4.4 Key Challenges in Semiconductor Manufacturing Equipment Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Semiconductor Manufacturing Equipment Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Semiconductor Manufacturing Equipment Market Outlook by Segments

7.1 Semiconductor Manufacturing Equipment Market Outlook by Segments, $ Million, 2021- 2030

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

8 North America Semiconductor Manufacturing Equipment Market Analysis and Outlook To 2030

8.1 Introduction to North America Semiconductor Manufacturing Equipment Markets in 2024

8.2 North America Semiconductor Manufacturing Equipment Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Semiconductor Manufacturing Equipment Market size Outlook by Segments, 2021-2030

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

9 Europe Semiconductor Manufacturing Equipment Market Analysis and Outlook To 2030

9.1 Introduction to Europe Semiconductor Manufacturing Equipment Markets in 2024

9.2 Europe Semiconductor Manufacturing Equipment Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Semiconductor Manufacturing Equipment Market Size Outlook by Segments, 2021-2030

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

10 Asia Pacific Semiconductor Manufacturing Equipment Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Semiconductor Manufacturing Equipment Markets in 2024

10.2 Asia Pacific Semiconductor Manufacturing Equipment Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Semiconductor Manufacturing Equipment Market size Outlook by Segments, 2021-2030

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

11 South America Semiconductor Manufacturing Equipment Market Analysis and Outlook To 2030

11.1 Introduction to South America Semiconductor Manufacturing Equipment Markets in 2024

11.2 South America Semiconductor Manufacturing Equipment Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Semiconductor Manufacturing Equipment Market size Outlook by Segments, 2021-2030

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

12 Middle East and Africa Semiconductor Manufacturing Equipment Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Semiconductor Manufacturing Equipment Markets in 2024

12.2 Middle East and Africa Semiconductor Manufacturing Equipment Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Semiconductor Manufacturing Equipment Market size Outlook by Segments, 2021-2030

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Advantest Corp

Applied Materials Inc

ASML

Hitachi Ltd

KLA Corp

Lam Research Corp

Plasma-Therm.

SCREEN Holdings Co. Ltd

Teradyne Inc

Tokyo Electron Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Front-end Equipment

Lithography

Wafer Surface Conditioning

Wafer Cleaning

Deposition

Others

By Back-end Equipment

Assembly and Packaging

Dicing

Metrology

Bonding

Wafer Testing/ IC Testing

By Fab Facility Equipment

Automation

Chemical Control

Gas Control

Others

By Product

Memory

Foundry

Logic

MPU

Discrete

Analog

MEMS

Others

By Dimension

2D ICs

2.5D ICs

3D ICs

By Supply Chain Participant

IDM Firms

OSAT Companies

Foundries

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)