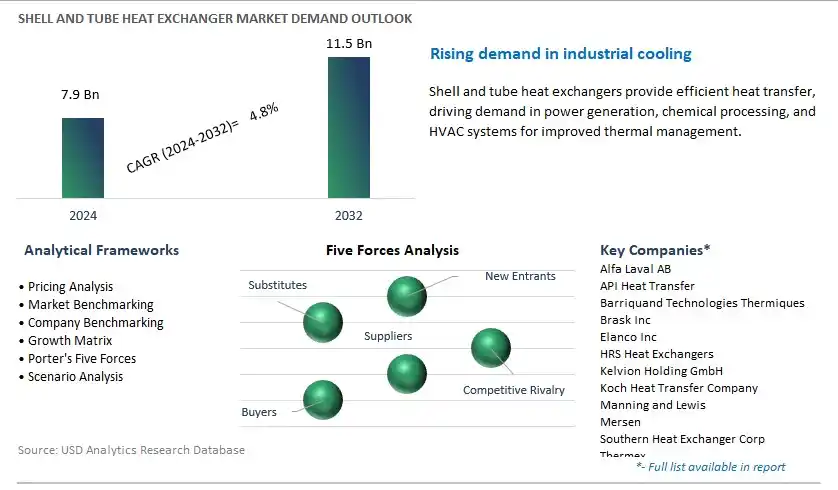

Global Shell and Tube Heat Exchanger Market Size is valued at $7.9 Billion in 2024 and is forecast to register a growth rate (CAGR) of 4.8% to reach $11.5 Billion by 2032.

The global Shell and Tube Heat Exchanger Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Haste Alloy, Titanium, Nickel & Nickel Alloys, Tantalum, Steel, Others), By End-User (Power Generation, Petrochemicals, Chemical, Food & Beverages, HVAC & Refrigerators, Pulp & Paper, Others).

An Introduction to Shell and Tube Heat Exchanger Market in 2024

In 2024, the shell and tube heat exchanger market remains vital for efficient heat transfer and thermal management in various industrial processes, HVAC systems, and power generation applications. Shell and tube heat exchangers consist of a bundle of tubes housed within a cylindrical shell, allowing for the exchange of heat between two fluids, typically a hot fluid flowing inside the tubes and a cold fluid circulating around the shell. These exchangers are widely used in industries such as oil and gas, chemical processing, food and beverage, and power plants for applications such as heating, cooling, condensing, and evaporation. The oil and gas sector is a major consumer of shell and tube heat exchangers, employing them in processes such as crude oil refining, natural gas processing, and petrochemical production for heat recovery and temperature control. Additionally, shell and tube heat exchangers find applications in HVAC systems for commercial buildings, industrial facilities, and power plants, providing efficient heat exchange in heating, ventilation, air conditioning, and refrigeration processes. With advancements in design optimization, material selection, and manufacturing technologies, the shell and tube heat exchanger market s to evolve to meet the growing demand for energy-efficient and environmentally friendly heat transfer solutions in various industries and applications.

Shell and Tube Heat Exchanger Market Competitive Landscape

The market report analyses the leading companies in the industry including Alfa Laval AB, API Heat Transfer, Barriquand Technologies Thermiques, Brask Inc, Elanco Inc, HRS Heat Exchangers, Kelvion Holding GmbH, Koch Heat Transfer Company, Manning and Lewis, Mersen, Southern Heat Exchanger Corp, Thermex, Tinita Engineering Pvt. Ltd, WCR Inc, Xylem Inc, and others.

Shell and Tube Heat Exchanger Market Dynamics

Market Trend: Increasing Adoption of Shell and Tube Heat Exchangers in Energy-Efficient Applications

One prominent market trend in shell and tube heat exchangers is the increasing adoption of these systems in energy-efficient applications. As industries and commercial sectors strive to reduce energy consumption and operating costs, there is a growing demand for heat exchangers that can efficiently transfer heat between fluid streams with minimal energy loss. Shell and tube heat exchangers offer high thermal efficiency, versatility, and reliability, making them ideal for a wide range of heating, cooling, and heat recovery applications in industries such as oil and gas, chemical processing, power generation, HVAC, and refrigeration. This trend is driven by the need for sustainable and eco-friendly solutions that optimize energy usage and enhance process efficiency in various industrial and commercial processes.

Market Driver: Growth in Industrialization and Process Industries

A key market driver for shell and tube heat exchangers is the growth in industrialization and process industries. With the expansion of manufacturing, refining, and chemical processing sectors worldwide, there is a continuous demand for heat exchangers to support various production processes, such as heating, cooling, condensation, and evaporation. Shell and tube heat exchangers play a vital role in facilitating heat transfer between different fluid streams, enabling efficient operation and temperature control in industrial equipment and systems. The drive for increased production capacity, improved product quality, and regulatory compliance fuels the demand for shell and tube heat exchangers as essential components of process equipment in diverse industries.

Market Opportunity: Development of Advanced Materials and Design Innovations

An emerging opportunity in the shell and tube heat exchanger market lies in the development of advanced materials and design innovations. While traditional shell and tube heat exchangers have been widely used for decades, there is potential to enhance their performance, durability, and efficiency through material advancements and design optimizations. Opportunities exist to explore new materials with improved corrosion resistance, thermal conductivity, and mechanical properties, such as high-performance alloys, composite materials, and nanostructured coatings. Additionally, there is room for innovation in heat exchanger design to optimize fluid flow patterns, enhance heat transfer efficiency, and reduce pressure drop across the exchanger. By investing in research and development initiatives focused on material science and engineering design, manufacturers can develop next-generation shell and tube heat exchangers that meet the evolving needs of industrial processes, improve energy efficiency, and drive sustainable growth in the heat exchanger market.

Shell & Tube Heat Exchanger Market Share Analysis: Steel segment generated the highest revenue in 2024

The largest segment in the Shell & Tube Heat Exchanger Market is typically the "Steel" segment. This is primarily due to the widespread use of steel in various industrial applications and its suitability for manufacturing heat exchangers. Steel offers potential advantages, including high strength, durability, corrosion resistance, and cost-effectiveness, making it a preferred material choice for constructing shell and tube heat exchangers. Additionally, steel is readily available, easy to fabricate, and compatible with a wide range of fluids and operating conditions, further contributing to its dominance in the market. While materials like Haste Alloy, Titanium, Nickel & Nickel Alloys, and Tantalum offer specific benefits in terms of corrosion resistance and thermal conductivity, steel remains the most commonly used material for shell and tube heat exchangers across industries due to its overall performance and cost-efficiency.

Shell & Tube Heat Exchanger Market Share Analysis: Petrochemicals is poised to register the fastest CAGR over the forecast period

The Petrochemicals segment is the fastest-growing segment in the Shell & Tube Heat Exchanger Market, driven by the expansion of the petrochemical industry and increasing demand for heat exchange solutions in petrochemical processing facilities. Shell and tube heat exchangers play a critical role in petrochemical plants by facilitating heat transfer processes involved in refining crude oil and processing various petrochemical products. These heat exchangers are utilized in processes such as distillation, condensation, evaporation, and heating of fluids to optimize energy efficiency and ensure product quality. With the growing global demand for petrochemical products, driven by industrialization, urbanization, and infrastructure development, petrochemical companies are investing in capacity expansion and modernization projects, leading to a surge in the demand for heat exchangers. Additionally, advancements in technology and increasing regulations regarding energy efficiency and emissions drive the adoption of efficient heat exchange solutions in the petrochemical industry, further fuelling the growth of the Petrochemicals segment in the Shell & Tube Heat Exchanger Market.

Shell and Tube Heat Exchanger Market

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Shell and Tube Heat Exchanger Companies Profiled in the Study

Alfa Laval AB

API Heat Transfer

Barriquand Technologies Thermiques

Brask Inc

Elanco Inc

HRS Heat Exchangers

Kelvion Holding GmbH

Koch Heat Transfer Company

Manning and Lewis

Mersen

Southern Heat Exchanger Corp

Thermex

Tinita Engineering Pvt. Ltd

WCR Inc

Xylem Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Shell and Tube Heat Exchanger Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Shell and Tube Heat Exchanger Market Size Outlook, $ Million, 2021 to 2032

3.2 Shell and Tube Heat Exchanger Market Outlook by Type, $ Million, 2021 to 2032

3.3 Shell and Tube Heat Exchanger Market Outlook by Product, $ Million, 2021 to 2032

3.4 Shell and Tube Heat Exchanger Market Outlook by Application, $ Million, 2021 to 2032

3.5 Shell and Tube Heat Exchanger Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Shell and Tube Heat Exchanger Industry

4.2 Key Market Trends in Shell and Tube Heat Exchanger Industry

4.3 Potential Opportunities in Shell and Tube Heat Exchanger Industry

4.4 Key Challenges in Shell and Tube Heat Exchanger Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Shell and Tube Heat Exchanger Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Shell and Tube Heat Exchanger Market Outlook by Segments

7.1 Shell and Tube Heat Exchanger Market Outlook by Segments, $ Million, 2021- 2032

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

8 North America Shell and Tube Heat Exchanger Market Analysis and Outlook To 2032

8.1 Introduction to North America Shell and Tube Heat Exchanger Markets in 2024

8.2 North America Shell and Tube Heat Exchanger Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Shell and Tube Heat Exchanger Market size Outlook by Segments, 2021-2032

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

9 Europe Shell and Tube Heat Exchanger Market Analysis and Outlook To 2032

9.1 Introduction to Europe Shell and Tube Heat Exchanger Markets in 2024

9.2 Europe Shell and Tube Heat Exchanger Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Shell and Tube Heat Exchanger Market Size Outlook by Segments, 2021-2032

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

10 Asia Pacific Shell and Tube Heat Exchanger Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Shell and Tube Heat Exchanger Markets in 2024

10.2 Asia Pacific Shell and Tube Heat Exchanger Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Shell and Tube Heat Exchanger Market size Outlook by Segments, 2021-2032

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

11 South America Shell and Tube Heat Exchanger Market Analysis and Outlook To 2032

11.1 Introduction to South America Shell and Tube Heat Exchanger Markets in 2024

11.2 South America Shell and Tube Heat Exchanger Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Shell and Tube Heat Exchanger Market size Outlook by Segments, 2021-2032

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

12 Middle East and Africa Shell and Tube Heat Exchanger Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Shell and Tube Heat Exchanger Markets in 2024

12.2 Middle East and Africa Shell and Tube Heat Exchanger Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Shell and Tube Heat Exchanger Market size Outlook by Segments, 2021-2032

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Alfa Laval AB

API Heat Transfer

Barriquand Technologies Thermiques

Brask Inc

Elanco Inc

HRS Heat Exchangers

Kelvion Holding GmbH

Koch Heat Transfer Company

Manning and Lewis

Mersen

Southern Heat Exchanger Corp

Thermex

Tinita Engineering Pvt. Ltd

WCR Inc

Xylem Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Haste Alloy

Titanium

Nickel & Nickel Alloys

Tantalum

Steel

-Stainless Steel

-Duplex Steel

-Carbon Steel

-Super Duplex Steel

-Others

Others

By End-User

Power Generation

Petrochemicals

Chemical

Food & Beverages

HVAC & Refrigerators

Pulp & Paper

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)