Smart Helmet Market Overview: Connected Safety Features and Advanced Wearable Technologies

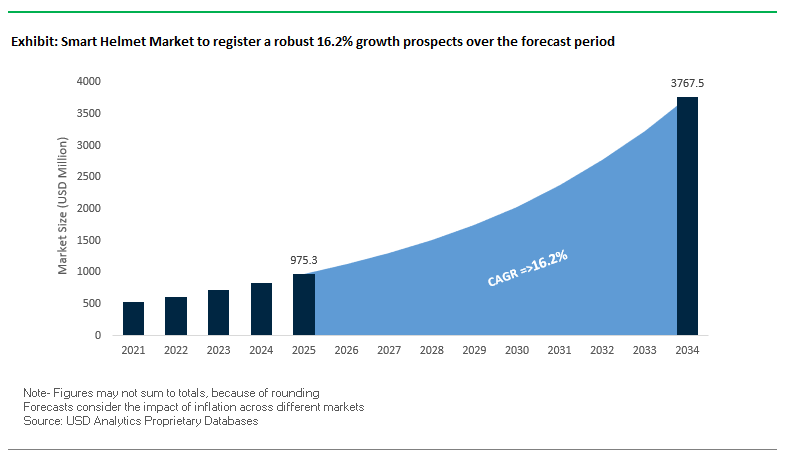

The global smart helmet market is projected to grow from $975.3 million in 2025 to $3,767 million by 2034, at a robust CAGR of 16.2%. Situated at the crossroads between personal protection equipment (PPE), wearable technology, and mobility safety solutions, the market is being driven by rising motorcycle usage, strict road safety regulations, and compliance with industrial safety standards. The segment is increasingly defined by its ability to incorporate AI-based functionality, advanced communication systems, health monitoring, and GPS navigation into protective headgear, enhancing safety and user experience.

Industry observers are noting firm adoption from motorcyclists, sports riders, and industrial workers spurred by high-profile product releases, government-sponsored safety campaigns, and technology collaborations between helmet makers and technology firms. Over 55% of the market is held by full-face helmet designs, appreciated for their enhanced safety and the ability to accommodate multiple smart features. Market growth is also being spurred by consumer interest in hands-free calls, with over 35% of models featuring Mesh Intercom systems that accommodate an unlimited number of callers.

Key Insights for Industry Professionals:

- Road Safety Imperative: U.S. recorded 40,990 road accidents in 2023, highlighting demand for advanced rider protection gear.

- Feature-Rich Designs: Over 33% of new launches include GPS, video recording, and health monitoring sensors.

- Industrial Adoption: Smart helmets are increasingly used in construction, mining, and manufacturing for safety compliance.

- Communication Advantage: Bluetooth headsets with up to 48 hours talk time and 110 hours standby are becoming standard.

- Global Demand Drivers: Urban mobility expansion and growth in emerging markets are accelerating uptake.

Strategic Expansions, Safety Innovations, and Cross-Industry Influence in Smart Helmet Market

The smart helmet industry has seen a series of strategic expansions from September 2023 to July 2025, focusing on safety innovation, market diversification, and high-end connectivity. In May 2024, Steelbird Helmets introduced its Fighter series, including an in-built Pin Lock-70 anti-fog shield, Bluetooth connectivity, and high-end safety features for motorcyclists looking for high-end comfort and technology. Similarly, in April 2024, Ather Energy introduced its Halo series, which includes high-grade safety certification in addition to internal padding and a protective shell, establishing the new standards for two-wheeler safety gear.

Industrial safety-oriented innovations are also making their mark on the market. In July 2025, Haws Corporation received its fourth SHARP certification in Nevada, emphasizing workplace safety best practices a standard for industrial intelligent helmet production. This is in line with increased PPE integration with IoT sensors and AI-driven monitoring systems. In September 2023, Indian company Takeward Innovation launched a helmet that will not allow bike ignition unless in use, focusing on theft prevention as well as on preventing accidents.

Cross-industry trends are influencing helmet design. Robotics integration, such as in October 2023 with automated cleaning solutions from Skyline Robotics, reflects the trend towards AI-enabling safety operations. Consumer electronics trends, such as immersive retail experiences such as June 2025's BSH Home Appliances' opening of Siemens store in India, reflect the growing significance of connected devices ecosystems, where smart helmets are part of a larger wearable tech ecosystem. Sponsorship-driven visibility, such as Adidas' September 2024 Liverpool FC tie-up, also reflects helmet makers' efforts to leverage brand partnerships to enter markets.

Trends and Opportunities Driving the Global Smart Helmet Market

AR HUD Integration Enhancing Professional Cycling and Motor Sports

Augmented Reality Head-Up Displays (AR HUDs) are becoming a revolutionary feature in the international smart helmet market, especially in professional cycling and high-speed motor racing. The systems display real-time performance and navigation information directly into the rider's field of view, allowing instant decision-making without visual distractions. Sophisticated models combine biometric performance monitoring tracking heart rate, cadence, and power output assisting athletes to optimize race strategies on the go. Adding rear-camera feeds into the HUD also removes blind spots, making the ride safer in competitive environments. Combined with mobile apps, riders can tailor their display settings, pre-load routes, and review post-ride performance, offering a seamless data-driven system that synergizes safety with athletic optimization.

AI-Enabled Construction Helmets Redefining Industrial Safety Standards

AI construction safety helmets are transforming industrial head protection through a change from passive shielding to active hazard avoidance. Equipped with sophisticated sensors, these helmets constantly track laborer vital signs like heart rate, temperature, and fatigue levels and sweep the environment for hazards such as chemical gas leaks or loud noise. AI-based processing in real-time analyzes this data and provides immediate audio, visual, or haptic warning to prevent any accidents. GPS functionality and automatic incident reporting further add to quicker emergency response times, especially in high-risk work areas. This forward-looking safety model is in harmony with more stringent occupational protection regulations globally, fueling demand in industries like construction, mining, and oil & gas.

Smart Helmet Fleet Solutions for Delivery and Logistics Operators

Delivery rider companies in the gig economy are a profitable market for smart helmet deployment, with GPS, AR navigation, and IoT connectivity built in to support safe and streamlined last-mile delivery. Fleet owners can utilize these helmets for real-time monitoring of riders, optimizing routes, and instant contact, increasing operational efficiency and worker safety. Functions such as accident alert, automatic SOS emergency alerts, and rear-view cameras reduce the risks in urban areas with high traffic. Through the integration of live performance analytics and predictive maintenance alerts, fleet management systems can minimize downtime, maximize delivery schedules, and enhance customer satisfaction making smart helmets a strategic investment for mass-scale logistics providers.

Child Safety Helmets with Integrated Impact Alerts for Parents

The smart helmet market for children presents a high-growth opportunity by integrating impact sensors and parental alert systems into sports and recreational headgear. When they sense serious impact, they will automatically send warnings with GPS coordinates to a parent's smartphone to allow for prompt response. In addition to crash detection, some of these models monitor sub-concussive impacts over time, providing parents and coaches with important information about the cumulative risks of head trauma. This is especially applicable to activities such as youth bicycling, skateboarding, and skiing, where injuries can be less apparent. By blending protective design with connected safety features, manufacturers can meet parental demand for advanced child safety solutions that deliver both peace of mind and tangible injury prevention.

Market Share Analysis of the Global Smart Helmet Market

Market Share by Component: Sensors Lead with Expanding Multi-Functional Integration

Sensors dominate the smart helmet component landscape, holding a 35% market share due to their critical role in impact detection, environmental monitoring, and biometric tracking. These sensor arrays enable features like crash alerts, air quality measurement, and real-time health monitoring, essential across both industrial and consumer segments. Communication systems, with a 30% share, are increasingly standard, offering Bluetooth connectivity, integrated microphones, and intercom functions for hands-free coordination in motorcycling, cycling, and worksite operations. Integrated video cameras are seeing rapid adoption among sports enthusiasts, delivery riders, and industrial inspectors for recording incidents or creating content. Navigation systems particularly AR-based solutions remain a premium feature but are gaining traction in logistics and professional sports where real-time guidance is critical.

.png)

Market Share by Technology: IoT-Enabled Helmets Driving Connected Safety Ecosystems

IoT-enabled smart helmets lead the technology segment with a 40% market share, reflecting their growing role in connected safety networks for fleet management, industrial monitoring, and performance optimization. These helmets transmit real-time data to cloud platforms, allowing for centralized analytics and incident reporting. Sensor-based technology follows closely at 30%, forming the backbone of both consumer and industrial smart helmet functionality. AI-powered solutions are rapidly expanding, offering predictive safety analytics, fatigue detection, and automated hazard identification. Augmented Reality (AR) technology, though still niche, is increasingly adopted in both industrial and sports helmets for overlaying navigation data, safety instructions, and remote expert guidance, signaling strong growth potential as hardware costs decline and application breadth expands.

Smart Helmet Market Competitive Landscape – Leading Players Defining Safety, Connectivity, and User-Centric Design

The smart helmet market is led by multinational corporations and specialized innovators leveraging technology integration, design excellence, and strategic market expansion to capture share across both consumer and industrial segments. Key players included are Sena Technologies, Inc., Forcite Helmet Systems Pty Ltd., LIVALL Tech Co., Ltd., Jarvish Inc., Bell Helmets, Daqri (a subsidiary of The Zentech Group), Torc Helmets, Lumos Helmet, CrossHelmet, 3M Company, Honeywell International Inc., Vuzix Corporation, TeamViewer AG, RealWear Inc., Safe-tech, Others.

Eicher Motors (Royal Enfield) – Blending Heritage with Smart Safety Innovations

Eicher Motors, by Royal Enfield, marries vintage motorcycling charm with cutting-edge safety technology. With 65% YoY export growth in Q1 FY26, the company is eyeing Southeast Asia, Europe, and Latin America. Strategic investments of ₹500 crore in EV R&D and 200 new global stores by 2030 put it on the path for long-term growth. Its intelligent helmet initiatives are backed by partnerships with technology collaborators, driving rider connectivity and safety.

KASK S.p.A. – Premium Italian Craftsmanship with Technological Excellence

KASK produces ergonomically superior helmets for cycling, skiing, and industry, with all production based in Italy. Latest introductions include a road model with aerodynamic profile and increased Protone Icon color options, appealing to performance-oriented and fashion-forward customers. Its strategic design balances functionality, safety standards compliance, and aesthetic value, earning it a prime position among professional and leisure uses.

SCHUBERTH GmbH – German Engineering with Motorsport Expertise

With close to a century of experience, SCHUBERTH utilizes its carbon lab, wind tunnel, and AI-based manufacturing processes to produce high-performance helmets. With expertise in noise reduction and embedded electronics, the company uses its Formula 1 engineering expertise in consumer products to deliver aerodynamics and comfort for road or track use.

3M Company – Industrial Safety Leadership through Material Science

3M smart helmets are mainly designed for industrial use, with Pressure Diffusion Technology to alleviate forehead pressure and a Uvicator™ UV indicator for optimal replacement timing. ANSI compliance and integration capability with earmuffs and communication devices make 3M a workplace PPE innovation leader.

Sena Technologies, Inc. – Pioneering Communication Systems for Helmets

Sena is distinguished by its Mesh Intercom technology, providing unlimited connectivity among users without interference. Its latest 60S series integrates Mesh 3.0, Harman Kardon audio, and AI noise suppression, serving motorcyclists and industrial workers who need clear, reliable communication in demanding situations.

United States: Regulatory Push and Consumer-Led Feature Adoption

The United States smart helmet market benefits from strict occupational safety regulations and a strong culture of innovation across industrial and consumer sectors. In construction, manufacturing, and energy, smart hard hats are increasingly deployed with integrated IoT sensors, AR displays, and AI-powered hazard detection to meet OSHA standards and improve on-site productivity. For consumer use, motorcyclists and cyclists are driving demand for helmets with Bluetooth connectivity, voice-assist integration, and GPS navigation overlays, aligning with the country’s preference for connected experiences. High-profile collaborations, such as Oakley’s partnership with twICEme, are introducing features like medical ID storage and emergency access, catering to both recreational users and first responders.

Industrial adoption is expanding beyond safety compliance into workflow optimization, with helmets capable of streaming live video, transmitting biometric data, and integrating with project management platforms. Emergency services including firefighting, policing, and disaster response are leveraging smart helmets to improve situational awareness and enable hands-free communications in critical operations. The U.S. market’s maturity, combined with a large base of early tech adopters, ensures continuous innovation and rapid commercial rollout, positioning the country as a leading driver of multi-sector smart helmet integration.

China: Policy-Driven Mass Adoption and Scalable Manufacturing Advantage

China’s smart helmet market has surged following the July 2020 government mandate requiring helmet use for e-bike riders, creating a massive consumer pool across urban and rural areas. With the world’s largest e-bike and motorcycle user base, the country presents unparalleled scale for smart helmet penetration. Domestic technology giants are introducing integrated communication and safety features Huawei’s “Helmetphone” being a notable example with voice commands, Bluetooth connectivity, and navigation support designed for the high-density urban commute.

In industrial and public health applications, China has demonstrated innovative deployments, such as thermal imaging smart helmets used for fever detection during COVID-19, underscoring the technology’s versatility. A robust manufacturing ecosystem enables low-cost, high-volume production while incorporating advanced materials and electronics. Domestic brands are also leveraging live-stream e-commerce platforms like Douyin and Tmall to drive rapid consumer adoption, reinforcing China’s role as both a leading market and the manufacturing backbone for the global smart helmet industry.

Germany: Engineering Excellence and Advanced Safety Integration

Germany’s smart helmet market thrives on precision engineering and high-tech innovation, particularly in automotive and motorcycle segments. The integration of augmented reality (AR) heads-up displays, AI-assisted hazard detection, and impact sensors reflects the country’s commitment to elevating road safety standards. Industrial safety regulations are also shaping demand, with smart helmets increasingly used in construction and manufacturing for real-time data collection, site navigation, and compliance tracking.

Consumer awareness campaigns and stringent EU safety directives are driving adoption rates, while a strong preference for premium, high-durability products aligns with Germany’s engineering reputation. Online retail has emerged as a growing sales channel, with both established and niche brands expanding their direct-to-consumer e-commerce strategies. Germany’s emphasis on safety, paired with technological sophistication, positions it as a trendsetter for integrated helmet safety solutions in Europe.

Japan: Workplace Safety Innovation and Precision Material Science

Japan’s smart helmet market is anchored by government-led workplace safety initiatives and an industry-wide push toward automation and real-time monitoring. Collaborative projects between construction firms and electronics manufacturers have led to helmets equipped with biometric sensors that detect heat stress and send alerts to supervisors, already deployed by over 100 companies nationwide. These systems align with Japan’s broader digital transformation goals, enhancing productivity and accident prevention.

Material innovation plays a key role, with Japanese manufacturers focusing on lightweight composites, advanced ventilation systems, and high-impact resistance materials. The country’s robust internet infrastructure supports cloud-connected helmets that enable remote oversight and data analysis. This integration of safety, durability, and connectivity ensures Japan remains at the forefront of specialized industrial smart helmet applications, while also catering to high-performance sports and motorcycling segments.

United Kingdom: Cycling Boom and Technology-Driven Market Expansion

The United Kingdom smart helmet market is benefiting from government cycling promotion programs and growing urban adoption of e-bikes. Heightened safety awareness, reinforced by public campaigns, has fueled demand for helmets with Bluetooth audio, GPS navigation, integrated lighting, and eco-friendly materials. UK consumers show strong interest in sustainable product lines, pushing brands to adopt recyclable shells and low-impact manufacturing processes.

Online retail is a dominant distribution channel, with brands leveraging e-commerce and digital marketing to reach cycling, motorcycling, and commuter audiences. The expanding e-bike market has created demand for specialized smart helmets with anti-theft tracking and battery monitoring integrations. This combination of urban mobility trends, sustainability focus, and digital retail strategies positions the UK as one of Europe’s most progressive markets for smart helmet adoption.

Australia: Homegrown Innovation and Rider-Centric Development

Australia’s smart helmet sector is defined by homegrown innovation from brands like Forcite Helmet Systems, which design ultra-light helmets with built-in cameras, Bluetooth controllers, and real-time navigation alerts. A strong community feedback model allows manufacturers to continuously refine product features, ensuring alignment with rider needs and local road conditions.

The market’s growth is supported by a high proportion of daily motorcycle commuters and recreational riders seeking connected, feature-rich gear. Advanced backend software systems provide personalized ride condition data, hazard alerts, and performance analytics, enhancing both safety and enjoyment. With rising demand for technology-infused protective equipment, Australia is emerging as a niche but influential player in shaping next-generation rider experience standards globally.

Smart Helmet Market Report Scope

Smart Helmet Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$975.3 Million

|

|

Market Size (2034)

|

$3767 Million

|

|

Market Growth Rate

|

16.2%

|

|

Segments

|

By Helmet Type (Full Face, Half Face, Smart Hard Hat), By Component (Communication System, Navigation System, Integrated Video Camera, Sensors (Impact, GPS, Temperature)), By Application (Consumer (Motorcycling, Cycling, Sports), Industrial (Construction, Manufacturing, Mining), Emergency Services (Firefighting, Law Enforcement)), By Connectivity (Bluetooth, Wi-Fi, Cellular), By Technology (Augmented Reality (AR), AI-powered, IoT-enabled, Sensor-based)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sena Technologies, Inc., Forcite Helmet Systems Pty Ltd., LIVALL Tech Co., Ltd., Jarvish Inc., Bell Helmets, Daqri (a subsidiary of The Zentech Group), Torc Helmets, Lumos Helmet, CrossHelmet, 3M Company, Honeywell International Inc., Vuzix Corporation, TeamViewer AG, RealWear Inc., Safe-tech, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Helmet Market Segmentation

By Helmet Type

- Full Face

- Half Face

- Smart Hard Hat

By Component

- Communication System

- Navigation System

- Integrated Video Camera

- Sensors

By Application

- Consumer

- Motorcycling

- Cycling

- Sports

- Industrial

- Construction

- Manufacturing

- Mining

- Emergency Services

- Firefighting

- Law Enforcement

By Connectivity

By Technology

- Augmented Reality (AR)

- AI-powered

- IoT-enabled

- Sensor-based

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Smart Helmet Market

- Sena Technologies Inc.

- Forcite Helmet Systems Pty Ltd.

- LIVALL Tech Co. Ltd.

- Jarvish Inc.

- Bell Helmets

- Daqri, a subsidiary of The Zentech Group

- Torc Helmets

- Lumos Helmet

- CrossHelmet

- 3M Company

- Honeywell International Inc.

- Vuzix Corporation

- TeamViewer AG

- RealWear Inc.

- Safe-tech

* List Not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the fast-evolving Smart Helmet Market, delivering analysis reviews of demand catalysts across consumer, industrial, and emergency-service use cases. It highlights breakthroughs in AR head-up displays, IoT telemetry, mesh intercoms, and AI-enabled safety analytics, while mapping regulatory, distribution, and pricing dynamics that shape adoption. Competitive moves, ecosystem partnerships, and go-to-market playbooks are benchmarked to reveal white spaces by technology, connectivity, and application. With granular market modeling to 2034 and evidence-backed strategic takeaways, this report is an essential resource for helmet OEMs, component suppliers, fleet operators, PPE distributors, investors, and policy stakeholders. Scope includes-

- Segmentation

- By Helmet Type: Full Face, Half Face, Smart Hard Hat

- By Component: Communication System, Navigation System, Integrated Video Camera, Sensors

- By Application: Consumer, Industrial, Emergency Services

- By Connectivity: Bluetooth, Wi-Fi, Cellular

- By Technology: Augmented Reality (AR), AI-powered, IoT-enabled, Sensor-based

- Geographic Scope: Coverage of 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historical baselines 2021–2024; forecasts 2025–2034 with scenarios and sensitivity tests.

- Companies: Analysis/profiles of 15+ players (e.g., Sena Technologies, Forcite, LIVALL, Jarvish, Bell, Daqri, Torc, Lumos, CrossHelmet, 3M, Honeywell, Vuzix, TeamViewer, RealWear, Safe-tech).

Methodology

USDAnalytics employed a mixed-methods approach combining executive interviews with helmet OEMs, chipset providers, connectivity platforms, industrial safety leaders, and channel partners, plus secondary intelligence from certifications, recalls, patents, procurement portals, and regulatory bulletins. We normalized shipment, ASP, and install-base data, triangulating with import/export codes and retailer sell-through to build bottom-up country models. A systems-dynamics forecast links unit adoption to drivers such as road-safety policy, e-bike penetration, industrial OSHA-style mandates, and feature attach rates (AR, AI, video, mesh). Competitive benchmarking uses a weighted index (tech readiness, integration depth, channel reach, price-performance) and feeds a 2025–2034 outlook with scenario ranges and risk factors (battery, optics, sensor supply, data privacy).

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.