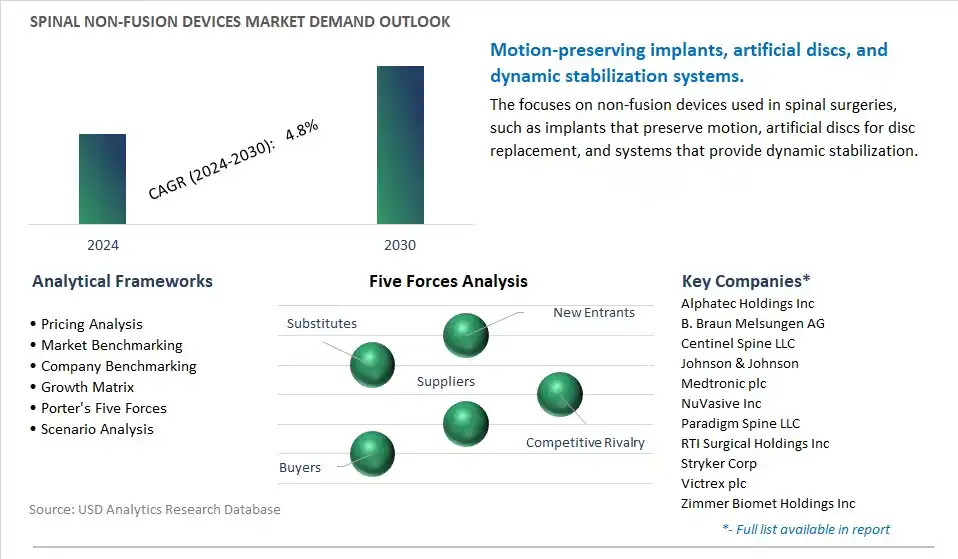

Spinal Non Fusion Devices Market is estimated to increase at a Compounded Annual Growth Rate of 4.8% CAGR over the forecast period from 2024 to 2030

The Spinal Non Fusion Devices Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Product (Artificial Discs Replacement, Dynamic Stabilization Devices, Annulus Repair Devices, Nuclear Disc Prostheses, Others), By End-User (Hospitals, Orthopedic Centers, Others).

An Introduction to Spinal Non Fusion Devices Market in 2024

In 2024, the market for spinal non-fusion devices continues to expand, offering innovative solutions for the treatment of various spinal conditions, including degenerative disc disease, spinal stenosis, and vertebral fractures. Spinal non-fusion devices aim to restore spinal stability, decompress neural structures, and preserve motion without the need for fusion surgery, thereby reducing the risk of adjacent segment degeneration and preserving spinal flexibility. These devices include artificial discs, dynamic stabilization systems, interspinous spacers, and vertebral augmentation techniques such as kyphoplasty and vertebroplasty. With advancements in biomaterials, biomechanical engineering, and surgical techniques, spinal non-fusion devices offer improved clinical outcomes, reduced postoperative morbidity, and faster recovery times compared to traditional fusion procedures. Moreover, the market is influenced by trends such as the development of patient-specific implants, the expansion of indications for non-fusion techniques, and the integration of minimally invasive approaches that minimize tissue trauma and operative time. Additionally, ongoing research focuses on optimizing device design, evaluating long-term outcomes, and identifying patient selection criteria to further enhance the effectiveness and safety of spinal non-fusion devices, reflecting the continuous innovation and evolution in spinal surgery techniques and technologies.

Market Trend: Shift Towards Minimally Invasive Procedures

A significant trend in the spinal non-fusion devices market is the shift towards minimally invasive procedures for treating spinal disorders and degenerative conditions. Minimally invasive techniques, such as percutaneous decompression, interspinous process decompression, and dynamic stabilization, are gaining popularity due to their associated benefits, including reduced tissue trauma, shorter hospital stays, faster recovery times, and lower complication rates compared to traditional open surgeries. As patients and healthcare providers seek less invasive treatment options that offer comparable outcomes to traditional fusion surgeries, there is a growing demand for spinal non-fusion devices that support minimally invasive approaches. This trend is driving innovation in device design and technology to meet the needs of surgeons and patients seeking alternatives to fusion procedures.

Market Driver: Aging Population and Rise in Degenerative Spinal Conditions

A primary driver propelling the spinal non-fusion devices market forward is the aging population and the corresponding increase in degenerative spinal conditions such as spinal stenosis, degenerative disc disease, and spondylolisthesis. As people age, they are more prone to developing spinal disorders due to factors such as wear and tear, loss of disc height, and degeneration of spinal structures. Additionally, sedentary lifestyles, obesity, and other lifestyle factors contribute to the prevalence of degenerative spinal conditions among older adults. The growing burden of degenerative spinal disorders fuels demand for non-fusion devices that offer alternatives to traditional fusion surgeries, allowing patients to preserve spinal motion and function while addressing symptoms such as pain, numbness, and weakness. As the aging population continues to grow globally, the need for effective and minimally invasive treatments for degenerative spinal conditions drives market growth and innovation in spinal non-fusion devices.

Market Opportunity: Expansion of Indications and Adoption of Motion-Preserving Technologies

An opportunity within the spinal non-fusion devices market lies in the expansion of indications and the adoption of motion-preserving technologies. While spinal fusion remains a standard treatment for certain spinal conditions, there is a growing recognition of the limitations and potential complications associated with fusion surgeries, such as adjacent segment degeneration and loss of spinal mobility. As a result, there is increasing interest in motion-preserving devices, such as artificial discs, interspinous spacers, and dynamic stabilization systems, that aim to maintain spinal motion and reduce the risk of adjacent segment degeneration. By expanding the indications for non-fusion devices and incorporating motion-preserving technologies into their product portfolios, device manufacturers can address a broader range of patient needs and clinical scenarios, attract new customer segments, and differentiate themselves in the competitive spinal implant market. Additionally, partnerships with surgeons, research institutions, and healthcare organizations can facilitate the development and adoption of innovative motion-preserving technologies, driving market expansion and improving patient outcomes.

Spinal Non-Fusion Devices Market Share Analysis: Dynamic Stabilization Devices

In the Spinal Non-Fusion Devices Market, the Dynamic Stabilization Devices segment is experiencing rapid growth. Dynamic stabilization devices are designed to preserve spinal motion while providing stability and support to the spine. These devices are utilized in the treatment of various spinal conditions, including degenerative disc disease, spinal stenosis, and spondylolisthesis. Dynamic stabilization devices offer advantages such as reduced adjacent segment degeneration, preservation of spinal mobility, and potentially quicker recovery compared to traditional fusion procedures. With an increasing emphasis on motion preservation and minimally invasive treatment options in spine surgery, dynamic stabilization devices are gaining popularity among surgeons and patients alike. Hospitals, orthopedic centers, and other healthcare facilities are the primary end-users adopting dynamic stabilization devices for spinal interventions, reflecting the widespread acceptance of these devices in clinical practice. As technological advancements improve the design and efficacy of dynamic stabilization devices and as awareness grows about the benefits of motion-preserving spinal procedures, the market for dynamic stabilization devices is expected to continue its rapid growth trajectory.

Spinal Non Fusion Devices Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossAlphatec Holdings Inc, B. Braun Melsungen AG, Centinel Spine LLC, Johnson & Johnson, Medtronic plc, NuVasive Inc, Paradigm Spine LLC, RTI Surgical Holdings Inc, Stryker Corp, Victrex plc, Zimmer Biomet Holdings Inc

Spinal Non Fusion Devices Market Segmentation

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Spinal Non Fusion Devices Market Companies

Alphatec Holdings Inc

B. Braun Melsungen AG

Centinel Spine LLC

Johnson & Johnson

Medtronic plc

NuVasive Inc

Paradigm Spine LLC

RTI Surgical Holdings Inc

Stryker Corp

Victrex plc

Zimmer Biomet Holdings Inc

Reasons to Buy the Spinal Non Fusion Devices Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Spinal Non Fusion Devices Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Spinal Non Fusion Devices Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Spinal Non Fusion Devices Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Spinal Non Fusion Devices Market Size Outlook, $ Million, 2021 to 2030

3.2 Spinal Non Fusion Devices Market Outlook by Type, $ Million, 2021 to 2030

3.3 Spinal Non Fusion Devices Market Outlook by Product, $ Million, 2021 to 2030

3.4 Spinal Non Fusion Devices Market Outlook by Application, $ Million, 2021 to 2030

3.5 Spinal Non Fusion Devices Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Spinal Non Fusion Devices Industry

4.2 Key Market Trends in Spinal Non Fusion Devices Industry

4.3 Potential Opportunities in Spinal Non Fusion Devices Industry

4.4 Key Challenges in Spinal Non Fusion Devices Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Spinal Non Fusion Devices Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Spinal Non Fusion Devices Market Outlook by Segments

7.1 Spinal Non Fusion Devices Market Outlook by Segments, $ Million, 2021- 2030

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

8 North America Spinal Non Fusion Devices Market Analysis and Outlook To 2030

8.1 Introduction to North America Spinal Non Fusion Devices Markets in 2024

8.2 North America Spinal Non Fusion Devices Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Spinal Non Fusion Devices Market size Outlook by Segments, 2021-2030

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

9 Europe Spinal Non Fusion Devices Market Analysis and Outlook To 2030

9.1 Introduction to Europe Spinal Non Fusion Devices Markets in 2024

9.2 Europe Spinal Non Fusion Devices Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Spinal Non Fusion Devices Market Size Outlook by Segments, 2021-2030

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

10 Asia Pacific Spinal Non Fusion Devices Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Spinal Non Fusion Devices Markets in 2024

10.2 Asia Pacific Spinal Non Fusion Devices Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Spinal Non Fusion Devices Market size Outlook by Segments, 2021-2030

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

11 South America Spinal Non Fusion Devices Market Analysis and Outlook To 2030

11.1 Introduction to South America Spinal Non Fusion Devices Markets in 2024

11.2 South America Spinal Non Fusion Devices Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Spinal Non Fusion Devices Market size Outlook by Segments, 2021-2030

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

12 Middle East and Africa Spinal Non Fusion Devices Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Spinal Non Fusion Devices Markets in 2024

12.2 Middle East and Africa Spinal Non Fusion Devices Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Spinal Non Fusion Devices Market size Outlook by Segments, 2021-2030

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Alphatec Holdings Inc

B. Braun Melsungen AG

Centinel Spine LLC

Johnson & Johnson

Medtronic plc

NuVasive Inc

Paradigm Spine LLC

RTI Surgical Holdings Inc

Stryker Corp

Victrex plc

Zimmer Biomet Holdings Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Artificial Discs Replacement

Dynamic Stabilization Devices

Annulus Repair Devices

Nuclear Disc Prostheses

Others

By End-User

Hospitals

Orthopedic Centers

Others

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)