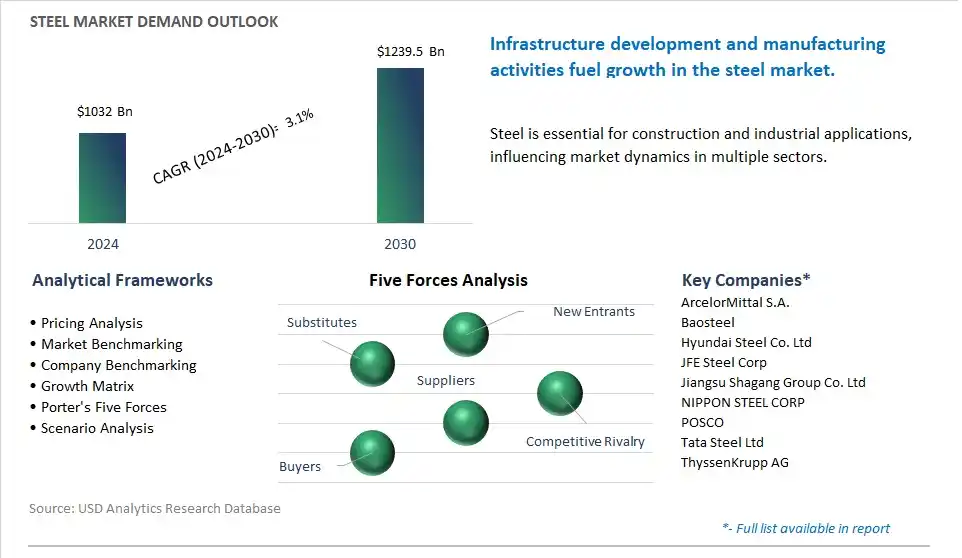

The global Steel Market is poised to register a 3.1% CAGR from $1032 Billion in 2024 to $1239.5 Billion in 2030.

The global Steel Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Hot Rolled Steel, Cold Rolled Steel, Direct Rolled Steel, Tubes, Others), By End-User (Pre-Engineered Metal Buildings, Bridges, Industrial Structures).

An Introduction to Global Steel Market in 2024

The steel market is undergoing transformation driven by evolving market dynamics, technological innovations, and sustainability initiatives. Key trends shaping the future of the industry include advancements in steelmaking processes, such as electric arc furnaces (EAFs), direct reduced iron (DRI), and hydrogen-based steel production, to reduce carbon emissions, energy consumption, and environmental footprint. Innovations in steel alloy compositions, microstructure control, and heat treatment techniques enable the development of high-strength, lightweight, and corrosion-resistant steels for automotive, aerospace, and construction applications. Moreover, digitalization and automation technologies such as artificial intelligence, robotics, and IoT are revolutionizing steel manufacturing processes, supply chain management, and product quality control, driving operational efficiency and competitiveness. Additionally, the transition towards circular economy principles and sustainable steel production practices, including scrap recycling, waste valorization, and carbon capture utilization and storage (CCUS), is reshaping the industry's approach to resource management and environmental stewardship. As stakeholders collaborate to address challenges related to decarbonization, resource efficiency, and supply chain resilience, the steel market is poised for continued growth and innovation as a foundational material for global infrastructure development, manufacturing, and economic prosperity.

Steel Market Competitive Landscape

The market report analyses the leading companies in the industry including ArcelorMittal S.A., Baosteel, Hyundai Steel Co. Ltd, JFE Steel Corp, Jiangsu Shagang Group Co. Ltd, NIPPON STEEL CORP, POSCO, Tata Steel Ltd, ThyssenKrupp AG.

Steel Market Dynamics

Steel Market Trend: Sustainable Steel Production Practices

A prominent trend in the steel market is the adoption of sustainable steel production practices. With increasing awareness of environmental concerns and regulatory pressure to reduce carbon emissions, steel manufacturers are focusing on implementing sustainable practices throughout the production process. This includes investing in energy-efficient technologies, recycling scrap steel, and reducing greenhouse gas emissions. Sustainable steel production not only helps to minimize the environmental impact of the steel industry but also meets the growing demand from consumers and businesses for environmentally friendly products. This trend reflects a broader shift towards sustainability in manufacturing industries and drives innovation in steel production methods and materials.

Steel Market Driver: Infrastructure Development and Urbanization

A key driver for the steel market is infrastructure development and urbanization. As economies grow and populations increase, there is a rising demand for steel in the construction of infrastructure projects such as roads, bridges, buildings, and utilities. Rapid urbanization, particularly in emerging markets, drives the need for steel in residential and commercial construction, transportation networks, and utilities infrastructure. Additionally, government initiatives aimed at revitalizing infrastructure and promoting economic growth further stimulate the demand for steel. The ongoing expansion of infrastructure and urbanization projects worldwide drives the consumption of steel as a fundamental material for building modern societies and supporting economic development.

Steel Market Opportunity: Innovation in High-Performance Steel Alloys and Applications

An opportunity within the steel market lies in innovation in high-performance steel alloys and applications. While steel is already widely used in various industries, there is potential for further innovation in alloy development to enhance properties such as strength, corrosion resistance, and lightweight characteristics. Manufacturers can invest in research and development to create new grades of steel tailored for specific applications or environments, such as automotive, aerospace, renewable energy, and construction. Advanced high-strength steel alloys can offer weight-saving solutions for automotive and aerospace industries, while corrosion-resistant stainless steels can address the needs of marine and chemical processing applications. By continuously innovating and expanding the range of steel alloys and applications, manufacturers can capitalize on new market opportunities and meet the evolving needs of customers across diverse industries.

Steel Market Share Analysis: Hot Rolled Steel segment generated the highest revenue in the industry

The hot rolled steel segment is the largest segment in the Steel Market due to its extensive use across various industries and applications. Hot rolled steel is produced through a rolling process at high temperatures, resulting in a rough surface finish and dimensional accuracy. This segment encompasses a wide range of steel products, including sheets, plates, coils, and structural sections, which find widespread applications in construction, automotive, manufacturing, infrastructure, and machinery industries. Hot rolled steel offers diverse advantages, including high strength, formability, weldability, and cost-effectiveness, making it suitable for a diverse range of structural and non-structural applications. Additionally, hot rolled steel products are utilized in the fabrication of beams, columns, channels, angles, pipes, and tubing for building construction, bridges, machinery, and transportation equipment. In addition, hot rolled steel is preferred for its versatility in manufacturing processes, including machining, welding, and forming, allowing for the production of complex shapes and components. Further, the availability of a wide range of grades, thicknesses, and sizes of hot rolled steel products meets the diverse needs of end-users in various industries. As industries continue to demand high-quality steel products for their projects and applications, the hot rolled steel segment maintains its dominance in the Steel Market.

Steel Market Share Analysis: Pre-Engineered Metal Buildings Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The pre-engineered metal buildings segment is the fastest-growing segment in the Steel Market due to increasing demand for cost-effective, sustainable, and rapidly deployable construction solutions across various end-user industries. Pre-engineered metal buildings (PEMBs) are custom-designed steel structures manufactured off-site and assembled on-site, offering advantages such as quick construction timelines, design flexibility, and cost efficiency. These buildings find applications in sectors such as commercial, industrial, agricultural, institutional, and recreational facilities, where they serve as warehouses, factories, distribution centers, offices, retail spaces, and community centers. The growth of the pre-engineered metal buildings segment is driven by factors such as urbanization, population growth, infrastructure development, and the need for scalable and adaptable building solutions. Additionally, advancements in design software, manufacturing processes, and construction techniques enable the production and erection of high-quality PEMBs with reduced material waste, energy consumption, and construction time. In addition, the inherent strength, durability, and recyclability of steel make it an ideal material for pre-engineered metal buildings, meeting stringent performance, safety, and environmental standards. Further, the flexibility of PEMBs allows for future expansion, modifications, and customization to accommodate changing business needs and industry requirements. As industries seek efficient and sustainable building solutions to meet their evolving needs, the demand for pre-engineered metal buildings is expected to experience rapid growth, positioning it as the fastest-growing segment in the Steel Market.

Steel Market Report Segmentation

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Steel Companies Profiled in the Market Study

ArcelorMittal S.A.

Baosteel

Hyundai Steel Co. Ltd

JFE Steel Corp

Jiangsu Shagang Group Co. Ltd

NIPPON STEEL CORP

POSCO

Tata Steel Ltd

ThyssenKrupp AG

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Steel Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Steel Market Size Outlook, $ Million, 2021 to 2030

3.2 Steel Market Outlook by Type, $ Million, 2021 to 2030

3.3 Steel Market Outlook by Product, $ Million, 2021 to 2030

3.4 Steel Market Outlook by Application, $ Million, 2021 to 2030

3.5 Steel Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Steel Industry

4.2 Key Market Trends in Steel Industry

4.3 Potential Opportunities in Steel Industry

4.4 Key Challenges in Steel Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Steel Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Steel Market Outlook by Segments

7.1 Steel Market Outlook by Segments, $ Million, 2021- 2030

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

8 North America Steel Market Analysis and Outlook To 2030

8.1 Introduction to North America Steel Markets in 2024

8.2 North America Steel Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Steel Market size Outlook by Segments, 2021-2030

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

9 Europe Steel Market Analysis and Outlook To 2030

9.1 Introduction to Europe Steel Markets in 2024

9.2 Europe Steel Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Steel Market Size Outlook by Segments, 2021-2030

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

10 Asia Pacific Steel Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Steel Markets in 2024

10.2 Asia Pacific Steel Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Steel Market size Outlook by Segments, 2021-2030

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

11 South America Steel Market Analysis and Outlook To 2030

11.1 Introduction to South America Steel Markets in 2024

11.2 South America Steel Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Steel Market size Outlook by Segments, 2021-2030

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

12 Middle East and Africa Steel Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Steel Markets in 2024

12.2 Middle East and Africa Steel Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Steel Market size Outlook by Segments, 2021-2030

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ArcelorMittal S.A.

Baosteel

Hyundai Steel Co. Ltd

JFE Steel Corp

Jiangsu Shagang Group Co. Ltd

NIPPON STEEL CORP

POSCO

Tata Steel Ltd

ThyssenKrupp AG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Hot Rolled Steel

Cold Rolled Steel

Direct Rolled Steel

Tubes

Others

By End-User

Pre-Engineered Metal Buildings

-Primary Members

-Secondary Members

-Roofs & Walls

-Panels

Bridges

Industrial Structures

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)