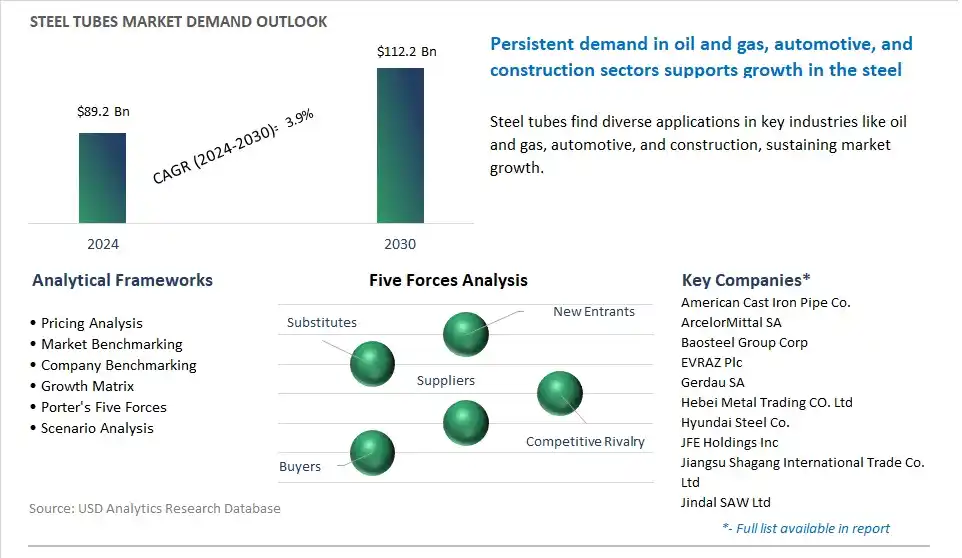

The global Steel Tubes Market is poised to register a 3.9% CAGR from $89.2 Billion in 2024 to $112.2 Billion in 2030.

The global Steel Tubes Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Seamless, Welded), By Material (Carbon Steel, Stainless Steel, Alloy Steel, Others), By End-User (Oil and Gas, Water and Sewage, Infrastructure and Construction, Automotive).

An Introduction to Global Steel Tubes Market in 2024

The steel tubes market is experiencing robust growth driven by increasing demand in construction, automotive, oil and gas, and industrial sectors for pipes, tubes, and hollow sections for structural, mechanical, and fluid transport applications. Key trends shaping the future of the industry include the rising adoption of seamless steel tubes, welded pipes, and specialty tubing products in critical infrastructure projects, energy exploration, and manufacturing processes. Moreover, there's a growing emphasis on product quality, reliability, and performance, driving investments in advanced steelmaking, tube manufacturing, and testing technologies to meet stringent specifications and industry standards. Additionally, advancements in tube design, alloy compositions, and surface coatings are driving innovation and customization, enabling manufacturers to offer specialized solutions for demanding applications and market segments, thereby fueling market growth and competitiveness in the global steel tubes market.

Steel Tubes Market Competitive Landscape

The market report analyses the leading companies in the industry including American Cast Iron Pipe Co., ArcelorMittal SA, Baosteel Group Corp, EVRAZ Plc, Gerdau SA, Hebei Metal Trading CO. Ltd, Hyundai Steel Co., JFE Holdings Inc, Jiangsu Shagang International Trade Co. Ltd, Jindal SAW Ltd, Nippon Steel Corp, Nucor Corp, PAO TMK, POSCO holdings Inc, Rama Steel Tubes Ltd, Steel Authority of India Ltd, Tata Steel Ltd, thyssenkrupp AG, US Steel Tubular Products Inc.

Steel Tubes Market Dynamics

Steel Tubes Market Trend: Increasing Adoption of Seamless Steel Tubes

The most prominent market trend for steel tubes is the increasing adoption of seamless steel tubes across various industries. Seamless steel tubes offer superior strength, durability, and corrosion resistance compared to welded tubes, making them ideal for critical applications such as oil and gas exploration, automotive manufacturing, aerospace, and power generation. This trend is driven by the need for high-performance tubing solutions that can withstand extreme operating conditions, provide reliable performance, and ensure safety and integrity in demanding environments. As industries strive for efficiency, reliability, and cost-effectiveness, the demand for seamless steel tubes continues to rise, leading to technological advancements and innovation in seamless tube manufacturing processes.

Steel Tubes Market Driver: Growth in Energy and Infrastructure Projects

A key market driver for steel tubes is the growth in energy and infrastructure projects worldwide. As countries invest in expanding energy infrastructure, upgrading utilities, and building transportation networks, there's a significant demand for steel tubes for applications such as oil and gas pipelines, power plant boilers, heat exchangers, and structural supports. Steel tubes play a crucial role in conveying fluids, gases, and steam, as well as providing structural support in construction projects such as bridges, buildings, and industrial facilities. The demand for steel tubes is particularly significant in emerging markets and developing regions, where rapid urbanization, population growth, and industrialization drive the need for new infrastructure investments and energy resources.

Steel Tubes Market Opportunity: Diversification into Specialized Tubing Solutions

An exciting opportunity in the steel tubes market lies in diversification into specialized tubing solutions tailored to specific industry requirements and niche applications. While steel tubes find widespread use in conventional applications such as construction, transportation, and energy sectors, there's a growing demand for specialized tubing products with unique properties and functionalities. For example, industries such as automotive, aerospace, medical devices, and electronics require precision-engineered tubing solutions with tight tolerances, smooth surfaces, and custom shapes for applications such as hydraulic systems, fuel lines, heat exchangers, and instrumentation. By investing in advanced manufacturing technologies, material science, and product development capabilities, steel tube manufacturers can capitalize on this opportunity to expand their product portfolios, cater to high-value market segments, and differentiate themselves from competitors. Developing innovative specialized tubing solutions allows steel tube manufacturers to address the evolving needs of end-users in various industries, driving growth and profitability in the marketplace.

Steel Tubes Market Share Analysis: The Welded segment generated the highest revenue in 2024

The largest segment in the Steel Tubes Market is the Welded category. welded steel tubes are commonly used in various industries and applications due to their versatility, availability, and cost-effectiveness. Welded tubes are manufactured by welding flat steel sheets or strips into cylindrical shapes, allowing for the production of tubes with a wide range of diameters, thicknesses, and lengths to suit different requirements. Additionally, welded tubes can be produced in large quantities using automated processes, leading to economies of scale and cost savings in manufacturing. Further, welded tubes are suitable for both structural and non-structural applications, including construction, infrastructure, automotive, machinery, furniture, and appliances, among others. Furthermore, welded tubes offer consistent quality, dimensional accuracy, and structural integrity, meeting industry standards and specifications for various applications. Accordingly, the Welded segment maintains its position as the largest segment in the Steel Tubes Market, with continued growth anticipated due to the consistent demand for these versatile and cost-effective tubular products.

Steel Tubes Market Share Analysis: The Welded segment generated the highest revenue in 2024

The largest segment in the Steel Tubes Market is the Welded category. Welded steel tubes hold a significant share in the market. welded tubes are widely used across various industries and applications due to their versatility and cost-effectiveness. They are commonly utilized in construction, infrastructure, automotive, machinery, furniture, and appliances, among other sectors. Welded tubes are manufactured by welding steel strips or sheets together to form cylindrical shapes, allowing for the production of tubes with different diameters, thicknesses, and lengths to suit specific requirements. Additionally, welded tubes can be produced in large quantities using automated processes, leading to cost efficiencies in manufacturing. Further, welded tubes offer structural integrity, dimensional accuracy, and consistent quality, meeting industry standards and specifications for various applications. Furthermore, advancements in welding technology have improved the quality and performance of welded tubes, further driving their widespread adoption. Accordingly, the Welded segment maintains its position as the largest segment in the Steel Tubes Market, with continued growth expected due to the ongoing demand for these versatile and cost-effective tubular products.

Steel Tubes Market Share Analysis: The Stainless Steel segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest growing segment in the Steel Tubes Market is the Stainless Steel category. stainless steel tubes offer superior corrosion resistance, durability, and aesthetic appeal compared to other materials like carbon steel and alloy steel. This makes them suitable for a wide range of applications in industries such as construction, automotive, aerospace, food and beverage, and oil and gas, among others. Additionally, the increasing demand for stainless steel tubes is driven by various factors such as urbanization, infrastructure development, industrialization, and stringent regulations regarding corrosion resistance and hygiene standards. Further, advancements in stainless steel manufacturing processes, including improvements in metallurgy, tube forming technologies, and surface finishing techniques, have enhanced the quality and performance of stainless steel tubes, further driving their adoption. Furthermore, the growing preference for sustainable and environmentally friendly materials in construction and manufacturing industries favors the use of stainless steel tubes, which are recyclable and contribute to reducing the environmental footprint. Accordingly, the Stainless Steel segment is witnessing rapid growth in the Steel Tubes Market, with continued expansion expected as industries increasingly prioritize the use of high-quality and corrosion-resistant materials in their applications.

Steel Tubes Market Share Analysis: The Infrastructure and Construction segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest growing segment in the Steel Tubes Market is the Infrastructure and Construction sector. infrastructure development projects such as roads, bridges, airports, railways, and utilities are on the rise globally due to population growth, urbanization, and the need for sustainable infrastructure solutions. As governments and private entities invest in infrastructure upgrades and expansions, there is a growing demand for steel tubes for various applications such as structural supports, piling, drainage systems, and transportation networks. Additionally, the construction industry is experiencing technological advancements and innovations that drive the demand for steel tubes with specific properties such as strength, durability, and corrosion resistance. Further, urbanization trends and the increasing demand for affordable housing and commercial spaces further stimulate construction activities, boosting the demand for steel tubes. Furthermore, government stimulus packages, infrastructure development initiatives, and public-private partnerships aimed at promoting economic growth and improving living standards drive investments in infrastructure projects, fueling the growth of the Infrastructure and Construction segment in the Steel Tubes Market.

Steel Tubes Market Report Segmentation

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Steel Tubes Companies Profiled in the Market Study

American Cast Iron Pipe Co.

ArcelorMittal SA

Baosteel Group Corp

EVRAZ Plc

Gerdau SA

Hebei Metal Trading CO. Ltd

Hyundai Steel Co.

JFE Holdings Inc

Jiangsu Shagang International Trade Co. Ltd

Jindal SAW Ltd

Nippon Steel Corp

Nucor Corp

PAO TMK

POSCO holdings Inc

Rama Steel Tubes Ltd

Steel Authority of India Ltd

Tata Steel Ltd

thyssenkrupp AG

US Steel Tubular Products Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Steel Tubes Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Steel Tubes Market Size Outlook, $ Million, 2021 to 2030

3.2 Steel Tubes Market Outlook by Type, $ Million, 2021 to 2030

3.3 Steel Tubes Market Outlook by Product, $ Million, 2021 to 2030

3.4 Steel Tubes Market Outlook by Application, $ Million, 2021 to 2030

3.5 Steel Tubes Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Steel Tubes Industry

4.2 Key Market Trends in Steel Tubes Industry

4.3 Potential Opportunities in Steel Tubes Industry

4.4 Key Challenges in Steel Tubes Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Steel Tubes Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Steel Tubes Market Outlook by Segments

7.1 Steel Tubes Market Outlook by Segments, $ Million, 2021- 2030

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

8 North America Steel Tubes Market Analysis and Outlook To 2030

8.1 Introduction to North America Steel Tubes Markets in 2024

8.2 North America Steel Tubes Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Steel Tubes Market size Outlook by Segments, 2021-2030

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

9 Europe Steel Tubes Market Analysis and Outlook To 2030

9.1 Introduction to Europe Steel Tubes Markets in 2024

9.2 Europe Steel Tubes Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Steel Tubes Market Size Outlook by Segments, 2021-2030

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

10 Asia Pacific Steel Tubes Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Steel Tubes Markets in 2024

10.2 Asia Pacific Steel Tubes Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Steel Tubes Market size Outlook by Segments, 2021-2030

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

11 South America Steel Tubes Market Analysis and Outlook To 2030

11.1 Introduction to South America Steel Tubes Markets in 2024

11.2 South America Steel Tubes Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Steel Tubes Market size Outlook by Segments, 2021-2030

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

12 Middle East and Africa Steel Tubes Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Steel Tubes Markets in 2024

12.2 Middle East and Africa Steel Tubes Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Steel Tubes Market size Outlook by Segments, 2021-2030

By Product

Seamless

Welded

By Material

Carbon Steel

Stainless Steel

Alloy Steel

Others

By End-User

Oil and Gas

Water and Sewage

Infrastructure and Construction

Automotive

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

American Cast Iron Pipe Co.

ArcelorMittal SA

Baosteel Group Corp

EVRAZ Plc

Gerdau SA

Hebei Metal Trading CO. Ltd

Hyundai Steel Co.

JFE Holdings Inc

Jiangsu Shagang International Trade Co. Ltd

Jindal SAW Ltd

Nippon Steel Corp

Nucor Corp

PAO TMK

POSCO holdings Inc

Rama Steel Tubes Ltd

Steel Authority of India Ltd

Tata Steel Ltd

thyssenkrupp AG

US Steel Tubular Products Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise