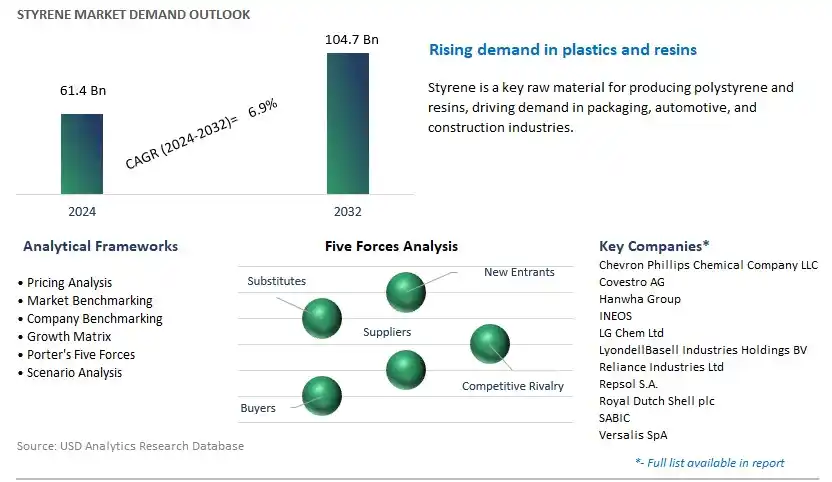

Global Styrene Market Size is valued at $61.4 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.9% to reach $104.7 Billion by 2032.

The global Styrene Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Polystyrene, Acrylonitrile Butadiene Styrene, Styrene Butadiene Rubber, Others), By End-User (Packaging, Construction, Consumer Goods, Automotive and Transportation, Electrical and Electronics, Others).

An Introduction to Styrene Market in 2024

Styrene is a versatile organic compound used primarily in the production of polystyrene, a widely used thermoplastic polymer known for its versatility, strength, and insulation properties. In 2024, the market for styrene remains significant, driven by its extensive applications in packaging, construction, automotive, electronics, and consumer goods. Polystyrene, derived from styrene monomer through polymerization, is used in various forms such as solid, foam, and expanded polystyrene (EPS), serving as packaging materials, insulation panels, disposable containers, and consumer products. Additionally, styrene is utilized in the production of styrene-butadiene rubber (SBR) for tire manufacturing, acrylonitrile-butadiene-styrene (ABS) resins for durable plastics, and styrene-based copolymers for coatings, adhesives, and synthetic rubbers. With a focus on sustainability and regulatory compliance, manufacturers are exploring bio-based sources of styrene and developing eco-friendly production processes to reduce environmental impact and carbon footprint. Further, the transition towards circular economy principles is driving initiatives for styrene recycling and waste reduction, promoting closed-loop systems and resource efficiency in styrene-based product manufacturing. As industries to innovate and address sustainability challenges, the market for styrene and its derivatives is poised for d evolution and growth, offering essential materials for a wide range of industrial and consumer applications worldwide.

Styrene Market Competitive Landscape

The market report analyses the leading companies in the industry including Chevron Phillips Chemical Company LLC, Covestro AG, Hanwha Group, INEOS, LG Chem Ltd, LyondellBasell Industries Holdings BV, Reliance Industries Ltd, Repsol S.A., Royal Dutch Shell plc, SABIC, Versalis SpA, and others.

Styrene Market Dynamics

Market Trend: Increasing Demand for Polystyrene and Expanded Polystyrene Products

A significant trend in the styrene market is the increasing demand for polystyrene (PS) and expanded polystyrene (EPS) products across various industries. Styrene is a key raw material used in the production of PS and EPS, which find applications in packaging, construction, automotive, electronics, and consumer goods sectors. With the rise in e-commerce, urbanization, and infrastructure development, there is a growing need for lightweight, durable, and cost-effective packaging solutions, driving the demand for PS and EPS products. Additionally, the versatility of PS and EPS materials, coupled with their excellent insulating properties, makes them ideal choices for construction insulation, disposable food packaging, automotive components, and consumer electronics packaging. This trend is expected to continue as industries seek sustainable and innovative solutions to meet evolving consumer preferences and regulatory requirements, fueling the growth of the styrene market.

Market Driver: Growth in End-use Industries and Manufacturing Activities

The primary driver behind the growth of the styrene market is the expansion of end-use industries and manufacturing activities worldwide. Styrene is a fundamental building block for a wide range of downstream products, including plastics, resins, synthetic rubber, and coatings, which are extensively used in manufacturing processes across various industries. With economic growth, urbanization, and industrialization driving demand for consumer goods, automobiles, electronics, appliances, and construction materials, there is a steady increase in the consumption of styrene-based products. Moreover, the recovery of global manufacturing activities following the COVID-19 pandemic and investments in infrastructure development projects further support the demand for styrene-derived materials. As industries continue to expand and innovate, the demand for styrene as a raw material is expected to grow, providing opportunities for styrene producers and suppliers to meet the evolving needs of downstream industries and capture market share.

Market Opportunity: Development of Bio-based Styrene and Sustainable Solutions

An opportunity for the styrene market lies in the development of bio-based styrene and sustainable solutions. With growing concerns about environmental sustainability, carbon emissions, and plastic waste management, there is increasing interest in bio-based alternatives to conventional styrene derived from fossil fuels. Manufacturers are exploring renewable feedstocks and innovative production processes to produce bio-based styrene, which offers potential benefits such as reduced carbon footprint, lower environmental impact, and enhanced sustainability credentials. Additionally, there is an opportunity to develop sustainable solutions for recycling and repurposing styrene-based products, such as PS and EPS packaging materials, to promote a circular economy and reduce plastic pollution. By investing in research and development initiatives focused on bio-based styrene production, recycling technologies, and eco-friendly applications, stakeholders in the styrene market can contribute to environmental stewardship, meet regulatory requirements, and capture opportunities in the growing market for sustainable materials and solutions. Expanding into bio-based styrene and sustainable solutions presents an opportunity for the styrene market to address environmental challenges, differentiate product offerings, and drive growth in the global chemicals industry.

Styrene Market Share Analysis: Polystyrene segment generated the highest revenue in 2024

Within the styrene market, the Polystyrene segment is the largest. Polystyrene is a versatile thermoplastic polymer derived from styrene monomer and is widely used in various applications across industries such as packaging, construction, electronics, automotive, and consumer goods. Its lightweight, durable, and cost-effective properties make it a preferred choice for packaging materials, including food packaging, disposable cups, containers, and protective packaging. Additionally, polystyrene's excellent insulating properties make it suitable for use in thermal insulation applications, such as in the construction of buildings and refrigeration equipment. Moreover, the ease of processing and molding characteristics of polystyrene enable manufacturers to produce a wide range of shapes and sizes, contributing to its versatility and applicability in diverse end-use sectors. Furthermore, ongoing advancements in polymer technology have led to the development of high-impact polystyrene (HIPS) and expanded polystyrene (EPS), which further expand the market potential of polystyrene-based products. As a result of these factors, the Polystyrene segment maintains its position as the largest within the styrene market, supported by its widespread use, versatility, and cost-effectiveness across various industries and applications.

Styrene Market Share Analysis: Packaging is poised to register the fastest CAGR over the forecast period

Within the styrene market, the Packaging segment is the fastest-growing. Packaging is a critical application for styrene-based products due to their lightweight, versatile, and cost-effective properties, making them ideal materials for various packaging solutions across industries such as food and beverage, healthcare, cosmetics, and e-commerce. Styrene-based polymers, including polystyrene, acrylonitrile butadiene styrene (ABS), and styrene-butadiene rubber (SBR), are widely used in the production of packaging materials such as trays, containers, cups, bottles, and films. Additionally, the increasing demand for convenience packaging, on-the-go meals, and single-serve portions drives the adoption of styrene-based packaging solutions that offer durability, insulation, and barrier properties to protect and preserve the contents. Moreover, the growing e-commerce sector and the shift towards online shopping have led to increased demand for protective packaging materials, including styrene-based foam packaging and cushioning materials, to ensure safe transit and delivery of goods. Furthermore, regulatory initiatives promoting sustainability and recyclability in packaging drive the development of innovative styrene-based packaging solutions with reduced environmental impact, such as bio-based and recyclable materials. As a result of these factors, the Packaging segment experiences rapid growth within the styrene market, propelled by the increasing demand for versatile, cost-effective, and sustainable packaging solutions across various end-user industries.

Styrene Market

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Styrene Companies Profiled in the Study

Chevron Phillips Chemical Company LLC

Covestro AG

Hanwha Group

INEOS

LG Chem Ltd

LyondellBasell Industries Holdings BV

Reliance Industries Ltd

Repsol S.A.

Royal Dutch Shell plc

SABIC

Versalis SpA

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Styrene Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Styrene Market Size Outlook, $ Million, 2021 to 2032

3.2 Styrene Market Outlook by Type, $ Million, 2021 to 2032

3.3 Styrene Market Outlook by Product, $ Million, 2021 to 2032

3.4 Styrene Market Outlook by Application, $ Million, 2021 to 2032

3.5 Styrene Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Styrene Industry

4.2 Key Market Trends in Styrene Industry

4.3 Potential Opportunities in Styrene Industry

4.4 Key Challenges in Styrene Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Styrene Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Styrene Market Outlook by Segments

7.1 Styrene Market Outlook by Segments, $ Million, 2021- 2032

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

8 North America Styrene Market Analysis and Outlook To 2032

8.1 Introduction to North America Styrene Markets in 2024

8.2 North America Styrene Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Styrene Market size Outlook by Segments, 2021-2032

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

9 Europe Styrene Market Analysis and Outlook To 2032

9.1 Introduction to Europe Styrene Markets in 2024

9.2 Europe Styrene Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Styrene Market Size Outlook by Segments, 2021-2032

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

10 Asia Pacific Styrene Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Styrene Markets in 2024

10.2 Asia Pacific Styrene Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Styrene Market size Outlook by Segments, 2021-2032

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

11 South America Styrene Market Analysis and Outlook To 2032

11.1 Introduction to South America Styrene Markets in 2024

11.2 South America Styrene Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Styrene Market size Outlook by Segments, 2021-2032

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

12 Middle East and Africa Styrene Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Styrene Markets in 2024

12.2 Middle East and Africa Styrene Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Styrene Market size Outlook by Segments, 2021-2032

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Chevron Phillips Chemical Company LLC

Covestro AG

Hanwha Group

INEOS

LG Chem Ltd

LyondellBasell Industries Holdings BV

Reliance Industries Ltd

Repsol S.A.

Royal Dutch Shell plc

SABIC

Versalis SpA

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Polystyrene

Acrylonitrile Butadiene Styrene

Styrene Butadiene Rubber

Others

By End-User

Packaging

Construction

Consumer Goods

Automotive and Transportation

Electrical and Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)