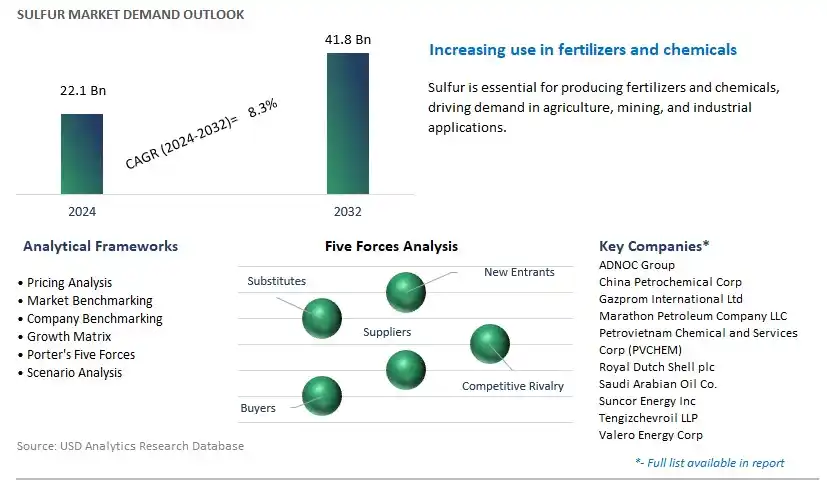

Global Sulfur Market Size is valued at $22.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 8.3% to reach $41.8 Billion by 2032.

The global Sulfur Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Form (Solid, Liquid), By Technology (Granules, Pastilles, Prilling), By End-User (Fertilizer, Chemical Processing, Metal Manufacturing, Rubber Processing, Others).

An Introduction to Sulfur Market in 2024

Sulfur is an essential element with diverse industrial applications in agriculture, chemicals, pharmaceuticals, petroleum refining, and manufacturing. In 2024, the market for sulfur remains significant, driven by its roles as a raw material, intermediate, and catalyst in various industrial processes. Sulfur is primarily used in the production of sulfuric acid, a key ingredient in fertilizer manufacturing, metal processing, and chemical synthesis. Additionally, sulfur finds applications in the vulcanization of rubber, preservation of food products, production of pharmaceuticals and cosmetics, and extraction of metals from ores in mining operations. With advancements in sulfur recovery technologies, environmental regulations, and sustainability initiatives, industries are adopting processes such as Claus sulfur recovery units (SRUs) and tail gas treatment units (TGTUs) to minimize sulfur emissions, reduce environmental impact, and maximize resource utilization. Further, the development of novel sulfur-based materials and chemical derivatives such as elemental sulfur nanoparticles, sulfur polymers, and sulfur-containing drugs is opening new opportunities for innovation and value creation in various sectors. As industries to innovate and adapt to changing market dynamics, the market for sulfur is poised for d evolution and growth, offering essential materials and solutions for diverse industrial applications and economic sectors worldwide.

Sulfur Market Competitive Landscape

The market report analyses the leading companies in the industry including ADNOC Group, China Petrochemical Corp, Gazprom International Ltd, Marathon Petroleum Company LLC, Petrovietnam Chemical and Services Corp (PVCHEM), Royal Dutch Shell plc, Saudi Arabian Oil Co., Suncor Energy Inc, Tengizchevroil LLP, Valero Energy Corp, and others.

Sulfur Market Dynamics

Market Trend: Increasing Demand for Sulfur in Agricultural Applications

A significant trend in the sulfur market is the increasing demand for sulfur in agricultural applications. Sulfur is an essential nutrient for plant growth and development, playing a crucial role in the synthesis of proteins, enzymes, and vitamins in plants. With the growing global population and the need to enhance agricultural productivity and food security, there is a rising demand for sulfur-based fertilizers and soil amendments to improve soil fertility, increase crop yields, and optimize nutrient uptake by plants. Additionally, sulfur is utilized in the production of pesticides, fungicides, and herbicides for pest and disease management in agriculture. The trend towards sustainable farming practices, organic agriculture, and environmentally friendly crop protection solutions further drives the adoption of sulfur-based products in the agricultural sector, stimulating market growth and innovation in sulfur applications for agriculture.

Market Driver: Expansion of Industrial Activities and Chemical Manufacturing

The primary driver behind the growth of the sulfur market is the expansion of industrial activities and chemical manufacturing worldwide. Sulfur is a key raw material used in various industrial processes, including petroleum refining, chemical synthesis, mining, metallurgy, and pharmaceutical manufacturing. With industrialization, urbanization, and economic development driving demand for energy, transportation fuels, consumer goods, and industrial products, there is a steady increase in the consumption of sulfur as a feedstock, catalyst, and additive in industrial processes. Moreover, sulfur is essential for the production of sulfuric acid, one of the most widely used industrial chemicals with applications in battery manufacturing, metal processing, fertilizer production, and wastewater treatment. As industries continue to grow and diversify, the demand for sulfur as a fundamental component in industrial activities is expected to rise, providing opportunities for sulfur producers and suppliers to meet the needs of various industrial sectors.

Market Opportunity: Development of Innovative Sulfur-based Products and Technologies

An opportunity for the sulfur market lies in the development of innovative sulfur-based products and technologies to address emerging market needs and applications. With advancements in chemical engineering, materials science, and biotechnology, there is potential to create value-added sulfur products with enhanced properties, functionality, and performance characteristics. For example, sulfur nanoparticles are being explored for applications in energy storage, catalysis, and environmental remediation due to their unique properties such as high surface area, reactivity, and stability. Additionally, there is an opportunity to develop sulfur-based materials for advanced applications in electronics, healthcare, construction, and renewable energy sectors. By investing in research and development initiatives focused on sulfur chemistry, process optimization, and product innovation, sulfur producers can expand their product portfolios, enter new markets, and capture opportunities in high-value applications. Expanding into innovative sulfur-based products and technologies presents an opportunity for the market to drive innovation, create value, and sustain growth in the sulfur industry while addressing evolving customer needs and market dynamics.

Sulfur Market Share Analysis: Solid segment generated the highest revenue in 2024

In the sulfur market, the Solid segment is the largest, primarily due to its widespread applications and favorable properties that make it the preferred form for various industries. Solid sulfur is commonly found in the form of sulfur pellets, granules, or flakes, and it is used in numerous industrial processes across sectors such as agriculture, chemicals, pharmaceuticals, and rubber manufacturing. One of the primary applications of solid sulfur is in agriculture, where it is used as a soil amendment or fertilizer to improve soil fertility and crop yields. Solid sulfur is also used in the production of sulfuric acid, which is a key raw material in the manufacturing of fertilizers, batteries, and industrial chemicals. Additionally, solid sulfur finds applications in the production of sulfur-based chemicals, such as sulfur dioxide and sulfuric acid, which are utilized in various industrial processes including petroleum refining, metal extraction, and wastewater treatment. Moreover, solid sulfur is preferred for transportation and storage purposes due to its stability and ease of handling compared to liquid sulfur, which requires specialized handling equipment and storage facilities. As a result of these factors, the Solid segment maintains its position as the largest within the sulfur market, supported by its versatile applications, ease of use, and compatibility with a wide range of industrial processes and end-user requirements.

Sulfur Market Share Analysis: Prilling is poised to register the fastest CAGR over the forecast period

In the sulfur market, the Prilling segment is the fastest-growing. Prilling technology involves the formation of small spherical pellets or beads of sulfur through a process known as prilling. These sulfur prills are uniform in size and shape, making them ideal for various applications across industries such as agriculture, chemicals, and pharmaceuticals. One of the primary reasons for the rapid growth of the Prilling segment is its efficiency in sulfur handling and application. Sulfur prills have a high surface area-to-volume ratio, allowing for faster dissolution and dispersion when used as a soil amendment or fertilizer in agriculture. Additionally, prilled sulfur is preferred for use in the production of sulfuric acid and sulfur-based chemicals due to its uniform particle size distribution and ease of handling in industrial processes. Moreover, prilled sulfur offers advantages in transportation and storage compared to other forms such as granules or pastilles. Sulfur prills are less prone to dust generation and caking, reducing material loss and handling risks during storage and transportation. Furthermore, advancements in prilling technology have led to improvements in process efficiency, product quality, and environmental sustainability, driving the adoption of prilled sulfur in various applications. As a result of these factors, the Prilling segment experiences rapid growth within the sulfur market, propelled by its efficiency, versatility, and advantages in handling, application, and industrial processing.

Sulfur Market Share Analysis: Fertilizer segment generated the highest revenue in 2024

In the sulfur market, the Fertilizer segment is the largest, primarily due to the extensive use of sulfur in agricultural applications. Sulfur is an essential nutrient for plant growth and development, playing a crucial role in various physiological processes such as enzyme activation, protein synthesis, and chlorophyll formation. Sulfur deficiency in soil can result in reduced crop yields and poor quality of agricultural produce. As a result, sulfur fertilizers are widely used to supplement sulfur deficiencies in soil and enhance crop productivity and quality. Additionally, sulfur is a key component of sulfuric acid, which is one of the most widely used fertilizers globally. Sulfuric acid is used in the production of phosphate fertilizers such as ammonium phosphate and triple superphosphate, where it reacts with phosphate rock to form soluble phosphate compounds that are readily available to plants. Moreover, elemental sulfur is also used directly as a soil amendment or fertilizer in the form of sulfur prills, pellets, or powders. The Fertilizer segment dominates the sulfur market due to the large-scale agricultural activities worldwide and the increasing demand for sulfur-containing fertilizers to meet the growing food requirements of a rapidly expanding global population. As a result, the Fertilizer segment maintains its position as the largest within the sulfur market, supported by the critical role of sulfur in enhancing agricultural productivity and addressing soil nutrient deficiencies.

Sulfur Market

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Sulfur Companies Profiled in the Study

ADNOC Group

China Petrochemical Corp

Gazprom International Ltd

Marathon Petroleum Company LLC

Petrovietnam Chemical and Services Corp (PVCHEM)

Royal Dutch Shell plc

Saudi Arabian Oil Co.

Suncor Energy Inc

Tengizchevroil LLP

Valero Energy Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Sulfur Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Sulfur Market Size Outlook, $ Million, 2021 to 2032

3.2 Sulfur Market Outlook by Type, $ Million, 2021 to 2032

3.3 Sulfur Market Outlook by Product, $ Million, 2021 to 2032

3.4 Sulfur Market Outlook by Application, $ Million, 2021 to 2032

3.5 Sulfur Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Sulfur Industry

4.2 Key Market Trends in Sulfur Industry

4.3 Potential Opportunities in Sulfur Industry

4.4 Key Challenges in Sulfur Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Sulfur Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Sulfur Market Outlook by Segments

7.1 Sulfur Market Outlook by Segments, $ Million, 2021- 2032

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

8 North America Sulfur Market Analysis and Outlook To 2032

8.1 Introduction to North America Sulfur Markets in 2024

8.2 North America Sulfur Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Sulfur Market size Outlook by Segments, 2021-2032

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

9 Europe Sulfur Market Analysis and Outlook To 2032

9.1 Introduction to Europe Sulfur Markets in 2024

9.2 Europe Sulfur Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Sulfur Market Size Outlook by Segments, 2021-2032

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

10 Asia Pacific Sulfur Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Sulfur Markets in 2024

10.2 Asia Pacific Sulfur Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Sulfur Market size Outlook by Segments, 2021-2032

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

11 South America Sulfur Market Analysis and Outlook To 2032

11.1 Introduction to South America Sulfur Markets in 2024

11.2 South America Sulfur Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Sulfur Market size Outlook by Segments, 2021-2032

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

12 Middle East and Africa Sulfur Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Sulfur Markets in 2024

12.2 Middle East and Africa Sulfur Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Sulfur Market size Outlook by Segments, 2021-2032

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ADNOC Group

China Petrochemical Corp

Gazprom International Ltd

Marathon Petroleum Company LLC

Petrovietnam Chemical and Services Corp (PVCHEM)

Royal Dutch Shell plc

Saudi Arabian Oil Co.

Suncor Energy Inc

Tengizchevroil LLP

Valero Energy Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Form

Solid

Liquid

By Technology

Granules

Pastilles

Prilling

By End-User

Fertilizer

Chemical Processing

Metal Manufacturing

Rubber Processing

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)