The global Syngas and Derivatives Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Primary Constituents (Methanol, Dimethyl Ether, Ammonia, Oxo Chemicals, Hydrogen), By Derivative (Formaldehyde, Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP), Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME), Dimethyl Terephthalate (DMT), Acetic Acid, Dimethyl Ether (DME), Methyl Methacrylate (MMA)), By Application (Aerosol Products, LPG Blending, Power Generation, Transportation Fuel, Acrylates, Glycol Ethers, Acetates, Lubes, Resins, Others), By End-User (Agriculture, Textiles, Mining, Pharmaceutical, Refrigeration, Chemicals, Transportation, Energy, Refining, Welding and Metal Fabrication, Others).

Syngas (synthesis gas), a mixture of carbon monoxide (CO) and hydrogen (H2), s to be a versatile feedstock for the production of various chemicals and fuels in 2024. Syngas is produced through the gasification of carbon-containing feedstocks such as coal, natural gas, biomass, or municipal solid waste. It serves as a precursor for the synthesis of a wide range of valuable products, including methanol, ammonia, synthetic fuels, and synthetic natural gas (SNG). These syngas-derived chemicals and fuels are used in industries such as chemicals, refining, fertilizers, and transportation, contributing to energy security, resource efficiency, and environmental sustainability. With advancements in gasification technology, catalysis, and process integration, syngas production and utilization to evolve, offering opportunities for cleaner and more efficient pathways for chemical and energy production.

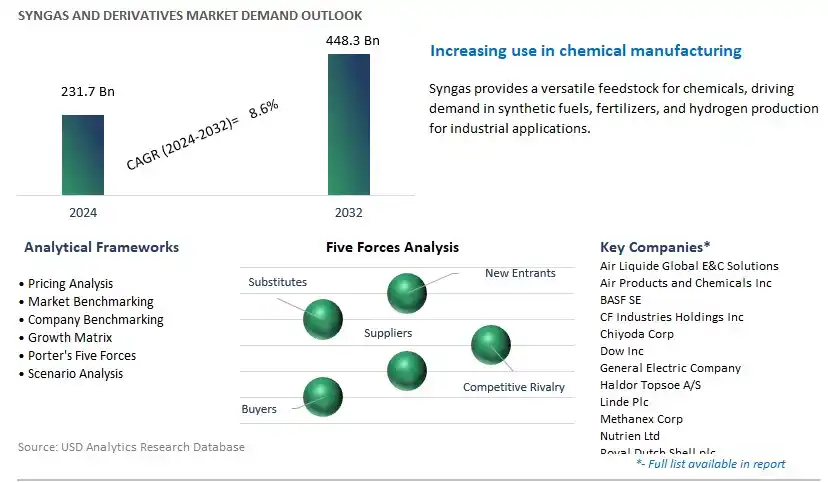

The market report analyses the leading companies in the industry including Air Liquide Global E&C Solutions, Air Products and Chemicals Inc, BASF SE, CF Industries Holdings Inc, Chiyoda Corp, Dow Inc, General Electric Company, Haldor Topsoe A/S, Linde Plc, Methanex Corp, Nutrien Ltd, Royal Dutch Shell plc, Sasol Ltd, Siemens AG, SynGas Technology LLC, Synthesis Energy Systems Inc, TechnipFMC PLC, and others.

A significant trend in the syngas and derivatives market is the shift towards sustainable energy sources and chemical production methods. With increasing concerns about climate change and environmental degradation, there is a growing emphasis on reducing greenhouse gas emissions and transitioning towards cleaner and more sustainable energy and chemical processes. Syngas, a mixture of carbon monoxide and hydrogen, is a versatile intermediate used in the production of various chemicals, fuels, and materials. The trend towards sustainability is driving the adoption of syngas-based processes such as gasification, steam reforming, and biomass conversion, which utilize renewable feedstocks such as biomass, municipal solid waste, and agricultural residues to produce syngas. Additionally, advancements in carbon capture and utilization (CCU) technologies enable the conversion of carbon dioxide into valuable chemicals and fuels using syngas as a precursor, contributing to the circular economy and reducing reliance on fossil fuels. As industries seek to reduce their carbon footprint and comply with regulatory mandates for emissions reduction, the demand for syngas and derivatives produced from sustainable sources is expected to grow.

The primary driver for the syngas and derivatives market is the growth in chemical and petrochemical industries worldwide, which rely on syngas as a key raw material for the production of a wide range of chemicals, fuels, and intermediates. Syngas serves as a feedstock for the synthesis of methanol, ammonia, hydrogen, synthetic natural gas (SNG), and various other products used in industries such as fertilizers, plastics, pharmaceuticals, and synthetic fibers. With urbanization, industrialization, and economic development driving demand for consumer goods and infrastructure, there is an increasing need for basic chemicals and intermediates derived from syngas to meet market demand. Additionally, the shale gas revolution and the availability of abundant natural gas resources in regions such as North America have spurred investments in syngas-based projects, including methanol-to-olefins (MTO) and methanol-to-propylene (MTP) plants, to capitalize on cost-competitive feedstocks and gain a competitive edge in the global chemical market. As emerging economies continue to industrialize and demand for chemical products grows, the demand for syngas and derivatives is expected to remain strong.

A significant opportunity for the syngas and derivatives market lies in the integration of syngas technologies with renewable energy sources such as wind, solar, and biomass. As the world transitions towards a low-carbon economy and seeks to reduce dependence on fossil fuels, there is a growing interest in renewable energy technologies that can produce clean hydrogen and syngas for various applications. Renewable sources such as biomass gasification, solar-driven water splitting, and wind-powered electrolysis offer opportunities to produce syngas sustainably without carbon emissions, contributing to decarbonization efforts and energy diversification. By leveraging advancements in renewable energy technologies and integrating them with syngas production processes, stakeholders can develop integrated energy systems that provide a reliable and sustainable source of syngas for chemical synthesis, power generation, and transportation fuels. Additionally, the integration of renewable syngas technologies with energy storage solutions such as hydrogen fuel cells and battery systems offers opportunities to address intermittency issues and enhance the flexibility and reliability of renewable energy systems. By embracing this opportunity, stakeholders can unlock new markets, reduce environmental impact, and contribute to the transition towards a more sustainable and resilient energy future.

Among the primary constituents delineated in the Syngas & Derivatives Market segmentation, Methanol is the largest segment. Methanol holds this prominent position due to its multifaceted applications across various industries. Methanol is a versatile chemical compound used as a feedstock in the production of numerous downstream chemicals and materials, including formaldehyde, acetic acid, olefins, and methyl tert-butyl ether (MTBE), among others. Its widespread use in the synthesis of value-added chemicals makes it a pivotal component in the syngas and derivatives market. Additionally, Methanol serves as a clean-burning alternative fuel, offering significant environmental benefits over traditional fossil fuels. Its adoption as a fuel in transportation and power generation sectors further contributes to its dominance in the market. Moreover, ongoing advancements in Methanol production technologies, such as syngas-based and biomass-to-methanol processes, enhance its economic viability and sustainability, driving its continued growth and market leadership. As industries continue to seek cleaner and more efficient alternatives, Methanol is poised to maintain its position as the largest segment in the syngas and derivatives market.

The Methanol-to-Olefins (MTO)/Methanol-to-Propylene (MTP) segment stands out as the fastest-growing segment in the Syngas & Derivatives Market. First and foremost, MTO/MTP processes offer a highly efficient and cost-effective route for the production of valuable olefin products, such as ethylene and propylene, from methanol feedstock. Ethylene and propylene are essential building blocks for various downstream industries, including plastics, chemicals, and polymers, driving robust demand for MTO/MTP-derived products. Moreover, the MTO/MTP process enables the utilization of abundant and low-cost methanol feedstock, especially in regions with significant methanol production capacities, further enhancing its attractiveness. Additionally, advancements in catalyst technologies and process optimization have improved the efficiency and yield of MTO/MTP processes, making them increasingly competitive against traditional steam cracking methods. As industries continue to seek sustainable and economically viable alternatives for olefin production, the MTO/MTP segment is expected to witness continued rapid growth, consolidating its position as a key driver in the Syngas & Derivatives Market.

The Power Generation segment is the largest segment in the Syngas & Derivatives Market. The large revenue share is primarily driven by the growing global demand for electricity and the increasing adoption of syngas-based power generation technologies. Syngas, a versatile fuel derived from various feedstocks such as coal, natural gas, biomass, and municipal solid waste, serves as a vital feedstock for power generation applications. Syngas-based power plants offer potential advantages, including lower emissions, greater fuel flexibility, and improved energy efficiency compared to traditional fossil fuel-based power plants. Moreover, advancements in gasification and combined cycle technologies have enhanced the efficiency and reliability of syngas-based power generation systems, further bolstering their appeal. Additionally, stringent environmental regulations aimed at reducing greenhouse gas emissions and promoting cleaner energy sources are driving the adoption of syngas-based power generation as a sustainable alternative. As the global demand for electricity continues to rise and governments prioritize clean energy initiatives, the Power Generation segment is expected to maintain its leadership position in the Syngas & Derivatives Market.

Within the Syngas & Derivatives Market, the Chemicals segment stands out as the fastest-growing segment. This rapid growth can be attributed to syngas serves as a crucial building block for a wide range of chemical products, including methanol, ammonia, and various hydrocarbons. These chemicals find extensive applications across numerous industries, such as manufacturing, construction, automotive, and pharmaceuticals. Additionally, advancements in syngas production technologies, such as steam reforming and gasification, have significantly enhanced the efficiency and cost-effectiveness of chemical production processes. Moreover, the growing global demand for petrochemicals and specialty chemicals, driven by population growth, urbanization, and industrialization, is fuelling the expansion of the Chemicals segment. Furthermore, increasing environmental concerns and regulations are prompting chemical manufacturers to explore cleaner and more sustainable production methods, with syngas-based processes offering a viable solution. As a result, the Chemicals segment is expected to experience robust growth in the coming years, driving the overall expansion of the Syngas & Derivatives Market.

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Air Liquide Global E&C Solutions

Air Products and Chemicals Inc

BASF SE

CF Industries Holdings Inc

Chiyoda Corp

Dow Inc

General Electric Company

Haldor Topsoe A/S

Linde Plc

Methanex Corp

Nutrien Ltd

Royal Dutch Shell plc

Sasol Ltd

Siemens AG

SynGas Technology LLC

Synthesis Energy Systems Inc

TechnipFMC PLC

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Syngas and Derivatives Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Syngas and Derivatives Market Size Outlook, $ Million, 2021 to 2032

3.2 Syngas and Derivatives Market Outlook by Type, $ Million, 2021 to 2032

3.3 Syngas and Derivatives Market Outlook by Product, $ Million, 2021 to 2032

3.4 Syngas and Derivatives Market Outlook by Application, $ Million, 2021 to 2032

3.5 Syngas and Derivatives Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Syngas and Derivatives Industry

4.2 Key Market Trends in Syngas and Derivatives Industry

4.3 Potential Opportunities in Syngas and Derivatives Industry

4.4 Key Challenges in Syngas and Derivatives Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Syngas and Derivatives Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Syngas and Derivatives Market Outlook by Segments

7.1 Syngas and Derivatives Market Outlook by Segments, $ Million, 2021- 2032

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

8 North America Syngas and Derivatives Market Analysis and Outlook To 2032

8.1 Introduction to North America Syngas and Derivatives Markets in 2024

8.2 North America Syngas and Derivatives Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Syngas and Derivatives Market size Outlook by Segments, 2021-2032

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

9 Europe Syngas and Derivatives Market Analysis and Outlook To 2032

9.1 Introduction to Europe Syngas and Derivatives Markets in 2024

9.2 Europe Syngas and Derivatives Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Syngas and Derivatives Market Size Outlook by Segments, 2021-2032

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

10 Asia Pacific Syngas and Derivatives Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Syngas and Derivatives Markets in 2024

10.2 Asia Pacific Syngas and Derivatives Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Syngas and Derivatives Market size Outlook by Segments, 2021-2032

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

11 South America Syngas and Derivatives Market Analysis and Outlook To 2032

11.1 Introduction to South America Syngas and Derivatives Markets in 2024

11.2 South America Syngas and Derivatives Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Syngas and Derivatives Market size Outlook by Segments, 2021-2032

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

12 Middle East and Africa Syngas and Derivatives Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Syngas and Derivatives Markets in 2024

12.2 Middle East and Africa Syngas and Derivatives Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Syngas and Derivatives Market size Outlook by Segments, 2021-2032

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Air Liquide Global E&C Solutions

Air Products and Chemicals Inc

BASF SE

CF Industries Holdings Inc

Chiyoda Corp

Dow Inc

General Electric Company

Haldor Topsoe A/S

Linde Plc

Methanex Corp

Nutrien Ltd

Royal Dutch Shell plc

Sasol Ltd

Siemens AG

SynGas Technology LLC

Synthesis Energy Systems Inc

TechnipFMC PLC

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Primary Constituents

Methanol

Dimethyl Ether

Ammonia

Oxo Chemicals

Hydrogen

By Derivative

Formaldehyde

Methanol-to-olefins (MTO)/Methanol-to-Propylene (MTP)

Methyl Tert-butyl Ether (MTBE)/ Tertiary Amyl Methyl Ether (TAME)

Dimethyl Terephthalate (DMT)

Acetic Acid

Dimethyl Ether (DME)

Methyl Methacrylate (MMA)

By Application

Aerosol Products

LPG Blending

Power Generation

Transportation Fuel

Acrylates

Glycol Ethers

Acetates

Lubes

Resins

Others

By End-User

Agriculture

Textiles

Mining

Pharmaceutical

Refrigeration

Chemicals

Transportation

Energy

Refining

Welding and Metal Fabrication

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Global Syngas and Derivatives Market Size is valued at $231.7 Billion in 2024 and is forecast to register a growth rate (CAGR) of 8.6% to reach $448.3 Billion by 2032.

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

Air Liquide Global E&C Solutions, Air Products and Chemicals Inc, BASF SE, CF Industries Holdings Inc, Chiyoda Corp, Dow Inc, General Electric Company, Haldor Topsoe A/S, Linde Plc, Methanex Corp, Nutrien Ltd, Royal Dutch Shell plc, Sasol Ltd, Siemens AG, SynGas Technology LLC, Synthesis Energy Systems Inc, TechnipFMC PLC

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2032; Currency: Revenue (USD); Volume