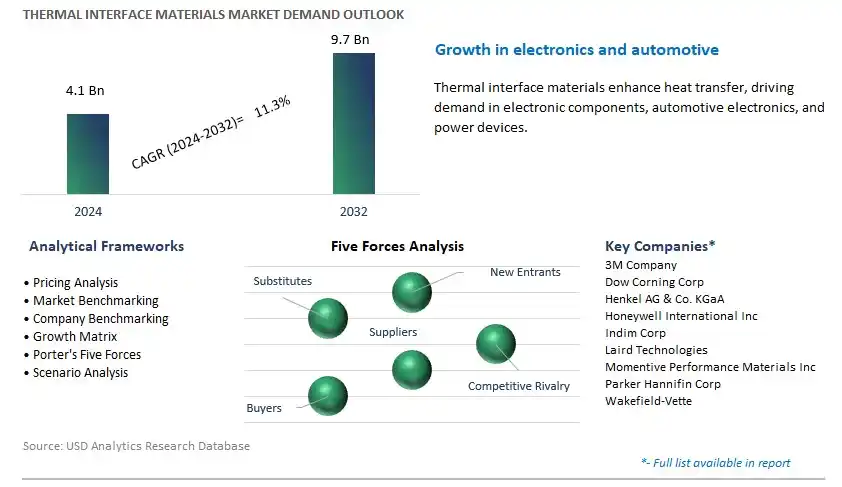

Global Thermal Interface Materials Market Size is valued at $4.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 11.3% to reach $9.7 Billion by 2032.

The global Thermal Interface Materials Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Tapes and films, Elastomeric Pads, Greases and Adhesives, Phase change materials, Metal Based, Others), By Application (Telecom, Computer, Medical devices, Industrial machinery, Consumer Durables, Automotive Electronics, Others).

An Introduction to Thermal Interface Materials Market in 2024

Thermal interface materials (TIMs) play a crucial role in managing heat dissipation and thermal conductivity in electronic devices and power systems in 2024. These materials are used to fill gaps and voids between heat-generating components and heat sinks, improving thermal contact and enhancing heat transfer efficiency. Thermal interface materials encompass a variety of products, including thermal greases, thermal pads, phase change materials, and thermal adhesives, each offering specific advantages in terms of thermal conductivity, flexibility, and ease of application. In industries such as electronics, automotive, telecommunications, and renewable energy, thermal interface materials help to prevent overheating, improve device reliability, and extend the lifespan of electronic components and power systems. With advancements in semiconductor technology, power density, and miniaturization, the demand for high-performance thermal interface materials s to rise, driving innovations in material formulations, packaging techniques, and thermal management strategies.

Thermal Interface Materials Market Competitive Landscape

The market report analyses the leading companies in the industry including 3M Company, Dow Corning Corp, Henkel AG & Co. KGaA, Honeywell International Inc, Indim Corp, Laird Technologies, Momentive Performance Materials Inc, Parker Hannifin Corp, Wakefield-Vette, and others.

Thermal Interface Materials Market Dynamics

Market Trend: Increasing Demand for Thermal Management Solutions

A significant trend in the thermal interface materials (TIMs) market is the increasing demand for thermal management solutions across various industries. With the proliferation of electronic devices, electric vehicles, renewable energy systems, and high-performance computing, there is a growing need to manage heat generated by electronic components and systems effectively. Thermal interface materials play a crucial role in optimizing heat transfer between electronic components and heat sinks, ensuring efficient thermal dissipation and preventing overheating. As industries strive for smaller, faster, and more powerful devices, the demand for TIMs with superior thermal conductivity, reliability, and thermal stability is expected to continue growing. Additionally, emerging applications such as 5G infrastructure, Internet of Things (IoT) devices, and artificial intelligence (AI) systems are driving demand for TIMs that can meet the unique thermal management challenges of these technologies. As a result, the TIMs market is experiencing significant expansion, driven by the need for materials that offer effective thermal management solutions in diverse applications and environments.

Market Driver: Technological Advancements and Miniaturization of Electronic Devices

The primary driver for the thermal interface materials market is technological advancements and the miniaturization of electronic devices. As electronic devices become smaller, lighter, and more powerful, there is a growing demand for TIMs that can efficiently dissipate heat from densely packed components in limited spaces. Technological advancements in materials science, nanotechnology, and manufacturing processes have enabled the development of TIMs with higher thermal conductivity, lower thermal resistance, and improved performance characteristics. Additionally, the transition to advanced packaging technologies such as flip-chip, system-in-package (SiP), and three-dimensional (3D) stacking has increased the complexity of thermal management challenges, driving the need for innovative TIM solutions. As manufacturers of electronic devices seek to improve performance, reliability, and longevity of their products, the demand for TIMs that offer superior thermal management capabilities is expected to grow. Furthermore, advancements in electric vehicle (EV) battery technology and renewable energy systems are creating opportunities for TIMs to enhance thermal management in battery packs, power electronics, and energy storage systems, driving further market growth and innovation.

Market Opportunity: Development of Next-Generation TIMs and Application-Specific Solutions

A significant opportunity for the thermal interface materials market lies in the development of next-generation TIMs and application-specific solutions that address evolving industry requirements and challenges. Manufacturers have the opportunity to invest in research and development to create TIMs with enhanced thermal conductivity, reduced thermal resistance, and improved reliability to meet the demands of high-performance electronic devices and systems. This includes the development of advanced materials such as graphene, carbon nanotubes, and metal-based nanocomposites, as well as novel manufacturing techniques to optimize material properties and performance. Additionally, there is an opportunity to provide application-specific TIM solutions tailored to the unique thermal management needs of different industries and end-use applications. This includes TIMs optimized for specific electronic devices, automotive components, telecommunications equipment, and renewable energy systems, as well as TIMs compatible with emerging technologies such as 5G, IoT, and AI. By collaborating with customers, semiconductor manufacturers, and system integrators, TIM manufacturers can identify unmet needs, develop innovative solutions, and capitalize on opportunities to differentiate their products in the market. As industries continue to demand high-performance thermal management solutions, the development of next-generation TIMs presents opportunities for growth, innovation, and market leadership in the thermal interface materials industry.

Thermal Interface Materials Market Share Analysis: Tapes and Films segment generated the highest revenue in 2024

Among the diverse array of products in thermal Interface Materials Market, the Tapes and Films segment is the largest and most significant player. Tapes and films offer a versatile and cost-effective solution for thermal management in various electronic and industrial applications. They are designed to provide efficient heat transfer between heat-generating components such as processors, integrated circuits, and heat sinks, ensuring optimal performance and reliability. Tapes and films are engineered with advanced materials such as silicone, acrylic, and polyimide, offering excellent thermal conductivity, electrical insulation, and durability. Moreover, their ease of application, flexibility, and compatibility with automated manufacturing processes make them preferred choices for thermal management solutions in industries such as electronics, telecommunications, automotive, and aerospace. Additionally, the growing demand for compact and lightweight electronic devices, coupled with the increasing adoption of advanced cooling technologies, drives the market for tapes and films in thermal interface applications. With ongoing advancements in material science and manufacturing techniques, the Tapes and Films segment is poised to maintain its leadership position and witness continued growth in thermal interface materials market.

Thermal Interface Materials Market Share Analysis: Medical Devices Application is poised to register the fastest CAGR over the forecast period

Among the diverse applications driving thermal Interface Materials (TIM) Market, the Medical Devices segment is the fastest-growing player. In the medical devices industry, thermal management is crucial for ensuring the reliability and performance of electronic components used in diagnostic equipment, patient monitoring devices, imaging systems, and other healthcare devices. As medical technology advances and the demand for more sophisticated and compact medical devices increases, the need for effective thermal management solutions becomes paramount. Thermal interface materials play a vital role in dissipating heat generated by electronic components, preventing overheating, and maintaining device functionality and longevity. The adoption of advanced medical technologies, such as wearable devices, remote patient monitoring systems, and minimally invasive surgical tools, further fuels the demand for thermal interface materials in the medical devices sector. Moreover, stringent regulatory requirements for product safety and reliability in the healthcare industry drive the adoption of high-performance thermal management solutions, propelling the growth of the Medical Devices segment in thermal interface materials market. As the healthcare sector continues to innovate and evolve, the demand for thermal interface materials in medical devices is expected to witness sustained growth, positioning this segment as a key driver in thermal interface materials market landscape.

Thermal Interface Materials Market

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Thermal Interface Materials Companies Profiled in the Study

3M Company

Dow Corning Corp

Henkel AG & Co. KGaA

Honeywell International Inc

Indim Corp

Laird Technologies

Momentive Performance Materials Inc

Parker Hannifin Corp

Wakefield-Vette

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Thermal Interface Materials Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Thermal Interface Materials Market Size Outlook, $ Million, 2021 to 2032

3.2 Thermal Interface Materials Market Outlook by Type, $ Million, 2021 to 2032

3.3 Thermal Interface Materials Market Outlook by Product, $ Million, 2021 to 2032

3.4 Thermal Interface Materials Market Outlook by Application, $ Million, 2021 to 2032

3.5 Thermal Interface Materials Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Thermal Interface Materials Industry

4.2 Key Market Trends in Thermal Interface Materials Industry

4.3 Potential Opportunities in Thermal Interface Materials Industry

4.4 Key Challenges in Thermal Interface Materials Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Thermal Interface Materials Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Thermal Interface Materials Market Outlook by Segments

7.1 Thermal Interface Materials Market Outlook by Segments, $ Million, 2021- 2032

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

8 North America Thermal Interface Materials Market Analysis and Outlook To 2032

8.1 Introduction to North America Thermal Interface Materials Markets in 2024

8.2 North America Thermal Interface Materials Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Thermal Interface Materials Market size Outlook by Segments, 2021-2032

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

9 Europe Thermal Interface Materials Market Analysis and Outlook To 2032

9.1 Introduction to Europe Thermal Interface Materials Markets in 2024

9.2 Europe Thermal Interface Materials Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Thermal Interface Materials Market Size Outlook by Segments, 2021-2032

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

10 Asia Pacific Thermal Interface Materials Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Thermal Interface Materials Markets in 2024

10.2 Asia Pacific Thermal Interface Materials Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Thermal Interface Materials Market size Outlook by Segments, 2021-2032

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

11 South America Thermal Interface Materials Market Analysis and Outlook To 2032

11.1 Introduction to South America Thermal Interface Materials Markets in 2024

11.2 South America Thermal Interface Materials Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Thermal Interface Materials Market size Outlook by Segments, 2021-2032

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

12 Middle East and Africa Thermal Interface Materials Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Thermal Interface Materials Markets in 2024

12.2 Middle East and Africa Thermal Interface Materials Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Thermal Interface Materials Market size Outlook by Segments, 2021-2032

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

3M Company

Dow Corning Corp

Henkel AG & Co. KGaA

Honeywell International Inc

Indim Corp

Laird Technologies

Momentive Performance Materials Inc

Parker Hannifin Corp

Wakefield-Vette

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Tapes and films

Elastomeric Pads

Greases and Adhesives

Phase change materials

Metal Based

Others

By Application

Telecom

Computer

Medical devices

Industrial machinery

Consumer Durables

Automotive Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)