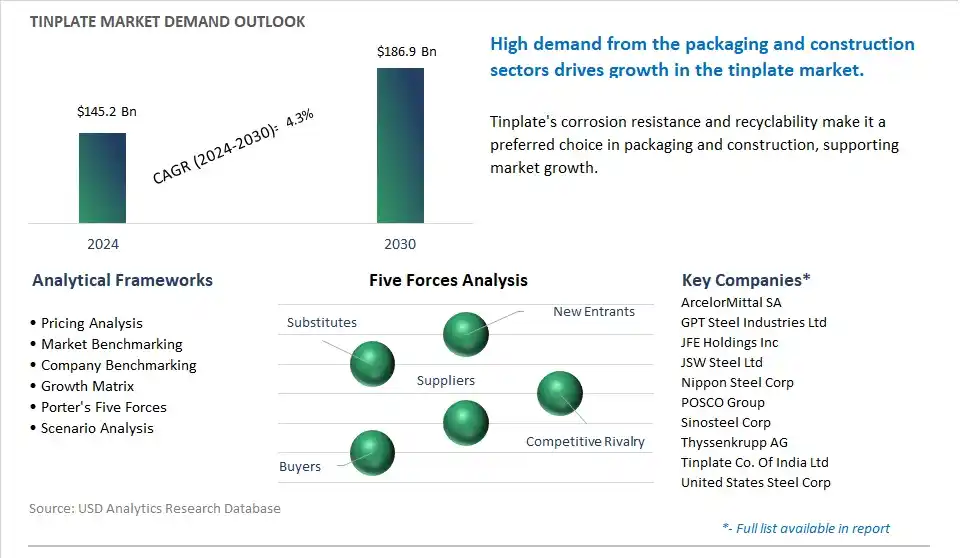

The global Tinplate Market is poised to register a 4.3% CAGR from $145.2 Billion in 2024 to $186.9 Billion in 2030.

The global Tinplate Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Cans, Drums and pails, Aerosols, Lids, Others), By Metal (Steel, Iron), By End-User (Food and beverage, Personal care, Others).

An Introduction to Global Tinplate Market in 2024

The tinplate market is witnessing steady growth driven by increasing demand in packaging, construction, electronics, and automotive industries for its corrosion resistance, formability, and aesthetic appeal. Key trends shaping the future of the industry include the rising adoption of tinplate for food and beverage packaging, aerosol cans, battery casings, and decorative applications, driven by its ability to protect against rust and contamination while offering branding opportunities and consumer convenience. Moreover, there's a growing emphasis on sustainability and recycling, leading to investments in tinplate recycling infrastructure and eco-friendly coatings to enhance material recovery and reduce environmental impact. Additionally, advancements in tinplate production processes, surface treatment methods, and printing technologies are driving innovation and market differentiation, enabling manufacturers to offer customized solutions for diverse packaging requirements and market trends, thereby fueling market growth and competitiveness in the global tinplate market.

Tinplate Market Competitive Landscape

The market report analyses the leading companies in the industry including ArcelorMittal SA, GPT Steel Industries Ltd, JFE Holdings Inc, JSW Steel Ltd, Nippon Steel Corp, POSCO Group, Sinosteel Corp, Thyssenkrupp AG, Tinplate Co. Of India Ltd, United States Steel Corp.

Tinplate Market Dynamics

Tinplate Market Trend: Increasing Demand for Sustainable Packaging Solutions

The most prominent market trend for tinplate is the increasing demand for sustainable packaging solutions. Tinplate, consisting of thin steel sheets coated with a layer of tin to prevent corrosion, is widely used in packaging applications such as food and beverage cans, aerosol containers, and metal closures. With growing environmental concerns and consumer preferences for eco-friendly packaging, there's a shift towards using recyclable and reusable materials like tinplate. This trend is driven by regulatory initiatives promoting recycling and waste reduction, as well as corporate sustainability goals aimed at minimizing environmental impact throughout the product lifecycle. As a result, tinplate manufacturers are exploring innovative coatings and processing techniques to enhance recyclability and reduce the carbon footprint of tinplate packaging.

Tinplate Market Driver: Growth in Food and Beverage Industry

A key market driver for tinplate is the growth in the food and beverage industry worldwide. Tinplate is a preferred packaging material for canned foods, beverages, and processed goods due to its barrier properties, durability, and shelf-life preservation capabilities. With changes in consumer lifestyles, dietary habits, and purchasing behaviors, there's an increasing demand for packaged food and beverage products that offer convenience, portability, and extended shelf life. The expansion of food processing, packaging, and distribution sectors drives the demand for tinplate, creating opportunities for manufacturers to innovate and develop new packaging formats, sizes, and functionalities to meet the evolving needs of consumers.

Tinplate Market Opportunity: Expansion into Emerging Markets and Applications

An exciting opportunity in the tinplate market lies in expansion into emerging markets and applications beyond traditional packaging sectors. While tinplate is predominantly used in food and beverage packaging, there's potential for growth in sectors such as cosmetics, pharmaceuticals, and industrial products that require durable and corrosion-resistant packaging solutions. Tinplate can be utilized in packaging for beauty and personal care products, pharmaceuticals, chemicals, and specialty goods where product integrity and protection are essential. By targeting emerging applications and markets, tinplate manufacturers can diversify their customer base, explore new revenue streams, and capitalize on the versatility and adaptability of tinplate as a packaging material. Additionally, the development of innovative coatings, printing techniques, and decorative finishes for tinplate packaging presents opportunities for differentiation and value creation in the market. This opportunity allows tinplate manufacturers to expand their market reach, strengthen their competitive position, and drive growth through strategic diversification initiatives aimed at addressing evolving consumer needs and market trends.

Tinplate Market Share Analysis: The Cans segment generated the highest revenue in 2024

The largest segment in the Tinplate Market is Cans. This dominance is driven by that make tinplate cans the preferred choice in various industries and applications. Tinplate cans are widely used for packaging food and beverages, including canned fruits, vegetables, soups, meats, seafood, and carbonated drinks. They offer Diverse key advantages that make them popular among consumers and manufacturers alike. tinplate cans provide excellent barrier properties against moisture, oxygen, light, and other external factors, ensuring the preservation of food quality, flavor, and shelf life. Further, tinplate cans are lightweight, durable, and stackable, offering convenience in storage, transportation, and handling. In addition, tinplate cans are recyclable and environmentally friendly, contributing to sustainability goals and reducing environmental impact compared to alternative packaging materials. Additionally, advancements in tinplate manufacturing technologies have improved can designs, production efficiency, and cost-effectiveness, further driving the adoption of tinplate cans in various industries. With the growing demand for packaged food and beverages worldwide, particularly in emerging economies, the demand for tinplate cans is expected to remain strong, maintaining their position as the largest segment in the Tinplate Market.

Tinplate Market Share Analysis: The Steel segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Tinplate Market is Steel. This rapid growth is driven by the increasing demand for steel tinplate in various industries and applications. Steel tinplate offers potential advantages over iron tinplate that make it increasingly preferred by manufacturers and consumers. steel tinplate provides superior strength, durability, and corrosion resistance compared to iron tinplate, making it suitable for a wide range of packaging applications, including food and beverage cans, aerosol cans, and containers for chemicals and pharmaceuticals. Further, steel tinplate offers better formability and weldability, allowing for the production of complex shapes and designs with high precision and consistency. In addition, steel tinplate can be produced in thinner gauges while maintaining structural integrity, resulting in lighter-weight packaging solutions that reduce material usage and transportation costs. Additionally, advancements in steelmaking technologies have improved the quality, performance, and cost-effectiveness of steel tinplate, further driving its adoption in the packaging industry. Furthermore, the growing emphasis on sustainability, recyclability, and environmental responsibility has led to increased demand for steel tinplate, as steel is highly recyclable and can be reused multiple times without losing its properties. As industries continue to prioritize efficient and eco-friendly packaging solutions, the demand for steel tinplate is expected to continue growing rapidly, making it the fastest-growing segment in the Tinplate Market.

Tinplate Market Share Analysis: The Food and Beverage segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Tinplate Market is the Food and Beverage sector. This rapid growth is driven by the increasing demand for tinplate packaging in the food and beverage industry. Tinplate offers potential advantages for food and beverage packaging that make it highly preferred by manufacturers and consumers alike. tinplate provides excellent barrier properties against moisture, oxygen, light, and other external factors, ensuring the preservation of food quality, flavor, and shelf life. Further, tinplate is safe and hygienic for food contact, meeting regulatory standards for food packaging materials. In addition, tinplate cans are lightweight, durable, and stackable, offering convenience in storage, transportation, and handling for both manufacturers and consumers. Additionally, tinplate packaging can be customized with various printing and decorative options to enhance product visibility, branding, and consumer appeal. Furthermore, the growing demand for packaged food and beverages, including canned fruits, vegetables, soups, meats, seafood, and carbonated drinks, is driving the need for efficient and sustainable packaging solutions. As consumers continue to seek convenient, safe, and environmentally friendly packaging options, the demand for tinplate packaging in the food and beverage industry is expected to continue growing rapidly, making it the fastest-growing segment in the Tinplate Market.

Tinplate Market Report Segmentation

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Tinplate Companies Profiled in the Market Study

ArcelorMittal SA

GPT Steel Industries Ltd

JFE Holdings Inc

JSW Steel Ltd

Nippon Steel Corp

POSCO Group

Sinosteel Corp

Thyssenkrupp AG

Tinplate Co. Of India Ltd

United States Steel Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Tinplate Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Tinplate Market Size Outlook, $ Million, 2021 to 2030

3.2 Tinplate Market Outlook by Type, $ Million, 2021 to 2030

3.3 Tinplate Market Outlook by Product, $ Million, 2021 to 2030

3.4 Tinplate Market Outlook by Application, $ Million, 2021 to 2030

3.5 Tinplate Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Tinplate Industry

4.2 Key Market Trends in Tinplate Industry

4.3 Potential Opportunities in Tinplate Industry

4.4 Key Challenges in Tinplate Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Tinplate Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Tinplate Market Outlook by Segments

7.1 Tinplate Market Outlook by Segments, $ Million, 2021- 2030

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

8 North America Tinplate Market Analysis and Outlook To 2030

8.1 Introduction to North America Tinplate Markets in 2024

8.2 North America Tinplate Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Tinplate Market size Outlook by Segments, 2021-2030

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

9 Europe Tinplate Market Analysis and Outlook To 2030

9.1 Introduction to Europe Tinplate Markets in 2024

9.2 Europe Tinplate Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Tinplate Market Size Outlook by Segments, 2021-2030

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

10 Asia Pacific Tinplate Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Tinplate Markets in 2024

10.2 Asia Pacific Tinplate Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Tinplate Market size Outlook by Segments, 2021-2030

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

11 South America Tinplate Market Analysis and Outlook To 2030

11.1 Introduction to South America Tinplate Markets in 2024

11.2 South America Tinplate Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Tinplate Market size Outlook by Segments, 2021-2030

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

12 Middle East and Africa Tinplate Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Tinplate Markets in 2024

12.2 Middle East and Africa Tinplate Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Tinplate Market size Outlook by Segments, 2021-2030

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ArcelorMittal SA

GPT Steel Industries Ltd

JFE Holdings Inc

JSW Steel Ltd

Nippon Steel Corp

POSCO Group

Sinosteel Corp

Thyssenkrupp AG

Tinplate Co. Of India Ltd

United States Steel Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Cans

Drums and pails

Aerosols

Lids

Others

By Metal

Steel

Iron

By End-User

Food and beverage

Personal care

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)