United States Molybdenum Market Size

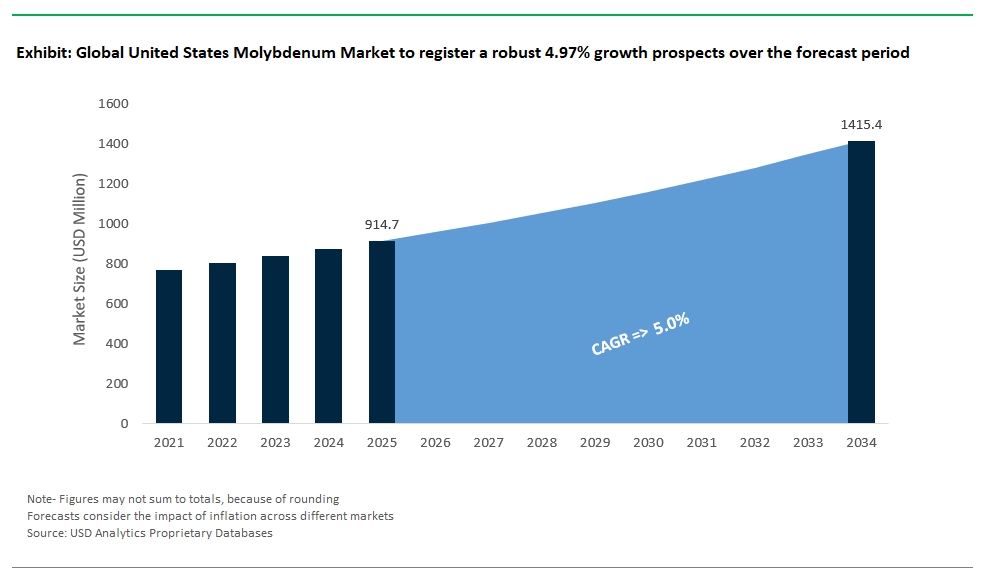

The US Molybdenum Market Size is estimated to increase at a 4.97% CAGR over the forecast period from $914.7 Million in 2025 to $1.4 Billion in 2034

The US molybdenum demand is driven by the increasing application of the refractory metal as an alloying agent in steel, cast iron, and superalloys to enhance hardenability, strength, toughness, and corrosion resistance properties. As U.S. manufacturing sectors including automotive, construction, and defense continue to require high-strength materials, the demand for molybdenum in steel production is on the rise. Special applications, like producing stainless and tool steel for the aerospace industry, in particular, support molybdenum's growth.

As the U.S. continues to refine its fuel mix and support petrochemical exports, molybdenum's role in catalytic processes is expected to grow. In addition, Molybdenum alloys play a critical role in producing energy-efficient and environmentally friendly technologies, which is boosting its use in the automotive and energy sectors. The U.S. steel industry accounted for over $300 billion with the increase in steel production driving higher molybdenum usage. Molybdenum’s high melting point and ability to withstand intense temperatures make it valuable in aerospace and defense applications, particularly in the production of turbine engines and missile components. The expansion of the U.S. aerospace industry, especially for military applications, drives the need for molybdenum in high-performance alloys and coatings.

The US oil and gas industry is one of the largest markets worldwide, with strong demand for molybdenum in drilling equipment and pipelines. In the oil & gas sector, molybdenum is essential in making pipelines and equipment resistant to extreme conditions, such as high-pressure, high-temperature environments, and corrosive elements. As U.S. domestic oil production remains robust, especially in shale regions like the Permian Basin, the need for molybdenum alloyed steels for drilling equipment and pipelines continues to drive demand. Further, with the U.S. transitioning towards a cleaner energy grid, molybdenum’s use in these emerging sectors is becoming increasingly significant. Molybdenum concentrate at primary molybdenum mines is produced in Colorado.

United States Molybdenum Market Analysis

Molybdenum concentrate at primary molybdenum mines is produced in Colorado. On the other hand, concentrate production from mines where molybdenum is obtained as a byproduct comes from six mines- Arizona (4), Montana (1), and Utah (1). On the supply-demand front, slow production in the US is encouraging global majors to boost their exports to the country. In addition to production growth in Asia Pacific, high molybdenum prices caused some consumers, especially in China, is freeing up volumes for export to the US. Currently, Peru, Chile, Mexico, South Korea, and others are the key exporters of molybdenum to the US. The US also exports a significant volume of Molybdenum to global markets.

According to the USGS, identified resources of molybdenum in the United States are about 5.4 million tons. Molybdenum occurs as the principal metal sulfide in large low-grade porphyry molybdenum deposits and as an associated metal sulfide in low-grade porphyry copper deposits. The recycling rate for molybdenum is relatively high in the country due to its value and the cost of extraction. Further, molybdenum from renewables is expected to increase steadily over the forecast period, presenting strong prospects for exporters.

United States Molybdenum Market Trends, Drivers, and Opportunities

Rising Use in Renewable Energy and Clean Technologies

The growing emphasis on reducing carbon emissions and transitioning to renewable energy is a major trend driving the U.S. molybdenum market. Molybdenum's unique properties, such as its strength at high temperatures, corrosion resistance, and catalytic abilities, make it a critical material in various clean technologies, particularly in solar energy, wind turbines, and energy storage systems.

The U.S. solar energy capacity has grown significantly, with over 150 gigawatts (GW) of installed capacity as of 2023, representing a 35% increase compared to the previous year. According to the Solar Energy Industries Association (SEIA), solar accounted for 54% of all new electricity-generating capacity added in the U.S. in 2022. Further, Molybdenum is used in wind turbine components, particularly in large bearings, gearboxes, and other critical parts that require high strength and corrosion resistance.

The U.S. wind energy market continues to expand, with over 140 GW of installed wind capacity as of 2023, and the sector is projected to grow by 60% by 2030. Offshore wind, which faces more demanding environmental conditions, is expected to account for 22 GW of this growth. As turbine technology advances to larger and more efficient designs, the use of molybdenum in key turbine components will likely increase.

In addition, The U.S. energy storage market is set to expand exponentially, with energy storage installations projected to reach 100 GW by 2030, a sharp increase from 12 GW in 2022. The role of molybdenum in energy storage systems, particularly in large-scale batteries, is becoming more prominent. In lithium-ion and other next-generation batteries, molybdenum compounds are used as catalysts and in the anode material.

Molybdenum-based catalysts are increasingly used in green hydrogen production, which is considered a critical technology for decarbonizing industries such as transportation, steel, and chemical processing. Molybdenum disulfide (MoSâ‚‚) acts as an efficient, cost-effective catalyst for hydrogen production through water electrolysis. Government policies are also fueling the use of molybdenum in renewable energy applications. Federal initiatives such as the Inflation Reduction Act (IRA) and the Infrastructure Investment and Jobs Act are encouraging investment in clean energy technologies, including solar, wind, and energy storage.

Focus on Lightweighting in Automotive Manufacturing

As automakers face stringent fuel efficiency standards and the shift toward electric vehicles (EVs), they are focusing on reducing vehicle weight without compromising strength, safety, or performance. Molybdenum’s ability to improve the strength of steel while reducing its weight makes it a key material in this transition. The 2025 CAFE standards require automakers to achieve a fleet-wide fuel efficiency of 54.5 miles per gallon. Lightweighting through advanced high-strength steel (AHSS), which incorporates molybdenum, can reduce a vehicle’s weight by up to 25%, resulting in an 8%–10% improvement in fuel efficiency.

The shift toward electric vehicles (EVs) is further intensifying the focus on lightweight materials. EVs require lighter components to offset the weight of heavy battery packs, enabling longer driving ranges and better energy efficiency. Molybdenum alloys and AHSS are playing a key role in this transition by helping automakers reduce the overall weight of EVs while maintaining structural integrity and safety.

Molybdenum is a key alloying element in AHSS (Advanced High-Strength Steels), which is used in critical automotive components such as frames, chassis, and body structures. AHSS provides high strength-to-weight ratios, enabling manufacturers to reduce the weight of vehicles while maintaining crashworthiness and durability.

With increasing pressure to improve fuel efficiency, reduce emissions, and enhance the performance of electric vehicles, automakers are relying on advanced materials like molybdenum-enhanced steels.

Domestic Production and Supply Chain Stability

The United States is one of the world’s leading producers of molybdenum, and this strong domestic output helps to ensure a stable supply for various industries, including aerospace, energy, automotive, and construction. Key U.S. mining operations, such as those in Colorado, Utah, and Arizona, provide a consistent stream of molybdenum, which is crucial for supporting manufacturing and technological advancements.

According to the U.S. Geological Survey (USGS), the United States was the second-largest producer of molybdenum in 2022, with an output of 49,000 metric tons. This represented approximately 15% of global molybdenum production, second only to China. The majority of U.S. molybdenum production comes as a by-product from large copper mining operations, notably the Climax and Henderson mines in Colorado, as well as mines in Arizona and Utah. These significant domestic resources ensure that the U.S. has a reliable supply of molybdenum to meet internal demand, reducing reliance on imports.

Domestic production of molybdenum ensures a high degree of supply chain stability, protecting U.S. industries from disruptions in global markets. With most of the molybdenum consumed domestically coming from U.S. mines, industries such as aerospace, automotive, and energy are less vulnerable to geopolitical risks, trade disputes, or supply chain bottlenecks that can impact international sourcing.

While the U.S. primarily relies on domestic production to meet its molybdenum needs, imports also play a role in ensuring a steady supply, especially for specialized products. In 2022, the U.S. imported approximately 9,700 metric tons of molybdenum, mainly in the form of molybdenum oxide and ferromolybdenum, with the bulk of these imports coming from countries like Chile, Canada, and Mexico.

Molybdenum is classified as a critical mineral in the U.S. due to its essential role in high-tech industries, including defense, energy, and infrastructure. Government policies aimed at strengthening the domestic mining sector and reducing dependence on foreign materials have reinforced the stability of the molybdenum supply chain.

Molybdenum Market Share and Leaders

The Molybdenum market is characterized by a competitive landscape with companies focusing technological advancements, strategic expansions, and localized product offerings to boost market shares. Key companies included in the report are- American CuMo Mining Corp – U.S., Freeport-McMoRan Inc, Rio Tinto Group, Centerra Gold Inc, Anglo American plc, Antofagasta plc, Compañía Minera Antamina S.A

Report Scope

|

Parameter

|

Details

|

|

Market Size (2025)

|

$914.7 Million

|

|

Market Size (2034)

|

$1.4 Billion

|

|

Market Growth Rate

|

4.97%

|

|

Largest Segment- Product

|

Engineering Steel (38.3% Market Share)

|

|

Largest End-User Industry

|

Energy and Power (21.3% Revenue Share)

|

|

Segments

|

Applications, End-User Industry

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

American CuMo Mining Corp – U.S., Freeport-McMoRan Inc, Rio Tinto Group, Centerra Gold Inc, Anglo American plc, Antofagasta plc, Compañía Minera Antamina S.A

|

|

States

|

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, North Carolina, Others

|

United States Molybdenum Market Segmentation

By Product

- Steel

- Chemical

- Foundry

- MO-Metal

- Nickel Alloy

- Others

By End-User

- Oil and Gas

- Energy and Power

- Chemical and Petrochemical

- Automotive

- Industrial Usage

- Building and Construction

- Aerospace and Defense

- Others

United States Molybdenum Market Companies Profiled in the Study:

- American CuMo Mining Corp – U.S.

- Freeport-McMoRan Inc

- Rio Tinto Group

- Centerra Gold Inc

- Anglo American plc

- Antofagasta plc

- Compañía Minera Antamina S.A

1. Executive Summary

US Molybdenum Market Introduction- 2024

Report Scope

Methodology

Market Size Outlook, USD Million, 2021- 2032

2. US Molybdenum Market Entropy

Competitive Landscape

US Market Share by Company, 2023

Recent Market Developments

Regulatory Scenario

3. US Molybdenum Market Dynamics

Market Ecosystem- Industry Stakeholders

Porter’s Five Forces Analysis

SWOT Profile

US Industry Trends and Drivers

US Industry Challenges

Inflation, Macroeconomics and Demographics Forecast

4. US Molybdenum Scenario Analysis

Low Growth

Reference Case

High Growth

5. US Molybdenum Market Outlook by Type

Engineering Steel

Stainless Steel

Tools Steel

Foundries

Alloys

Others

7. US Molybdenum Market Outlook by Application

Chemicals and Petrochemicals

Energy and Power

Mechanical Engineering

Automotive and Transportation

Building and Construction

Aerospace and Defense

Others

8. US Molybdenum Market by State

California

Texas

New York

Florida

Illinois

Pennsylvania

Ohio

Georgia

New Jersey

North Carolina

Others

9. Company Profiles of Leading US Molybdenum Companies

American CuMo Mining Corp

Freeport-McMoRan Inc

Rio Tinto Group

Centerra Gold Inc

Anglo American plc

Antofagasta plc

Compañía Minera Antamina S.A

10. Appendix

Data Sources

Methodology and Research Approach

Conclusion