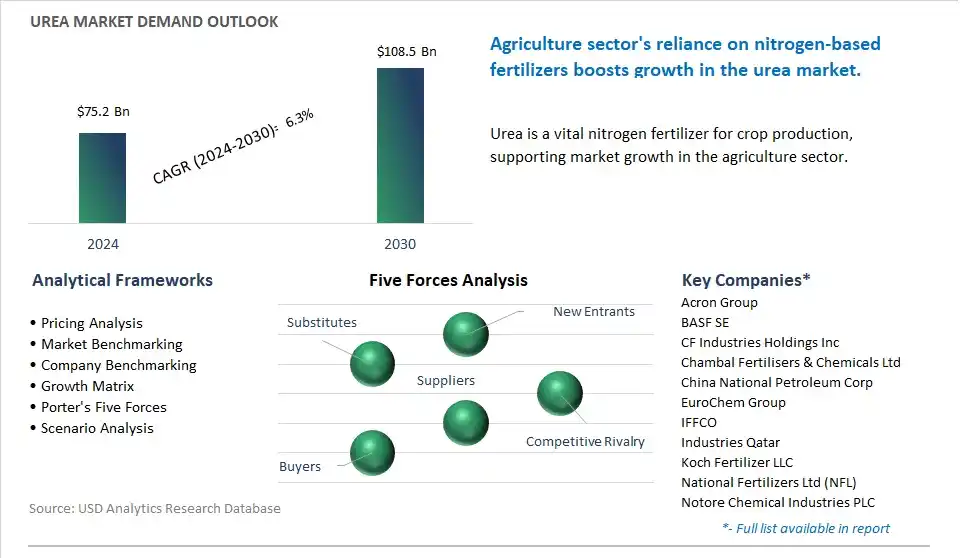

The global Urea Market is poised to register a 6.3% CAGR from $75.2 Billion in 2024 to $108.5 Billion in 2030.

The global Urea Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Grade (Fertilizer, Feed, Technical), By End-User (Agriculture, Chemical, Automotive, Medical, Others).

An Introduction to Global Urea Market in 2024

The urea market is experiencing transformative shifts driven by agricultural demands, environmental concerns, and technological advancements. Key trends shaping the future of the industry include the increasing adoption of urea as a nitrogen fertilizer due to its high nitrogen content and cost-effectiveness, particularly in large-scale agricultural operations. Moreover, there's a growing emphasis on sustainable agriculture practices and nutrient management, leading to innovations in urea formulations, application methods, and controlled-release technologies to reduce nutrient runoff and environmental impact. Additionally, advancements in urea production processes, such as carbon capture and utilization, are driving innovation and market differentiation, enabling manufacturers to offer environmentally friendly urea products while meeting regulatory standards and customer needs. However, challenges such as price volatility, market competitiveness, and fluctuating demand patterns also influence the urea market's trajectory, necessitating strategic planning and adaptation to ensure growth and sustainability in the global urea industry.

Urea Market Competitive Landscape

The market report analyses the leading companies in the industry including Acron Group, BASF SE, CF Industries Holdings Inc, Chambal Fertilisers & Chemicals Ltd, China National Petroleum Corp, EuroChem Group, IFFCO, Industries Qatar, Koch Fertilizer LLC, National Fertilizers Ltd (NFL), Notore Chemical Industries PLC, Nutrien Ltd, OCI N.V., Paradeep Phosphates Ltd, Petróleo Brasileiro S.A. (Petrobras), PT Pupuk Kalimantan Timur, Saudi Basic Industries Corp (SABIC), The Chemical Company (TCC), URALCHEM Joint Stock Company (JSC), Yara International ASA.

Urea Market Dynamics

Urea Market Trend: Increasing Demand for Agricultural Fertilizers to Enhance Crop Yields

The most prominent market trend for urea is the increasing demand for agricultural fertilizers to enhance crop yields. As global population continues to grow, there is a rising need to increase food production to feed the expanding population. Urea, a nitrogen-based fertilizer, is widely used in agriculture to provide essential nutrients to crops, promote healthy plant growth, and improve crop yields. This trend is driven by the growing demand for food security, changing dietary preferences, and expansion of agricultural land to meet the needs of a growing population. As a result, the demand for urea is expected to continue rising, particularly in developing regions where agriculture plays a significant role in the economy.

Urea Market Driver: Growth in Population and Changing Dietary Patterns

A key market driver for urea is the growth in population and changing dietary patterns worldwide. With the global population projected to reach nearly 10 billion by 2050, there is increasing pressure on agricultural systems to produce more food to feed the growing populace. Additionally, changing dietary preferences, particularly in emerging economies, are driving demand for protein-rich foods such as meat and dairy products, which require higher agricultural inputs to produce. Urea, as a primary nitrogen fertilizer, plays a crucial role in meeting the nutrient requirements of crops and sustaining agricultural productivity to support the growing demand for food. The combination of population growth, urbanization, and dietary shifts fuels the demand for urea in agriculture, making it a vital component in global food production systems.

Urea Market Opportunity: Development of Enhanced Urea Formulations and Application Technologies

An exciting opportunity in the urea market lies in the development of enhanced urea formulations and application technologies. While urea is a widely used fertilizer, there are opportunities to improve its efficiency, reduce nitrogen losses, and minimize environmental impact through innovation. Manufacturers can explore the development of controlled-release urea formulations that release nitrogen gradually over time, reducing the risk of nutrient leaching and volatilization. Additionally, advancements in precision agriculture and nutrient management technologies offer opportunities to optimize urea application rates, timing, and placement to maximize crop uptake and minimize waste. By investing in research and development of advanced urea products and application methods, companies can address sustainability concerns, enhance fertilizer efficiency, and meet the evolving needs of farmers for high-performance agricultural inputs. This opportunity allows urea manufacturers to differentiate their products, capture market share, and contribute to sustainable agriculture practices for long-term food security and environmental stewardship.

Urea Market Share Analysis: Fertilizer Grade segment generated the highest revenue in the industry

The Fertilizer Grade segment is the largest segment in the Urea Market due to diverse significant factors. The urea is primarily known and widely utilized as a nitrogen-rich fertilizer in agriculture. Nitrogen is an essential nutrient for plant growth, and urea, with its high nitrogen content (around 46%), serves as an efficient and cost-effective source of nitrogen for crops. As global agricultural practices evolve to meet the increasing demand for food production driven by population growth and changing dietary preferences, the demand for urea as a fertilizer remains robust. Additionally, urea's versatility and compatibility with various crops, soil types, and application methods further contribute to its widespread use in agriculture. In addition, government subsidies and support programs for fertilizers in many countries incentivize farmers to use urea, further bolstering its dominance in the fertilizer grade segment of the Urea Market. Over the forecast period, the Fertilizer Grade segment retains its position as the largest segment in the Urea Market due to the crucial role of urea in modern agriculture and its widespread adoption as a key fertilizer ingredient worldwide.

Urea Market Share Analysis: Agriculture Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Agriculture segment is the fastest-growing segment in the Urea Market due to diverse compelling reasons. The agriculture remains the primary end-user of urea, accounting for the largest share of urea consumption globally. As the world population continues to grow, so does the demand for food, driving the need for increased agricultural productivity. Urea, with its high nitrogen content, plays a crucial role in promoting plant growth and enhancing crop yields. In addition, as agricultural practices evolve towards more intensive and efficient methods to meet growing food demand, the use of urea-based fertilizers becomes increasingly essential. Additionally, the adoption of precision agriculture techniques, coupled with the rising trend of sustainable farming practices, further boosts the demand for urea in agriculture. Further, government initiatives and subsidies aimed at promoting agricultural productivity and ensuring food security contribute to the growth of the Agriculture segment in the Urea Market.

Urea Market Report Segmentation

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Urea Companies Profiled in the Market Study

Acron Group

BASF SE

CF Industries Holdings Inc

Chambal Fertilisers & Chemicals Ltd

China National Petroleum Corp

EuroChem Group

IFFCO

Industries Qatar

Koch Fertilizer LLC

National Fertilizers Ltd (NFL)

Notore Chemical Industries PLC

Nutrien Ltd

OCI N.V.

Paradeep Phosphates Ltd

Petróleo Brasileiro S.A. (Petrobras)

PT Pupuk Kalimantan Timur

Saudi Basic Industries Corp (SABIC)

The Chemical Company (TCC)

URALCHEM Joint Stock Company (JSC)

Yara International ASA

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Urea Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Urea Market Size Outlook, $ Million, 2021 to 2030

3.2 Urea Market Outlook by Type, $ Million, 2021 to 2030

3.3 Urea Market Outlook by Product, $ Million, 2021 to 2030

3.4 Urea Market Outlook by Application, $ Million, 2021 to 2030

3.5 Urea Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Urea Industry

4.2 Key Market Trends in Urea Industry

4.3 Potential Opportunities in Urea Industry

4.4 Key Challenges in Urea Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Urea Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Urea Market Outlook by Segments

7.1 Urea Market Outlook by Segments, $ Million, 2021- 2030

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

8 North America Urea Market Analysis and Outlook To 2030

8.1 Introduction to North America Urea Markets in 2024

8.2 North America Urea Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Urea Market size Outlook by Segments, 2021-2030

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

9 Europe Urea Market Analysis and Outlook To 2030

9.1 Introduction to Europe Urea Markets in 2024

9.2 Europe Urea Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Urea Market Size Outlook by Segments, 2021-2030

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

10 Asia Pacific Urea Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Urea Markets in 2024

10.2 Asia Pacific Urea Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Urea Market size Outlook by Segments, 2021-2030

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

11 South America Urea Market Analysis and Outlook To 2030

11.1 Introduction to South America Urea Markets in 2024

11.2 South America Urea Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Urea Market size Outlook by Segments, 2021-2030

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

12 Middle East and Africa Urea Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Urea Markets in 2024

12.2 Middle East and Africa Urea Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Urea Market size Outlook by Segments, 2021-2030

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Acron Group

BASF SE

CF Industries Holdings Inc

Chambal Fertilisers & Chemicals Ltd

China National Petroleum Corp

EuroChem Group

IFFCO

Industries Qatar

Koch Fertilizer LLC

National Fertilizers Ltd (NFL)

Notore Chemical Industries PLC

Nutrien Ltd

OCI N.V.

Paradeep Phosphates Ltd

Petróleo Brasileiro S.A. (Petrobras)

PT Pupuk Kalimantan Timur

Saudi Basic Industries Corp (SABIC)

The Chemical Company (TCC)

URALCHEM Joint Stock Company (JSC)

Yara International ASA

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Grade

Fertilizer

Feed

Technical

By End-User

Agriculture

Chemical

Automotive

Medical

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)