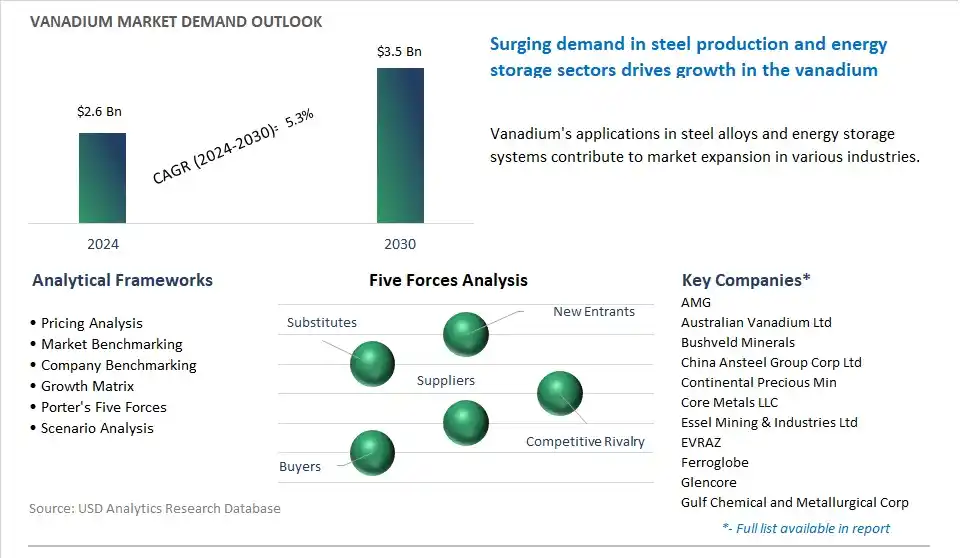

The global Vanadium Market is poised to register a 5.3% CAGR from $2.6 Billion in 2024 to $3.5 Billion in 2030.

The global Vanadium Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Grade (FeV40, FeV50, FeV60, FeV80), By Production Process (Aluminothermic Reduction Technique, Silicon Reduction Technique), By Application (Iron and Steel, Chemical, Titanium Alloys, Others), By End-User (Automotive Chemical, Energy Storage, Others).

An Introduction to Global Vanadium Market in 2024

The vanadium market is experiencing notable shifts driven by factors such as energy storage, steel production, and industrial applications. Key trends shaping the future of the industry include the increasing demand for vanadium in energy storage systems, particularly vanadium redox flow batteries (VRFBs), due to their high energy density, long cycle life, and grid stabilization capabilities. Moreover, there's a growing emphasis on vanadium as a steel additive for strengthening and alloying applications, driven by infrastructure development, urbanization, and automotive manufacturing. Additionally, advancements in vanadium extraction, processing, and recycling technologies are driving innovation and market competitiveness, enabling cost-effective and sustainable vanadium production. However, challenges such as price volatility, supply chain disruptions, and regulatory uncertainties also influence the vanadium market's trajectory, requiring strategic planning and risk management to ensure long-term growth and sustainability in the global vanadium industry.

Vanadium Market Competitive Landscape

The market report analyses the leading companies in the industry including AMG, Australian Vanadium Ltd, Bushveld Minerals, China Ansteel Group Corp Ltd, Continental Precious Min, Core Metals LLC, Essel Mining & Industries Ltd, EVRAZ, Ferroglobe, Glencore, Gulf Chemical and Metallurgical Corp, HBIS GROUP, JAYESH, Largo Inc, Treibacher Industrie AG, Tremond Metals Corp, VanadiumCorp Resource Inc, Williams, Yilmaden.

Vanadium Market Dynamics

Vanadium Market Trend: Increasing Demand for Vanadium Redox Flow Batteries (VRFBs) in Energy Storage

The most prominent market trend for vanadium is the increasing demand for Vanadium Redox Flow Batteries (VRFBs) in energy storage applications. As renewable energy sources like solar and wind become more prevalent, the need for efficient energy storage solutions to manage intermittent power generation and stabilize the grid grows. VRFBs, which utilize vanadium electrolyte solutions, offer scalable and long-duration energy storage capabilities, making them ideal for grid-level energy storage, backup power systems, and remote/off-grid applications. This trend is driven by the expanding renewable energy market, grid modernization initiatives, and the need for reliable energy storage solutions to support the transition to a low-carbon energy future.

Vanadium Market Driver: Growing Demand from the Steel and Alloy Industries

A key market driver for vanadium is the growing demand from the steel and alloy industries. Vanadium is primarily used as an alloying element in the production of high-strength, low-alloy steels (HSLA) and specialty alloys. These alloys are utilized in a wide range of applications such as structural components in buildings and bridges, automotive parts, pipelines, and aerospace components. The increasing demand for lightweight, durable materials with superior mechanical properties drives the need for vanadium-containing alloys, particularly in industries where strength-to-weight ratio, corrosion resistance, and fatigue performance are critical. The growth of infrastructure development, urbanization, and automotive manufacturing in emerging economies further fuels the demand for vanadium as an essential alloying element, positioning it as a key driver of the global vanadium market.

Vanadium Market Opportunity: Expansion into Vanadium-based Energy Storage and Electrochemical Applications

An exciting opportunity in the vanadium market lies in the expansion into vanadium-based energy storage and electrochemical applications beyond VRFBs. While VRFBs represent a significant growth opportunity, there is potential to leverage vanadium's unique properties in other electrochemical systems such as redox flow batteries (RFBs), supercapacitors, and electrolyzers for hydrogen production. Vanadium's reversible redox reactions, high energy density, and long cycle life make it an attractive material for energy storage and conversion devices. By investing in research and development, innovation, and commercialization efforts, vanadium producers and technology developers can unlock new applications and markets for vanadium-based electrochemical technologies. Additionally, partnerships, collaborations, and strategic investments in emerging energy storage markets and applications offer opportunities for vanadium companies to diversify their revenue streams, capture market share, and contribute to the advancement of sustainable energy solutions. This opportunity allows vanadium stakeholders to capitalize on the growing demand for energy storage technologies and position vanadium as a key enabler of the global energy transition towards a more resilient and sustainable energy infrastructure.

Vanadium Market Share Analysis: FeV80 segment generated the highest revenue in the industry

The largest segment in the Vanadium Market is FeV80. This dominance can be attributed to diverse factors. The FeV80, or ferrovanadium with 80% vanadium content, is considered the highest grade among the options listed. It offers superior quality and purity compared to lower-grade ferrovanadium alloys such as FeV40, FeV50, and FeV60. FeV80 is widely used in the production of high-strength steel alloys, where vanadium acts as a crucial alloying element to improve the strength, hardness, and durability of steel. Industries such as construction, automotive, and aerospace rely heavily on high-strength steel alloys for various applications, driving significant demand for FeV80. Additionally, FeV80's higher vanadium content makes it more effective in achieving desired alloying effects, such as grain refinement and precipitation strengthening, leading to improved mechanical properties in steel products. In addition, FeV80's superior performance and versatility make it a preferred choice for manufacturers seeking to optimize the quality and performance of their steel products, further cementing its position as the largest segment in the vanadium market.

Vanadium Market Share Analysis: Aluminothermic Reduction Technique Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Vanadium Market is the Aluminothermic Reduction Technique. The rapid growth is driven by the aluminothermic reduction technique offers diverse advantages over the traditional silicon reduction technique. Aluminothermic reduction allows for the production of high-purity vanadium with minimal impurities, resulting in superior quality vanadium products that command premium prices in the market. Additionally, the aluminothermic process is more environmentally friendly compared to silicon reduction, as it produces fewer greenhouse gas emissions and requires less energy consumption. Further, advancements in aluminothermic reduction technology have led to increased efficiency and scalability, enabling manufacturers to meet growing demand for vanadium in various industries such as steel production, energy storage, and chemical manufacturing. As a result of these factors, the aluminothermic reduction technique is experiencing rapid adoption and is poised to become the fastest-growing segment in the vanadium market.

Vanadium Market Share Analysis: Titanium Alloys Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Vanadium Market is the Titanium Alloys segment. This growth is primarily driven by the increasing demand for titanium alloys in various industries, particularly aerospace, automotive, and medical devices. Vanadium is a key alloying element in titanium alloys, where it improves the strength, corrosion resistance, and heat resistance of the final product. With the aerospace industry expanding rapidly and demanding lighter yet stronger materials for aircraft manufacturing, the use of titanium alloys containing vanadium is on the rise. Additionally, titanium alloys are gaining popularity in the automotive sector for their ability to reduce vehicle weight while maintaining structural integrity and fuel efficiency. Further, advancements in medical implant technologies require biocompatible materials with high strength and corrosion resistance, further driving the demand for vanadium-containing titanium alloys in the healthcare sector. As a result, the Titanium Alloys segment is experiencing significant growth in the vanadium market due to its widespread applications and the unique properties offered by vanadium in enhancing the performance of titanium alloys.

Vanadium Market Report Segmentation

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Vanadium Companies Profiled in the Market Study

AMG

Australian Vanadium Ltd

Bushveld Minerals

China Ansteel Group Corp Ltd

Continental Precious Min

Core Metals LLC

Essel Mining & Industries Ltd

EVRAZ

Ferroglobe

Glencore

Gulf Chemical and Metallurgical Corp

HBIS GROUP

JAYESH

Largo Inc

Treibacher Industrie AG

Tremond Metals Corp

VanadiumCorp Resource Inc

Williams

Yilmaden

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Vanadium Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Vanadium Market Size Outlook, $ Million, 2021 to 2030

3.2 Vanadium Market Outlook by Type, $ Million, 2021 to 2030

3.3 Vanadium Market Outlook by Product, $ Million, 2021 to 2030

3.4 Vanadium Market Outlook by Application, $ Million, 2021 to 2030

3.5 Vanadium Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Vanadium Industry

4.2 Key Market Trends in Vanadium Industry

4.3 Potential Opportunities in Vanadium Industry

4.4 Key Challenges in Vanadium Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Vanadium Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Vanadium Market Outlook by Segments

7.1 Vanadium Market Outlook by Segments, $ Million, 2021- 2030

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

8 North America Vanadium Market Analysis and Outlook To 2030

8.1 Introduction to North America Vanadium Markets in 2024

8.2 North America Vanadium Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Vanadium Market size Outlook by Segments, 2021-2030

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

9 Europe Vanadium Market Analysis and Outlook To 2030

9.1 Introduction to Europe Vanadium Markets in 2024

9.2 Europe Vanadium Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Vanadium Market Size Outlook by Segments, 2021-2030

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

10 Asia Pacific Vanadium Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Vanadium Markets in 2024

10.2 Asia Pacific Vanadium Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Vanadium Market size Outlook by Segments, 2021-2030

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

11 South America Vanadium Market Analysis and Outlook To 2030

11.1 Introduction to South America Vanadium Markets in 2024

11.2 South America Vanadium Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Vanadium Market size Outlook by Segments, 2021-2030

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

12 Middle East and Africa Vanadium Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Vanadium Markets in 2024

12.2 Middle East and Africa Vanadium Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Vanadium Market size Outlook by Segments, 2021-2030

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AMG

Australian Vanadium Ltd

Bushveld Minerals

China Ansteel Group Corp Ltd

Continental Precious Min

Core Metals LLC

Essel Mining & Industries Ltd

EVRAZ

Ferroglobe

Glencore

Gulf Chemical and Metallurgical Corp

HBIS GROUP

JAYESH

Largo Inc

Treibacher Industrie AG

Tremond Metals Corp

VanadiumCorp Resource Inc

Williams

Yilmaden

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Grade

FeV40

FeV50

FeV60

FeV80

By Production Process

Aluminothermic Reduction Technique

Silicon Reduction Technique

By Application

Iron and Steel

Chemical

Titanium Alloys

Others

By End-User

Automotive Chemical

Energy Storage

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)