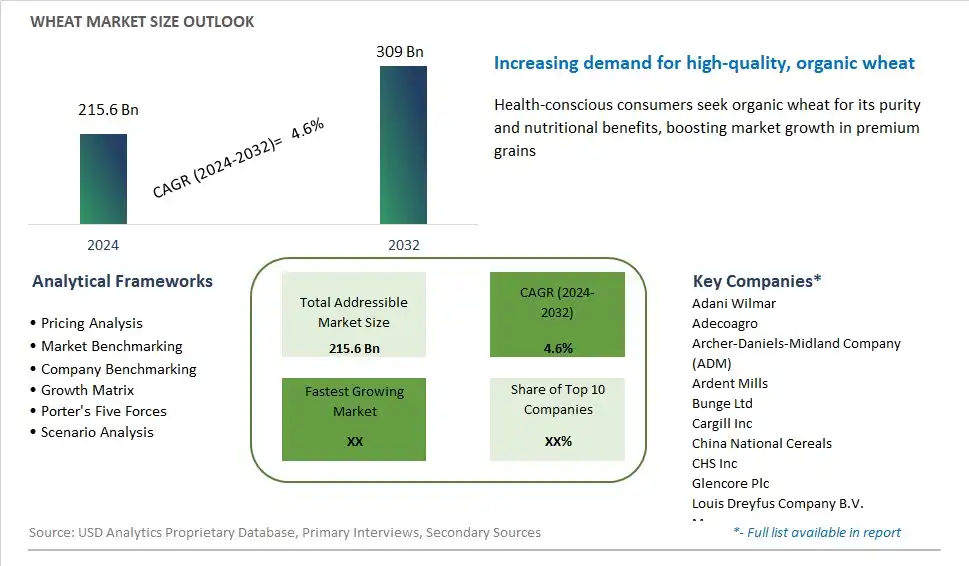

Global Wheat Market Size is valued at $215.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 4.6% to reach $309 Billion by 2032.

The global Wheat Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Nature (Organic, Conventional), By End-User (B2B, B2C)

An Introduction to Wheat Market

Wheat remains a staple crop and essential ingredient in global food systems in 2024, playing a critical role in providing sustenance and nutrition to billions of people worldwide. As one of the most widely cultivated grains, wheat is versatile in its applications, used to produce a diverse range of foods such as bread, pasta, noodles, cereals, and baked goods. With advancements in agricultural practices, breeding techniques, and processing technologies, wheat production continues to increase to meet the growing demand for food, feed, and industrial uses. From traditional wheat varieties to modern hybrids and genetically modified strains, wheat cultivars are continuously being developed to improve yield, resistance to pests and diseases, and nutritional quality. As consumer preferences evolve, there is a growing interest in heritage and ancient wheat varieties, as well as gluten-free alternatives for individuals with celiac disease or gluten sensitivities. Despite challenges such as climate change and resource constraints, wheat remains a cornerstone of global food security and economic development, providing sustenance and livelihoods to millions of farmers and communities around the world.

Wheat Competitive Landscape

The market report analyses the leading companies in the industry including Adani Wilmar, Adecoagro, Archer-Daniels-Midland Company (ADM), Ardent Mills, Bunge Ltd, Cargill Inc, China National Cereals, CHS Inc, Glencore Plc, Louis Dreyfus Company B.V., Munsa, Nisshin Seifun Group Inc, Oils and Foodstuffs Corp (COFCO), SENSAKO, The Scoular Company, The Soufflet Group, and Others.

Wheat Market Dynamics

Wheat Market Trend: Growing Demand for Healthy and Alternative Wheat Products

A significant trend in the wheat market is the increasing demand for healthy and alternative wheat products. As consumers become more health-conscious and seek to diversify their diets, there's a rising interest in wheat-based products that offer nutritional benefits beyond traditional refined flour. This trend is driven by concerns about the health implications of refined carbohydrates and gluten sensitivity, as well as a desire for variety and innovation in food choices. Alternative wheat products, such as whole wheat flour, spelt flour, and ancient grain varieties like einkorn and emmer, are gaining popularity for their higher fiber content, enhanced nutritional profiles, and potential health benefits. Additionally, there's growing interest in wheat alternatives such as gluten-free flours made from grains like rice, quinoa, and buckwheat, catering to consumers with gluten intolerance or celiac disease. Manufacturers are responding to this trend by expanding their product lines to include a variety of alternative wheat products, tapping into the growing market for healthier and more diverse wheat options.

Market Driver: Global Population Growth and Increasing Food Consumption

A significant driver propelling the wheat market is the global population growth and increasing food consumption. Wheat is one of the world's most widely cultivated and consumed cereal grains, serving as a staple food for billions of people worldwide. With the global population projected to reach over 9 billion by 2050, there's a growing demand for wheat to meet the dietary needs of a growing population. Additionally, rising incomes and urbanization in developing countries are driving changes in dietary preferences and food consumption patterns, leading to increased demand for wheat-based products such as bread, pasta, noodles, and baked goods. Furthermore, wheat is used as a feed grain for livestock production, further contributing to its demand. The combination of population growth, urbanization, and changing dietary habits is driving sustained demand for wheat across various sectors, making it a key driver of market growth and stability.

Market Opportunity: Innovation in Wheat-Based Functional Foods and Ingredients

An opportunity within the wheat market lies in innovation in wheat-based functional foods and ingredients to meet evolving consumer preferences and address emerging health concerns. While wheat is traditionally used in a wide range of staple foods and baked goods, there's room for innovation in product development to create value-added wheat-based products that offer additional health benefits and functionality. Manufacturers can capitalize on this opportunity by developing functional foods fortified with wheat-derived ingredients such as wheat germ, wheat bran, and wheat protein isolates, which offer enhanced nutritional profiles and potential health-promoting properties. Additionally, there's potential for the development of wheat-based ingredients for use in plant-based meat alternatives, dairy substitutes, and gluten-free products, catering to consumers' growing interest in alternative protein sources and dietary restrictions. By investing in research and development and leveraging the versatility and nutritional benefits of wheat, manufacturers can unlock new opportunities for market expansion and differentiation in the dynamic and competitive food industry landscape.

Wheat Market Share Analysis: Conventional held the dominant market share in 2024

In the Wheat Market, the Conventional segment dominates as the largest segment due to several factors. Conventional wheat production typically involves higher yields and lower production costs compared to organic methods, making conventional wheat more economically viable for both farmers and consumers. Additionally, conventional wheat often benefits from established supply chains and distribution networks, allowing it to reach a wider consumer base through mainstream retail channels. While organic wheat appeals to consumers seeking products grown without synthetic pesticides or fertilizers, the higher price point and limited availability often restrict its market share compared to conventional wheat. As a result, the Conventional segment maintains its dominance in the Wheat Market, meeting the bulk of global wheat demand for food, feed, and industrial applications.

Wheat Market Share Analysis: B2C, Online Channels market is poised to register the fastest growth rae over the forecast period to 2032

In the Wheat Market, the Business-to-Consumer (B2C) segment, particularly through online channels, is the fastest-growing category, driven by the increasing adoption of e-commerce platforms and changing consumer shopping habits. Online retail channels offer convenience, accessibility, and a wide variety of wheat-based products to consumers, facilitating easy comparison and purchase from the comfort of their homes. Further, the COVID-19 pandemic accelerated the shift towards online shopping as consumers sought safer alternatives to traditional brick-and-mortar stores. Additionally, the growing trend of health-conscious and environmentally aware consumers drives the demand for organic and specialty wheat products, which are often more readily available through online platforms. As a result, the B2C segment, especially through online channels, experiences exponential growth in the Wheat Market, reshaping the industry landscape and presenting significant opportunities for manufacturers and retailers alike.

Wheat Market Segmentation

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Wheat Companies Profiled in the Study

Adani Wilmar

Adecoagro

Archer-Daniels-Midland Company (ADM)

Ardent Mills

Bunge Ltd

Cargill Inc

China National Cereals

CHS Inc

Glencore Plc

Louis Dreyfus Company B.V.

Munsa

Nisshin Seifun Group Inc

Oils and Foodstuffs Corp (COFCO)

SENSAKO

The Scoular Company

The Soufflet Group

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Wheat Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Wheat Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Wheat Market Share by Company, 2023

4.1.2. Product Offerings of Leading Wheat Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Wheat Market Drivers

6.2. Wheat Market Challenges

6.6. Wheat Market Opportunities

6.4. Wheat Market Trends

Chapter 7. Global Wheat Market Outlook Trends

7.1. Global Wheat Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Wheat Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Wheat Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Chapter 8. Global Wheat Regional Analysis and Outlook

8.1. Global Wheat Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Wheat Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Wheat Regional Analysis and Outlook

8.2.2. Canada Wheat Regional Analysis and Outlook

8.2.3. Mexico Wheat Regional Analysis and Outlook

8.3. Europe Wheat Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Wheat Regional Analysis and Outlook

8.3.2. France Wheat Regional Analysis and Outlook

8.3.3. United Kingdom Wheat Regional Analysis and Outlook

8.3.4. Spain Wheat Regional Analysis and Outlook

8.3.5. Italy Wheat Regional Analysis and Outlook

8.3.6. Russia Wheat Regional Analysis and Outlook

8.3.7. Rest of Europe Wheat Regional Analysis and Outlook

8.4. Asia Pacific Wheat Revenue (USD Million) by Country (2021-2032)

8.4.1. China Wheat Regional Analysis and Outlook

8.4.2. Japan Wheat Regional Analysis and Outlook

8.4.3. India Wheat Regional Analysis and Outlook

8.4.4. South Korea Wheat Regional Analysis and Outlook

8.4.5. Australia Wheat Regional Analysis and Outlook

8.4.6. South East Asia Wheat Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Wheat Regional Analysis and Outlook

8.5. South America Wheat Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Wheat Regional Analysis and Outlook

8.5.2. Argentina Wheat Regional Analysis and Outlook

8.5.3. Rest of South America Wheat Regional Analysis and Outlook

8.6. Middle East and Africa Wheat Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Wheat Regional Analysis and Outlook

8.6.2. Africa Wheat Regional Analysis and Outlook

Chapter 9. North America Wheat Analysis and Outlook

9.1. North America Wheat Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Wheat Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Wheat Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Wheat Revenue (USD Million) by Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Chapter 10. Europe Wheat Analysis and Outlook

10.1. Europe Wheat Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Wheat Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Wheat Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Wheat Revenue (USD Million) by Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Chapter 11. Asia Pacific Wheat Analysis and Outlook

11.1. Asia Pacific Wheat Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Wheat Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Wheat Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Wheat Revenue (USD Million) by Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Chapter 12. South America Wheat Analysis and Outlook

12.1. South America Wheat Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Wheat Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Wheat Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Wheat Revenue (USD Million) by Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Chapter 13. Middle East and Africa Wheat Analysis and Outlook

13.1. Middle East and Africa Wheat Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Wheat Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Wheat Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Wheat Revenue (USD Million) by Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Chapter 14. Wheat Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Adani Wilmar

Adecoagro

Archer-Daniels-Midland Company (ADM)

Ardent Mills

Bunge Ltd

Cargill Inc

China National Cereals

CHS Inc

Glencore Plc

Louis Dreyfus Company B.V.

Munsa

Nisshin Seifun Group Inc

Oils and Foodstuffs Corp (COFCO)

SENSAKO

The Scoular Company

The Soufflet Group

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Wheat Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Wheat Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Wheat Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Wheat Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Wheat Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Wheat Market Share (%) By Regions (2021-2032)

Table 12 North America Wheat Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Wheat Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Wheat Revenue (USD Million) By Country (2021-2032)

Table 15 South America Wheat Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Wheat Revenue (USD Million) By Region (2021-2032)

Table 17 North America Wheat Revenue (USD Million) By Type (2021-2032)

Table 18 North America Wheat Revenue (USD Million) By Application (2021-2032)

Table 19 North America Wheat Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Wheat Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Wheat Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Wheat Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Wheat Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Wheat Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Wheat Revenue (USD Million) By Product (2021-2032)

Table 26 South America Wheat Revenue (USD Million) By Type (2021-2032)

Table 27 South America Wheat Revenue (USD Million) By Application (2021-2032)

Table 28 South America Wheat Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Wheat Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Wheat Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Wheat Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Wheat Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Wheat Market Share (%) By Regions (2023)

Figure 6. North America Wheat Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Wheat Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Wheat Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Wheat Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Wheat Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Wheat Revenue (USD Million) By Country (2021-2032)

Figure 12. France Wheat Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Wheat Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Wheat Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Wheat Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Wheat Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Wheat Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Wheat Revenue (USD Million) By Country (2021-2032)

Figure 12. China Wheat Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Wheat Revenue (USD Million) By Country (2021-2032)

Figure 14. India Wheat Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Wheat Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Wheat Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Wheat Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Wheat Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Wheat Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Wheat Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Wheat Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Wheat Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Wheat Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Wheat Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Wheat Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Wheat Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Wheat Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Wheat Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Wheat Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Wheat Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Wheat Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Wheat Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Wheat Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Wheat Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Wheat Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Wheat Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Wheat Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Wheat Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Wheat Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Wheat Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Wheat Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Wheat Revenue (USD Million) By Product (2021-2032)

By Nature

Organic

Conventional

By End-User

B2B

-Food & Beverages

-Animal Feed

-Industrial Use

-Others

B2C

-Online

-Offline

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)