The global Wind Turbine Composites Material Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Resin (Epoxy, Polyester, Vinyl Ester), By Fiber (Glass Fiber, Carbon Fiber), By Manufacturing Process (Vacuum Injection Molding, Prepreg, Hand Lay-up), By Application (Blades, Nacelles, Others).

Wind turbine composites materials play a crucial role in the construction of wind turbine blades, towers, nacelles, and other components, enabling the efficient capture and conversion of wind energy into electricity in 2024. These materials are engineered to provide high strength-to-weight ratio, fatigue resistance, durability, and corrosion resistance, essential for withstanding the harsh environmental conditions and mechanical stresses experienced by wind turbines. Wind turbine composites typically consist of fiberglass reinforced polymers (FRP), carbon fiber reinforced polymers (CFRP), epoxy resins, and core materials such as foam or balsa wood, tailored to meet the specific performance requirements of different turbine components. In wind turbine blades, composites materials offer lightweight construction, aerodynamic efficiency, and structural integrity, allowing for longer and more efficient blades that capture more wind energy. Similarly, in turbine towers and nacelles, composites materials provide strength, stiffness, and durability while reducing weight and manufacturing costs compared to traditional materials such as steel or concrete. With the d growth of wind energy as a clean and renewable power source, wind turbine manufacturers are investing in research and development of advanced composites materials and manufacturing processes to optimize turbine performance, increase reliability, and reduce the levelized cost of energy (LCOE), driving innovation and progress in the wind energy industry worldwide.

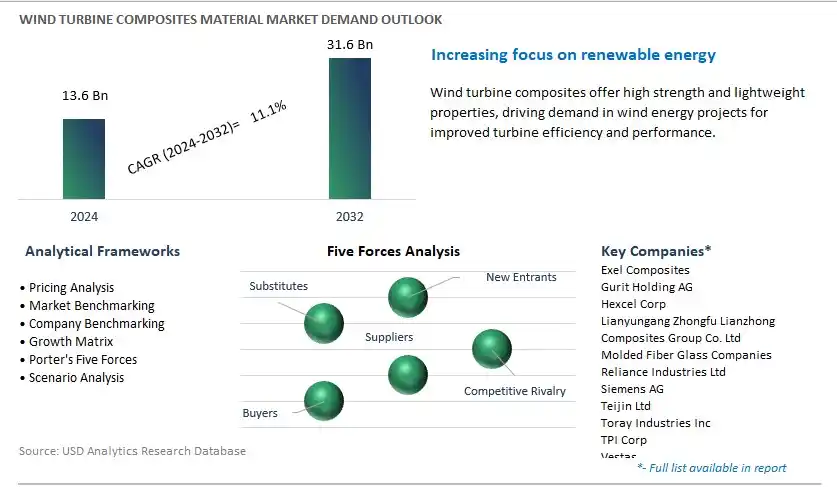

The market report analyses the leading companies in the industry including Exel Composites, Gurit Holding AG, Hexcel Corp, Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd, Molded Fiber Glass Companies, Reliance Industries Ltd, Siemens AG, Teijin Ltd, Toray Industries Inc, TPI Corp, Vestas, and others.

A significant market trend in the wind turbine composites material industry is the increased adoption of longer blades and larger turbines. As wind energy continues to play a vital role in the transition towards renewable energy sources, there is a growing demand for wind turbines with greater power output and efficiency. This trend is driven by advancements in turbine design and technology, aiming to capture more wind energy at higher altitudes and in lower wind speed conditions. Longer blades and larger turbines require lightweight yet durable materials to withstand the structural demands and environmental conditions, leading to higher usage of composite materials such as fiberglass and carbon fiber reinforced polymers (CFRP). As wind turbine manufacturers strive to optimize turbine performance and reduce the cost of energy production, the market for composite materials tailored for longer blades and larger turbines is experiencing growth and innovation.

The driver behind the growth of the wind turbine composites material market is the global emphasis on renewable energy and carbon emissions reduction. With increasing awareness of climate change and the need to transition away from fossil fuels, governments, corporations, and consumers are increasingly investing in renewable energy sources such as wind power. This driver is fueled by factors such as international agreements, renewable energy targets, and government incentives aimed at promoting clean energy technologies. Wind turbines play a crucial role in harnessing wind energy and reducing greenhouse gas emissions, driving the demand for materials that enable the construction of efficient and reliable wind turbines. As countries worldwide prioritize renewable energy development and seek to achieve carbon neutrality goals, the demand for wind turbine composites materials is expected to rise, creating opportunities for material suppliers and manufacturers in the wind energy supply chain.

An opportunity for growth and differentiation in the wind turbine composites material market lies in the development of advanced composite technologies and manufacturing processes. While composite materials offer numerous advantages such as high strength-to-weight ratio, corrosion resistance, and design flexibility, there is potential for further innovation to meet the evolving needs of the wind energy industry. By investing in research and development, wind turbine composites material manufacturers can develop new materials with enhanced properties such as improved fatigue resistance, higher stiffness, and better damage tolerance. Additionally, there is an opportunity to optimize manufacturing processes to increase production efficiency, reduce material waste, and lower overall costs. By collaborating with wind turbine OEMs (Original Equipment Manufacturers) and leveraging advancements in materials science and engineering, composite material suppliers can capitalize on opportunities to provide innovative solutions that drive the growth and competitiveness of the wind energy sector.

Within the Wind Turbine Composites Material market, the Epoxy segment is the largest segment. Epoxy resins are widely favored in the manufacturing of wind turbine components due to their superior mechanical properties, including high strength, stiffness, and fatigue resistance. These properties make epoxy resins ideal for reinforcing composite materials used in critical wind turbine parts such as blades, nacelles, and towers, where durability and performance are paramount. Additionally, epoxy resins offer excellent adhesion to various reinforcement fibers such as glass, carbon, and aramid, enabling the production of lightweight yet robust composite structures. Moreover, the increasing demand for larger and more efficient wind turbines to meet renewable energy targets drives the adoption of epoxy-based composites, as they enable the design and construction of larger turbine components capable of withstanding harsh environmental conditions and prolonged operational lifespans. As a result, the Epoxy segment commands a significant share of the Wind Turbine Composites Material market, reflecting its widespread use and suitability for meeting the stringent performance requirements of modern wind turbine applications.

Within the Wind Turbine Composites Material market, the Carbon Fiber segment is experiencing rapid growth. Carbon fiber offers superior strength-to-weight ratio and stiffness compared to traditional glass fiber, making it an attractive choice for reinforcing composite materials used in wind turbine components. The increasing demand for larger and more efficient wind turbines drives the need for lightweight yet robust materials capable of withstanding high loads and fatigue stresses. Carbon fiber composites provide enhanced performance and durability, allowing for the design and manufacturing of longer and more slender turbine blades that can capture more wind energy efficiently. Additionally, advancements in carbon fiber manufacturing technologies, such as lower-cost production methods and improved fiber quality, are making carbon fiber more accessible and cost-effective for wind turbine applications. Moreover, carbon fiber's resistance to corrosion and fatigue, coupled with its ability to reduce overall turbine weight, result in improved turbine efficiency and lower maintenance costs over the turbine's operational lifespan. As a result, the Carbon Fiber segment is the fastest-growing segment within the Wind Turbine Composites Material market, driven by its superior performance characteristics and increasing adoption in next-generation wind turbine designs.

Within the Wind Turbine Composites Material market, the Prepreg segment is the largest segment. Prepreg, short for pre-impregnated fibers, involves the impregnation of reinforcement fibers with a resin matrix before the molding process. This method offers precise control over resin content, fiber orientation, and laminate thickness, resulting in high-quality composite parts with consistent mechanical properties. Prepreg materials are widely used in wind turbine manufacturing due to their excellent mechanical performance, ease of handling, and suitability for automated manufacturing processes. Additionally, prepreg materials exhibit superior strength, stiffness, and fatigue resistance, making them ideal for critical wind turbine components such as blades, nacelles, and towers. Moreover, the ability to tailor prepreg formulations to meet specific performance requirements and design criteria further contributes to their dominance in the market. As a result, the Prepreg segment commands a significant share of the Wind Turbine Composites Material market, reflecting its widespread adoption and preference in the wind energy industry for producing reliable and high-performance composite structures.

Within the Wind Turbine Composites Material market, the Nacelles segment is experiencing rapid growth. Nacelles house critical components of a wind turbine, including the gearbox, generator, and control systems, and are subjected to high mechanical loads, dynamic forces, and environmental conditions during operation. As wind turbines continue to increase in size and capacity, there is a growing demand for lightweight yet durable materials capable of withstanding these challenging conditions. Composite materials offer significant advantages over traditional materials such as steel in terms of weight savings, corrosion resistance, and design flexibility, making them increasingly preferred for nacelle construction. Additionally, the integration of advanced composite materials in nacelle design allows for improved aerodynamics, reduced weight, and enhanced energy efficiency, contributing to the overall performance and reliability of wind turbines. Moreover, the expanding global wind energy market, coupled with government initiatives to promote renewable energy, drives the demand for new wind turbine installations, further fuelling the growth of the Nacelles segment. As a result, the Nacelles segment is the fastest-growing segment within the Wind Turbine Composites Material market, propelled by the increasing adoption of composite materials to meet the evolving requirements of modern wind turbine designs.

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Exel Composites

Gurit Holding AG

Hexcel Corp

Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

Molded Fiber Glass Companies

Reliance Industries Ltd

Siemens AG

Teijin Ltd

Toray Industries Inc

TPI Corp

Vestas

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Wind Turbine Composites Material Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Wind Turbine Composites Material Market Size Outlook, $ Million, 2021 to 2032

3.2 Wind Turbine Composites Material Market Outlook by Type, $ Million, 2021 to 2032

3.3 Wind Turbine Composites Material Market Outlook by Product, $ Million, 2021 to 2032

3.4 Wind Turbine Composites Material Market Outlook by Application, $ Million, 2021 to 2032

3.5 Wind Turbine Composites Material Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Wind Turbine Composites Material Industry

4.2 Key Market Trends in Wind Turbine Composites Material Industry

4.3 Potential Opportunities in Wind Turbine Composites Material Industry

4.4 Key Challenges in Wind Turbine Composites Material Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Wind Turbine Composites Material Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Wind Turbine Composites Material Market Outlook by Segments

7.1 Wind Turbine Composites Material Market Outlook by Segments, $ Million, 2021- 2032

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

8 North America Wind Turbine Composites Material Market Analysis and Outlook To 2032

8.1 Introduction to North America Wind Turbine Composites Material Markets in 2024

8.2 North America Wind Turbine Composites Material Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Wind Turbine Composites Material Market size Outlook by Segments, 2021-2032

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

9 Europe Wind Turbine Composites Material Market Analysis and Outlook To 2032

9.1 Introduction to Europe Wind Turbine Composites Material Markets in 2024

9.2 Europe Wind Turbine Composites Material Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Wind Turbine Composites Material Market Size Outlook by Segments, 2021-2032

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

10 Asia Pacific Wind Turbine Composites Material Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Wind Turbine Composites Material Markets in 2024

10.2 Asia Pacific Wind Turbine Composites Material Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Wind Turbine Composites Material Market size Outlook by Segments, 2021-2032

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

11 South America Wind Turbine Composites Material Market Analysis and Outlook To 2032

11.1 Introduction to South America Wind Turbine Composites Material Markets in 2024

11.2 South America Wind Turbine Composites Material Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Wind Turbine Composites Material Market size Outlook by Segments, 2021-2032

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

12 Middle East and Africa Wind Turbine Composites Material Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Wind Turbine Composites Material Markets in 2024

12.2 Middle East and Africa Wind Turbine Composites Material Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Wind Turbine Composites Material Market size Outlook by Segments, 2021-2032

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Exel Composites

Gurit Holding AG

Hexcel Corp

Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

Molded Fiber Glass Companies

Reliance Industries Ltd

Siemens AG

Teijin Ltd

Toray Industries Inc

TPI Corp

Vestas

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Resin

Epoxy

Polyester

Vinyl Ester

By Fiber

Glass Fiber

Carbon Fiber

By Manufacturing Process

Vacuum Injection Molding

Prepreg

Hand Lay-up

By Application

Blades

Nacelles

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Global Wind Turbine Composites Material Market Size is valued at $13.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 11.1% to reach $31.6 Billion by 2032.

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

Exel Composites, Gurit Holding AG, Hexcel Corp, Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd, Molded Fiber Glass Companies, Reliance Industries Ltd, Siemens AG, Teijin Ltd, Toray Industries Inc, TPI Corp, Vestas

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2032; Currency: Revenue (USD); Volume