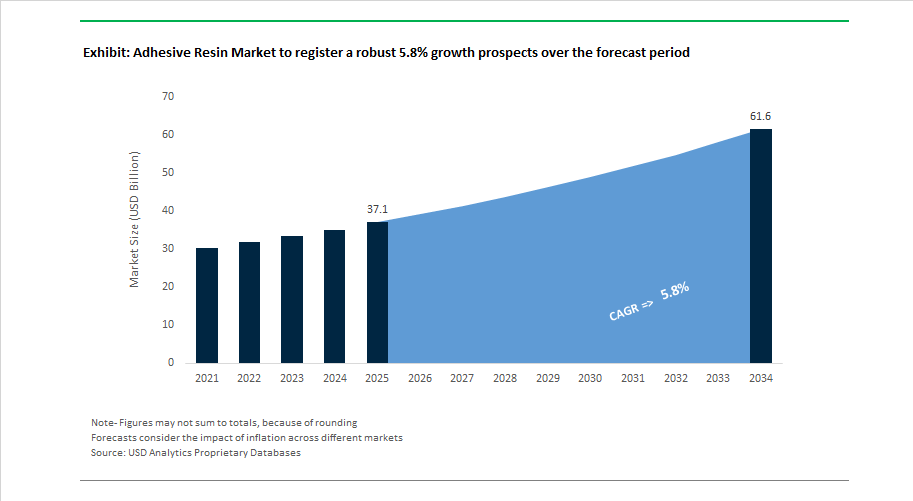

Market Overview: Adhesive Resin Market Set to Reach $61.6 Billion by 2034 as EV Bonding, Sustainable Chemistries, and High-Performance Formulations Accelerate

The global adhesive resin market is projected to grow from $37.1 billion in 2025 to $61.6 billion by 2034, advancing at a 5.8% CAGR. Market expansion is supported by rising use of structural acrylic resins, epoxy systems, silane-modified polymers, hot melt adhesive resins, and waterborne formulations across electric vehicles, aerospace assemblies, advanced packaging, infrastructure waterproofing, and industrial flooring. Adhesive resins are central to modern lightweight engineering, multi-material bonding, and energy-efficient manufacturing, delivering performance in shear strength, thermal resistance, flexibility, chemical durability, and low-temperature curing. Sustainability pressures are reshaping resin development toward bio-based feedstocks, phthalate-free chemistries, ISCC PLUS certified mass-balance materials, and carbon-neutral adhesive systems, while EV battery architectures and large-format automotive displays are creating new technical bonding requirements that conventional fastening cannot address.

Strategic activity intensified in April 2024 when Henkel expanded its African footprint through acquisition of a regional adhesives business, integrating local resin technologies for construction and consumer sectors. In September 2024, H.B. Fuller and Sika formed a sustainability collaboration to co-develop carbon-neutral adhesive resin technologies. Automotive bonding innovation accelerated in January 2025 as 3M launched Scotch-Weld DP8000 structural acrylic adhesives engineered for bonding aluminum to composites in EVs. Infrastructure-driven growth strengthened in March 2025 when Sika acquired Gulf Seal in Saudi Arabia, expanding capacity for resin-based waterproofing membranes aligned with regional construction programs. Portfolio expansion continued in May 2025 with Sika acquiring HPS North America, enhancing its industrial resin flooring systems presence. Sustainable chemistry breakthroughs followed in June 2025 when Sika patented a bio-based amine hardener for epoxy systems suitable for aerospace and automotive performance standards.

Advanced formulation development intensified through August 2025 as Henkel introduced phthalate-free Darex COV PVC-based resins that enable lower curing temperatures for metal packaging seals. Process-enhancing additives entered the market in November 2025 when Sasol Chemicals launched hydrogenated hard wax for high-performance hot melt adhesive resins, improving thermal stability and line speeds in automated packaging. Circular and low-carbon resin production advanced in November 2025 as Arkema secured ISCC PLUS certification for its waterborne resin site, enabling bio-attributed adhesive formulations. Electronics and vehicle interior bonding progressed in December 2025 with Henkel’s Loctite MS 9650 SMP resin for large automotive displays. EV structural bonding integration accelerated in October 2025 when Sika joined Alumobility to supply SmartFlow injection resins for aluminum chassis assemblies. Battery system innovation expanded in February 2026 as Arkema signed an MoU with Senior to deploy Incellion acrylic-based resins designed to enhance adhesion and safety in lithium-ion battery modules.

Strategic Industry Trends and Emerging Growth Opportunities Reshaping the Adhesive Resin Market

Market Trend: Adhesive Resin Reformulation Accelerates To Meet Bio-Based and Circular Packaging Regulation

A priority shift is taking place in adhesive formulation, moving toward bio-based, mass-balanced, and recycling-friendly chemistries. The regulatory catalyst is the EU Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be recyclable by 2030 and pushes converters toward mono-material laminates that simplify recycling pathways.

In March 2025, Bostik (Arkema) launched Fast Glue Ultra+, featuring 60% bio-based content, giving brand owners a quantifiable Scope 3 emissions advantage. Arkema’s eight-year biomethane supply agreement with ENGIE enables ISCC+ certified adhesive resin output, scaling low-carbon production across France and the EU. Dow’s divestment of its flexible packaging laminating adhesive business to Arkema further concentrates industry capability: Dow focuses on its Circulus recycling model while Arkema positions itself to own the next generation of recyclable-laminate adhesives. In 2025 and beyond, adhesive resins that support circularity will define procurement criteria, particularly in FMCG, food packaging, and health products.

Market Trend: Localization and Onshoring of Adhesive Resin Manufacturing to Reduce Strategic Dependency

Geopolitical instability, shipping constraints, and solvent regulatory restrictions are accelerating regional manufacturing footprints for adhesive resins. H.B. Fuller’s FY2025 capex of USD 140 million is centered on regionalizing production capacity to serve high-growth sectors such as medical devices, electronics, and automotive assembly. The “customer-centric innovation” model signals a new trend where producers align R&D hubs directly beside customer manufacturing clusters for faster qualification and stronger design co-development.

Arkema’s USD 27 million expansion in Middleton, Massachusetts will significantly scale high molecular weight polyester adhesive resins, which are crucial for recyclable flexible packaging. Meanwhile, U.S. EPA and EU solvent crackdowns (including Regulation (EU) 2025/1090) have increased demand for water-based and low-VOC resin systems, driving approximately 30% growth in regional R&D investments from 2025–2026. By 2030, resin companies that maintain offshore-heavy production will face cost disadvantages and slower speed-to-market compared to those with localized polymer value chains.

Market Opportunity: High-Performance Adhesive Resins Becoming Critical to EV Battery Cell Assembly and Thermal Safety

The shift toward Cell-to-Pack (CtP) and Cell-to-Chassis (CtC) battery architecture in electric vehicles is expanding the use of adhesive resins beyond bonding into thermal interface material (TIM) roles. Leading epoxy-based resins released in Q1 2025 are engineered to maintain structural adhesion at temperatures above 80°C, replacing mechanical fasteners and enabling 15 to 20% EV battery pack weight reduction, improving range and efficiency.

Fire-control performance is now a selection metric. 3M’s Flame Barrier FRB-NT resin platform is being integrated by battery module manufacturers to inhibit thermal runaway propagation while still meeting UL 94 V-0 dielectric criteria. Academic and commercial innovation is also shaping recyclability. MIT’s August 2025 breakthrough in self-assembling “debond-on-demand” aramid amphiphile electrolytes opens a long-term pathway where battery components can be chemically separated at end-of-life, an advancement that could solve the recycling barrier in solid-state batteries. Over the next decade, adhesive resins that combine bond strength, heat dissipation, and reversible debonding will unlock long-duration OEM contracts and pricing premiums.

Market Opportunity: Structural Adhesive Resins Driving the Rise of Mass Timber and Green Building Infrastructure

Mass timber is emerging as a high-value demand engine for structural adhesive resins, particularly in high-rise construction where wood competes with steel and concrete on carbon credentials. The adhesives used in engineered wood products such as Cross-Laminated Timber (CLT) and Glue-Laminated Timber (GLT) must deliver fire resistance, load-bearing consistency, and long open-time performance for factory throughput.

Henkel’s Loctite HB XE PUR adhesive achieves a 0.65 mm per minute linear charring rate, meeting Eurocode 5 and enabling wood-based skyscrapers without structural compromise. Kiilto’s Pro SW line demonstrated 30% increased bonding efficiency for CLT factories, significantly improving cycle time without capital equipment upgrades. At Ligna 2025, demand for ultra-low diisocyanate adhesives (<0.1 percent) surged due to REACH enforcement, creating a premium pricing segment inside the USD 2.7 billion global construction adhesive resin market. As cities mandate embodied carbon reductions in buildings, adhesive resin suppliers are strategically positioned to capture growth through fire-rated, micro-emission, and high-efficiency engineered-wood formulations.

Adhesive Resin Market Share and Segmentation Insights

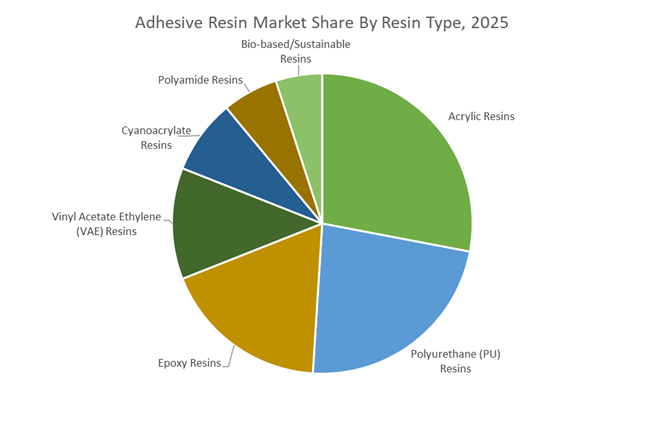

Market Share by Resin Type: Acrylic Resins Lead as Sustainable Chemistries Gain Momentum

Acrylic resins account for approximately 28% of the global adhesive resin market in 2025, leading due to superior weatherability, optical clarity, and cost efficiency, making them the default choice for pressure-sensitive adhesives used in labels, tapes, and graphics films. Accelerating adoption of waterborne acrylics to meet VOC regulations further strengthens this segment. Polyurethane resins rank second, offering unmatched versatility across flexible packaging laminates, automotive structural bonding, and reactive hot melts, with solvent-free and 100% solids systems driving innovation. Epoxy resins dominate premium structural applications requiring high strength and chemical resistance, including aerospace, wind blades, and electronics underfill, though growth is moderated by slower cure speeds. Cyanoacrylates remain indispensable for rapid bonding in medical devices and electronics assembly. Bio-based and sustainable resins hold the smallest share but are the fastest growing, as regulatory pressure and corporate net-zero targets accelerate adoption despite 20 to 30% price premiums.

Market Share by Application: Packaging Dominates While EVs and Electronics Reshape Demand

Packaging represents roughly 34% of adhesive resin consumption in 2025, driven by acrylic and VAE resins used in carton sealing, case sealing, and flexible laminates, with e-commerce expansion and water-based adhesive substitution sustaining volume growth. Construction ranks second, supported by flooring systems, roofing membranes, and panel lamination, as infrastructure spending offsets softer residential activity. Automotive & transportation is undergoing a material transition, with polyurethane and epoxy resins replacing mechanical fasteners for lightweight aluminum and composite bonding, while battery pack assembly in EVs drives structural adhesive demand. Electronics & semiconductors rely on high-purity acrylics and epoxy underfills for miniaturized components, with 5G infrastructure and AI server deployments accelerating uptake. Aerospace & defense remains the smallest by volume but delivers the highest value per kilogram, led by epoxy film adhesives and cyanoacrylates. Healthcare maintains stable growth, while woodworking remains mature but volume-intensive.

Competitive Landscape: Technology-Driven Differentiation in the Global Adhesive Resin Market

The Adhesive Resin Market is increasingly shaped by regulatory compliance, electrification, sustainable packaging, and advanced materials engineering. Leading manufacturers are pivoting toward silane-modified polymers, low-monomer polyurethanes, bio-based elastomers, and recyclable adhesive systems to support automotive displays, EV batteries, flexible packaging, and modular construction. Competitive advantage now hinges on application-specific resin design, customer co-creation platforms, and digital material science. Strategic expansions across Asia-Pacific and North America further reflect rising demand from electronics, construction, and clean energy assembly.

Henkel AG & Co. KGaA advances functional sustainability across automotive, packaging, and electronics

Henkel AG & Co. KGaA remains the global benchmark in adhesive technologies, embedding “functional sustainability” across its structural adhesive and hot-melt resin portfolios. In early 2026, Henkel launched Loctite MS 9650, a next-generation silane-modified polymer adhesive engineered for automotive displays, delivering high UV resistance and faster curing cycles. The company is transitioning its Darex COV sealant range to phthalate-free and PVC-free formulations to meet evolving REACH and SVHC requirements. Core offerings span Loctite, Teroson, and Technomelt systems, while the Inspiration Center Düsseldorf enables real-time customer co-creation and recyclability validation through its Packaging RecycLab platform.

Arkema S.A. scales Bostik adhesive resins for flexible packaging and advanced mobility

Arkema operates its adhesive resin business primarily through its Bostik brand, positioning itself as a pure-play specialty materials supplier. The successful integration of Dow’s laminating adhesives business in 2025 significantly strengthened Arkema’s presence in flexible packaging and electronics. Its Orevac® grafted polyolefins and M-Resins® support resealable packaging and multilayer structural films, while current R&D emphasizes Advanced Mobility with adhesive resins for lithium-ion battery cell-to-pack bonding and thermal management. Arkema’s “close to customer” strategy includes new manufacturing facilities in Gujarat, Malaysia, and the Philippines, targeting high-growth Asian construction and industrial markets.

H.B. Fuller focuses on high-value specialty resins across hygiene, aerospace, and roofing

H.B. Fuller, the world’s largest pure-play adhesives company, concentrates on complex formulations that deliver mission-critical performance despite representing a small fraction of total product cost. In late 2025, the company exited low-margin commodity segments to focus on 32 high-growth technology platforms, including e-commerce packaging and clean energy. Key innovations include plasticizer-resistant polymers for luxury vinyl tile, preventing sunlight-driven adhesive degradation. H.B. Fuller supplies specialized resins for diapers, aerospace components requiring extreme-temperature elasticity, and commercial roofing systems. Its core strength lies in technical agility and customized service for a highly fragmented global customer base.

3M Company integrates digital material science into advanced adhesive resin development

3M leverages proprietary technology platforms such as microreplication, thin films, and precision coating to engineer differentiated adhesive resin chemistries. In 2025, the company received an ASC Innovation Award for 3M™ Fastbond™ PSA 1049, a high-performance water-based alternative to solvent systems. Its VHB™ and Scotch-Weld™ acrylic and epoxy resins are widely adopted for industrial metal-to-plastic bonding. In 2026, 3M launched the “Ask 3M” AI assistant, enabling engineers to specify adhesive resins for novel material combinations. The company’s Digital Bonding strategy integrates automated dispensing with data-driven formulation design.

Sika AG dominates construction adhesives while accelerating EV-ready bonding systems

Sika AG leads the construction and infrastructure adhesive resin segment, while rapidly expanding into electric vehicle assembly. The launch of Purform® Technology introduced ultra-low monomer polyurethane adhesives compliant with new European safety thresholds. Sikaflex® and SikaTack® remain industry standards for elastic bonding in transport and building applications. Strategically, Sika is focused on sealing and bonding solutions for modular and prefabricated construction, a fast-growing trend across Asia-Pacific. Its global R&D platform spans silicones, STP, epoxies, and acrylates, enabling technology-agnostic customer solutions across construction, mobility, and industrial markets.

Dow Inc. strengthens circular packaging and bio-based adhesive resin platforms

Dow operates across the adhesive resin value chain, supplying tackifiers and polyolefin elastomers while also producing formulated systems for construction and electronics. Key offerings include AFFINITY™ RE bio-based elastomers and DOWSIL™ silicone adhesives for lighting and architectural facades. Dow recently introduced tall-oil-derived bio-feedstock resins that reduce carbon footprints without requiring hot-melt equipment retrofits. Capacity expansions in China and North America during 2025–2026 support 5G antenna and solar panel assembly. Dow’s strategic focus on circular packaging centers on adhesive resins engineered to preserve recyclability in multilayer polyethylene films.

Germany Adhesive Resin Market: Recyclability-Driven Innovation and High-Precision Resin Engineering

Germany remains the European benchmark for advanced adhesive resin development, supported by strong regulatory leadership and continuous industrial modernization. In October 2024, Henkel announced an investment of approximately €20 million to expand and modernize its Bopfingen adhesives plant through 2025. The project is focused on scaling production of hot-melt and polyurethane adhesive resins to serve automotive, electronics, and industrial assembly markets where consistency and high thermal resistance are critical.

Regulatory pressure is a primary growth catalyst. Germany’s commitment to achieving 90% recyclability or reusability in plastic packaging by 2025 is accelerating the adoption of de-bondable adhesive resins that enable clean separation of multilayer materials during recycling. At the same time, German manufacturers are prioritizing compliance with EN 50642 standards, driving demand for low-halogen and halogen-free epoxy and polyurethane systems that meet strict fire safety and toxicity thresholds. Innovation is extending into additive manufacturing; in November 2025, Henkel introduced Loctite 3D MED414 Red and Clear medical-grade photopolymer resins at Formnext 2025, addressing growing demand for biocompatible materials in medical device manufacturing. Complementing these advances, Evonik’s Smart Effects platform integrates silane and silica technologies to improve de-inking and recyclability in flexible packaging, while automation-driven micro-dosing systems are optimizing high-viscosity resin usage in automotive and electronics applications.

India Adhesive Resin Market: Localization, Infrastructure Expansion, and Smart Manufacturing Adoption

India’s adhesive resin market is transitioning rapidly from import dependence toward localized, technology-driven production. In July 2024, Henkel completed Phase III of its Kurkumbh facility near Pune, commissioning a dedicated Loctite plant to serve domestic demand from the MRO and automotive sectors. The site incorporates Automated Storage and Retrieval Systems and LEED Gold certification, reflecting India’s broader push toward Industry 4.0-enabled and environmentally responsible chemical manufacturing.

Demand growth is strongly linked to infrastructure development. The National Infrastructure Pipeline is driving large-scale consumption of structural epoxy and polyurethane adhesive resins for metro rail projects and 5G base station deployment, where vibration resistance and long-term durability are essential. Policy incentives are reinforcing this trend; the Production Linked Incentive scheme for chemicals is encouraging domestic players such as Indofil Industries to expand R&D into bio-based reactive resins. Packaging is another high-growth segment, as India’s food and beverage industry shifts toward premium flexible packaging, increasing demand for high-barrier laminating adhesive resins. Skill development initiatives launched in collaboration with Central Institute of Petrochemicals Engineering and Technology are strengthening technical capabilities in advanced polymer resin compounding, supporting long-term industry scalability.

China Adhesive Resin Market: Trade Reorientation, EV Supply Chains, and Electronics-Focused Resins

China’s adhesive resin industry is navigating a complex environment shaped by trade actions, domestic electrification, and electronics manufacturing expansion. In July 2025, the European Commission imposed definitive anti-dumping duties of 17.3 to 33% on epoxy resins originating from China, prompting manufacturers to redirect exports toward Southeast Asia and the Middle East. Despite these constraints, domestic adhesive resin volumes remained resilient in 2025, supported by strong internal demand.

Electrification is a central growth engine. China continues to scale production of PVDF and halogen-free flame-retardant masterbatches used in adhesive systems for EV batteries and large-scale battery energy storage systems. Advanced electronics manufacturing is also driving investment in flexible epoxy resins for 5G circuit boards, where signal integrity and thermal stability are critical. Regulatory changes are influencing formulations; new national standards for high-volume additives, including xanthan gum and L-malic acid, coming into force in March 2026, are impacting aqueous adhesive systems used in packaging and paper applications. On the supply side, energy transition projects such as the Evonik-Fuhua hydrogen peroxide joint venture are ensuring consistent access to high-purity inputs required for semiconductor-grade adhesive resins.

United States Adhesive Resin Market: Defense Applications, PFAS Substitution, and Circular Epoxy Systems

The United States adhesive resin market is characterized by consolidation, sustainability-driven reformulation, and high-value defense and energy applications. In October 2025, Chase Corporation completed the acquisition of United Resin, significantly strengthening its portfolio of MIL-SPEC and UL-approved epoxy resins for aerospace and defense use. This reflects growing demand for high-reliability adhesive systems in mission-critical applications.

Regulatory pressure is accelerating innovation. State-level PFAS bans taking effect between 2025 and 2026 are driving rapid commercialization of non-PFAS, silicone-based, and low-retention adhesive resins. Sustainability is also influencing product design; Westlake Epoxy launched an ISCC PLUS-certified bio-attributed epoxy resin in late 2025 to reduce the carbon footprint of wind turbine blade manufacturing. Broader decarbonization efforts are evident, with Dow sourcing 750 MW of renewable power by the end of 2025 to lower Scope 2 emissions from adhesive resin production. Automotive electrification is another catalyst, as Hexion introduced a fire-retardant epoxy system that delays thermal runaway in EV battery enclosures without heavy mineral fillers. At the innovation frontier, U.S. startups are advancing vitrimer epoxies that combine thermoset performance with heat-enabled recyclability.

Japan Adhesive Resin Market: Optical Precision, Electronics Reliability, and Bio-Based Transition

Japan’s adhesive resin industry is distinguished by precision engineering, electronics leadership, and materials innovation. In December 2025, Mitsubishi Chemical Group developed a high-transparency epoxy resin for optical sensors that maintains clarity during high-temperature soldering, addressing stringent requirements in imaging and sensing devices. The expansion of 5G infrastructure is reinforcing demand for advanced electronics adhesives; in November 2025, DIC Corporation launched a flexible epoxy resin designed to minimize signal loss and cracking in high-speed circuit boards.

Logistics and process efficiency are also shaping innovation. ADEKA Corporation introduced a latent curing agent in October 2025 that enables room-temperature storage of one-pot epoxy adhesives, simplifying global distribution. In maritime applications, Kansai Paint developed an epoxy primer with enhanced corrosion resistance to extend vessel maintenance cycles. Electrification trends are driving development of polyurethane-based thermal interface materials for EV battery potting, while updated certifications from Japan’s Ministry of Economy, Trade and Industry are encouraging the use of biomass-derived monomers in electronic-grade adhesive resins.

Comparative Summary: Strategic Positioning in the Adhesive Resin Industry

Adhesive Resin Market County Level Snapshot

|

Country

|

Primary Growth Drivers

|

Strategic Impact on Adhesive Resins

|

|

Germany

|

Recyclability mandates, fire safety standards, automation

|

Leadership in de-bondable and halogen-free resins

|

|

India

|

Localization, infrastructure projects, PLI incentives

|

Rapid domestic scale-up and application diversification

|

|

China

|

EV batteries, 5G electronics, trade reorientation

|

High-volume production with electronics focus

|

|

United States

|

Defense demand, PFAS bans, renewable energy

|

High-performance and circular epoxy innovation

|

|

Japan

|

Optical sensors, 5G reliability, bio-based materials

|

Precision-engineered and specialty resin leadership

|

Adhesive Resin Market Report Scope

Adhesive Resin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.1 Billion

|

|

Market Size (2034)

|

$61.6 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Resin Type (Epoxy Resins, Polyurethane (PU) Resins, Acrylic Resins, Vinyl Acetate Ethylene (VAE) Resins, Polyamide Resins, Cyanoacrylate Resins, Bio-based/Sustainable Resins), By Technology (Water-based Adhesives, Solvent-based Adhesives, Hot-melt Adhesives, Reactive/Two-component Systems, UV/Light-cured Resins), By Application (Packaging, Construction, Automotive & Transportation, Electronics & Semiconductors, Aerospace & Defense, Healthcare & Medical, Woodworking & Furniture), By Formulation Form (Liquid/Dispersion, Solid/Pellet, Film/Tape, Paste/Putty)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Arkema S.A., H.B. Fuller Company, Dow Inc., Sika AG, 3M Company, Evonik Industries AG, Mitsubishi Chemical Group, Huntsman Corporation, Westlake Epoxy, DIC Corporation, Wanhua Chemical Group, LG Chem Ltd., Chase Corporation, Indofil Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Adhesive Resin Market Segmentation

By Resin Type

- Epoxy Resins

- Polyurethane (PU) Resins

- Acrylic Resins

- Vinyl Acetate Ethylene (VAE) Resins

- Polyamide Resins

- Cyanoacrylate Resins

- Bio-based/Sustainable Resins

By Technology

- Water-based Adhesives

- Solvent-based Adhesives

- Hot-melt Adhesives

- Reactive/Two-component Systems

- UV/Light-cured Resins

By Application

- Packaging

- Construction

- Automotive & Transportation

- Electronics & Semiconductors

- Aerospace & Defense

- Healthcare & Medical

- Woodworking & Furniture

By Formulation

- Liquid/Dispersion

- Solid/Pellet

- Film/Tape

- Paste/Putty

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Adhesive Resin Market

- Henkel AG & Co. KGaA

- Arkema S.A.

- H.B. Fuller Company

- Dow Inc.

- Sika AG

- 3M Company

- Evonik Industries AG

- Mitsubishi Chemical Group

- Huntsman Corporation

- Westlake Epoxy

- DIC Corporation

- Wanhua Chemical Group

- LG Chem Ltd.

- Chase Corporation

- Indofil Industries Limited

*- List not Exhaustive