Market Overview: High-Performance Metrics Driving the 11.1% CAGR in Advanced Phase Change Materials Market Size

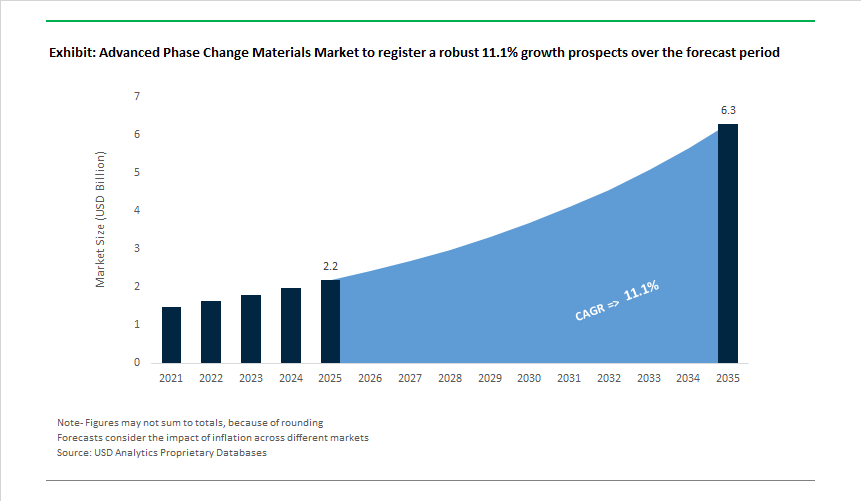

The Advanced Phase Change Materials Market, valued at USD 2.2 billion in 2025, is forecast to reach USD 6.3 billion by 2035 at an impressive 11.1% CAGR, propelled by the intensifying need for precision thermal control across energy storage, EV battery safety, cold-chain logistics, smart apparel, and building energy efficiency. As major manufacturers scale next-generation PCM technologies, the competitive landscape is being reshaped by advances in high latent-heat formulations, microencapsulation durability, nanomaterial-enhanced thermal conductivity, and bio-derived PCM chemistry.

Leading PCM producers have demonstrated that commercial materials must achieve >300 MJ/m³ latent heat density, high thermal conductivities, and thermal stability cycles without phase separation-reflecting benchmarks set by innovators such as Rubitherm’s RT-series, Microtek’s MPCM microcapsules, and Climator’s ClimSel® salt-hydrate systems. In EV platforms, automotive suppliers increasingly specify PCMs that maintain dimensional stability above 120-140°C, integrate into module-level fire-propagation barriers, and demonstrate validated UL 94 V-0 flammability ratings-requirements aligned with ongoing development efforts by Phase Change Energy Solutions and Croda’s bio-based CrodaTherm™ PCMs.

In temperature-controlled logistics, system integrators are prioritizing food-grade, non-corrosive PCM formulations capable of maintaining 2-8°C for >72 hours in high-load insulated shippers, mirroring performance characteristics of Sonoco ThermoSafe and Cold Chain Technologies systems. In the built environment, PCMs embedded into gypsum boards and plasters are increasingly engineered for 50+ year stability, high cycling resistance, and compatibility with automated panel manufacturing lines.

Market Analysis: Strategic Shifts, Regulatory Pressures, and Application Momentum Shape the Market Outlook

The global PCM landscape experienced accelerated commercialization and regulatory transitions. In December 2025, TempraMed achieved a major global milestone via its partnership with Maccabi Healthcare Services, enabling large-scale deployment of medication-protection devices using PCMs. This aligns with a broader trend of PCM adoption in pharmaceuticals, where controlled temperature stability has become a competitive differentiator. In November 2025, BASF allocated a significant portion of its 2026 R&D budget to advancing microencapsulation technologies for EV battery thermal control, signaling strong industry focus on preventing thermal runaway and improving battery lifespan across e-mobility platforms.

October 2025 saw Rubitherm launching SP-line inorganic PCMs with verified 10,000-cycle stability, strengthening the material foundation for district heating/cooling and industrial TES systems. On the other hand, August 2025 marked a major sustainability milestone for Croda International, which confirmed its entire CrodaTherm™ portfolio as 100% USDA-certified bio-based, matching rising demand for renewable and non-toxic thermal management materials. May 2025 further expanded market manufacturing capability when Cryopak opened a 60,000 sq ft facility in Atlanta to support scaled production of PCM-based temperature-controlled packaging-vital for global cold-chain logistics.

Strategic momentum continued into March 2025, with PureTem LLC introducing PCM-enabled textile coatings designed to buffer ambient temperature fluctuations-driving adoption in high-performance apparel and protective clothing. Regulatory pressure intensified in January 2025, when the EU (ECHA) finalized new REACH mandates requiring toxicity testing and material reformulation for select inorganic PCM additives, impacting European suppliers and accelerating compliance-driven innovation. Complementing regulatory initiatives, the U.S. DOE issued a $15 million funding program in December 2024 to integrate PCM-enhanced insulation in residential HVAC systems, supporting national energy-efficiency goals and strengthening PCM integration into the building sector.

Advanced Phase Change Materials (PCM) Market: Trends and Opportunities

High-Capacity, Form-Stable PCMs Redefine Passive Cooling in AI Data Centers

Hyperscale data centers are rapidly adopting isothermal thermal management strategies as AI and high-performance computing (HPC) workloads generate short-duration heat spikes that overwhelm conventional air and liquid cooling. Advanced form-stable PCMs are now being embedded directly into server heat sinks, rack-door heat exchangers, and raised-floor panels to absorb transient thermal loads and discharge heat during off-peak periods.

Technical benchmarks finalized in early 2025 show that PCMs can store 5–14× more thermal energy per unit volume than sensible heat materials such as water or concrete. This density advantage enables effective peak shaving in facilities where space cooling can account for over 40% of total building energy consumption during summer peaks. By shifting heat rejection to nighttime via passive ventilation, PCM-integrated data halls significantly reduce chiller runtime and grid stress.

Thermal performance is also improving through materials engineering. March 2025 academic studies demonstrated that organic PCMs encapsulated within metallic foams dramatically enhance thermal conductivity, accelerating charge–discharge rates and converting cooling assemblies into high-efficiency Thermal Energy Storage (TES) units without external power draw. Operationally, PCM-buffered racks have been shown to maintain server inlet temperatures within a ±2°C band, minimizing rapid thermal cycling that accelerates semiconductor aging and failure—particularly in dense GPU clusters used for AI training.

Low-Temperature, High-Cycle PCMs Become Core to EV Battery Thermal Management

Electric vehicle manufacturers are converging on battery temperature uniformity (25°C–40°C) as the primary design objective for next-generation Battery Thermal Management Systems (BTMS). Advanced PCMs—frequently doped with expanded graphite or carbon nanotubes—are being deployed to suppress hot spots during ultra-fast DC charging and high-discharge driving.

A large 2025 analysis of 1,320 real-world fast-charging events showed that state-of-charge gains drop by up to 19% once cell temperatures exceed 40°C, while active cooling systems draw 20–25% more energy under extreme conditions. PCM-based passive regulation mitigates both penalties by absorbing latent heat during peak loads, reducing reliance on pumps and chillers.

Thermal uniformity thresholds are tightening. Mid-2025 R&D benchmarks specify that inter-cell temperature deltas must remain below 5°C to prevent localized degradation and thermal runaway. Nano-doped PCMs provide sufficient thermal conductivity to redistribute heat across modules within ~6-minute fast-charge cycles, effectively acting as a passive “thermal fuse.” Over the long term, hybrid PCM–liquid cooling architectures are demonstrating the ability to preserve battery health beyond 10,000 cycles, a performance baseline increasingly required for next-generation chemistries such as LTO and emerging graphene–aluminum-ion systems.

PCM-Integrated Building Envelopes Accelerate Compliance with Net-Zero Energy Codes

Regulatory mandates in Europe and North America are transforming PCMs from optional efficiency enhancers into code-driven building materials. The EU’s recast Energy Performance of Buildings Directive (EU/2024/1275) finalized in 2025 requires all new public buildings to be zero-emission by 2028, extending to all new buildings by January 1, 2030. These rules explicitly encourage thermal energy storage and grid flexibility, creating structural demand for PCM-enhanced wallboards, ceilings, and façade systems.

In the United States, building codes are following suit. By December 1, 2025, Rhode Island adopted the 2024 International Energy Conservation Code (IECC) with “electric-ready” and passive-house compliance pathways that favor PCM-integrated materials to meet Thermal Energy Demand Intensity (TEDI) thresholds.

Measured performance supports regulatory momentum. Comprehensive 2025 reviews indicate that PCM-integrated walls deliver ~14.7% heating energy savings and ~24.5% cooling savings in temperate climates. In semi-arid regions, optimized PCM systems (e.g., RT-35HC) have reduced annual energy gains by up to 66%, positioning PCMs as a cornerstone material for high-performance, low-carbon construction.

High-Temperature PCMs Unlock Long-Duration Grid Storage in CSP Systems

Concentrated Solar Power (CSP) is re-emerging as a viable long-duration energy storage (LDES) solution as grids require firm, dispatchable renewable capacity. Next-generation CSP plants are moving beyond sensible molten-salt storage toward Latent Heat Thermal Energy Storage (LHTES) using PCMs operating between 500°C and 800°C.

China is leading deployment. By mid-2025, installed CSP capacity reached 1.14 GW, with a pipeline exceeding 8 GW across desert-base provinces such as Qinghai and Xinjiang. The country’s 2025 Energy Law mandates long-duration thermal storage for new projects, structurally positioning high-temperature PCMs as essential for peak shaving and grid inertia.

In parallel, the U.S. Department of Energy—through its Solar Energy Technologies Office—is funding R&D to achieve $0.05/kWh baseload CSP, a target that depends on PCMs with volumetric latent heat 5–14× higher than conventional molten salts. Advanced metallic and eutectic salt PCMs are already demonstrating >93% round-trip efficiency, reducing storage tank size and capital intensity. With over 5 GW of CSP projects under development globally, high-cycle-stable, high-temperature PCMs represent one of the most capital-efficient pathways to grid-scale, renewable baseload power.

Market Share Analysis: Advanced Phase Change Materials Market

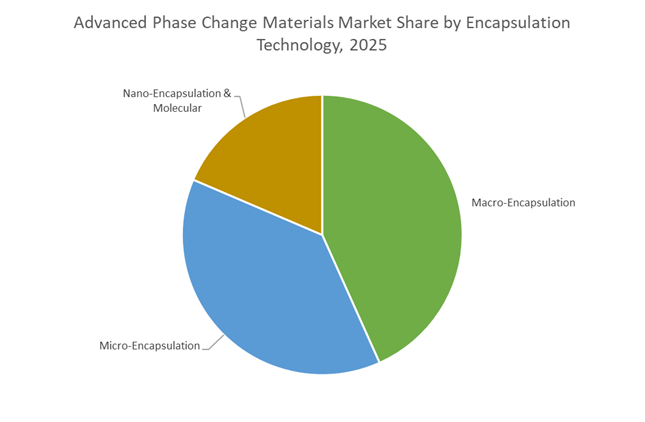

Market Share by Encapsulation Technology: Macro-Encapsulation Anchors Scalable Thermal Storage Deployment

Macro-encapsulation accounts for approximately 42% of the global Advanced Phase Change Materials Market, reflecting its position as the most practical and scalable encapsulation technology for high-capacity thermal energy storage. This segment leads because macro-encapsulated systems can accommodate a very high proportion of active phase change material, enabling superior energy density compared with micro-encapsulated alternatives that dilute PCM content within host materials. Higher PCM loading allows designers to achieve the same thermal storage capacity with smaller system footprints, a critical advantage in space-constrained commercial buildings and infrastructure projects. Market share is further reinforced by leakage control and long-term durability, as sealed panels, pouches, and tubes physically isolate the PCM from surrounding construction materials, preserving performance over multi-decade service lives. From an engineering perspective, macro-encapsulation delivers predictable thermal capacity and repeatable phase-change behavior, simplifying system design and performance modeling. Retrofit compatibility has become an additional growth lever, as macro-encapsulated panels can be integrated into existing ceilings and wall cavities with minimal structural modification, reducing installation time and labor costs. Together, these capacity, durability, and deployment advantages position macro-encapsulation as the dominant encapsulation format for large-scale PCM adoption, securing its leading market share.

Market Share by Application: Building and Construction Drive Demand Through Energy Efficiency Mandates

The building and construction sector represents approximately 35% of total demand in the Advanced Phase Change Materials Market, making it the largest and most influential application segment. This dominance is driven by the sector’s urgent need to reduce operational energy consumption and peak electricity demand as governments tighten net-zero building standards. PCMs embedded within building envelopes act as thermal buffers, absorbing excess heat during the day and releasing it during cooler periods, which significantly reduces reliance on mechanical heating and cooling systems. Market adoption is further accelerated by the ability of PCMs to shift cooling loads away from peak pricing periods, delivering direct operating cost savings for commercial property owners and facility managers. Improved indoor temperature stability also enhances occupant comfort, extending the time buildings remain within optimal comfort ranges without active HVAC intervention. From a compliance standpoint, PCM integration supports high-value green building certifications, where documented energy performance improvements translate into LEED and BREEAM credits. As energy efficiency and lifecycle cost reduction become core design criteria, building and construction remain the primary demand anchor for advanced phase change materials, sustaining their leading share in the global market.

Competitive Landscape: Technology Leadership, Bio-Based Innovation & High-Cycle Pcm Performance

Competition in the Advanced Phase Change Materials market is shaped by companies that excel in microencapsulation science, salt-hydrate engineering, bio-based PCM chemistry, and thermal conductivity enhancement technologies. Suppliers offering custom melting-point formulations, high-cycle durability, and application-specific PCM formats (macro-encapsulated, microencapsulated, textile-integrated) are positioned for strong demand across smart textiles, e-mobility thermal management, cold-chain logistics, construction materials, and TES infrastructure.

BASF SE - Leader in Encapsulated PCM For Construction and E-Mobility Thermal Management

BASF leverages global-scale chemical integration to produce Micronal® PCM, a highly stable microencapsulated solution designed for direct incorporation into plasters, drywall, and building envelopes. Its R&D prioritizes Li-ion battery thermal runaway mitigation, developing PCM materials that expand the safe operating temperature window for EV batteries. BASF’s Schwarzheide site, opened in June 2023, integrates battery materials and recycling operations, giving the company a built-in customer base for PCM-based thermal buffers. Its portfolio includes custom melting-point PCM blends for large-scale TES systems and energy-efficient building materials.

Croda International Plc - Global Pioneer in 100% Bio-Based Phase Change Materials

Croda delivers a fully bio-based PCM range, CrodaTherm™, which is biodegradable, non-toxic, and aligned with major green building certifications. Products such as CrodaTherm 29 offer high latent heat capacity at narrow temperature windows, making them ideal for HVAC, building envelope systems, and comfort modulation applications. Croda’s early commercialization of microencapsulated bio-based PCM (since July 2019) allows seamless adoption in bedding, apparel, and consumer goods. The company also targets the temperature-controlled packaging market, where bio-based PCMs support sustainable cold-chain logistics.

Rubitherm Technologies Gmbh - Specialist in High-Stability Salt Hydrate and Paraffin-Based PCM Systems

Rubitherm is a recognized leader in salt-hydrate PCM engineering, offering SP-line formulations with latent heat storage capacities up to 320 kJ/kg and proven 10,000+ cycle stability, confirmed through in-house long-duration thermal testing. Its RT-line paraffin PCMs span melting points from −9°C to 100°C, enabling integration into solar thermal systems, waste-heat recovery applications, and industrial temperature control solutions. Rubitherm prioritizes PCM formats optimized for macro-encapsulation, ensuring compatibility with passive and active cooling/heating devices in HVAC and TES applications.

Outlast Technologies LLC - Market Leader in Smart Textiles and Thermoregulating Apparel

Outlast holds patented Thermocules™ microencapsulation technology, enabling precise deployment of PCMs into fibers and fabrics. The company dominates the smart textiles and performance apparel segment, partnering with major global brands across sportswear, bedding, and medical textiles. Its PCM-treated bedding materials can maintain surface temperatures up to 3°C lower during heat peaks, demonstrating measurable comfort performance. Outlast offers temperature-tuned PCM ranges engineered to sustain a stable microclimate and improve wearer comfort across diverse climatic conditions.

The United States advanced phase change materials market is being reshaped by federal energy resilience funding and the rapid emergence of “cooling-as-a-service” business models. In 2025, Department of Energy (DOE) programs such as the Critical Facility Energy Resilience (CiFER) initiative and the Energy Storage Innovations Prize have elevated PCMs from passive insulation additives to active thermal energy storage assets. These programs are directly stimulating demand for salt-hydrate and paraffin-based PCMs in commercial buildings, hospitals, and mission-critical infrastructure. The rapid expansion of AI data centers has further intensified adoption, as operators seek non-mechanical thermal buffering solutions to manage peak server loads. Corporations such as Honeywell and Phase Change Solutions are increasingly supplying bio-based PCMs and thermal interface materials optimized for high-density electronics, positioning the U.S. as a demand-led innovation hub for advanced PCM systems.

China’s Dual Circulation Strategy and Industrial-Scale PCM Supply Chains

China’s advanced phase change materials market is defined by industrial scale, vertical integration, and policy-driven self-sufficiency. Under the concluding phase of the 14th Five-Year Plan, PCMs are embedded into the broader “dual circulation” strategy, ensuring domestic control over high-purity chemical intermediates while maintaining export competitiveness. The commissioning of BASF’s Zhanjiang Verbund complex marks a structural milestone, enabling large-volume supply of low-carbon organic intermediates used in encapsulated PCMs. Parallel to this, domestic producers are scaling bio-based and polymer-encapsulated PCMs for EV battery thermal management, a critical requirement in China’s high-nickel battery ecosystem. Urban policy frameworks are also accelerating PCM-integrated construction materials, positioning China as the world’s largest volume market for building-scale thermal energy storage.

European Union Advanced Materials Policy and Sustainability-by-Design Leadership

The European Union is shaping the advanced phase change materials market through regulation rather than volume expansion. The “Advanced Materials for Industrial Leadership” framework and the anticipated Advanced Materials Act are embedding safe-and-sustainable-by-design (SSbD) criteria into PCM commercialization. This regulatory environment is steering demand toward bio-based eutectics, microencapsulated fatty acids, and recyclable PCM textiles. Pan-European funding instruments such as M-ERA.NET are accelerating cross-border R&D in waste-heat recovery and PCM-enhanced coatings. Industrial players including Croda International are actively reformulating PCM portfolios to align with EU chemical safety and circularity mandates, reinforcing Europe’s position as a premium, compliance-driven market for advanced PCMs.

India’s PLI-Backed Cold Chain and HVAC Transformation

India’s advanced phase change materials market is emerging through targeted Production Linked Incentive (PLI) schemes and infrastructure modernization priorities. Increased budgetary allocations for white goods and specialty steel are indirectly catalyzing PCM adoption in energy-efficient air conditioners, cold storage, and refrigerated logistics. The pharmaceutical supply chain is a particularly strong demand center, with form-stable PCMs enabling precise temperature control for vaccines and biologics. Indigenous innovation is expanding beyond construction and logistics into textiles and personal cooling solutions, driven by public-sector research collaborations. These developments position India as a high-growth market where PCMs are tightly linked to energy efficiency, healthcare resilience, and climate adaptation.

Japan’s Materials DX Platform and Electronics-Focused PCM Innovation

Japan’s advanced phase change materials market is anchored in Digital Transformation (DX) and electronics thermal management. The government-supported Materials Research DX Platform is accelerating the design of nano-enhanced and composite PCMs with higher thermal conductivity and faster response times. Strategic collaborations between domestic chemical producers and global PCM specialists are enabling deployment in high-rise buildings, logistics hubs, and semiconductor facilities. Japan’s focus on power electronics, 5G/6G infrastructure, and data-intensive systems ensures sustained demand for precision-engineered PCMs rather than commodity formulations.

South Korea’s MPE 2030 Roadmap and Battery-Centric Localization

South Korea is aligning advanced phase change materials with its Materials, Parts, and Equipment (MPE) 2030 roadmap, emphasizing localization for electronics and battery applications. Government incentives are accelerating the development of solid-to-solid and encapsulated PCMs that can be directly integrated into flexible displays, mobile devices, and EV charging infrastructure. Corporate R&D efforts are increasingly focused on graphite-enhanced and composite PCMs capable of handling extreme heat flux, reinforcing South Korea’s role as a technology-intensive market serving global electronics and EV value chains.

Strategic Investment Comparison: Advanced Phase Change Materials Market (2025)

Advanced Phase Change Materials Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

Key Policy or Investment

|

Dominant PCM Focus

|

|

United States

|

Grid resilience & data centers

|

DOE CiFER and storage funding

|

Salt hydrates, paraffins

|

|

China

|

Industrial scale & self-sufficiency

|

Zhanjiang Verbund expansion

|

Organic & encapsulated PCMs

|

|

European Union

|

Sustainability regulation

|

Advanced Materials Act

|

Bio-based, SSbD PCMs

|

|

India

|

Cold chain & HVAC efficiency

|

PLI schemes for white goods

|

Form-stable, bio-based PCMs

|

|

Japan

|

Electronics & DX

|

Materials Research DX Platform

|

Nano-enhanced composites

|

|

South Korea

|

Battery & display localization

|

MPE 2030 incentives

|

Solid-state composite PCMs

|

Advanced Phase Change Materials Market Report Scope

Advanced Phase Change Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2035)

|

$6.3 Billion

|

|

Market Growth Rate

|

11.1%

|

|

Segments

|

By Material Type (Organic PCMs, Inorganic PCMs, Metallic PCMs, Composite & Hybrid PCMs, Eutectic PCMs), By Encapsulation Technology (Micro-Encapsulation, Macro-Encapsulation, Nano-Encapsulation, Molecular Encapsulation), By Application (Building & Construction, Energy Storage, Electronics Thermal Management, Automotive & Transportation, Cold Chain & Packaging, Textiles & Wearables, Commercial Refrigeration & HVAC), By Thermal Performance (Low, Medium, High Temperature)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International Inc., BASF SE, Croda International Plc, Henkel AG & Co. KGaA, DuPont de Nemours Inc., Sasol Limited, Rubitherm Technologies GmbH, Phase Change Solutions, Pluss Advanced Technologies Pvt. Ltd., Microtek Laboratories Inc., Outlast Technologies LLC, PureTemp LLC, Climator Sweden AB, Cryopak, Phase Change Energy Solutions Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Phase Change Materials Market Segmentation

By Material Type

- Organic Phase Change Materials

- Inorganic Phase Change Materials

- Metallic Phase Change Materials

- Composite and Hybrid Phase Change Materials

- Eutectic Phase Change Materials

By Encapsulation Technology

- Micro-Encapsulation

- Macro-Encapsulation

- Nano-Encapsulation

- Molecular Encapsulation

By Application

- Building and Construction

- Energy Storage

- Electronics Thermal Management

- Automotive and Transportation

- Cold Chain and Packaging

- Textiles and Wearables

- Commercial Refrigeration and HVAC

By Thermal Performance

- Low Temperature

- Medium Temperature

- High Temperature

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Phase Change Materials Market

- Honeywell International Inc.

- BASF SE

- Croda International Plc

- Henkel AG & Co. KGaA

- DuPont de Nemours, Inc.

- Sasol Limited

- Rubitherm Technologies GmbH

- Phase Change Solutions

- Pluss Advanced Technologies Private Limited

- Microtek Laboratories, Inc.

- Outlast Technologies LLC

- PureTemp LLC

- Climator Sweden AB

- Cryopak

- Phase Change Energy Solutions Inc.

*- List not Exhaustive