Market Overview: Aerogel Blanket Market to Reach $7.6 Billion by 2034 as EV Thermal Barriers, LNG Insulation, and Advanced Construction Materials Accelerate Adoption

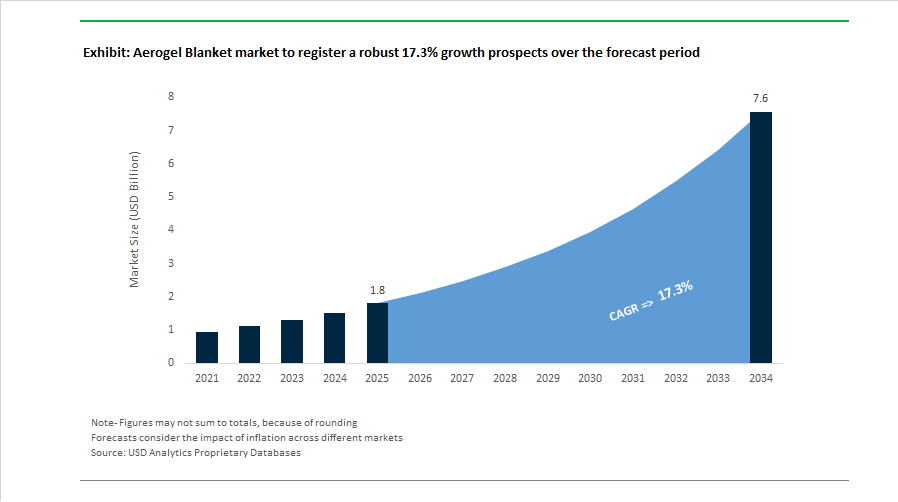

The global aerogel blanket market is projected to expand from $1.8 billion in 2025 to $7.6 billion by 2034, advancing at a rapid 17.3% CAGR. Growth is driven by demand for ultra-low thermal conductivity insulation, fire-resistant thermal barriers, cryogenic insulation systems, and lightweight high-performance building materials across electric vehicles, energy infrastructure, aerospace, defense, and green construction. Aerogel blankets, based on silica aerogel and fiber-reinforced structures, deliver superior thermal resistance, hydrophobicity, flexibility, and space-saving insulation performance compared with conventional mineral wool or foam systems. Market momentum is supported by stricter fire safety regulations, expansion of LNG and subsea energy projects, EV battery thermal runaway mitigation requirements, and adoption of aerogel-enhanced materials in sustainable construction.

Industrial and energy sector developments gained traction in June 2025 when Alkegen commenced full-scale production of AlkeGel fiber-enhanced aerogel insulation engineered for EV battery fire protection. In August 2025, Foli Aerogel formed a strategic alliance with Aerogel Technologies to develop aerogel-based adhesive tapes for electronics and aerospace integration. Construction applications expanded in late 2025 as Isoltech demonstrated aerogel-enhanced cellular concrete using Quartzene material, improving thermal performance while addressing mechanical durability. Strategic portfolio integration advanced in late 2025 when BASF incorporated Aspen’s aerogel technology into Slentex and Slentite insulation platforms for defense and high-end building uses. Supply resilience in industrial insulation was highlighted in November 2025 as Aspen Aerogels reported growth in its energy industrial segment, supported by LNG and subsea project pipelines.

Automotive and textile applications accelerated adoption. In November 2025, Aspen Aerogels secured a major European OEM contract for PyroThin thermal barrier blankets for EV platforms, with production beginning in 2027. Regional manufacturing diversification advanced in early 2026 as Indian firms MG Materials and Wedge India expanded silica aerogel blanket production to serve green building standards and domestic EV markets. Textile integration progressed in January 2026 when Svenska Aerogel received a record order from Outlast Technologies for Aersulate material used in insulated apparel and bedding. The same month, Svenska Aerogel expanded into defense applications with Quartzene-based thermal shielding solutions. Energy infrastructure demand strengthened in January 2026 as Aspen Aerogels confirmed supply of Cryogel blankets for Venture Global’s CP2 LNG project. Material innovation in corrosion control followed in March 2026 with Armacell launching ArmaGel XGH high-temperature aerogel blankets for CUI mitigation in refineries and offshore platforms. These developments position aerogel blanket technologies as critical enablers of lightweight thermal management across transportation, energy, and advanced construction sectors.

Strategic Market Trends and High-Value Opportunities Reshaping the Aerogel Blanket Market

Market Trend: Industrial Retrofit Adoption Accelerates as Energy Efficiency Becomes a Compliance Obligation

A defining trend is the accelerated uptake of aerogel blankets for in-situ retrofits across oil and gas, petrochemical, and heavy manufacturing facilities. The driver is no longer optional energy savings but the need to meet regulated emission reduction timelines. Aerogel delivers up to five times more thermal performance compared to legacy mineral wool systems. This allows operators to reduce insulation thickness by 25 to 30 percent, a key advantage in space-restricted offshore assets and refinery piping networks.

Operational ROI is emerging as the core value proposition. Case studies documented in 2025 show replacement of degraded insulation with silica aerogel blankets reducing steam line surface temperatures by over 50°C, improving thermal containment and cutting heat loss by 15 to 20%. To meet global retrofit demand, Armacell opened a new aerogel factory in Pune, India in June 2025, expanding capacity for its ArmaGel XG product line engineered to withstand –196°C to +650°C. These investments position aerogel as a retrofit-first solution for asset owners trying to reduce maintenance cycles, protect worker safety, and lower operational energy intensity.

Market Trend: Aerogel Innovation Shifts Toward Reinforced, High-Durability, Multi-Material Systems

Early-generation aerogels faced performance limitations due to fragility and moisture sensitivity. The industry is now responding with reinforced composite aerogels that combine silica matrices with aramid fibers and polymeric binders. This shift allows aerogel blankets to withstand vibration, compression, moisture ingress, and cyclic fatigue typical of aerospace, marine, and deep-sea industrial environments.

Outlast Technologies’ Aersulate, launched in May 2024, illustrates this new performance standard – engineered to resist pressure and moisture for long-duration operation in turbine housings and marine engines. Hydrophobic aerogels developed by JIOS maintain less than 1% moisture absorption, significantly mitigating Corrosion Under Insulation (CUI), a problem costing the oil and gas sector billions of dollars in annual unplanned maintenance. Strategic moves such as Armacell’s September 2024 acquisition of full ownership of the Armacell-JIOS joint venture enable vertically integrated powder-to-blanket production, improving supply certainty for the energy and aerospace sectors.

Market Opportunity: Thermal Safety Barriers for EV Battery Packs Create a Fast-Scaling Revenue Channel

As EV architectures evolve, aerogel blankets are emerging as gold-standard solutions for thermal runaway containment. Their dual function – thermal shielding plus compression pad – positions aerogels uniquely relative to mica and polyurethane foam. Aspen Aerogels’ PyroThin material demonstrates temperature resistance up to 1,400°C and, in standardized 62 Ah prismatic-cell trials, prevented propagation between cells for over 30 minutes, outperforming the regulatory baseline requirement of five minutes.

EV OEM adoption is accelerating. General Motors’ 2024 Launch Excellence Award to Aspen signifies a broader industry shift: aerogel is becoming a specified requirement for next-generation EV platforms, particularly those sold into high-regulation markets such as California, the EU, and South Korea. As platforms scale and battery form factors diversify, aerogel suppliers positioned with compression-tolerant and ultra-thin configurations will capture long-term contracts from global vehicle manufacturers.

Market Opportunity: Aerogel as a Compliance Mechanism for EU Building Envelope Retrofits

The European renovation mandate is creating one of the most significant non-industrial demand pools for aerogel insulation. Under the Energy Performance of Buildings Directive (EU 2024/1275), countries must upgrade the worst-performing 16% of non-residential buildings by 2030, a requirement that disproportionately affects historic and multi-story urban structures where space cannot be sacrificed.

Aerogel blankets allow space-efficient insulation with as little as 20 mm thickness replacing 80 mm of rock wool, retaining up to 500% more usable floor area. Economic models in Rome (2025) show that this reclaimed interior area can raise commercial rental revenue by USD 100–250 per square foot, framing aerogel as a profit-generating retrofit material rather than a cost burden. The introduction of 100% bio-based aerogel fibers by SA-Dynamics in April 2024 positions aerogel products to meet Whole-Life Carbon Assessment mandates that become compulsory across the EU beginning 2028, aligning insulation procurement directly with ESG reporting and building-portfolio decarbonization.

Aerogel blankets are shifting from niche thermal insulation into a strategic material class tied to emissions compliance, EV safety, and building decarbonization. Companies capable of delivering reinforced, compression-tolerant aerogel blankets, domestic production near downstream demand hubs, and ESG-certified low-carbon formulations will define competitive leadership in the market through 2030.

Aerogel Blanket Market Share and Segmentation Insights

Market Share by Material Type: Silica Aerogels Dominate While Polymer Variants Accelerate in EV Applications

Silica aerogels account for approximately 78% of the global aerogel blanket market in 2025, maintaining clear dominance due to ultra-low thermal conductivity of 10 to 15 mW per m·K, hydrophobicity, and scalable supercritical drying processes. Fiber reinforcement using glass, PET, or carbon fiber has improved mechanical durability in blanket formats, mitigating inherent brittleness. Commercial benchmarks such as Spaceloft and Lumira remain industry references for high-performance insulation. Polymer aerogels represent the fastest-growing segment, with polyimide, polyurethane, and cellulose variants offering enhanced flexibility and vibration resistance, gaining adoption in EV battery thermal runaway barriers and cryogenic LNG systems. Carbon aerogels remain niche, primarily serving supercapacitors and catalyst supports due to electrical conductivity constraints. Bio-based aerogels hold the smallest share, largely pilot-scale, but benefit from EU-driven circular economy mandates supporting cellulose and chitosan-based insulation alternatives despite performance gaps versus silica.

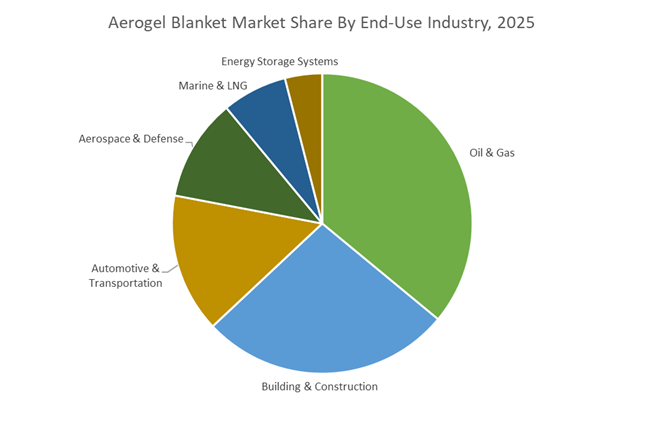

Market Share by End-Use Industry: Oil & Gas Leads Volume While EVs Drive Structural Growth

Oil & gas represent roughly 36% of aerogel blanket demand in 2025, supported by subsea pipeline insulation and refinery steam tracing where reduced thickness and weight advantages are critical for offshore platforms. Building & construction ranks second, driven by net-zero retrofits, Passivhaus specifications, and historic preservation projects under policy incentives such as EU renovation programs and US tax credits. Automotive & transportation is the fastest-growing segment, propelled by EV battery thermal management requirements and safety standards mandating thermal runaway mitigation, making aerogel sheets increasingly standard between lithium-ion cells. Aerospace & defense remain high-margin but low-volume, while marine and LNG applications sustain steady demand in piping and regasification systems. Energy storage systems represent the smallest yet highest-potential segment, with grid-scale battery deployments expected to drive compounded growth beyond 30% through 2030.

Competitive Landscape: EV Thermal Protection and Industrial Decarbonization Accelerating the Aerogel Blanket Market

The Aerogel Blanket Market is rapidly evolving from industrial insulation toward electrification-driven thermal management, lightweight defense systems, and ultra-thin electronics protection. Competitive advantage now hinges on proprietary aerogel platforms, EV battery thermal barrier integration, corrosion-under-insulation mitigation, and scalable manufacturing economics. Market leaders are investing in automotive-qualified production lines, low-CAPEX licensing hubs, and advanced silica particle technologies while expanding across Asia-Pacific, Europe, and North America. Growth is increasingly concentrated in EV battery packs, LNG infrastructure, net-zero buildings, and aerospace, where aerogel blankets deliver unmatched thermal resistance at minimal thickness.

Aspen Aerogels, Inc. pivots from industrial insulation to Tier-1 EV thermal barrier supply

Aspen Aerogels is the global technology leader, actively transforming into a Tier-1 automotive supplier through its PyroThin® platform. The company is repositioning itself as an electrification solutions provider, prioritizing European EV program ramp-ups as of early 2026. In late 2025, Aspen secured a major thermal barrier contract from a leading European OEM, with production scheduled for 2026–2027. Its portfolio spans PyroThin® battery thermal barriers and Pyrogel® / Cryogel® blankets for extreme-temperature industrial environments. Aspen also collaborates with national laboratories on carbon aerogels for next-generation batteries, leveraging its Aerogel Technology Platform® to rapidly engineer flexible, mechanically robust insulation systems.

JIOS Aerogel disrupts EV battery insulation with Thermal Blade® and licensing-led scale

JIOS Aerogel has emerged as a disruptive force by adopting a low-CAPEX licensing and regional hub model to accelerate global production. In January 2026, its Korean licensee secured a major contract to supply Thermal Blade® barriers for next-generation vehicles from Hyundai and Kia. Thermal Blade® is engineered for thin-profile cell-to-cell EV battery protection. JIOS operates an advanced battery testing lab in Singapore in partnership with VDE Renewables, enabling real-time Li-ion performance validation. Strategically, the company is building manufacturing hubs near automotive clusters across Asia and North America.

Armacell International S.A. bridges foam insulation and aerogels with ArmaGel® for LNG and CUI mitigation

Armacell International is integrating high-performance aerogels into its insulation ecosystem via the ArmaGel® platform. The company commissioned a state-of-the-art aerogel manufacturing facility in Pune, India during 2025–2026 to serve Asia-Pacific LNG and industrial markets. Key products include ArmaGel® XG for high temperatures and ArmaGel® XGC for dual-temperature cryogenic systems. Armacell differentiates through corrosion-under-insulation expertise, delivering breathable, hydrophobic blankets that protect pipelines from degradation. In 2025, it introduced the ArmaWin™ digital thermal calculator, enabling engineers to quantify energy savings and carbon reduction from aerogel deployments.

Cabot Corporation advances silica aerogel particles for ultra-thin electronics and 5G insulation

Cabot Corporation focuses on high-purity silica aerogels through its ENTERA® particle technology, supplying lightweight additives used to manufacture blankets, foams, and composites. The ENTERA® portfolio delivers particles up to 20 times lighter than conventional insulation fillers, supporting applications in 5G infrastructure and ultra-thin electronics. Cabot is advancing ambient pressure drying to reduce aerogel production costs while strengthening surface modification to preserve hydrophobicity in harsh outdoor environments. Rather than producing finished blankets, Cabot enables formulators with scalable aerogel building blocks, positioning itself upstream in the global aerogel insulation value chain.

Svenska Aerogel Holding AB scales Quartzene® for defense textiles and net-zero construction

Svenska Aerogel leads the advanced additive segment with its proprietary Quartzene® material, used in aerogel blankets and technical textiles. The company reported a 50% increase in commercial-stage customers during 2025, signaling accelerating adoption in defense and performance fabrics. Its largest-ever order came from Outlast Technologies for Aersulate®, an aerogel-integrated insulating textile. Svenska Aerogel also supports dual-use defense projects for thermal signature management and partnered with Isoltech to embed Quartzene® into low-density cellular concrete for net-zero building facades.

Guangdong Alison Hi-Tech Co., Ltd. drives global cost efficiency with high-volume silica aerogel blankets

Guangdong Alison Hi-Tech is one of the world’s largest aerogel blanket manufacturers, anchoring cost competitiveness through massive scale. Its Alison GR10 series, reinforced with glass fiber, withstands temperatures up to 800°C and is widely deployed in steam pipelines and petrochemical tanks. Alison operates fully integrated production from silica precursors to finished nano-technology carpets, supplying China’s infrastructure boom while exporting extensively to the Americas. In 2026, the company expanded its custom-shape division, delivering pre-cut aerogel blankets for aerospace escape capsules and specialized military equipment, reinforcing its role as the volume backbone of the global aerogel supply chain.

United States Aerogel Blanket Market: EV Battery Safety, Energy Resilience, and Aerospace Pull

The United States is consolidating leadership in high-value aerogel blanket applications, particularly in electric mobility and energy infrastructure. In October 2025, Aspen Aerogels expanded its domestic manufacturing footprint with a new Louisiana facility dedicated to silica aerogel blankets for EV battery packs. This investment aligns with rising OEM demand for ultra-thin thermal barriers that mitigate thermal runaway while minimizing weight penalties. Aspen’s late-2025 pivot toward capital efficiency further sharpened focus on its PyroThin® thermal barrier line, which secured a major European OEM contract with production targeted for 2027.

Energy and climate resilience remain strong demand drivers. Cabot Corporation launched an advanced aerogel composite in September 2025 for offshore oil and gas pipelines in the Gulf of Mexico, emphasizing ultra-low thermal conductivity in corrosive marine environments. Collaboration between U.S. aerogel producers and carbon capture startups is accelerating the use of aerogel blankets as lightweight scaffolds in Direct Air Capture systems. Public funding reinforces adoption, as the U.S. Department of Energy continued grants in 2025 for aerogel-based retrofitting to meet National Precision Building Standards. Aerospace demand is expanding as NASA and private firms deploy aerogel blankets for cryogenic fuel tank insulation, leveraging superior weight-to-performance for long-duration missions.

China Aerogel Blanket Market: Scale Manufacturing, EV Thermal Management, and LNG Infrastructure

China leads the aerogel blanket market by production scale and rapid deployment across industrial energy systems. In July 2025, IBIH Advanced Materials inaugurated an international aerogel R and D center to advance high-volume EV battery thermal management solutions. Provincial energy intensity mandates are accelerating replacement of mineral wool with aerogel blankets in petrochemical plants and district heating pipelines, where temperature stability and space savings are critical.

Supply chain depth and infrastructure investment reinforce growth. Aspen Aerogels confirmed in February 2025 that it is leveraging Chinese contract manufacturing to scale its Energy Industrial and EV segments more cost-effectively. In marine and LNG infrastructure, China National Offshore Oil Corporation earmarked significant capital in early 2025 for LNG terminals, where cryogenic aerogel blankets are primary insulation for tanks and offloading lines. Product diversification is visible in textiles as Jiangyin Qingfeng Chemical Fiber showcased aerogel-infused fibers and flexible blankets for extreme-cold apparel in September 2024. To ensure quality at scale, the Ministry of Industry and Information Technology released updated standards for nano-porous thermal insulation materials in late 2025.

India Aerogel Blanket Market: Capacity Doubling, Refining Demand, and LNG Readiness

India is emerging as a fast-growing production and consumption hub for aerogel blankets, driven by petrochemical expansion and transport modernization. In June 2025, Armacell inaugurated a new Pune facility that doubles global capacity for the ArmaGel XG product line. The site is strategically located to serve India’s expanding refining and petrochemical hubs, where aerogel blankets are increasingly adopted to cut heat loss in steam piping and improve operational efficiency.

Product breadth supports multiple temperature regimes. The Pune plant produces ArmaGel XGH for applications up to 650°C and ArmaGel XGC for cryogenic service, aligning with India’s growing LNG import terminal footprint. Transportation applications are advancing as Armacell showcased rail-specific aerogel insulation at IREE 2025, targeting thermal and acoustic comfort in next-generation high-speed trains. Policy support under the Production Linked Incentive scheme is encouraging local sourcing of silica aerogel precursors, reducing import reliance and strengthening domestic value chains.

Germany Aerogel Blanket Market: Bio-Based Construction, Aviation MRO, and Hydrogen Validation

Germany’s aerogel blanket market is shaped by sustainability leadership and advanced industrial use cases. In August 2025, BASF launched a bio-based aerogel blanket line for sustainable construction, designed to meet stringent passive house efficiency standards. This positions aerogel as a premium insulation solution for low-energy buildings and retrofits.

Industrial and aviation demand adds depth. Germany remains a hub for aerogel maintenance and retrofitting, with Lufthansa Technik integrating aerogel blankets into engine pylon and fuselage insulation packages. Hydrogen economy initiatives are validating aerogel blankets for liquid hydrogen supply chains, where vacuum compatibility and thermal performance are decisive. Circular economy integration is advancing through take-back programs that recycle silica content from decommissioned aerogel blankets into new insulation products.

South Korea Aerogel Blanket Market: EV Safety, Electronics Miniaturization, and Supply Chain Control

South Korea is rapidly building aerogel capacity around batteries and electronics. LG Chem is progressing a 310 billion won investment in Dangjin to establish a dedicated aerogel plant producing high-performance insulators for EV batteries and liquid hydrogen storage. In late 2025, LG Chem launched Nexula™, a proprietary aerogel designed to prevent thermal runaway propagation in high-energy-density energy storage systems.

Consumer electronics provide an additional growth vector. Korean firms are pioneering ultra-thin aerogel blankets as thermal shields in foldable smartphones and slim laptops, where heat dissipation and form factor are tightly constrained. Supply chain consolidation followed the acquisition of shares in JIOS Aerogel, enabling tighter control over aerogel powder inputs used in composite blanket manufacturing and improving cost and quality consistency.

United Arab Emirates Aerogel Blanket Market: Building Codes, Oil and Gas Efficiency, and Diversification

The United Arab Emirates is accelerating aerogel blanket adoption through regulation and industrial modernization. The 2025 update to Green Building Regulations mandates strict thermal transmittance thresholds for new construction, driving use of aerogel-core blankets in facade systems where space efficiency is essential. These codes are catalyzing demand across commercial and residential developments.

Oil and gas modernization remains a powerful driver. ADNOC is deploying aerogel blankets for enhanced oil recovery steam injection lines to minimize heat loss across long desert distances. Strategically, the UAE’s diversification agenda supports advanced materials investment, with the non-oil sector contributing more than 70% of GDP, reinforcing the case for local aerogel-based industrial insulation capabilities.

Country-Level Positioning in the Aerogel Blanket Industry

Aerogel Blanket market County Level Snapshot

|

Country

|

Strategic Focus

|

Market Impact

|

|

United States

|

EV thermal barriers, DAC, aerospace cryogenics

|

High-value innovation and premium demand

|

|

China

|

Scale manufacturing, LNG, EV batteries

|

Volume leadership with standards enforcement

|

|

India

|

Capacity doubling, refining, LNG

|

Rapid domestic adoption and export potential

|

|

Germany

|

Bio-based construction, hydrogen, MRO

|

Sustainability-led premium applications

|

|

South Korea

|

EV safety, electronics miniaturization

|

Advanced battery and device integration

|

|

UAE

|

Green buildings, EOR pipelines

|

Regulation-driven and industrial efficiency growth

|

Aerogel Blanket Market Report Scope

Aerogel Blanket market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$7.6 Billion

|

|

Market Growth Rate

|

17.3%

|

|

Segments

|

By Material Type (Silica Aerogels, Carbon Aerogels, Polymer Aerogels, Bio Based Aerogels), By Form and Processing (Fibrous Reinforced Aerogel Blankets, Composite Aerogel Blankets, Additive Enhanced Aerogel Blankets), By Application (Thermal Insulation, Fire Protection and Passive Fire Protection, Acoustic Insulation, Thermal Barriers for Batteries), By End Use Industry (Oil and Gas, Building and Construction, Automotive and Transportation, Aerospace and Defense, Marine and LNG, Energy Storage Systems)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Aspen Aerogels, Cabot Corporation, Armacell International, BASF, LG Chem, Guangdong Alison Hi Tech, Svenska Aerogel, Aerogel Technologies, JIOS Aerogel, Active Aerogels, Nano Tech, Enersens, Thermablok Aerogels, IBIH Advanced Materials, Hubei Jianghan New Materials

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aerogel Blanket Market Segmentation

By Material Type

- Silica Aerogels

- Carbon Aerogels

- Polymer Aerogels

- Bio Based Aerogels

By Form and Processing

- Fibrous Reinforced Aerogel Blankets

- Composite Aerogel Blankets

- Additive Enhanced Aerogel Blankets

By Application

- Thermal Insulation

- Fire Protection and Passive Fire Protection

- Acoustic Insulation

- Thermal Barriers for Batteries

By End Use Industry

- Oil and Gas

- Building and Construction

- Automotive and Transportation

- Aerospace and Defense

- Marine and LNG

- Energy Storage Systems

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aerogel Blanket Industry

- Aspen Aerogels

- Cabot Corporation

- Armacell International

- BASF

- LG Chem

- Guangdong Alison Hi Tech

- Svenska Aerogel

- Aerogel Technologies

- JIOS Aerogel

- Active Aerogels

- Nano Tech

- Enersens

- Thermablok Aerogels

- IBIH Advanced Materials

- Hubei Jianghan New Materials

*- List not Exhaustive