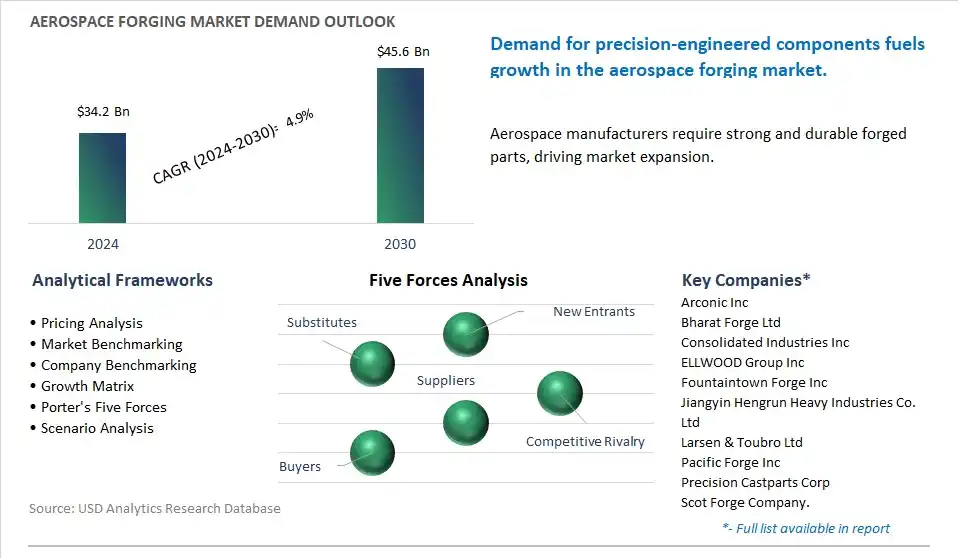

The global Aerospace Forging Market is poised to register a 4.9% CAGR from $34.2 Billion in 2024 to $45.6 Billion in 2030.

The global Aerospace Forging Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Aluminum Alloy, Titanium, Stainless Steel, Others), By Aircraft (Fixed Wing, Rotary Wing), By Application (Rotors, Turbine Disc, Shafts, Fan Case, Others), By End-User (Commercial, Military).

An Introduction to Global Aerospace Forging Market in 2024

The aerospace forging market is witnessing significant growth driven by increasing demand for high-strength, precision-engineered components in aircraft engines, landing gear, and structural assemblies. Key trends shaping the future of the industry include the growing adoption of advanced forging techniques such as closed-die forging, isothermal forging, and superplastic forming to produce complex shapes with tight tolerances and superior mechanical properties. Moreover, there's a rising emphasis on material innovation and alloy development to enhance performance characteristics such as fatigue resistance, corrosion resistance, and temperature stability in demanding aerospace applications. Additionally, advancements in forging equipment, simulation software, and quality control systems are driving innovation and market competitiveness, enabling forging companies to offer reliable, cost-effective, and customized solutions for aerospace OEMs and suppliers in the global aerospace forging market.

Aerospace Forging Market Competitive Landscape

The market report analyses the leading companies in the industry including Arconic Inc, Bharat Forge Ltd, Consolidated Industries Inc, ELLWOOD Group Inc, Fountaintown Forge Inc, Jiangyin Hengrun Heavy Industries Co. Ltd, Larsen & Toubro Ltd, Pacific Forge Inc, Precision Castparts Corp, Scot Forge Company.

Aerospace Forging Market Dynamics

Aerospace Forging Market Trend: Increasing Demand for Lightweight and High-Strength Components

A prominent market trend for aerospace forging is the increasing demand for lightweight and high-strength components. As aircraft manufacturers seek to improve fuel efficiency, reduce emissions, and enhance performance, there's a growing preference for forged components made from advanced materials such as titanium, nickel alloys, and aluminum alloys. Aerospace forging processes, such as closed-die forging and precision forging, enable the production of complex shapes with superior mechanical properties, including high tensile strength, fatigue resistance, and dimensional accuracy. The trend towards lightweight materials and advanced forging techniques reflects the industry's continuous pursuit of weight savings and structural optimization in aircraft design.

Aerospace Forging Market Driver: Growth in Commercial Aircraft Production and Defense Spending

A significant driver for the aerospace forging market is the growth in commercial aircraft production and defense spending worldwide. With increasing air travel demand, fleet expansion plans by airlines, and government investments in military modernization programs, there's a robust demand for forged components for both commercial and military aerospace applications. Aerospace forging manufacturers play a vital role in supplying critical components such as engine shafts, landing gear components, wing ribs, and structural fittings to aircraft OEMs and defense contractors. The steady growth in aircraft deliveries and defense procurement contracts drives market demand for aerospace forging products and services, supporting industry growth and supplier development initiatives.

Aerospace Forging Market Opportunity: Expansion into Additive Manufacturing and Hybrid Processes

An opportunity for the aerospace forging market lies in the expansion into additive manufacturing (AM) and hybrid manufacturing processes. While traditional forging techniques offer advantages in terms of material properties and production scalability, AM technologies such as selective laser melting (SLM) and electron beam melting (EBM) enable the production of complex, near-net shape components with reduced lead times and material waste. Aerospace forging companies can leverage AM technologies to complement existing forging capabilities, offering customers a broader range of manufacturing solutions for customized and low-volume parts. Additionally, the integration of hybrid manufacturing processes, combining forging and AM techniques, presents opportunities to optimize component performance, reduce production costs, and accelerate innovation in the aerospace industry. By embracing additive and hybrid manufacturing, aerospace forging manufacturers can enhance their competitive position, address evolving customer needs, and capitalize on emerging market opportunities.

Aerospace Forging Market Share Analysis: Titanium material segment generated the highest revenue in the industry

The largest segment in the Aerospace Forging Market is the Titanium material segment. This dominance can be attributed to diverse factors. The titanium offers exceptional strength-to-weight ratio, corrosion resistance, and high temperature performance, making it ideal for aerospace applications where lightweight yet durable materials are essential. Aircraft components made from titanium forgings can withstand harsh operating conditions, including high stress, temperature variations, and corrosive environments, ensuring long-term reliability and safety. Additionally, titanium forgings are widely used in critical aerospace components such as landing gear, engine parts, structural components, and fasteners, where high strength, fatigue resistance, and dimensional stability are paramount. In addition, advancements in titanium forging technology, including precision forging processes, advanced metallurgy, and computer-aided design (CAD) software, have improved manufacturing efficiency, product quality, and cost-effectiveness, further driving the adoption of titanium forgings in the aerospace industry. Further, the aerospace industry's increasing demand for lightweight materials to improve fuel efficiency, reduce emissions, and enhance aircraft performance has led to a growing preference for titanium forgings over conventional materials like steel and aluminum alloys. With its superior properties and extensive applications in critical aerospace components, the Titanium material segment remains the largest in the Aerospace Forging Market.

Aerospace Forging Market Share Analysis: Fixed Wing aircraft Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Aerospace Forging Market is the Fixed Wing aircraft category. Diverse factors contribute to this growth. The fixed-wing aircraft, including commercial airliners, business jets, and military planes, constitute a significant portion of the global aerospace industry. These aircraft require a wide range of forged components for their airframes, engines, landing gear, and structural assemblies. With increasing air travel demand, expanding airline fleets, and the introduction of next-generation aircraft models, there is a growing need for forged components to support aircraft production and maintenance activities. Additionally, advancements in aerospace technology, including lightweight materials, advanced manufacturing processes, and innovative design concepts, have led to the development of more fuel-efficient, reliable, and high-performance fixed-wing aircraft. These modern aircraft designs require precision-engineered forged components to meet stringent performance, safety, and regulatory requirements. In addition, the fixed-wing aircraft segment benefits from ongoing investments in aerospace research and development, infrastructure modernization, and defense procurement programs, driving the demand for forged components for new aircraft production and aftermarket services. Further, the increasing emphasis on aircraft sustainability, environmental compliance, and operational efficiency favors the adoption of forged components made from lightweight materials like titanium and composites, further boosting demand in the fixed-wing aircraft segment. With its significant contributions to global air transportation, defense, and economic growth, the Fixed Wing aircraft segment is the fastest-growing segment in the Aerospace Forging Market.

Aerospace Forging Market Share Analysis: Turbine Disc application Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Aerospace Forging Market is the Turbine Disc application category. The rapid growth is driven by turbine discs are critical components in aircraft engines, serving as the primary rotating elements that convert fuel energy into mechanical power to drive the aircraft's propulsion system. As aircraft engine technology continues to advance, there is a growing demand for turbine discs that can withstand higher operating temperatures, pressures, and mechanical loads while maintaining optimal performance and reliability. Additionally, advancements in aerospace materials, such as high-strength alloys and superalloys, have enabled the development of turbine discs with enhanced properties, including superior strength, fatigue resistance, and creep resistance, necessary for demanding aerospace applications. In addition, turbine discs play a crucial role in improving aircraft engine efficiency, fuel economy, and emissions reduction, aligning with industry trends towards sustainability and environmental stewardship. Further, the aerospace industry's focus on lightweighting and optimization drives the demand for forged turbine discs made from advanced materials and manufacturing processes. These turbine discs offer reduced weight, improved aerodynamics, and higher efficiency compared to conventional cast or machined components, contributing to Over the forecast period aircraft performance and operational cost savings. With the increasing demand for turbine discs to support aircraft engine modernization, new aircraft programs, and aftermarket services, the Turbine Disc application segment is the fastest-growing segment in the Aerospace Forging Market.

Aerospace Forging Market Report Segmentation

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Aerospace Forging Companies Profiled in the Market Study

Arconic Inc

Bharat Forge Ltd

Consolidated Industries Inc

ELLWOOD Group Inc

Fountaintown Forge Inc

Jiangyin Hengrun Heavy Industries Co. Ltd

Larsen & Toubro Ltd

Pacific Forge Inc

Precision Castparts Corp

Scot Forge Company.

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Aerospace Forging Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Aerospace Forging Market Size Outlook, $ Million, 2021 to 2030

3.2 Aerospace Forging Market Outlook by Type, $ Million, 2021 to 2030

3.3 Aerospace Forging Market Outlook by Product, $ Million, 2021 to 2030

3.4 Aerospace Forging Market Outlook by Application, $ Million, 2021 to 2030

3.5 Aerospace Forging Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Aerospace Forging Industry

4.2 Key Market Trends in Aerospace Forging Industry

4.3 Potential Opportunities in Aerospace Forging Industry

4.4 Key Challenges in Aerospace Forging Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Aerospace Forging Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Aerospace Forging Market Outlook by Segments

7.1 Aerospace Forging Market Outlook by Segments, $ Million, 2021- 2030

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

8 North America Aerospace Forging Market Analysis and Outlook To 2030

8.1 Introduction to North America Aerospace Forging Markets in 2024

8.2 North America Aerospace Forging Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Aerospace Forging Market size Outlook by Segments, 2021-2030

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

9 Europe Aerospace Forging Market Analysis and Outlook To 2030

9.1 Introduction to Europe Aerospace Forging Markets in 2024

9.2 Europe Aerospace Forging Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Aerospace Forging Market Size Outlook by Segments, 2021-2030

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

10 Asia Pacific Aerospace Forging Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Aerospace Forging Markets in 2024

10.2 Asia Pacific Aerospace Forging Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Aerospace Forging Market size Outlook by Segments, 2021-2030

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

11 South America Aerospace Forging Market Analysis and Outlook To 2030

11.1 Introduction to South America Aerospace Forging Markets in 2024

11.2 South America Aerospace Forging Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Aerospace Forging Market size Outlook by Segments, 2021-2030

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

12 Middle East and Africa Aerospace Forging Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Aerospace Forging Markets in 2024

12.2 Middle East and Africa Aerospace Forging Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Aerospace Forging Market size Outlook by Segments, 2021-2030

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Arconic Inc

Bharat Forge Ltd

Consolidated Industries Inc

ELLWOOD Group Inc

Fountaintown Forge Inc

Jiangyin Hengrun Heavy Industries Co. Ltd

Larsen & Toubro Ltd

Pacific Forge Inc

Precision Castparts Corp

Scot Forge Company.

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Aluminum Alloy

Titanium

Stainless Steel

Others

By Aircraft

Fixed Wing

Rotary Wing

By Application

Rotors

Turbine Disc

Shafts

Fan Case

Others

By End-User

Commercial

Military

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)