Robust Expansion in the Air Purifier Market: Growth, Value, and Outlook

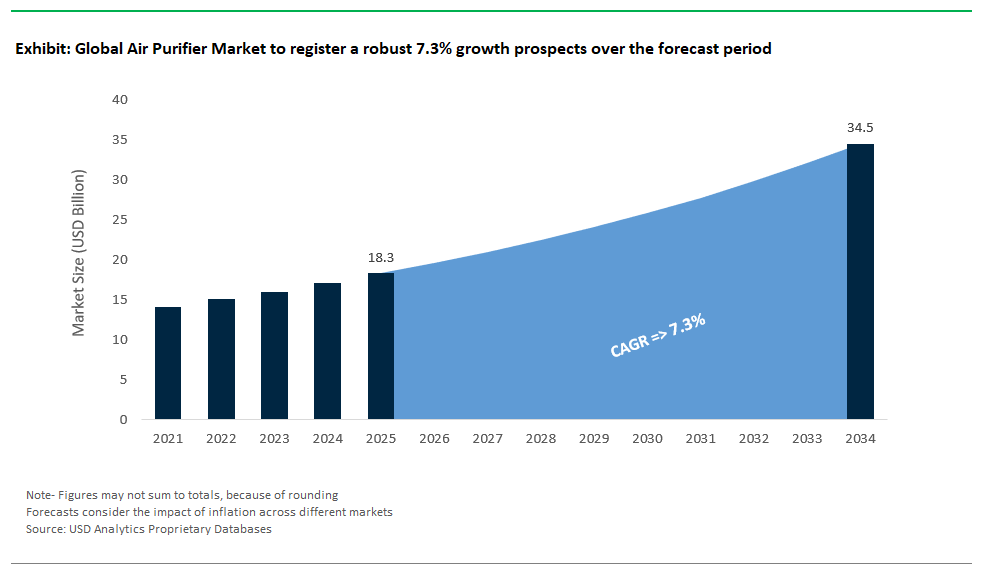

The worldwide Air Purifier Market is gaining strong footprints across developing markets and is estimated to be $18.3 billion in 2025 and is poised to be $34.5 billion by 2034 at a high-growth CAGR from 2018 to 2034 of 7.3%. This strong growth momentum is driven by rising attention to air quality, increasing incidence of respiratory health problems, and rapid urbanization, which drive demand for state-of-the-art indoor air purification technologies across homes, businesses, and industries. The market’s expansion showcases its pivotal role in tackling the problems generated by air pollution, and signals its status as being an integral part of the global wellness and smart home sectors.

With the impact of outdoor and indoor air pollution becoming more prominent, Air Purifier market plays an important role in creating a healthy living and working environment. The previous couple of decades have given rise to a new kind of purifier that employs newfangled technology—HEPA filters, activated carbon, UV-C light, and ionizing systems—to eliminate allergens, particulate matter, volatile organic compounds (VOCs), smoke, bacteria, and viruses. It is also growing across commercial environments like healthcare, schools, buildings and in office buildings, where tough indoor air quality (IAQ) guidelines became the norm. The adoption of smart features like connectivity with Apps, real-time monitoring, and automatic optimization of performance is identified as one of the key trends in the market, which is indicative of the convergence of health technology with IoT-enabled smarter home ecosystem. Asia is still the leading production base and North America and Europe are the key demand markets, particularly with increasing global urbanization and health consciousness.

Innovation, Partnerships, and Expansion Drive the Air Purifier Market Forward

The Air Purifier Market is experiencing an unprecedented wave of innovation and strategic expansion, with leading brands continuously upgrading their portfolios and technologies. In July 2025, Philips launched its 900i smart air purifier in India, offering a compact and energy-efficient device with 3-layer filtration capable of capturing ultra-fine particles, and integrated smart control via mobile app catering to the fast-growing demand for intelligent, connected appliances. In the same month, Dyson unveiled updates to its Cool Gen1 TP10 Air Multiplier, integrating H13 HEPA filtration, 350° airflow, and real-time air quality monitoring for large spaces, reinforcing Dyson’s reputation for high-performance and user-centric design.

The introduction of IQAir’s next-generation XE series in North America spotlighted advanced fan technology that delivers triple the energy efficiency of previous models. In May, Honeywell rolled out its Air Touch P1 air purifier for large rooms, featuring a comprehensive 4-stage filtration system, including a nano-silver antibacterial layer and real-time PM2.5 monitoring a response to growing consumer expectations for visible, data-driven air quality control. LG’s PuriCare AeroFurniture, launched in Singapore in May 2025, illustrates the fusion of functionality and aesthetic design, positioning air purifiers as a seamless part of modern interiors. March saw Camfil debut its Opakfil ES+ V-Bank filter, offering enhanced performance and longevity for commercial HVAC systems, while SOTO PLUS in February 2025 introduced the SOTO-Y6 with UV-PCO sterilization, targeting the increasingly important hygiene market. Coway’s Airmega 100 and Blueair’s ComfortPure 3-in-1 further demonstrate the trend toward affordable, multifunctional, and compact air purification solutions.

The commercial and industrial sectors are also witnessing rapid technological advancement. Cummins’ Retrofit Aftertreatment System (RAS), launched in September 2024, provides efficient emission control for gensets, significantly reducing particulate and gaseous pollutants. Manufacturers are not only prioritizing product innovation but are also expanding partnerships and distribution channels, targeting both established and emerging markets to capture the rising demand for high-performance, scalable air purification systems.

Trends and Opportunities Transforming the Global Air Purifier Industry

Smart Features and IoT Integration Lead Air Purifier Market Innovation

A transformative trend in the Air Purifier Market is the rapid integration of smart features and IoT connectivity, which is redefining user experience and operational efficiency. The proliferation of smart home ecosystems and rising consumer expectations for convenience, data, and control have pushed manufacturers to embed Wi-Fi, real-time air quality sensors, and app-based management into their products. Global search volumes for “Smart WiFi Air Purifiers” soared between January and July 2025, evidencing consumer demand for advanced, automated IAQ solutions. Devices from leading brands like Philips, Dyson, and Coway now offer remote operation, live monitoring of PM2.5 and VOC levels, and automated adaptation based on air quality making proactive air management an attainable reality. Strategic partnerships with smart home platforms and voice assistants (Amazon Alexa, Google Assistant) are ensuring seamless device integration, while manufacturers continue to invest in predictive algorithms and personalized purification routines. This evolution is resulting in a new generation of multi-functional air purifiers combining purification with heating, cooling, and humidity control firmly establishing these devices as core components of connected, healthy living spaces.

Surging Commercial and Industrial Demand Creates High-Value Market Opportunities

The growing focus on indoor air quality in public, commercial, and industrial environments presents a major opportunity for large-scale air purification systems. The post-pandemic era has ushered in heightened health and safety standards for offices, healthcare facilities, schools, and public venues leading to increased investment in robust air filtration and HVAC-compatible solutions. The commercial air filter segment alone was valued at $6.03 billion in 2024, with HEPA filters accounting for $2.1 billion in 2023 due to their dominance in eliminating particulates and allergens. Companies such as Camfil, Honeywell, and Cummins are pioneering commercial-grade filtration, retrofitting systems for enhanced performance, and introducing new solutions like Camfil’s Opakfil ES+ and Cummins’ Retrofit Aftertreatment System. The deployment of custom air purification installations such as Nencki AG’s partnership with Zehnder Clean Air Solutions demonstrates the scale and impact of integrated air quality management. These developments are supported by evolving building codes and government mandates that require compliance with stricter IAQ benchmarks, creating a stable, high-value segment that is fueling continued R&D, strategic alliances, and global market expansion.

Competitive Landscape: Industry Leaders Shaping the Future of Air Purification

The global Air Purifier Market is dominated by established electronics giants and specialized air quality innovators, all pushing the boundaries of technology and market reach.

Dyson Sets the Standard for Premium, Multi-Functional Air Purification

Dyson Ltd. is renowned for design-driven, high-performance air purifiers that often combine heating, cooling, and advanced particle removal in a single device. The July 2025 update of the Cool Gen1 TP10, with H13 HEPA filtration and 350° airflow, underlines Dyson’s commitment to innovation and smart integration. Their August 2024 Purifier Big+Quiet, designed for spaces up to 1,000 sq. ft., demonstrates leadership in both engineering and aesthetics, maintaining Dyson’s reputation for user-centric, feature-rich solutions.

Philips Expands Global Reach with Smart, Health-Focused Air Purifiers

Koninklijke Philips N.V. leverages its health technology leadership to deliver a comprehensive range of air purification products. The July 2025 launch of the 900i Smart Air Purifier in India, with app connectivity and multi-stage filtration, highlights Philips’ strategy of addressing air quality challenges in high-growth regions. Their expansive distribution and ongoing innovation in real-time monitoring cement their position as a go-to brand for both residential and commercial air purification.

Coway Innovates with Advanced Filtration and Adaptive Operation

Coway Co., Ltd. is a front-runner in smart air and water purification, with standout products like the Airmega 100 and 400S offering 360° air intake, multi-stage HEPA filtration, and real-time adaptation to air quality changes. Coway’s focus on affordability, compact design, and user-friendly smart features drives penetration in both homes and small businesses, supported by robust app integration and a growing global footprint.

Honeywell Delivers Reliable, Industrial-Strength Air Quality Solutions

Honeywell International Inc. brings decades of expertise in building technologies to the air purification sector, delivering robust, multi-stage filtration systems suitable for homes, offices, and large-scale industrial facilities. The May 2025 launch of the Air Touch P1, with advanced antibacterial and PM2.5 monitoring features, showcases Honeywell’s dedication to performance, reliability, and smart home integration.

LG Blends Design and Performance with the PuriCare Series

LG Electronics Inc. is recognized for seamlessly integrating advanced technology, design, and smart features in its PuriCare air purifiers. The May 2025 AeroFurniture model, blending 360° HEPA filtration with contemporary aesthetics and Wi-Fi connectivity, positions LG as a premium choice for tech-savvy, design-conscious consumers. The company’s ThinQ platform ensures comprehensive smart home management and continuous innovation in the premium segment.

Air Purifier Market Share Analysis: Technology and Application Insights for 2025

HEPA and Activated Carbon Filters Dominate Technology Mix; Emerging Solutions Gain Traction

HEPA filter technology maintains its dominance in the global air purifier market, securing a 42% share in 2025. Recognized for removing 99.97% of particles larger than 0.3 microns, HEPA filters are the benchmark for residential and sensitive commercial applications particularly in regions battling PM2.5 crises. Activated carbon filters, holding a 25% share, are indispensable for trapping volatile organic compounds (VOCs) and neutralizing odors, and are often paired with HEPA in premium units. UV-C (ultraviolet germicidal irradiation) technology is on the rise in healthcare and public spaces post-pandemic, offering pathogen control and enhanced safety. Ionic filters, though controversial due to ozone generation, are popular in compact, personal devices. Photocatalytic oxidation (PCO) and electrostatic precipitators are gaining attention for their ability to break down chemicals and particulate matter, but market adoption is limited by safety and regulatory scrutiny. Innovations such as multi-stage filtration combining HEPA, carbon, and UV-C are increasingly seen in smart home systems, reflecting evolving consumer expectations for both efficacy and convenience.

.png)

Residential Market Leads Applications, with Commercial and Industrial Demand Accelerating

Residential air purifiers account for 55% of the global market, underpinned by urban air pollution, rising allergy cases, and the smart home revolution. Demand is surging in megacities across APAC, where air quality crises drive adoption in homes, apartments, and even vehicles. Commercial applications including offices, hotels, and schools are expanding rapidly, driven by post-pandemic regulatory requirements for indoor air quality (IAQ), HVAC system integration, and employee/student wellness. Industrial demand, while a smaller share, is propelled by cleanroom standards in pharmaceuticals, electronics, and manufacturing, with electrostatic and advanced HEPA systems prevalent for compliance with OSHA/NIOSH standards. As urbanization, climate change, and public health concerns intensify, the scope for air purification technology will broaden, with growth in both premium and value segments worldwide.

China: The Epicenter of Air Purifier Manufacturing and Urban Adoption

China is the world’s largest air purifier market, driven by severe outdoor and indoor pollution in urban centers. Massive investments in manufacturing capacity and smart home technology underpin market leadership. The Chinese government has implemented stringent air quality regulations and public campaigns, fueling rapid market expansion in both residential and commercial segments. Domestic brands innovate aggressively, integrating advanced HEPA, activated carbon, and UV-C solutions, and are increasingly exporting smart purifiers worldwide. Notably, new launches like SOTO PLUS’s SOTO-Y6 (February 2025) showcase the integration of multiple filtration technologies and real-time air quality sensors, appealing to health-conscious, tech-savvy consumers. As awareness and regulation continue to tighten, China’s role as both a manufacturer and end-user will shape global trends.

China’s air purifier landscape is also characterized by growing demand in schools, hospitals, and offices, supported by government investment and evolving health standards. The combination of policy intervention, consumer awareness, and product innovation ensures that China remains a dominant force in shaping the future of air purification technologies globally.

United States: R&D Powerhouse and Smart Purification Pioneer

The United States stands out for technological innovation in air purification, with leading companies investing heavily in advanced filtration, energy efficiency, and smart home integration. EPA guidelines and rising concerns over wildfires, allergens, and climate-driven air quality issues are major market catalysts. Demand is high from residential users, especially in wildfire-prone states and allergy hotspots. Commercial and healthcare adoption is also strong, with hospitals and offices seeking to meet higher IAQ standards. Recent product launches such as IQAir’s XE series (June 2025) highlight trends toward energy efficiency and custom solutions for various room sizes and pollutant profiles.

Regulations on performance, safety, and transparency (like CADR ratings) are strengthening, fostering a more educated and discerning consumer base. The US air purifier market is further supported by growing online sales and partnerships with home automation ecosystems (e.g., Alexa, Google Home). Strategic investments in both manufacturing and R&D reinforce the country’s global leadership in both market share and innovation.

India: Rapid Urbanization and Air Quality Crisis Drive Adoption

India faces some of the world’s worst air pollution, especially in urban areas such as Delhi and Mumbai. This has triggered an exponential surge in air purifier demand across residential and, increasingly, commercial spaces. The National Clean Air Programme (NCAP) and similar initiatives aim to reduce PM10 and PM2.5 levels, indirectly driving air purifier adoption as public awareness grows. Manufacturers are launching models tailored to Indian needs robust HEPA and activated carbon filters to handle extreme particulate and odor loads, alongside features like anti-bacterial pre-filters and real-time monitoring. The July 2025 launch of Philips’ 900i Smart Air Purifier, specifically designed for India, exemplifies this focus.

Despite evolving direct regulation on IAQ appliances, severe pollution ensures strong market growth. Expansion of domestic manufacturing and assembly, coupled with a tech-savvy urban population, positions India as one of the fastest-growing air purifier markets globally.

South Korea: Design Innovation and Premium Penetration

South Korea is at the forefront of air purifier technology, blending advanced filtration with design aesthetics and smart features. Companies such as Coway and LG lead in R&D investment, pioneering AI-powered sensors, 360° air intake, and low-noise, energy-efficient models. Penetration is especially high in residential markets, where health consciousness drives demand for premium products. Government campaigns and national standards for air purifier performance support innovation and adoption.

The market is also evolving with multi-functional purifiers that integrate humidification, dehumidification, and air quality analytics. Innovations like LG’s PuriCare AeroFurniture Air Purifier (May 2025) showcase how South Korean brands combine lifestyle and health technology. Strong export capability makes South Korea a hub for next-generation air purification solutions globally.

Germany: Energy-Efficient and Sustainable Air Purification Solutions

Germany leads Europe in energy-efficient and sustainable air purification. Manufacturers invest heavily in advanced filtration media, sensor arrays, and smart systems that offer both performance and low environmental impact. Strict EU regulations on appliance energy use and waste reduction influence product design, while public health campaigns increase residential and commercial demand for air purifiers. The focus is on allergen removal, high CADR ratings, and integration with smart home platforms.

German brands emphasize product durability, low-noise operation, and robust air quality monitoring. The push for green and circular economy principles also spurs the development of recyclable components and eco-friendly materials, making Germany a reference point for sustainable air purification technology.

Japan: Compact, Quiet, and Multi-Functional Air Purifiers

Japan’s air purifier market is characterized by compact, ultra-quiet, and highly efficient devices, led by brands such as Sharp and Panasonic. Technologies like Plasmacluster Ion and advanced HEPA integration address both allergens and airborne viruses, appealing to consumers in densely populated cities. Multi-functionality combining air purification with humidification or dehumidification is a hallmark of Japanese innovation.

Government-led health campaigns and stringent regulatory standards for performance ensure widespread adoption in homes, offices, and healthcare facilities. Investment in manufacturing and continuous technological upgrades enable Japanese brands to remain at the cutting edge of global air purification markets.

Canada: Growing Demand from Climate and Health Concerns

Canada’s air purifier market is expanding rapidly, fueled by increased wildfire smoke events, rising pollen/allergy cases, and greater public awareness of indoor air quality. Residential adoption is strongest in regions impacted by smoke and seasonal pollutants, while commercial uptake grows in offices, schools, and public spaces. R&D is focused on enhancing HEPA and activated carbon filtration, optimizing devices for Canadian environmental challenges. IQAir’s XE launch in June 2025 is a recent example of innovative solutions impacting the market.

Compliance with North American safety standards and consumer demand for smart, data-driven air purifiers support ongoing growth. The trend towards smart features and mobile integration mirrors broader North American market dynamics.

United Kingdom: Urbanization and Health Awareness Drive Market Growth

The UK is a key European market for air purifiers, shaped by urbanization, rising allergy and asthma cases, and strong public health messaging. Brands like Dyson leverage local R&D to deliver stylish, energy-efficient, and multi-functional air purifiers. Government initiatives highlight indoor air quality, supporting residential and commercial demand. Urban households, offices, and educational institutions are major adopters, especially in cities with air quality concerns.

Innovation focuses on integrating air purifiers with smart home ecosystems, improving energy efficiency, and delivering advanced filtration for allergens, PM2.5, and VOCs. UK and EU regulatory frameworks drive manufacturers toward higher safety and environmental standards.

Air Purifier Market Report Scope

Air Purifier Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.3 Billion

|

|

Market Size (2034)

|

$34.5 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Technology (HEPA Filter, Activated Carbon Filter, Ionic Filter, UV-C (Ultraviolet Germicidal Irradiation), Photocatalytic Oxidation (PCO), Electrostatic Precipitators, Others)

By Product Type (Standalone/Portable Air Purifiers, In-duct/Fixed Air Purifiers)

By Application (Residential, Commercial (Offices, Healthcare Facilities, Hospitality, Educational Institutions, Retail, etc.), Industrial (Manufacturing, Power Generation, Chemical Processing, etc.))

By End-Use Vertical (Healthcare, Building & Construction, Automotive, Manufacturing, Food & Beverage, Electronics, Others)

By Distribution Channel (Online (E-commerce Websites, Company Websites), Offline (Specialty Stores, Hypermarkets/Supermarkets, Department Stores, Direct Sales)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dyson Ltd., Koninklijke Philips N.V., Coway Co., Ltd., Honeywell International Inc., LG Electronics Inc., Blueair (a Unilever brand), IQAir AG, Sharp Corporation, Panasonic Corporation, Daikin Industries, Ltd., Xiaomi Corporation, Carrier Global Corporation, Camfil AB, Samsung Electronics Co., Ltd., Eureka Forbes Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Air Purifier Market Segmentation

By Technology

- HEPA Filter

- Activated Carbon Filter

- Ionic Filter

- UV-C (Ultraviolet Germicidal Irradiation)

- Photocatalytic Oxidation (PCO)

- Electrostatic Precipitators

- Others

By Product Type

- Standalone/Portable Air Purifiers

- In-duct/Fixed Air Purifiers

By Application

- Residential

- Commercial (Offices, Healthcare Facilities, Hospitality, Educational Institutions, Retail, etc.)

- Industrial (Manufacturing, Power Generation, Chemical Processing, etc.)

By End-Use Vertical

- Healthcare

- Building & Construction

- Automotive

- Manufacturing

- Food & Beverage

- Electronics

- Others

By Distribution Channel

- Online (E-commerce Websites, Company Websites)

- Offline (Specialty Stores, Hypermarkets/Supermarkets, Department Stores, Direct Sales)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Air Purifier Market

- Dyson Ltd.

- Koninklijke Philips N.V.

- Coway Co., Ltd.

- Honeywell International Inc.

- LG Electronics Inc.

- Blueair (a Unilever brand)

- IQAir AG

- Sharp Corporation

- Panasonic Corporation

- Daikin Industries, Ltd.

- Xiaomi Corporation

- Carrier Global Corporation

- Camfil AB

- Samsung Electronics Co., Ltd.

- Eureka Forbes Ltd.

* List Not Exhaustive

Research Coverage

This USDAnalytics report investigates the dynamic, innovation-driven air purifier market reviewing technology breakthroughs, application trends, and regulatory impacts. The analysis covers detailed segmentation by technology, product type, application, end-use vertical, and distribution channel. It highlights drivers such as urban air pollution, pandemic-driven IAQ regulation, smart home integration, and green technology adoption. Covering historic data (2021–2024) and forecasts (2025–2034), this report is an essential resource for appliance manufacturers, investors, HVAC companies, and policymakers seeking a complete view of the air purifier industry.

Segmentation:

By Technology: HEPA Filter, Activated Carbon Filter, Ionic Filter, UV-C, PCO, Electrostatic Precipitators, Others

By Product Type: Standalone/Portable, In-duct/Fixed Air Purifiers

By Application: Residential, Commercial, Industrial

By End-Use Vertical: Healthcare, Building & Construction, Automotive, Manufacturing, Food & Beverage, Electronics, Others

By Distribution Channel: Online (E-commerce, Company Websites), Offline (Specialty Stores, Hypermarkets, Direct Sales)

Geographic Scope: 25+ countries across North America, Europe, Asia Pacific, South America, Middle East & Africa

Historic Data: 2021–2024 and Forecast Data: 2025–2034

Companies Covered: Dyson, Philips, Coway, Honeywell, LG, Blueair, IQAir, Sharp, Panasonic, Daikin, Xiaomi, Carrier, Camfil, Samsung, Eureka Forbes

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.