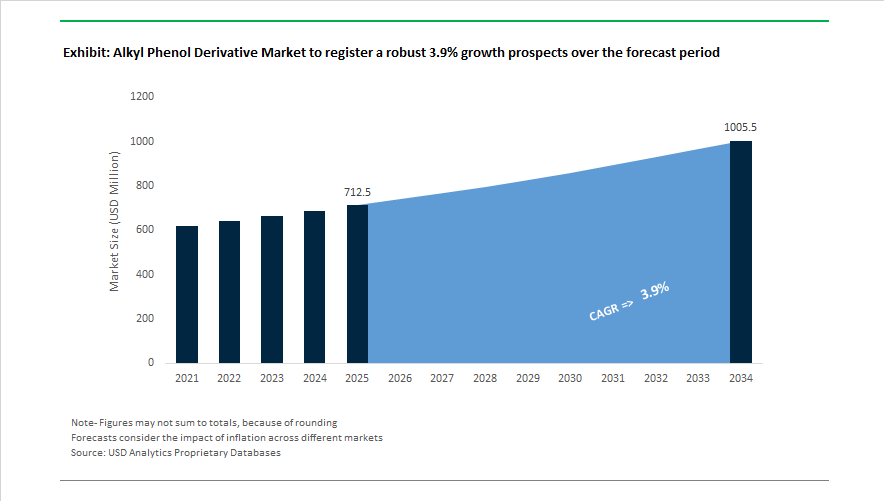

Market Overview: Alkyl Phenol Derivative Market to Reach $1,005.4 Million by 2034 as Value Chain Realignment, Resin Demand, and Green Chemistry Regulations Reshape Industry

The global alkyl phenol derivative market is projected to grow from $712.5 Million in 2025 to $1,005.4 Million by 2034, registering a 3.9% CAGR supported by sustained demand across epoxy resins, polymer stabilizers, antioxidants, lubricant additives, surfactants, and industrial coatings intermediates. Alkyl phenol derivatives remain critical building blocks for phenolic resins, fuel additives, plastic antioxidants, rubber processing chemicals, and specialty solvents, particularly in automotive, electronics, construction, and petrochemical sectors. Market dynamics are being influenced by feedstock integration, cost optimization strategies, and tightening environmental regulations targeting nonylphenol ethoxylates (NPEs). Producers are restructuring manufacturing footprints while investing in nitration, hydrogenation, and advanced downstream chemistries to maintain supply resilience and margin stability.

Industry restructuring began in August 2024 when Deepak Nitrite earmarked ₹2,000 crore for expansion in nitration, hydrogenation, and specialty phenol derivatives. In September 2024, SI Group announced closure of its Singapore alkylphenol plant by late 2025, shifting supply to Europe and the Americas, while strengthening its regional presence through partnership with Liaoning Dingjide Chemical during 2024–2025. In July 2025, DIC Corporation committed to building a new epoxy resin facility in Chiba, a major downstream outlet for alkyl phenol feedstocks. Regulatory momentum intensified in late 2025 as US EPA and ECHA advanced guidance on phasing out NPEs, accelerating transition toward bio-based surfactants. In August 2025, SABIC confirmed progress on the Fujian Petrochemical Complex, strengthening integrated phenol and olefin supply in Asia.

Capacity expansion and operational realignment accelerated through November 2025. Prasol Chemicals announced expansion plans and IPO filing to scale alkyl phenol intermediates, while SONGWON Industrial Group revealed greenfield investment in Saudi Arabia for polymer stabilizer systems. SONGWON’s Q3 2025 results highlighted stable lubricant additive demand despite European energy cost pressures. Organizational transformation followed as DIC introduced its Global Operating Model effective January 2026, supported by its Asia Pacific "mother plant" manufacturing framework initiated in 2025. In January 2026, Deepak Nitrite commissioned a Dahej facility focused on nitration and hydrogenation intermediates, reinforcing India’s role in specialty alkyl phenol production. These developments indicate a market transitioning toward integrated production networks, regulatory-compliant chemistries, and higher-value downstream applications across global specialty chemical value chains.

Strategic Market Trends and High-Value Opportunities Reshaping the Alkyl Phenol Derivative Market

Market Trend: Global Elimination of NPEs Resets Demand Toward Compliant, Biodegradable Alkyl Phenol Alternatives

One major transformation is the accelerated removal of Nonylphenol Ethoxylates (NPEs) across textile, home-care, and industrial cleaning supply chains. While the regulatory phase-out began several years ago, 2024–2025 marks the period when compliance became global, enforceable, and commercially binding. EU REACH now enforces a 0.01% allowable limit on NPEs in imported textiles, preventing an estimated 15 tonnes of NP emissions into EU rivers and lakes each year, primarily through laundering runoff. This enforcement has elevated environmental compliance from a voluntary sustainability measure to a mandatory import-qualification threshold, particularly impacting exporters from Bangladesh, China, Türkiye, and Vietnam.

The ZDHC MRSL V3.1 (2025) maintains NP/NPEs on its restricted list, and now over 30 multinational brands require MRSL Level 3 certification for all textile chemical inputs. This effectively eliminates NPE use across Tier-2 and Tier-3 suppliers. Additionally, heightened border testing in 2025 using HPLC-MS screening is creating real-time compliance risk for exporters, turning NPE-free formulations into a commercial passport for textile chemical suppliers. As global retailers and apparel conglomerates extend their zero-discharge audits deeper into supply networks, compliant alkyl phenol derivatives—particularly linear alcohol ethoxylates and new NP-free stabilizers—are gaining accelerated adoption.

Market Trend: High-Purity Alkyl Phenols Gain Strategic Importance in Advanced Materials and Electronics

A second structural trend is the growing prioritization of ultra-pure alkyl phenols used as feedstock for high-performance polymers and dielectric substrates. Instead of pursuing traditional volume growth, leading producers are strategically exiting commodity production to strengthen their position in electronics-grade and aerospace-grade phenolic intermediates. SABIC’s December 2025 expansion of Polyphenylene Ether (PPE) oligomer capacity exemplifies this shift. The new production stream is specifically designed to supply bi-functional PPE oligomers for high-speed AI server printed circuit boards and 5G base-station hardware. These substrates require exceptional dielectric strength, thermal stability, and flame resistance—properties derived directly from high-purity phenolic precursors.

At the same time, SI Group’s closure of its Jurong Island alkyl phenol facility signals broader geographic consolidation, refocusing production into Europe and North America where margins favor specialty additives and purified intermediates. Regulatory scrutiny is reinforcing this pivot. At K-2025, SI Group showcased Weston 705, a Nonylphenol-free phosphite antioxidant approved for food contact in more than 50 countries—positioning the product as a regulatory-safe upgrade to older alkyl phenol stabilizers increasingly flagged for endocrine disruption concerns.

Market Opportunity: Alkyl Phenol-Derived Phenolic Binders for Electric Vehicle Braking Systems

Electric Vehicles (EVs) are creating new material-science challenges for brake systems. Regenerative braking significantly reduces mechanical pad usage, causing low-use corrosion, oxidation, and particulate formation under moisture-rich environments. The Euro 7 regulatory standard, adopted in March 2024 and entering application in 2025, is the first legislation to mandate brake dust emissions limits (PM10), making friction-material chemistry a compliance-driven growth category.

Cresol-modified phenolic resins, cashew-nut-shell-liquid (CNSL) phenolics, and alkylated phenol mixes are emerging as the essential binders that protect pad integrity, maintain friction coefficients, and prevent resin bleed-out during corrosive idle cycles. Cardolite’s 2025 demonstrations showed CNSL-modified phenolics offer superior impact resistance and flexibility versus conventional phenolic binders, making them suitable for both EV platforms and high-load rail brake systems. Adhesion performance is becoming especially critical. EV brake pads remain idle for long durations, requiring reactive softeners within phenolic networks—such as cardanol/cardol derivatives—to maintain bonding strength across temperature and humidity variations. These engineered resins represent a high-margin, formulation-locked niche where suppliers can secure multi-year OEM contracts.

Market Opportunity: Scaling Bio-Based Alkyl Phenols Through Lignin Depolymerization and RCF Technologies

The drive toward green chemistry is opening a second major growth avenue: renewable phenolic building blocks produced through lignin valorization. Advancements in Reductive Catalytic Fractionation (RCF) are converting wood-derived lignin into simple aromatic molecules like bio-cresols and bio-xylenols, which serve as drop-in substitutes for petroleum-derived phenols used in adhesives, insulation binders, composites, and coatings.

Stora Enso’s NeoLigno bio-based binder, integrated into thermal insulation products in July 2025, demonstrates successful commercial deployment at scale. The binder eliminates formaldehyde exposure, enabling compliance with stricter 2026 EU formaldehyde-emission legislation while providing a 40% carbon-footprint reduction versus phenol-formaldehyde resins. Stora Enso’s €1.1 billion renewable-packaging hub investment, inaugurated August 2025, allocates dedicated resources to lignin-based chemical precursor development for automotive and aerospace supply chains.

As bio-aromatics move from pilot to scaled production, the Alkyl Phenol Derivative Market will see portfolio bifurcation: legacy petro-phenols concentrated in low-margin applications and renewable high-purity phenolics capturing premium pricing in automotive, electronics, and engineered materials.

Alkyl Phenol Derivative Market Share and Segmentation Insights

Market Share by Derivative Type: Phenolic Resins Anchor Volume as Amines Deliver Growth

Phenolic resins account for approximately 42% of the alkyl phenol derivative market in 2025, making them the most defensible segment. These polymerized nonylphenol and octylphenol formaldehyde resins are critical in tire rubber tackifiers, food-can varnishes, and high-heat electrical laminates, where technical substitution remains difficult and regulatory exposure is lower than for monomeric alkylphenols. Alkyl phenol ethoxylates rank second but are in structural decline in Europe and North America due to REACH and EPA restrictions, with Asia-Pacific now the primary remaining growth region. Alkyl phenol phosphites represent a stable, high-value antioxidant segment, widely used to protect polyolefins and styrenics during processing, with growing migration toward polymer-bound alternatives. Alkyl phenol amines are the smallest yet fastest-growing category, driven by corrosion inhibitor demand in lubricants, fuel additives, and recovering aerospace and industrial manufacturing.

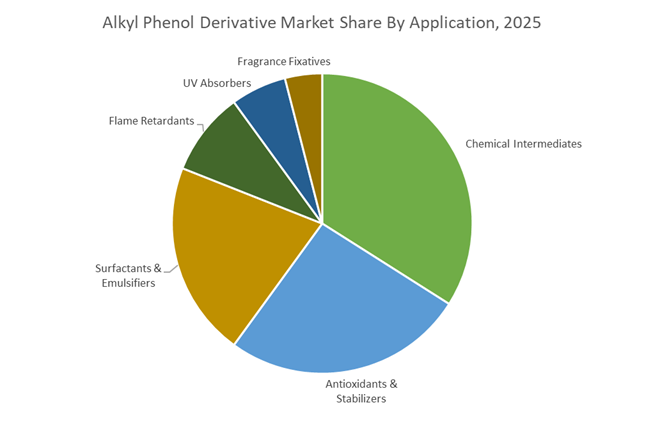

Market Share by Application: Chemical Intermediates Lead While Stabilizers Gain from Recycling

Chemical intermediates represent roughly 34% of alkyl phenol derivative consumption in 2025, dominated by captive use for producing phenolic resins, phosphites, and amines. Merchant sales continue to decline in regulated regions but remain resilient across India, Southeast Asia, and Latin America. Antioxidants and stabilizers rank second and deliver the highest value per kilogram, supporting polymer processing and service life, with demand rising as recycled plastics require additional stabilization against prior thermal degradation. Surfactants and emulsifiers show the steepest contraction, in developed markets, following widespread APEO phase-outs under Zero Discharge of Hazardous Chemicals commitments. Flame retardants form a flat niche as brominated alkylphenol systems face substitution by phosphorus-based chemistries. UV absorbers remain specialized and stable, while fragrance fixatives are the smallest segment, with synthetic musk usage largely eliminated in Europe and North America and confined to low-cost emerging markets.

Competitive Landscape: Sustainable Phenolic Stabilizers and Circular Polymer Integration Reshaping the Alkyl Phenol Derivative Market

The Alkyl Phenol Derivative Market is evolving under regulatory scrutiny, circular economy mandates, and accelerating demand from EVs, high-performance lubricants, polymer stabilizers, and specialty resins. Competitive leadership now hinges on feedstock integration, carbon-efficient phenol production, bio-renewable alternatives, and high-purity intermediates for antioxidants and epoxy systems. Leading producers are strengthening APAC presence, investing in climate-neutral manufacturing, and developing next-generation phenolic stabilizers that protect polymers in high-heat and recycled environments.

SI Group recapitalizes to accelerate EV-focused phenolic stabilizer innovation

SI Group has re-emerged as a financially strengthened performance additives leader after completing a comprehensive recapitalization in December 2025, reducing net debt by over 80%. This restructuring enhances capital flexibility to expand across rubber, plastics, and lubricant sectors. The company operates 18 manufacturing facilities globally under a unified operating platform, ensuring synchronized antioxidant and intermediate supply. In 2025, SI Group opened a new Innovation Center focused on alkyl phenol-based stabilizers designed to prevent thermal degradation in EV battery housings. Strategically, the company is positioning itself as a sustainable additive powerhouse, with a strong emphasis on APAC growth and polymer innovation showcases.

BASF SE advances circular phenol derivatives through Verbund efficiency

BASF leverages its integrated Verbund sites to manufacture alkyl phenol derivatives with industry-leading carbon efficiency. Under its circular economy transition strategy, BASF committed up to €1 billion toward climate-neutral technologies by 2025. The company is scaling bio-based surfactants derived from alkyl phenol alternatives to align with European regulatory pressures for safer detergents and wetting agents. Deep vertical integration into ethylene and phenol feedstocks enables high-purity p-tert-butylphenol production for low-emission resins. BASF’s phenolic antioxidants and stabilizers are increasingly tailored to automotive and EV applications, supporting rapid electrification-driven polymer demand.

SABIC strengthens phenolic value chain through Aramco integration and TRUCIRCLE™

SABIC capitalizes on its partnership with Saudi Aramco to dominate the alkyl phenol value chain through secure feedstock access and large-scale petrochemical integration. Its BLUEHERO™ initiative, launched in 2025–2026, applies phenolic materials to enhance EV battery safety and thermal management. Through its TRUCIRCLE™ portfolio, SABIC integrates certified bio-renewable and circular feedstocks into polycarbonate and epoxy intermediates. Ongoing synergy targets of up to $1.8 billion annually by 2025 support capacity expansion and downstream OEM relationships, reinforcing SABIC’s global presence in high-performance phenolic intermediates.

Sasol Limited balances synthetic and natural phenol derivatives with mobility-driven focus

Sasol operates a dual-track platform combining synthetic and natural alcohol derivatives within its International Chemicals division. In late 2025, Sasol reported a fatality-free financial year in mining operations, reinforcing operational reliability for industrial clients. The company is optimizing its portfolio toward higher-margin mobility and commercial applications, targeting improved EBITDA performance through 2026. Sasol supplies specialized alkylates for lubricants, detergents, and oilfield chemicals, leveraging internalized supply chains to mitigate tariff volatility. Its high-purity alcohol and phenol derivatives support industrial surfactants and extreme-pressure lubricant systems.

Dover Chemical Corporation expands recycled polymer stabilization with DoverCycle™ platform

Dover Chemical focuses on niche, high-performance polymer additives with advanced automation at its Ohio and Indiana facilities. In September 2025, Dover expanded its Doverphos® LGP-11/12 platform with DoverCycle™, specifically engineered to stabilize recycled polyolefins. The company produces consistent para- and di-nonylphenol and cumylphenol derivatives for demanding antioxidant applications. As a Responsible Care member under the American Chemistry Council, Dover integrates environmental stewardship into its manufacturing processes. Its alkyl phenol derivatives are widely used in metalworking fluids and drilling muds where oxidative and thermal stability under pressure are critical.

SONGWON Industrial Group enhances polymer longevity with smart phenolic antioxidants

SONGWON Industrial Group is a global leader in plastic additives, delivering solution-driven phenolic antioxidants under its SONGNOX® brand. In 2025, the company intensified development of Smart Additives to extend the life cycle of plastics used in infrastructure and heavy machinery. Expansion across EMEA distribution networks during 2025–2026 improves supply reliability for phenolic stabilizers. Strategically, SONGWON is reinforcing its Asia-Pacific footprint, particularly in electronics and consumer goods requiring low-color, low-odor alkyl phenol derivatives. Its antioxidants protect polymers during high-temperature processing and long-term service, supporting durability in advanced resin systems.

United States Alkyl Phenol Derivative Market: Reshoring Incentives and Application-Led Reformulation

The United States is prioritizing domestic resilience in alkyl phenol derivatives through fiscal incentives and targeted innovation. Federal reshoring initiatives are supporting expansions in high-purity octylphenol and nonylphenol output to secure supply for automotive lightweighting and aerospace-grade materials. At the formulation level, U.S. producers introduced new alkyl phenol-based antioxidants in mid-2025 designed to stabilize next-generation hydrofluoroolefin blowing agents and refrigerants, aligning with low global warming potential requirements.

Regulatory scrutiny is sharpening differentiation. The U.S. Environmental Protection Agency initiated a review of selected alkyl phenol ethoxylates in late 2025, accelerating a shift toward branched derivatives with improved biodegradation profiles. In parallel, Huntsman Corporation launched an advanced Bisphenol A alternative in November 2024, engineered for enhanced thermal stability and reduced environmental footprint in automotive and electronics. Pricing dynamics also influenced contracts in 2025 as Gulf Coast reports cited a short-term uptick tied to benzene tightness and energy costs. Downstream, U.S. construction materials are adopting alkyl phenol-enhanced phenolic resins with ultra-low formaldehyde emissions to meet indoor air quality expectations.

India Alkyl Phenol Derivative Market: Capacity Build-Out and Export-Oriented Specialty Surfactants

India is consolidating its position as a specialty manufacturing hub for alkyl phenol derivatives through capacity additions and policy streamlining. In May 2025, Deepak Nitrite announced a $30 million expansion to raise domestic alkyl phenol output, directly addressing import dependence while serving agrochemical and pharmaceutical clusters. Policy liberalization followed in November 2025 when the Ministry of Chemicals and Fertilizers rescinded several Quality Control Orders, easing access to intermediates for additive manufacturers.

Export momentum is anchored in agrochemicals. India has emerged as a key supplier of alkyl phenol-derived emulsifiers for crop protection, supported by government programs under Make in India that target Southeast Asian markets. Feedstock security is also improving as Haldia Petrochemicals Ltd. executed a licensing agreement with Lummus Technology to expand phenol capacity at its West Bengal complex by 2026. At the specialty end, producers in the Gujarat corridor are prioritizing p-tert-butylphenol for fragrance intermediates and pharmaceutical-grade resins, reflecting a move toward higher value derivatives.

China Alkyl Phenol Derivative Market: Feedstock Integration and Standards-Driven Upgrading

China’s alkyl phenol derivative sector is being recalibrated by mandatory standards and upstream integration. The State Administration for Market Regulation issued GB 30981.2-2025 in late 2025, imposing stricter volatile organic compound limits on coatings and adhesives formulated with alkyl phenol derivatives. Compliance with these thresholds is pushing formulators toward cleaner synthesis routes and refined product grades.

Supply security is improving through integrated refining. Sinopec completed the mechanical phase of its Zhenhai integrated project in 2025, lifting domestic availability of phenol and propylene for downstream alkylation. Logistics governance also tightened as updated ocean shipping protocols were introduced in 2025 to enhance maritime safety for liquid derivatives. Demand from electronics is rising in parallel, with domestic wafer fabrication expanding the use of ultra-high-purity alkyl phenol resins in photoresist systems. Energy efficiency is another lever, as Chinese producers adopt catalytic distillation technologies that reduce alkylation energy consumption versus legacy units.

Germany Alkyl Phenol Derivative Market: Bio-Based Pathways and REACH-Driven Substitution

Germany is steering Europe’s transition toward safer and lower-impact alkyl phenol derivatives. In January 2025, BASF unveiled a bio-based phenol derivative process that materially reduces carbon emissions and water intensity, aligning with Net Zero industrial targets. This innovation supports downstream users seeking verified low-impact inputs for lubricants, coatings, and engineered materials.

Regulatory pressure is accelerating substitution. German manufacturers are leading the phase-out of conventional nonylphenol ethoxylates in favor of alcohol-based surfactants and modified alkyl phenol derivatives with improved eco-toxicological profiles. EU REACH requirements in 2025 have further encouraged the adoption of long-chain alkyl phenols as safer alternatives in lubricant additive packages. Strategically, BASF’s announced plan to IPO its specialized agricultural and industrial solutions segments underscores the importance of alkyl phenol-based passive fire protection materials and specialty resins within focused growth platforms.

South Korea Alkyl Phenol Derivative Market: Automotive Materials and Export-Focused Consistency

South Korea is aligning alkyl phenol derivative development with advanced mobility and export reliability. LG Chem highlighted a strategic pivot in late 2025 toward bio-synthesized resins derived from phenolic chemistry, targeting electric vehicle battery housings that demand heat resistance and dimensional stability. This approach links alkyl phenol derivatives to next-generation materials platforms.

Regional consolidation has sharpened R&D focus. Following INEOS Phenol’s acquisition of Mitsui Phenol Singapore, South Korean producers such as Kumho P&B Chemicals intensified development of Bisphenol A and high-performance phenolic adhesives. Export channels strengthened in 2025 as shipments of para-octylphenol to North American rubber processors reached record levels, supported by preferential trade frameworks and tight quality control.

Strategic Positioning by Country in Alkyl Phenol Derivatives

Alkyl Phenol Derivative Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Industry Implication

|

|

United States

|

Reshoring incentives and low-impact reformulation

|

Secure supply with compliance-ready antioxidants and resins

|

|

India

|

Capacity expansion and agrochemical exports

|

Scale-up of specialty surfactants and pharma-grade derivatives

|

|

China

|

Integrated feedstocks and mandatory standards

|

Cleaner production with electronics-driven purity upgrades

|

|

Germany

|

Bio-based processes and REACH substitution

|

Transition to safer, lower-carbon alkyl phenol pathways

|

|

South Korea

|

EV materials and export consistency

|

High-performance phenolics linked to mobility and rubber

|

Alkyl Phenol Derivative Market Report Scope

Alkyl Phenol Derivative Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$712.5 Million

|

|

Market Size (2034)

|

$1005.4 Million

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Product Type (Nonylphenol, Octylphenol, Para tert Butylphenol, Dodecylphenol, Di tert Butylphenols), By Derivative Type (Alkyl Phenol Ethoxylates, Phenolic Resins, Alkyl Phenol Phosphites, Alkyl Phenol Amines), By Application (Antioxidants and Stabilizers, Surfactants and Emulsifiers, UV Absorbers, Flame Retardants, Chemical Intermediates, Fragrance Fixatives), By End Use Industry (Automotive and Aerospace, Construction, Agriculture, Consumer Goods, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, INEOS Phenol, SABIC, Shell plc, Solvay SA, Deepak Nitrite Limited, LG Chem Ltd, Mitsui Chemicals Inc, Kumho P and B Chemicals, Formosa Chemicals and Fibre Corporation, Sinopec Group, Dow Inc, Huntsman Corporation, SI Group, Aditya Birla Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Alkyl Phenol Derivative Market Segmentation

By Product Type

- Nonylphenol

- Octylphenol

- Para tert Butylphenol

- Dodecylphenol

- Di tert Butylphenols

By Derivative Type

- Alkyl Phenol Ethoxylates

- Phenolic Resins

- Alkyl Phenol Phosphites

- Alkyl Phenol Amines

By Application

- Antioxidants and Stabilizers

- Surfactants and Emulsifiers

- UV Absorbers

- Flame Retardants

- Chemical Intermediates

- Fragrance Fixatives

By End Use Industry

- Automotive and Aerospace

- Construction

- Agriculture

- Consumer Goods

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Alkyl Phenol Derivative Industry

- BASF SE

- INEOS Phenol

- SABIC

- Shell plc

- Solvay SA

- Deepak Nitrite Limited

- LG Chem Ltd

- Mitsui Chemicals Inc

- Kumho P and B Chemicals

- Formosa Chemicals and Fibre Corporation

- Sinopec Group

- Dow Inc

- Huntsman Corporation

- SI Group

- Aditya Birla Chemicals

*- List not Exhaustive