Aluminum Foil Packaging Market Overview: Market Size, Growth, and Key Insights

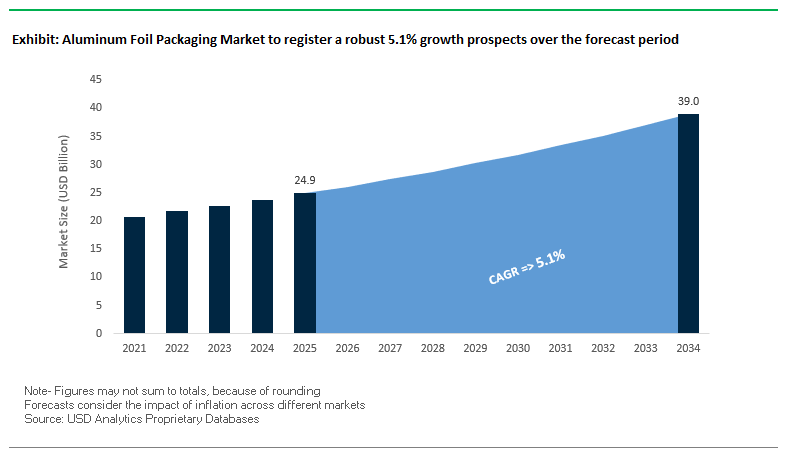

The Global Aluminum Foil Packaging Market is projected to reach $24.9 billion in 2025 and expand to $39 billion by 2034, growing at a CAGR of 5.1%. Aluminum foil continues to gain traction as one of the most versatile and sustainable packaging materials, providing unmatched barrier properties against oxygen, light, moisture, and bacteria. With just a 6-micron layer, it delivers complete product protection, extending shelf life across industries such as food, pharmaceuticals, and cosmetics.

Sustainability remains a defining driver. Approximately 75% of all aluminum ever produced is still in circulation, reflecting its infinite recyclability and strong role in the circular economy. At the same time, pharmaceutical applications remain critical, with blister packs ensuring tamper-evident, hygienic storage of medicines. In addition, aluminum foil’s ability to form laminates with paper and plastics enhances flexibility, printability, and durability, supporting diverse consumer and industrial applications.

Key Insights for Industry Professionals

- Barrier Advantage: Thin aluminum foil layers ensure total protection against oxygen, bacteria, and moisture.

- Sustainability Strength: Nearly three-quarters of all aluminum ever made is still in use, highlighting its circular economy impact.

- Pharmaceutical Reliance: Blister packs ensure medicine safety, integrity, and extended shelf life.

- Versatility in Lamination: Aluminum laminates combine durability, flexibility, and attractive printability for multi-industry adoption.

Market Analysis: Recent Developments and Strategic Shifts

The aluminum foil packaging industry has been marked by strategic investments, product launches, and sustainability-focused innovations. In August 2025, Constantia Flexibles announced a transformative €100 million investment to modernize its global production network. This included a €50 million expansion at its Teich plant in Austria, boosting foil production by 30% to 90,000 tons annually. In the same month, Sealed Air Corporation reported volume growth in its industrial packaging portfolio, signaling a positive trend for aluminum foil demand across industrial sectors.

Crown Holdings’ July 2025 second-quarter results highlighted resilience in beverage packaging, a key application area for aluminum foil. Similarly, Ball Corporation received four prestigious EMBANEWS Awards in May 2025, showcasing inclusivity-driven packaging designs such as a braille-embossed energy drink lid. These awards underline the market’s shift toward accessibility, consumer engagement, and sustainability.

On the product innovation front, Constantia Flexibles introduced its recyclable ComforLid in April 2025, winning the Global Packaging Award. At the same time, Shyam Metalics & Energy launched SEL Tiger Foil in April 2024, addressing household food safety with customizable roll sizes. Beverage packaging also evolved when Capri Sun introduced a recyclable pouch in March 2024, integrating aluminum, PE, and PET to lower carbon footprints. Meanwhile, Constantia Flexibles’ acquisition of a 57% stake in Aluflexpack AG in February 2024 reinforced its dominance in Europe’s flexible packaging sector.

Emerging Trends and Growth Opportunities Shaping the Aluminum Foil Packaging Market

Strategic Lightweighting and Alloy Optimization to Mitigate Cost and Sustainability Pressures

The aluminum foil packaging market is undergoing a significant transformation driven by the need to reduce material costs and environmental impact. Manufacturers are increasingly adopting advanced lightweighting techniques and optimized alloy compositions to lower material usage per package while preserving essential barrier properties. Technological innovations have enabled foil thickness reductions of up to 30% without compromising protection against light, moisture, or oxygen. Specific high-performance alloys, such as 8011 and 1235, are engineered to maintain pinhole-free integrity, ensuring that critical sectors like pharmaceuticals and food can continue to rely on aluminum foil for high-barrier applications. These strategies simultaneously reduce carbon emissions associated with aluminum production and transportation, highlighting the dual economic and environmental benefits of lightweight foil adoption.

Integration of Aluminum Foil into High-Barrier, Mono-Polymer Structures for Recyclability

Addressing end-of-life challenges for multi-material laminates, converters are innovating by combining ultra-thin aluminum foil with compatible polymers to form high-barrier mono-material structures. This approach allows packaging to retain barrier functionality while being recyclable within standard polyolefin streams. Innovations such as delamination processes using acid solutions to separate foil from plastic or paper facilitate the recovery of high-purity aluminum for reuse, promoting circular economy principles. Companies like Toppan are spearheading mono-material barrier packaging development, signaling a long-term strategic shift toward recyclable, sustainable flexible packaging solutions that maintain high-performance characteristics.

Development of a Viable, Scalable Recycling Stream for Flexible Foil-Laminated Packaging

There is a substantial growth opportunity in creating scalable recycling technologies for post-consumer foil-laminated packaging. Advanced sorting, delamination, and electrolytic recovery solutions can enable the extraction of high-purity aluminum, reducing environmental impact and supporting circular economy initiatives. Governmental regulations, such as India’s draft Extended Producer Responsibility (EPR) rules for non-ferrous metals, mandate recycling targets for aluminum producers, incentivizing investment in innovative recycling infrastructure. Public-private collaborations, exemplified by the Jawaharlal Nehru Aluminium Research Development and Design Centre (JNARDDC), are actively researching advanced recovery technologies, laying the groundwork for a robust, scalable recycling ecosystem for complex foil-based packaging materials.

Expansion of Aluminum Foil in Pharmaceutical and ESG-Conscious Battery Supply Chains

Beyond conventional food packaging, aluminum foil is seeing growing adoption in high-value, high-growth sectors like pharmaceutical blister packs and lithium-ion battery casings. Its exceptional barrier properties make it ideal for protecting moisture- and light-sensitive drugs, ensuring compliance with global regulatory standards set by the International Council for Harmonisation (ICH). In the energy sector, aluminum foil serves as a critical component for the cathode in lithium-ion batteries, offering excellent electrical conductivity and mechanical strength necessary for EVs and consumer electronics. Ongoing publicly funded research projects aim to further enhance foil performance in battery applications, highlighting a promising diversification path that aligns with ESG-focused manufacturing and the rapidly expanding energy storage market.

Competitive Landscape: Leading Companies in Global Aluminum Foil Packaging

The competitive environment of the aluminum foil packaging market is shaped by global leaders driving sustainability, industrial scale, and advanced packaging technologies. These companies are enhancing recyclability, expanding geographic reach, and strengthening their portfolios through product launches and acquisitions.

Constantia Flexibles: Expanding Global Capacity and Sustainable Innovation

Constantia Flexibles is a global packaging leader with a strong aluminum foil product range for food, pharma, and personal care. In February 2024, it acquired a majority stake in Aluflexpack AG, strengthening its European presence, while in August 2025 it committed over €100 million to global upgrades. Its new ComforLid emphasizes recyclability and CO2 reduction, reflecting its focus on sustainable, consumer-friendly solutions.

Amcor plc: Innovating with Recyclable Alternatives to Aluminum Laminates

Amcor offers a broad portfolio of aluminum foil packaging but is also pioneering alternatives such as AmLite Recyclable, a high-barrier metal-free solution compatible with recycling streams. Its Amcor 360 service and MaXQ Smart Packaging support clients with end-to-end solutions and consumer engagement tools. Amcor’s strategy is anchored in achieving 100% recyclable or reusable packaging by 2025.

Huhtamaki Oyj: Strengthening Global Flexible Packaging Footprint

Huhtamaki integrates aluminum foil into its high-performance laminates and pouches for food and beverages. In February 2025, it restructured its Fiber Foodservice Europe-Asia-Oceania segment to sharpen focus and efficiency. With strong operations across India and other growth markets, Huhtamaki leverages vertical integration and an extensive R&D network to accelerate product commercialization.

UACJ Corporation: Leveraging Industrial Scale and R&D Strength

UACJ is a world leader in aluminum production with a capacity of over 1.4 million tons annually, including a diverse range of aluminum foil applications spanning food, pharma, and energy storage. In November 2022, its subsidiary Tri-Arrows Aluminum earned ASI certification, reinforcing its sustainability credentials. UACJ’s competitive edge lies in its technological expertise and its joint-development model for accelerating product innovation.

Aluminum Foil Packaging Market Share Insights

Pouches Lead Market Share by Product Type in the Aluminum Foil Packaging Industry

Aluminum foil pouches hold the largest share at 32%, reflecting their versatility and ability to serve multiple industries from coffee and snacks to pharmaceuticals and pet food. Their dominance stems from high-barrier protection against moisture, light, and oxygen combined with lightweight properties that reduce shipping costs and align with sustainability goals through source reduction. Blister packs, with 28%, represent the pharmaceutical standard, delivering hermetic sealing and tamper evidence for tablets, capsules, and OTC drugs. Rolled foil continues to be the consumer and industrial workhorse, sustaining entrenched household use for cooking and food storage while also serving food service and industrial applications like insulation and shielding. Backed foil maintains a niche role in specialized applications such as yogurt lids, butter wraps, and laminated seals, where enhanced printability and tear resistance are required. Containers foil trays and pans serve the premium prepared food segment, offering durability, heat conductivity, and recyclability that cater to the convenience-driven ready-meal market. This segmentation highlights how aluminum foil packaging maintains relevance across both traditional and emerging applications by balancing performance with sustainability.

Food and Beverages Dominate Market Share by End-Use in the Aluminum Foil Packaging Industry

Food and beverages account for nearly 65% of global demand, cementing their role as the primary driver of aluminum foil packaging consumption. Foil’s unique ability to extend shelf life, preserve aroma, and prevent contamination makes it indispensable for dairy lidding, confectionery wraps, pet food pouches, and ready-meal trays. Pharmaceuticals and healthcare form the high-value core, where aluminum blister packs and sterile foil pouches are critical for maintaining drug integrity and patient safety under stringent regulatory requirements. Cosmetics and personal care rely on foil’s premium appeal and barrier properties to protect active ingredients in creams, serums, and luxury samples, aligning packaging with brand positioning. The “other” category covering automotive and construction represents an industrial niche where foil is used for moisture-proofing sensitive components, adhesives, and sealants. While food drives sheer volume and pharmaceuticals drive value, cosmetics and industrial applications demonstrate aluminum foil’s versatility across both consumer and technical markets.

United States: Advanced Recycling and Sustainable Solutions Drive Aluminum Foil Packaging Market

The U.S. aluminum foil packaging market is increasingly shaped by evolving regulations and sustainability initiatives. State-level Extended Producer Responsibility (EPR) laws are a major driver, holding producers accountable for the lifecycle management of packaging waste and encouraging the adoption of recyclable materials. Technological advancements are accelerating industry efficiency; a notable example is the strategic partnership between Lotte Aluminium Materials USA and SMS Group in January 2024 to implement a logistics and digitalization package for Lotte's greenfield aluminum cathode foil plant in Kentucky, focusing on ultra-thin aluminum foil for electric vehicle batteries.

Corporate initiatives are also playing a pivotal role in expanding sustainable packaging solutions. Wyda Packaging entered the U.S. market in November 2024 with a new facility producing 100% recyclable aluminum foil and trays for food service, hospitality, and consumer sectors. Consumer demand for eco-friendly products continues to drive investment, with Novelis Inc. expanding recycling capabilities to support a circular economy. Key applications in food, pharmaceuticals, and consumer goods are stimulating the development of high-barrier laminates, ensuring product integrity, sterility, and extended shelf life.

Germany: Circular Economy Leadership and Regulatory Compliance Shape Market Growth

Germany’s aluminum foil packaging market is strongly guided by stringent regulations and circular economy principles. The EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates full recyclability or reuse by 2030 and establishes minimum targets for recycled content. Complementing this, the German Packaging Act (VerpackG) ensures producers are responsible for the full lifecycle of packaging, leading to innovations in mono-material foil and robust recycling systems.

Technological advancements are driving next-generation lightweight foil solutions, exemplified by Toyo Seikan’s 6.1g beverage can launched in 2024, reducing material usage while maintaining strength. The food and pharmaceutical sectors remain key applications, requiring superior barrier properties to preserve freshness and product safety. The rise of e-commerce further necessitates durable and high-quality packaging to withstand shipping, while the market is seeing a clear shift toward recyclable and lightweight materials to meet both consumer and regulatory demands.

China: Dual Carbon Goals and Industrial Applications Propel Aluminum Foil Packaging

China’s aluminum foil packaging market is rapidly expanding under government initiatives aimed at achieving carbon peak and carbon neutrality. The new packaging regulation effective June 2025 promotes recycled materials and reusable systems, while stricter environmental policies are consolidating smaller mills, enhancing the market share of larger, efficient producers.

Technological advancements, including automation, AI, and “5G plus industrial internet” integration, are improving production efficiency and flexible manufacturing capacity. China is also a leading producer of battery-grade aluminum foil, producing 122,700 tons in the first half of 2023, highlighting the importance of industrial applications such as electric vehicles. Sustainability efforts are shaping material choices, with a growing preference for paper-based and recyclable alternatives. The expansion of domestic e-commerce platforms is fueling demand for customizable and protective packaging solutions across chemicals, food products, and industrial goods.

India: Government Incentives and Biodegradable Innovation Strengthen Aluminum Foil Packaging

India’s aluminum foil packaging market is benefiting from government programs such as “Make in India” and “Zero Effect Zero Defect,” which promote domestic manufacturing and high-quality production. The Production Linked Incentive (PLI) Scheme for the food processing industry further drives demand for standardized, high-quality packaging solutions. Regulatory policies, including the Plastic Waste Management (Amendment) Rules, encourage the adoption of eco-friendly alternatives.

Technological advancements are prominent, with IIT Madras developing agricultural waste-based packaging materials as sustainable substitutes for conventional foams. Corporate initiatives, such as Hindalco Industries’ acquisition of Hydro’s aluminum extrusions business, expand capabilities in aluminum packaging solutions. The market is increasingly focused on biodegradable and compostable materials, exemplified by WOL3D, a Mumbai-based company producing innovative protective packaging. Rising infrastructure investments and emphasis on sustainability position India as a rapidly growing hub for advanced aluminum foil packaging solutions.

Brazil: Circular Economy Policies and Strategic Investments Enhance Aluminum Foil Packaging

Brazil’s aluminum foil packaging market is driven by the National Solid Waste Policy, promoting a circular economy and reusable, durable alternatives. Technological advancements, including AI and robotics, are improving operational efficiency, from automated sorting to defect detection. Sustainability initiatives, reinforced by a January 2025 ban on importing solid waste, encourage domestic waste management practices and eco-friendly material adoption.

Strategic investments are shaping the market landscape, such as Novelis Inc.’s Customer Solution Center in São José dos Campos, launched in March 2023, focusing on sustainable aluminum solutions for beverage packaging. Key applications span the food and beverage sector, with demand for foil bags, totes, and containers increasing alongside the expanding food processing industry. HTMM is also customizing aluminum foil offerings for the Brazilian flexible packaging market, producing 6–7 micron foils suitable for food, pharmaceuticals, consumer goods, and personal care packaging, reflecting growing innovation and sustainability adoption.

Japan: Advanced Recycling and Bio-Based Materials Revolutionize Aluminum Foil Packaging

Japan’s aluminum foil packaging market emphasizes advanced recycling and innovation. The country’s Containers and Packaging Recycling Law assigns clear responsibilities to businesses, establishing an efficient system for collecting and repurposing packaging materials. Regulatory updates by the Ministry of Health, Labour and Welfare (MHLW) in May 2025 revise requirements for food-contact packaging, ensuring safety and compliance.

The market is increasingly adopting bio-based materials, with LyondellBasell integrating bio-based polypropylene into Shiseido’s packaging, demonstrating the trend toward sustainable solutions. Continuous functional innovations are enhancing dimensional stability and resistance to deformation for high-performance applications. Corporate collaborations, such as Toyo Aluminium K.K.’s merger with JIC Capital in August 2022, strengthen manufacturing technology, streamline logistics, and integrate IT systems to optimize costs. These efforts underscore Japan’s leadership in sustainable, high-quality aluminum foil packaging solutions.

Aluminum Foil Packaging Market Report Scope

Aluminum Foil Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.9 Billion

|

|

Market Size (2034)

|

$39 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Rolled Foil, Backed Foil, Pouches, Blister Packs, Containers), By Material (Plain Aluminum Foil, Laminated Aluminum Foil), By Application (Food Packaging, Pharmaceutical Packaging, Industrial Packaging, Household Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Automotive, Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Novelis Inc., Hindalco Industries Limited, Constantia Flexibles Group GmbH, UACJ Corporation, Ball Corporation, Mondi Group, Alufoil Products Pvt. Ltd., Eurofoil Group S.A., Ardagh Group S.A., Sonoco Products Company, Ess Dee Aluminium, Symetal S.A., Aliberico S.A., Wyda Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aluminum Foil Packaging Market Segmentation

By Product Type

- Rolled Foil

- Backed Foil

- Pouches

- Blister Packs

- Containers

By Material

- Plain Aluminum Foil

- Laminated Aluminum Foil

By Application

- Food Packaging

- Pharmaceutical Packaging

- Industrial Packaging

- Household Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Automotive

- Construction

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aluminum Foil Packaging Market

- Amcor plc

- Novelis Inc.

- Hindalco Industries Limited

- Constantia Flexibles Group GmbH

- UACJ Corporation

- Ball Corporation

- Mondi Group

- Alufoil Products Pvt. Ltd.

- Eurofoil Group S.A.

- Ardagh Group S.A.

- Sonoco Products Company

- Ess Dee Aluminium

- Symetal S.A.

- Aliberico S.A.

- Wyda Packaging

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-dimensional research methodology to deliver actionable insights on the global Aluminum Foil Packaging Market. Our analysis integrates primary research, including interviews with packaging engineers, supply chain managers, R&D professionals, and sustainability experts, with secondary research sourced from corporate filings, industry journals, regulatory databases, and trade publications. Market sizing from $24.9 billion in 2025 to $39 billion by 2034 at a CAGR of 5.1% is determined using a combination of top-down and bottom-up approaches, accounting for product types (rolled foil, backed foil, pouches, blister packs, containers), materials (plain and laminated aluminum foil), applications (food, pharmaceuticals, industrial, household), and end-use industries (food & beverages, pharmaceuticals, cosmetics, automotive, construction). USDAnalytics also evaluates emerging trends such as lightweighting, high-barrier mono-material structures, scalable recycling streams, and adoption in ESG-focused battery and pharmaceutical applications. Regional insights across the U.S., Germany, China, India, Brazil, and Japan consider regulatory frameworks, sustainability mandates, and technological integration. Competitive benchmarking covers major players such as Constantia Flexibles, Amcor, UACJ, Hindalco, and Novelis, focusing on capacity expansion, product innovation, and sustainable packaging initiatives. This methodology ensures precise, industry-relevant intelligence for professionals seeking to optimize packaging performance, sustainability outcomes, and regulatory compliance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.