Anti-Corrosion Nanocoating Market Size and Growth Driven by Advanced Surface Engineering and Precision Applications

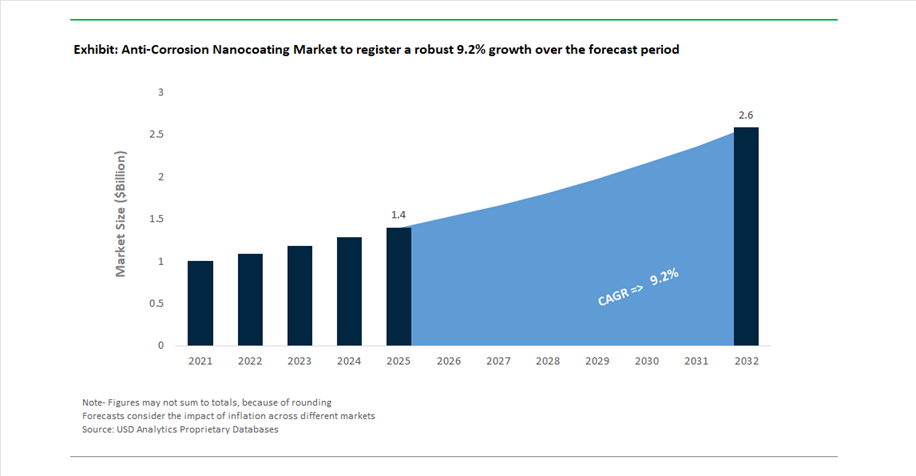

The Anti-Corrosion Nanocoating Market is emerging as a high-growth, technology-driven segment, expanding from USD 1.4 billion in 2025 to USD 2.6 billion by 2032, registering a robust CAGR of 9.2%. This accelerated growth reflects the increasing adoption of nanotechnology-enabled coating systems that deliver superior protection at minimal thickness, particularly in industries requiring precision performance such as electronics, aerospace, medical devices, and advanced manufacturing.

Nanocoatings represent a paradigm shift in corrosion protection by utilizing nanoscale particles and engineered surface interactions to create ultra-thin, highly uniform protective layers. These coatings offer enhanced adhesion, self-healing capabilities, hydrophobicity, and resistance to chemical and environmental degradation, outperforming traditional coatings in demanding applications. Their ability to provide high-performance protection without adding significant weight or thickness makes them especially valuable in aerospace and electronics, where material efficiency and miniaturization are critical.

The market is also benefiting from growing demand for multi-functional coatings, where anti-corrosion performance is combined with features such as anti-reflective properties, self-cleaning surfaces, and energy efficiency enhancements. For instance, nanocoatings are increasingly being deployed in solar panels, offshore wind structures, and precision medical instruments, where durability and performance consistency are essential. Additionally, regulatory pressure to eliminate hazardous substances such as chromates is accelerating the adoption of environmentally compliant nanostructured alternatives.

From a technological standpoint, the integration of smart materials, nanosensors, and digital monitoring capabilities is redefining corrosion management strategies. These advancements enable predictive maintenance and real-time performance tracking, reducing downtime and extending asset lifespans. The competitive landscape is characterized by intensive R&D investment, strategic consolidation, and targeted expansion into high-value applications, positioning nanocoatings as a cornerstone of next-generation surface protection technologies

Nanotechnology Integration, Smart Coatings, and Strategic Investments Accelerating Market Evolution

The anti-corrosion nanocoating market is undergoing rapid transformation driven by nanotechnology innovation, strategic mergers, and global capacity expansion. Product development is also expanding into multi-functional applications. TriNANO Technologies’ June 2024 launch of nano anti-reflective solar coatings demonstrates how nanocoatings can simultaneously enhance corrosion resistance and energy efficiency, improving solar panel output while protecting structural components. Additionally, PPG’s Envirocron® Extreme Protection Edge Plus (October 2025) incorporates nanoparticle dispersion technology to achieve superior edge coverage and adhesion, eliminating labor-intensive surface preparation steps.

Sustainability and regulatory compliance are key innovation drivers. Indestructible Paint’s January 2025 chromium-free nanostructured primers provide an environmentally compliant alternative to traditional chromate-based systems, aligning with stringent REACH regulations while maintaining high-performance corrosion protection. In parallel, AkzoNobel’s December 2025 divestment of its decorative business in India underscores a strategic pivot toward high-margin industrial technologies, including nanocoatings and advanced powder systems.

Strategic project participation further validates the market’s growth trajectory. Jotun’s involvement in France’s EOLMED floating wind project (mid-2025) highlights the deployment of nanostructured barrier coatings in extreme marine environments, where long-term durability is essential.

Atomic Layer Deposition (ALD) Enabling Ultra-Conformal Nanocoatings for EV Battery Protection

The anti-corrosion nanocoating industry is entering a high-precision manufacturing phase with the rapid adoption of Atomic Layer Deposition (ALD) for electric vehicle battery components. As EV architectures shift toward higher voltage platforms and aggressive thermal cycling conditions, conventional coating technologies are increasingly inadequate due to pinhole formation and non-uniform surface coverage. ALD addresses these limitations by delivering sub-nanometer thin films with atomic-level control, enabling the formation of defect-free, conformal coatings across complex geometries such as battery cooling plates, porous electrodes, and high-aspect-ratio structures.

ALD nanocoatings typically range between 1 and 50 nanometers in thickness, yet provide complete surface coverage, ensuring 100% conformality that cannot be achieved through spray, dip, or electrochemical coating methods. This structural precision directly contributes to enhanced battery safety. Nanocoated cathode and anode materials have demonstrated the ability to increase the onset temperature for thermal runaway, providing a critical safety buffer for high-energy-density, high-nickel chemistries increasingly used in modern EVs.

From a scalability perspective, advancements in spatial ALD systems are overcoming historical cost barriers. High-throughput manufacturing lines are now capable of processing between 3,000 kg and 30,000 kg of material per day, reducing coating costs to below $1/kg at industrial scale. In terms of performance, ALD-passivated battery materials exhibit significantly reduced impedance growth over time, enabling cycle life improvements of approximately 20% to 30% compared to uncoated systems. These advantages position ALD nanocoatings as a core enabling technology in next-generation EV battery design, supporting both safety and lifecycle performance requirements.

Microplastic Restrictions Accelerating Shift to Inorganic and Biodegradable Nanocoatings

The regulatory landscape for coatings is tightening further with the enforcement of microplastic restrictions under EU REACH Entry 78, which entered a critical implementation phase in 2026. This regulation directly impacts anti-corrosion nanocoatings that rely on synthetic polymer microparticles as binders or functional additives, forcing a widespread transition toward environmentally benign alternatives. The introduction of a 0.01% concentration threshold for synthetic polymer microparticles has triggered strict labeling requirements and initiated phased elimination timelines for non-compliant formulations.

Compliance obligations have intensified significantly. Beginning in May 2026, manufacturers are required to submit detailed annual reports to regulatory authorities, including comprehensive emission estimates and full disclosure of polymer compositions used in coating systems. This level of transparency is increasing operational complexity and driving investment in digital compliance infrastructure. Many organizations are adopting AI-driven environmental accountability platforms to manage regulatory reporting, track formulation changes, and ensure adherence to evolving environmental standards ahead of enforcement deadlines in 2026 and 2027.

The reformulation impact is substantial, with approximately 25% of traditional sacrificial coatings and anti-fouling systems currently undergoing redesign to replace non-biodegradable polymer carriers. Emerging alternatives include nanocellulose-based binders and silica hybrid systems, which offer improved environmental profiles while maintaining functional performance. This regulatory push is accelerating innovation in inorganic nanocoatings and sustainable material science, creating a competitive advantage for manufacturers capable of delivering compliant, high-performance anti-corrosion solutions aligned with global environmental mandates.

Nanocomposite Coatings Enhancing Durability and Efficiency in Desalination Systems

The growing global water scarcity challenge is driving rapid expansion in desalination infrastructure, creating a strong demand for advanced anti-corrosion nanocoatings tailored for reverse osmosis (RO) systems. High-salinity environments present severe corrosion risks for pressure vessels, pipelines, and structural components, necessitating coatings that can provide long-term protection while supporting operational efficiency.

Nanocomposite coatings incorporating green materials such as biopolymers and natural nanoparticles are emerging as high-performance solutions for desalination applications. These coatings enable enhanced permeability performance, with water flux values ranging between 90 and 110 L/m²·h·bar, optimizing energy consumption in RO systems. At the same time, advanced surface engineering techniques are achieving salt rejection rates between 96% and 100%, ensuring high-purity water output while protecting infrastructure from chloride-induced corrosion and pitting.

Fouling resistance is another critical advantage. Nanostructured coating surfaces exhibit low fouling characteristics, maintaining resistance values between 6 and 10 kPa, which reduces the frequency of chemical cleaning cycles and extends operational uptime. In terms of durability, inorganic nanocoatings—accounting for approximately 73.5% of the market volume in this segment—are enabling desalination facilities to target design lifespans of up to 30 years for critical components. This combination of efficiency, durability, and sustainability is positioning nanocomposite coatings as a key enabler of next-generation water treatment infrastructure.

Hydrophobic Nanocoatings Extending Service Life of Bridge Cable Infrastructure

Aging infrastructure is a critical global challenge, particularly for bridge systems exposed to harsh environmental conditions. Hydrophobic nanocoatings are emerging as an effective solution for protecting cable-stayed bridge structures against moisture ingress, corrosion, and freeze-thaw damage. These coatings, typically formulated using silica nanoparticles, titanium dioxide, and advanced ceramic composites, create highly water-repellent surfaces that significantly reduce corrosion risk.

Superhydrophobic nanocoatings achieve contact angles exceeding 150°, enabling rapid water shedding and preventing the accumulation of moisture and de-icing salts on cable surfaces. This performance is particularly valuable in regions subject to extreme weather fluctuations, where repeated freeze-thaw cycles accelerate material degradation. By minimizing water ingress, these coatings help maintain structural integrity and reduce the likelihood of corrosion-induced failures.

From a lifecycle perspective, the application of hydrophobic nanocoatings can extend the service life of bridge infrastructure by 30% to 50%, delaying costly replacement and rehabilitation projects. Additionally, reduced maintenance frequency translates into lower lifecycle carbon emissions, with estimates indicating up to 40% reduction compared to conventional maintenance-intensive systems. Advanced material systems, including graphene-based nanocomposites and ceramic nano-layers, are further enhancing barrier performance, outperforming traditional epoxy coatings in long-term durability tests, particularly in high-vibration environments typical of cable-stayed bridges.

Nanocomposites Dominate Anti-Corrosion Nanocoating Market Share in 2025 with Graphene-Driven Performance Gains

Nanomaterial Type Analysis: Graphene-Enhanced Nanocomposites Lead with 48% Market Share

Nanocomposites command a dominant 48.0% share of the global anti-corrosion nanocoating market in 2025, driven by their unmatched cost-performance efficiency and seamless integration into existing coating systems. By incorporating graphene nanoplatelets, nano-silica, and nano-clay (0.5%–3.0% by weight) into conventional epoxy and polyurethane coatings, manufacturers achieve 50%–70% improvement in barrier properties, significantly reducing permeability to corrosive agents. This “drop-in nanotechnology” approach eliminates the need for new application infrastructure, accelerating adoption across marine coatings, offshore wind towers, ballast tanks, and infrastructure protection. The key mechanism, tortuous path extension, creates a complex microstructure that slows chloride and oxygen diffusion, enhancing durability. With declining graphene costs in 2025, nanocomposites have transitioned from niche aerospace applications to large-scale marine newbuilding and bridge infrastructure projects, solidifying their leadership in the anti-corrosion coatings market.

Oil & Gas Sector Leads Anti-Corrosion Nanocoating Market Demand with High-Risk ROI Justification

End-Use Industry Analysis: Oil & Gas Captures 28.5% Share Amid High Failure Costs

The oil and gas industry accounts for 28.5% of the anti-corrosion nanocoating market in 2025, making it the largest end-use segment due to the extreme financial and environmental risks associated with corrosion failures. With potential losses ranging from $5 million to $50 million per day from leaks or downtime, operators prioritize advanced nanocoating technologies despite a 20–40% cost premium, as they deliver strong risk-reduction ROI. Key applications include nanocomposite epoxy linings replacing costly corrosion-resistant alloys (CRA) in pipelines, metallic nanocoatings (zinc/aluminum platelets) protecting offshore fasteners and flange systems, and ceramic nanocoatings addressing under-insulation corrosion (CUI) in high-temperature environments. Additionally, stringent compliance with ISO 12944 CX (Offshore) and NACE TM0104 standards creates a high barrier to entry, ensuring long-term contracts for qualified suppliers. This regulatory moat further reinforces oil & gas dominance in the global anti-corrosion nanocoatings market.

Anti Corrosion Nanocoating Market Competitive Landscape Driven by Nano-Engineered Protection and Sustainable Coating Technologies

The anti corrosion nanocoating market is driven by graphene coatings, nano-silicone systems, and nano-reinforced epoxy technologies. Key players are focusing on VOC-free formulations, self-healing coatings, and high-performance nanocomposites to enhance durability, reduce lifecycle costs, and meet stringent environmental regulations across aerospace, marine, energy, and infrastructure sectors.

AkzoNobel accelerates nano-reinforced coatings with laser-curing and sustainability leadership

AkzoNobel is strengthening its position in anti corrosion nanocoatings through technology-led innovation and strategic consolidation. The company reported €10.16 billion in 2025 revenue with a 14.2% adjusted EBITDA margin, supported by high-margin performance coatings and nano-powder technologies. Its proposed merger with Axalta Coating Systems in 2026 is focused on consolidating R&D capabilities for nano-reinforced automotive coatings and industrial primers. Collaboration with IPG Photonics enabled the development of laser-curing powder coatings, ensuring uniform nanoparticle dispersion and reduced energy consumption. The company achieved nearly 50% reduction in Scope 1 and 2 emissions compared to 2018, driven by VOC-free nanocoating adoption. Product innovation continues to focus on high-performance, sustainable anti-corrosion coatings for industrial applications.

PPG Industries expands graphene-based nanocoatings and digital protective systems

PPG Industries leads the anti corrosion nanocoating market through advanced electrocoat systems and graphene-enhanced coatings. The company reported $15.9 billion in net sales in 2025, with 43% of revenue derived from sustainably advantaged coatings. Its Sigma Sailadvance NX nanocoating introduces advanced antifouling technology that reduces drag and corrosion in marine environments. In April 2026, PPG launched integrated protective solutions for data centers, combining nanocoatings with electromagnetic interference shielding and thermal management capabilities. A $50 million investment in 2026 supports modernization of European facilities for chromate-free nano-primers targeting aerospace coatings. Product development continues to emphasize multifunctional coatings with enhanced durability and environmental compliance.

Hempel advances nano-silicone and activated zinc coatings for long-term corrosion protection

Hempel A/S is emerging as a key innovator in anti corrosion nanocoatings through nano-silicone and activated zinc technologies. The company reported €259 million in free cash flow in 2025 with an 18.2% EBITDA margin, supporting increased R&D investment in nanotechnology. Its Hempaguard NB nano-silicone coating reduces fuel consumption and corrosion from initial vessel deployment, improving operational efficiency in marine coatings applications. The Avantguard® range utilizes nanotechnology in zinc primers to deliver C5-M corrosion protection exceeding 35 years, significantly extending maintenance cycles for offshore assets. Leadership expansion in 2026 supports global rollout of nano-enhanced protective coatings across shipping and energy sectors. Product development continues to focus on durability and lifecycle optimization in extreme environments.

AnCatt disrupts anti corrosion coatings with heavy-metal-free nanotechnology solutions

AnCatt is redefining the anti corrosion nanocoating market with heavy-metal-free coating systems based on conducting polymer nano dispersion technology. Its Rust-Legend™ coating has exceeded 13,000 hours in ASTM B117 salt fog testing, outperforming conventional zinc-rich coatings by 3 to 6 times in durability. The technology forms a dense metal oxide protective layer without the use of lead, chromate, or zinc, aligning with evolving REACH and EPA regulations. The coating system requires less than half the thickness of traditional coatings, reducing material usage and asset weight in aerospace and automotive applications. Its solutions are increasingly adopted in energy, mining, and aerospace sectors where regulatory pressure is accelerating the shift toward green coatings. Product innovation focuses on sustainability, efficiency, and high-performance corrosion protection.

Jotun expands nanocoating applications in EV batteries and offshore wind infrastructure

Jotun A/S is strengthening its role in anti corrosion nanocoatings through expansion in energy infrastructure and electric vehicle applications. The company reported revenues exceeding NOK 34 billion ($3.1 billion) in 2025, supported by new manufacturing facilities in emerging markets. It introduced nanocoatings for EV battery housings that provide dielectric insulation and corrosion resistance against environmental exposure and mechanical stress. Integration of marine and protective coatings into a unified Steel Protection platform enhances development of nanocomposite epoxy coatings for offshore wind projects. The company is targeting significant share in the global offshore wind market by 2030 through self-healing nanocoatings that reduce maintenance requirements. Product innovation continues to focus on high-performance coatings for extreme and remote operating environments.

China Anti-Corrosion Nanocoating Market: Graphene Industrialization and Infrastructure-Led Nanotech Adoption

China’s anti-corrosion nanocoating market is advancing rapidly, driven by large-scale industrialization and government-backed material innovation strategies. The standardization of graphene-oxide-modified epoxy nanocoatings has significantly enhanced coating efficiency, enabling reduced film thickness while delivering superior salt-spray resistance for offshore wind and marine infrastructure. These developments are strengthening China’s position as a global leader in nanotechnology-driven corrosion protection solutions.

Government initiatives under the “14th Five-Year Plan” are accelerating the commercialization of nano-ceramic coatings, particularly in aerospace and high-performance industrial applications. The rapid expansion of the electric vehicle ecosystem is also boosting the adoption of ultra-thin nanocoatings for battery components, improving both corrosion resistance and thermal performance. Additionally, regulatory mandates enforcing low-VOC coatings are driving widespread adoption of water-borne nanocoating systems. Infrastructure megaprojects, including Belt and Road developments, are further amplifying demand for advanced self-cleaning and nanocomposite coatings in pipelines and structural assets.

United States Anti-Corrosion Nanocoating Market: Infrastructure Rehabilitation and Smart Nanocoating Innovations

The United States anti-corrosion nanocoating market is experiencing strong growth, fueled by infrastructure modernization and cutting-edge technological advancements. Large-scale investments in bridge rehabilitation and industrial infrastructure are driving demand for nanostructured cermet coatings that provide superior durability and resistance to mechanical wear.

Innovation is a key differentiator in the US market, with the development of smart self-healing nanocoatings that automatically release corrosion inhibitors when damage occurs. Advanced research initiatives have also led to the creation of superhydrophobic coatings that reduce drag and enhance corrosion resistance in marine environments. Regulatory pressure to reduce hazardous emissions is accelerating the adoption of UV-curable nanocoatings, which offer rapid curing and environmental compliance. Additionally, high-performance nano-enhanced coatings are being widely deployed in energy and petrochemical sectors, particularly for protecting critical equipment exposed to aggressive operating conditions.

Germany Anti-Corrosion Nanocoating Market: Bio-Based Nanocoatings and Industry 4.0 Integration

Germany’s anti-corrosion nanocoating market is defined by its leadership in sustainable materials and digital manufacturing technologies. The transition toward isocyanate-free nanocoatings and bio-attributed resins is significantly reducing environmental impact while maintaining high-performance standards required for industrial and automotive applications.

Technological advancements are further strengthening the market, particularly through the integration of IoT-enabled nano-sensors within coating systems for real-time monitoring of structural integrity. The country’s hydrogen infrastructure initiatives are also driving demand for advanced nanocomposite coatings designed to prevent material degradation in extreme environments. Additionally, innovations such as single-coat polyaspartic nanocoatings are improving application efficiency and durability. Strong investments in offshore and infrastructure projects are further supporting the adoption of nano-reinforced coatings for enhanced protection against harsh environmental conditions.

India Anti-Corrosion Nanocoating Market: Infrastructure Growth and Cost-Effective Nanotechnology Adoption

India’s anti-corrosion nanocoating market is expanding rapidly, supported by infrastructure development and government-led initiatives promoting domestic manufacturing. Investments in advanced nano-additives are reducing production costs, making high-performance nanocoatings more accessible across industrial sectors.

Infrastructure expansion projects are driving demand for durable coatings in transportation and energy sectors, particularly for high-speed rail and refinery applications. The adoption of moisture-cured nanocoatings is addressing challenges associated with high humidity environments, enabling efficient application in coastal and tropical regions. Innovations in multifunctional coatings, including antimicrobial and anti-corrosive hybrids, are expanding use cases in public infrastructure and healthcare. Additionally, growing investments in semiconductor manufacturing are creating demand for specialized anti-static nanocoatings, further diversifying the market landscape.

South Korea Anti-Corrosion Nanocoating Market: Shipbuilding Leadership and Advanced Nano-Siloxane Technologies

South Korea continues to dominate the anti-corrosion nanocoating market, driven by its global leadership in shipbuilding and advanced industrial manufacturing. The country’s shipyards are major consumers of cryogenic-stable nanocoatings used in LNG carrier construction, ensuring durability and performance under extreme conditions.

Technological advancements in application processes, including robotic systems and automated coating technologies, are improving precision and efficiency. Innovations in nano-siloxane coatings are delivering superior hardness and long-term weatherability, while regulatory policies are accelerating the shift toward solvent-free formulations. Investments in hydrogen infrastructure and advanced research are further expanding the scope of nanocoating applications, particularly in marine and energy sectors. Additionally, the development of biocide-free antifouling nanocoatings is enhancing environmental sustainability while maintaining high performance in maritime environments.

Japan Anti-Corrosion Nanocoating Market: Cryogenic Innovation and Smart Infrastructure Protection

Japan’s anti-corrosion nanocoating market is advancing through its focus on high-performance materials and sustainable infrastructure development. Innovations in nanocomposite coatings capable of operating at cryogenic temperatures are supporting the growth of hydrogen-based energy systems, ensuring long-term durability in extreme conditions.

The country is also investing in infrastructure modernization, with nano-silica coatings being widely used to protect rail networks and urban structures from environmental degradation. Photocatalytic nanocoatings are gaining traction for their self-cleaning properties, reducing maintenance costs and improving aesthetic longevity. Expansion in semiconductor manufacturing is further driving demand for advanced nano-materials, while government initiatives promoting energy-efficient coatings are accelerating adoption in urban construction. Additionally, the development of high-refractive-index nanocoatings for automotive and electronics applications highlights Japan’s leadership in multifunctional coating technologies.

Anti-Corrosion Nanocoating Market Report Scope

Anti-Corrosion Nanocoating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2032)

|

$2.6 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Nanomaterial (Nanocomposites, Metallic Nanocoatings, Ceramic Nanocoatings, Bio-based Nanocoatings), By Coating Technology (Sol-Gel Process, Chemical Vapor Deposition, Physical Vapor Deposition, Atomic Layer Deposition, Electrophoretic Deposition, Thermal Spraying), By Type of Protection (Barrier Protection, Cathodic Protection, Inhibitive Protection, Multi-functional Nanocoatings), By Substrate Compatibility (Ferrous Metals, Non-Ferrous Metals, Composites and Hybrid Substrates, Concrete and Reinforcing Steel), By End-Use Industry (Marine and Offshore, Oil and Gas, Aerospace and Defense, Automotive and Transportation, Power Generation, Industrial Manufacturing, Electronics and Telecommunications, Infrastructure), By Application Focus (OEM, MRO)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Hempel A/S, Jotun A/S, Tesla Nanocoatings, Inc., NanoVere Technologies, LLC, P2i Ltd., Aculon, Inc., NEI Corporation, Nanofilm Technologies International Limited, ACTnano, Inc., NanoXplore Inc., Haydale Graphene Industries PLC, HZO, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti-Corrosion Nanocoating Market Segmentation

By Nanomaterial

- Nanocomposites

- Metallic Nanocoatings

- Ceramic Nanocoatings

- Bio-based Nanocoatings

By Coating Technology

- Sol-Gel Process

- Chemical Vapor Deposition

- Physical Vapor Deposition

- Atomic Layer Deposition

- Electrophoretic Deposition

- Thermal Spraying

By Type of Protection

- Barrier Protection

- Cathodic Protection

- Inhibitive Protection

- Multi-functional Nanocoatings

- Self-healing

- Hydrophobic and Superhydrophobic

- Corrosion Sensing

- Antimicrobial Anti-corrosion

By Substrate Compatibility

- Ferrous Metals

- Non-Ferrous Metals

- Composites and Hybrid Substrates

- Concrete and Reinforcing Steel

By End-Use Industry

- Marine and Offshore

- Oil and Gas

- Aerospace and Defense

- Automotive and Transportation

- Power Generation

- Industrial Manufacturing

- Electronics and Telecommunications

- Infrastructure

By Application Focus

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Anti Corrosion Nanocoating Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Hempel A/S

- Jotun A/S

- Tesla Nanocoatings, Inc.

- NanoVere Technologies, LLC

- P2i Ltd.

- Aculon, Inc.

- NEI Corporation

- Nanofilm Technologies International Limited

- ACTnano, Inc.

- NanoXplore Inc.

- Haydale Graphene Industries PLC

- HZO, Inc.

*- List not Exhaustive

Table of Contents: Anti-Corrosion Nanocoating Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Anti-Corrosion Nanocoating Market Landscape & Outlook (2025–2032)

2.1. Introduction to Anti-Corrosion Nanocoating Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Growth Drivers: Advanced Surface Engineering and Precision Applications

2.4. Multi-Functional Coatings and Sustainability Trends

2.5. Integration of Smart Materials and Predictive Maintenance Technologies

3. Innovations Reshaping the Anti-Corrosion Nanocoating Market

3.1. Trend: Nanotechnology Integration, Smart Coatings, and Strategic Investments

3.2. Trend: Microplastic Restrictions and Shift to Inorganic/Biodegradable Nanocoatings

3.3. Opportunity: Atomic Layer Deposition (ALD) for EV Battery Protection

3.4. Opportunity: Nanocomposite Coatings in Desalination and Infrastructure Applications

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Anti-Corrosion Nanocoating Market

5.1. By Nanomaterial

5.1.1. Nanocomposites

5.1.2. Metallic Nanocoatings

5.1.3. Ceramic Nanocoatings

5.1.4. Bio-based Nanocoatings

5.2. By Coating Technology

5.2.1. Sol-Gel Process

5.2.2. Chemical Vapor Deposition

5.2.3. Physical Vapor Deposition

5.2.4. Atomic Layer Deposition

5.2.5. Electrophoretic Deposition

5.2.6. Thermal Spraying

5.3. By Type of Protection

5.3.1. Barrier Protection

5.3.2. Cathodic Protection

5.3.3. Inhibitive Protection

5.3.4. Multi-functional Nanocoatings

5.4. By Functional Capability

5.4.1. Self-healing

5.4.2. Hydrophobic and Superhydrophobic

5.4.3. Corrosion Sensing

5.4.4. Antimicrobial Anti-corrosion

5.5. By Substrate Compatibility

5.5.1. Ferrous Metals

5.5.2. Non-Ferrous Metals

5.5.3. Composites and Hybrid Substrates

5.5.4. Concrete and Reinforcing Steel

5.6. By End-Use Industry

5.6.1. Marine and Offshore

5.6.2. Oil and Gas

5.6.3. Aerospace and Defense

5.6.4. Automotive and Transportation

5.6.5. Power Generation

5.6.6. Industrial Manufacturing

5.6.7. Electronics and Telecommunications

5.6.8. Infrastructure

5.7. By Application Focus

5.7.1. OEM

5.7.2. MRO

6. Country Analysis and Outlook of Anti-Corrosion Nanocoating Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Anti-Corrosion Nanocoating Market Size Outlook by Region (2025–2032)

7.1. North America Anti-Corrosion Nanocoating Market Size Outlook to 2032

7.1.1. By Nanomaterial

7.1.2. By Coating Technology

7.1.3. By Type of Protection

7.1.4. By Functional Capability

7.1.5. By Substrate Compatibility

7.1.6. By End-Use Industry

7.1.7. By Application Focus

7.2. Europe Anti-Corrosion Nanocoating Market Size Outlook to 2032

7.2.1. By Nanomaterial

7.2.2. By Coating Technology

7.2.3. By Type of Protection

7.2.4. By Functional Capability

7.2.5. By Substrate Compatibility

7.2.6. By End-Use Industry

7.2.7. By Application Focus

7.3. Asia Pacific Anti-Corrosion Nanocoating Market Size Outlook to 2032

7.3.1. By Nanomaterial

7.3.2. By Coating Technology

7.3.3. By Type of Protection

7.3.4. By Functional Capability

7.3.5. By Substrate Compatibility

7.3.6. By End-Use Industry

7.3.7. By Application Focus

7.4. South America Anti-Corrosion Nanocoating Market Size Outlook to 2032

7.4.1. By Nanomaterial

7.4.2. By Coating Technology

7.4.3. By Type of Protection

7.4.4. By Functional Capability

7.4.5. By Substrate Compatibility

7.4.6. By End-Use Industry

7.4.7. By Application Focus

7.5. Middle East and Africa Anti-Corrosion Nanocoating Market Size Outlook to 2032

7.5.1. By Nanomaterial

7.5.2. By Coating Technology

7.5.3. By Type of Protection

7.5.4. By Functional Capability

7.5.5. By Substrate Compatibility

7.5.6. By End-Use Industry

7.5.7. By Application Focus

8. Company Profiles: Leading Players in the Anti-Corrosion Nanocoating Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. The Sherwin-Williams Company

8.4. Hempel A/S

8.5. Jotun A/S

8.6. Tesla Nanocoatings, Inc.

8.7. NanoVere Technologies, LLC

8.8. P2i Ltd.

8.9. Aculon, Inc.

8.10. NEI Corporation

8.11. Nanofilm Technologies International Limited

8.12. ACTnano, Inc.

8.13. NanoXplore Inc.

8.14. Haydale Graphene Industries PLC

8.15. HZO, Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures