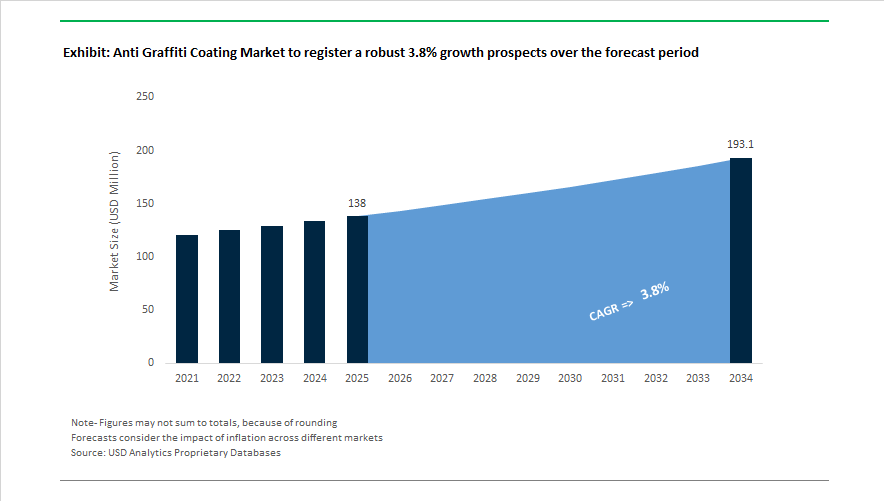

Market Overview: Anti Graffiti Coating Market Expands with $138 Million Valuation in 2025 as Durable Architectural and Infrastructure Protection Technologies Gain Traction

The anti graffiti coating market is valued at $138 Million in 2025 and is projected to reach $193 Million by 2034, registering a CAGR of 3.8%. Demand is anchored in the global expansion of urban infrastructure protection, transportation coatings, architectural metal coatings, and civil asset maintenance programs. Anti-graffiti coatings form a critical segment within protective coatings, industrial coatings, polyurethane topcoats, fluoropolymer coatings, and silicone-based permanent barriers, enabling the removal of spray paints and inks without substrate damage. Growth is influenced by increasing investments in public transit systems, smart city infrastructure, stadiums, airports, tunnels, bridges, and commercial real estate, where vandalism mitigation reduces lifecycle maintenance costs. Formulation advancements emphasize UV resistance, chemical resistance, scratch durability, hydrophobic surfaces, and low-VOC sustainable chemistries, aligning with stricter environmental compliance standards across North America, Europe, and Asia-Pacific.

Technology enhancement activity intensified beginning in 2024 when Wacker Chemie AG broadened the application scope of its silicone-based permanent protective system designed to withstand over 20 cleaning cycles. Strategic market positioning advanced in October 2024 as Nippon Paint outlined its 2024–2026 Southeast Asia industrial coatings expansion plan targeting infrastructure protection. Sustainable additive innovation followed in March 2025 with Evonik launching mass-balanced coating additives for reduced carbon footprint formulations. In June 2025, PPG Industries introduced DURANAR graffiti-resistant architectural metal coatings engineered for easy cleaning. Capacity reinforcement occurred in October 2025 as Evonik established a specialty additives plant in Japan to serve Asian industrial coating demand.

Major portfolio realignment shaped competitive positioning in November 2025 when AkzoNobel and Axalta Coating Systems entered a $25 billion merger agreement combining powder and liquid protective technologies. Infrastructure-linked production expansion continued in December 2025 with AkzoNobel scaling U.S. specialty coatings capacity, while Nippon Paint India launched advanced protective architectural systems. Digitalization entered the market in January 2026 as Sherwin-Williams deployed AI-based coating specification tools. UV durability technologies were highlighted in February 2026 by BASF, enhancing stabilization of clear topcoats. Continued performance innovation is supported through AkzoNobel’s extended motorsport collaboration announced in January 2026, while regulatory filings confirm the merger completion timeline toward late 2026, indicating long-term structural consolidation across global anti-graffiti coating supply chains.

Trends and Opportunities Reshaping Commercial Demand in the Anti Graffiti Coating Market

Municipal Mandates and P3 Procurement Models Are Hardwiring “Protection by Design”

The Anti Graffiti Coating Market is being structurally reshaped by a shift from discretionary repaint-and-clean maintenance budgets toward mandated installation of permanent anti-graffiti coatings during new asset development, driven by municipal procurement and P3 (public-private partnership) financing models. In the United States, the Texas Department of Transportation (TxDOT) DMS-8111 specification, effective October 2025, makes it compulsory for all high-risk infrastructure projects to use Type II (solvent cleanable) or Type III (water cleanable) coatings that demonstrate adhesion and colorfastness retention after multiple cleaning cycles. This embeds coating demand into capital expenditure rather than operating budgets, a structural transformation for market forecasting.

The same trend is visible in EU rolling stock: DBS 918 340 standards in Germany are now mirroring Poland’s PESA requirement that new railcars such as the Elf2 must withstand at least ten full graffiti-removal cycles without damage to OEM livery. This “design-to-protect” model elevates anti-graffiti coatings from optional utilities to contract-bound performance deliverables, creating guaranteed baseline volume in transport projects. Meanwhile, municipal “beautification ROI” reporting from the Graffiti Resource Council (GRC) shows cities using contractual anti-graffiti protection achieve 30 to 50% lower recurring vandalism and cleaning costs, strengthening the finance-case narrative that anti-graffiti coatings are a bankability tool for attracting private co-funding into public infrastructure.

Low-VOC Polysiloxane Systems and Chemical-Resistant Coatings Target Regulatory Compliance and Complex Surfaces

Regulatory tightening under EU REACH Regulation 2025/1090 and EPA solvent restrictions is accelerating the transition toward fluorine-free, tin-free and low-VOC polysiloxane-based anti graffiti coatings. Emerging UV-initiated radical polymerization coatings, featured at the 2025 CoatingsTech Conference, create dynamic repellency and prevent oil-based inks from penetrating porous stone or concrete, a breakthrough for heritage-site preservation where VOC-based removers are prohibited.

Powder-coating innovation is also redefining the sustainability narrative. PPG ENVIROLUXE Plus (May 2025) incorporates 18% post-industrial recycled rPET and delivers a 30% lower carbon footprint without compromising serviceability on transit wraps, highway barriers or decorative façades. This drives ESG-aligned CapEx adoption by airports, stadium builders and high-traffic commercial properties that must demonstrate Scope-3 reductions under investor reporting frameworks.

Opportunities Creating Long-Run Competitive Advantage

Protective Coatings for EV Charging Infrastructure Become a “Critical-Path Component”

The surge in global EV charging infrastructure is creating a structurally new vertical for the Anti Graffiti Coating Market. With 20 million EVs expected on the road in 2025, anti-graffiti protection is now tied directly to charger uptime and revenue capture. Hardware suppliers are integrating surface-protection specifications directly into BOMs to reduce vandalism-related screen failures, which are a top reason for station downtime.

Technology differentiation is widening. Axalta Alesta e-PRO (late 2025) combines anti-graffiti performance with dielectric insulation capable of passing 6KV hipot tests and fire protection up to 1,200°C, enabling a dual-function coating that protects both electronics and brand-visible exterior shells. Market pull is especially pronounced in emerging economies. Under India’s PM E-DRIVE scheme (₹2,000 crore, 2024–2026), chargers must meet defined visibility and durability conditions, triggering demand for anti-fading signage coatings and chemically resistant enamel-top layers for outdoor stations deployed at malls, hotels and highway rest stops.

UV-Stable “Anti-Reflective + Anti-Graffiti” Coatings for Solar Arrays Create a High-Value Niche

Graffiti contamination and urban “soiling” can reduce photovoltaic energy output by up to 30 percent, creating a premium niche for optically clear anti-reflective anti-graffiti coatings for solar glass. Next-generation Smart Anti-Reflective Coatings (ARCs), launched 2025, can enhance panel performance by 3 to 4% while using hydrophobic nanostructures modeled on moth-eye geometry that repel both dust particulates and spray-paint molecules.

For developers operating in desert climates such as Rajasthan and Gujarat, coatings that maintain hydrophobic behavior for decades reduce water-intensive cleaning cycles and help meet ESG water-use reduction targets. Studies show ROI for ARC-integrated anti-graffiti protection is achieved within 6 to 8 months on utility-scale arrays, making this a profitable add-on for EPC contractors and a differentiator for solar OEMs fighting margin compression.

Anti-Graffiti Coating Market Share and Segmentation Insights

Market Share by Product Type: Permanent Systems Lead While Semi-Sacrificial Coatings Gain Momentum

Permanent anti-graffiti coatings account for approximately 52% of global market share in 2025, dominating due to their hard, non-sacrificial barrier that prevents paint adhesion and enables repeated cleaning via solvents or high-pressure washing without damaging the substrate. Polyurethane, polysiloxane, fluoropolymer (PVDF, PTFE), and hybrid sol-gel chemistries are preferred in high-vandalism urban zones, transport assets, and heritage-adjacent infrastructure where lowest lifetime cost outweighs higher upfront investment. Semi-sacrificial coatings represent the fastest-growing segment, combining a permanent base with a removable topcoat that balances cleaning efficiency and recoating cost, making them attractive to budget-conscious facility managers. Sacrificial coatings (acrylics, waxes, polysaccharides) continue to lose share due to frequent reapplication and rising VOC compliance pressure, though they remain relevant for temporary construction protection and low-budget municipalities. Overall demand is increasingly shaped by durability, maintenance economics, and regulatory-driven shifts toward waterborne and high-solids formulations.

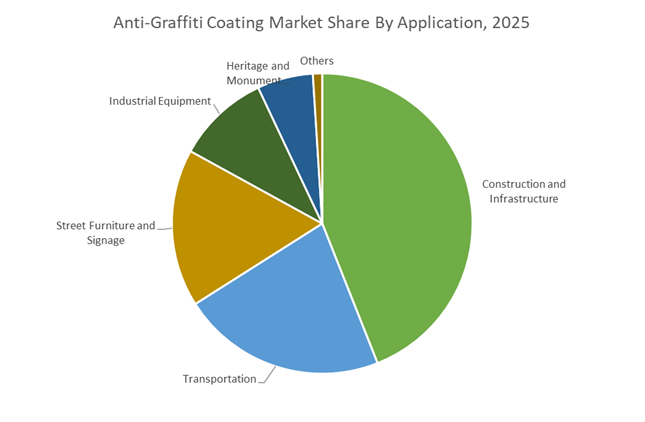

Market Share by Application: Construction Dominates as Transit Assets and Urban Furniture Drive Specification

Construction and infrastructure represent roughly 44% of anti-graffiti coating demand in 2025, covering public buildings, bridges, tunnels, underpasses, and housing estates where vandalism creates persistent maintenance costs. Municipal authorities increasingly specify permanent anti-graffiti systems for high-visibility assets as urbanization accelerates. Transportation ranks second, spanning rail cars, buses, and aviation ground equipment, where graffiti directly impacts service availability and advertising revenue, driving adoption of permanent polyurethane clear coats over branded liveries. Street furniture and signage form a high-exposure, cost-sensitive segment, often favoring semi-sacrificial systems for benches, shelters, bollards, and signal cabinets. Industrial equipment relies on permanent coatings to protect resale value and safety markings. Heritage and monument preservation remains a small but high-value niche, requiring reversible, breathable sacrificial systems. Regionally, North America leads infrastructure volumes, Europe drives low-VOC heritage solutions, and Asia-Pacific is the fastest-growing market on China and India urban expansion.

Anti Graffiti Coating Market Competitive Landscape

The global anti graffiti coating market is rapidly evolving as municipalities, infrastructure developers, and commercial property owners prioritize vandalism resistance, aesthetic preservation, and low-VOC surface protection. Leading manufacturers are advancing permanent and semi-permanent anti graffiti coatings, siloxane and silane technologies, powder-based systems, and waterborne clearcoats to meet rising demand from smart city projects, transit infrastructure, and heritage restoration. Innovation is centered on breathable coatings, non-sacrificial systems, fast-cure formulations, and “one-layer” protection concepts that reduce labor and lifecycle costs. Strategic mergers, regional capacity expansions, and integration of digital monitoring are reshaping competition across North America, Europe, and Asia-Pacific.

Invisible architectural protection and smart city coatings leadership by AkzoNobel N.V.

AkzoNobel leads the anti graffiti coating market through high-transparency architectural finishes engineered to preserve heritage aesthetics while delivering long-term vandalism resistance. Its Dulux Trade Anti-Graffiti Clearcoat, a two-pack water-based polyacrylic system, is widely specified for hospitals and schools due to its low-odor, non-toxic profile. In late 2025, AkzoNobel announced a landmark all-stock merger with Axalta, creating the world’s largest specialized coatings platform by mid-2026. The company is expanding powder and protective coatings capacity in Vietnam and North America to support smart city infrastructure. Its core strength lies in “almost invisible” protection that maintains facade appearance while enabling easy graffiti removal.

Single-component siloxane systems strengthen public works dominance at Sherwin-Williams

Sherwin-Williams dominates North America’s anti graffiti coatings segment with heavy-duty siloxane technologies designed for bridges, rail cars, and highway structures. Its single-component anti graffiti coating forms a non-stick surface, allowing graffiti removal with simple pressure washing or water wipes, reducing labor costs by up to 40% versus multi-part epoxies. In 2026, Sherwin-Williams integrated real-time monitoring sensors into its industrial coating lines, enabling facility managers to detect vandalism hotspots digitally. Engineered for UV resistance and anti-chalking performance, its coatings excel in exposed environments. Cost efficiency, ease of application, and durability make Sherwin-Williams a preferred supplier for large-scale transit and municipal projects.

PVDF-integrated vandal resistance defines PPG Industries’ industrial strategy

PPG Industries differentiates through integrating anti graffiti performance directly into high-end architectural and industrial paint systems. In mid-2025, PPG added validated graffiti resistance to its DURANAR® 70% PVDF coatings, enabling architects to specify a single solution for extreme weather protection and vandalism control. Its Envirocron® P8 Series hybrid powder coatings are formulated without CMR substances, supporting safer indoor transit environments. PPG’s clean technology roadmap prioritizes non-isocyanate hardeners to meet stringent 2026 European regulations. Through coil and extrusion integration, PPG delivers pre-coated metal panels with baked-in anti graffiti protection, streamlining construction workflows and reducing on-site application costs.

Breathable silane protection positions Evonik Industries AG as monument specialist

Evonik leads in breathable anti graffiti solutions for porous substrates such as concrete and natural stone. Its Protectosil® ANTIGRAFFITI range chemically bonds with surfaces, delivering oil and water repellency while remaining fully vapor permeable. The 2025 launch of Protectosil® ANTIGRAFFITI SP introduced a semi-permanent aqueous system capable of withstanding up to five cleaning cycles, making it ideal for historical landmarks. Evonik coatings are used at globally recognized sites, including the Louvre and New York’s World Trade Center subway station. Its non-film-forming technology avoids the plasticized appearance common with conventional coatings, offering invisible protection for culturally sensitive architecture.

Powder-based durability and one-layer efficiency drive Axalta Coating Systems’s urban expansion

Axalta Coating Systems is a global authority in powder-based anti graffiti coatings, serving urban furniture and transportation infrastructure. Its Alesta® AP AntiGraffiti Outdoor delivers permanent graffiti resistance in a single layer while meeting QUALICOAT and GSB architectural standards. In 2025, Axalta expanded production across North America and China to support rising demand for metal-based kiosks, bus shelters, and lockers. The company’s mechanical durability ensures impact and scratch resistance without compromising surface protection. Axalta’s “one-layer economy” strategy eliminates additional clear coats and primers, reducing environmental footprint while improving throughput for high-volume coating operations.

Maintenance-ready solutions and rapid deployment from RPM International Inc. / Rust-Oleum

RPM International, through its Rust-Oleum division, targets the maintenance and repair segment with accessible anti graffiti coatings for commercial and municipal users. GraffitiShield™ creates a permanent hydrophobic barrier that prevents aerosol paint adhesion, while 2025 fast-cure upgrades deliver chemical resistance even in humid coastal climates. RPM integrates anti graffiti with building envelope systems via Tremco and Carboline, combining waterproofing and surface aesthetics. Its urban restoration strategy aligns with rising city beautification funding in 2026, offering bulk-order solutions for rapid deployment. Ease of application, contractor-friendly formats, and integrated repair systems position RPM as a key player in facility management and public infrastructure markets.

United States Anti Graffiti Coating Market: Infrastructure Spending and PFAS Reformulation Set the Pace

The United States remains a technology and specification-led market for anti-graffiti coatings, supported by infrastructure modernization and environmental compliance. In October 2025, the Texas Department of Transportation implemented the revised DMS-8111 specification, introducing stringent pre-qualification standards for solvent-cleanable and water-cleanable anti-graffiti systems used on bridges and highways. These specifications are now acting as reference benchmarks for other state agencies evaluating long-life surface protection.

Federal investment has amplified demand. Under the Infrastructure Investment and Jobs Act, metropolitan authorities in New York and Los Angeles expanded 2025 budgets for urban beautification, prioritizing permanent siloxane-based anti-graffiti coatings on transit hubs, tunnels, and sound walls. On the manufacturing side, Sherwin-Williams announced that its North American production sites for the Invisi-Shield™ series are now powered by renewable electricity credits, strengthening competitiveness in government tenders that emphasize product carbon footprint disclosure. Product innovation has also accelerated, with Axalta launching anti-graffiti powder coatings in early 2025 for smart-city furniture and EV charging stations. Regulatory pressure is reshaping formulations, as 85% of premium U.S. anti-graffiti lines were reformulated by late 2025 to align with California S.B. 903, targeting PFAS elimination ahead of 2030.

Germany Anti Graffiti Coating Market: Rail Standards and Bio-Based Chemistry Redefine Performance Expectations

Germany’s anti-graffiti coating market is driven by rail modernization, sustainability leadership, and circular economy alignment. In early 2025, Deutsche Bahn Systemtechnik updated DBS 918 300 regulations, mandating qualified anti-graffiti systems for all new rolling stock and noise-reduction barriers. These rules emphasize extended maintenance intervals and lifecycle cost reduction, reinforcing demand for high-durability liquid coatings and protective films.

The transition toward greener chemistry is equally influential. Evonik Industries shifted its German polyurethane-additive production assets to green electricity in May 2025, supporting low-VOC cross-linkers used in advanced anti-graffiti formulations. Public funding is reinforcing innovation pipelines, as the Federal Ministry of Transport allocated €15 million in 2025 for research into bio-based silane coatings that provide permanent graffiti resistance without hazardous solvents. Circularity considerations are also shaping product design. AkzoNobel highlighted its Accelshield™ technology at late-2025 trade fairs, demonstrating coatings that preserve substrate recyclability while maintaining long-term surface integrity.

Spain Anti Graffiti Coating Market: Transit Protection and Heritage Preservation Converge

Spain presents a dual-use market where anti-graffiti coatings serve both modern transit systems and historic urban assets. In 2025, Transports Metropolitans de Barcelona reported a 70% reduction in graffiti-related cleaning costs following the widespread application of high-performance anti-graffiti coatings across its 220-train fleet. This outcome has positioned permanent coating systems as a preferred alternative to repeated chemical cleaning.

Technological experimentation is expanding alongside coatings. Spanish research institutions successfully tested ultra-freezing air projection methods in late 2025 as a non-chemical graffiti removal approach on pre-coated railway structures, reinforcing sustainability objectives. At the same time, the Ministry of Culture’s “Patrimonio Limpio” initiative has applied breathable, vapor-permeable anti-graffiti coatings to historic stone monuments in Madrid and Seville, demonstrating how preservation requirements are influencing formulation choices.

China Anti Graffiti Coating Market: Urban Scale and Integrated Chemical Supply Chains Accelerate Adoption

China’s anti-graffiti coating demand is closely linked to rapid urbanization and vertically integrated chemical production. In late 2025, AkzoNobel expanded its Chinese partnerships to accelerate sustainable marine and industrial coatings, including anti-graffiti variants for the high-speed rail network. National smart city budgets in 2025 included a dedicated $200 million allocation for protective coatings on tunnels and bridges, underscoring the role of anti-graffiti systems in long-term infrastructure resilience.

Local innovation is also advancing. Manufacturers in the Jiangsu chemical corridor reported a 15% increase in amino acid-based bio-additives for mild, water-borne anti-graffiti finishes during 2025. Supply chain localization is strengthening competitiveness, as the startup of the BASF Zhanjiang Verbund site has localized production of acrylic and amine precursors critical to the domestic anti-graffiti coating value chain.

Japan Anti Graffiti Coating Market: High-Purity Standards and Asset Longevity Focus

Japan’s anti-graffiti coating market is characterized by precision standards and aging infrastructure priorities. Firms such as Tosoh Corporation commercialized ultra-high-purity surface treatments in 2025 that function as anti-graffiti agents for clean-room facilities and high-tech electronic enclosures, where contamination control is critical. These dual-use applications illustrate how electronics manufacturing standards are influencing surface protection technologies.

Policy direction reinforces long-term durability. The Ministry of Land, Infrastructure, Transport and Tourism mandated in 2025 that bridge rehabilitation projects incorporate fluorinated anti-graffiti topcoats, with the objective of extending asset life by an estimated 15 years. This requirement positions anti-graffiti coatings as a strategic maintenance tool rather than a cosmetic add-on.

Country-Level Strategic Drivers in the Anti-Graffiti Coating Industry

Anti-Graffiti Coating Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Industry Implication

|

|

United States

|

Infrastructure spending and PFAS reformulation

|

Specification-driven adoption and premium innovation

|

|

Germany

|

Rail modernization and bio-based chemistry

|

High-durability, low-VOC systems with circularity focus

|

|

Spain

|

Transit cost reduction and heritage protection

|

Permanent coatings and non-chemical removal synergy

|

|

China

|

Smart city expansion and integrated supply chains

|

Large-scale deployment with localized raw materials

|

|

Japan

|

High-purity standards and infrastructure longevity

|

Precision coatings for extended asset lifecycle

|

Anti-Graffiti Coating Market Report Scope

Anti Graffiti Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$138 Million

|

|

Market Size (2034)

|

$193 Million

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Product Type (Permanent Anti Graffiti Coatings, Sacrificial Anti Graffiti Coatings, Semi Sacrificial Anti Graffiti Coatings), By Technology (Water Borne Coatings, Solvent Borne Coatings, Powder Coatings, UV Curable Coatings), By Substrate (Concrete and Masonry, Metals, Wood, Glass and Plastics), By Application (Transportation, Construction and Infrastructure, Industrial Equipment, Street Furniture and Signage, Heritage and Monument Preservation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin Williams Company, Akzo Nobel NV, PPG Industries Inc, Axalta Coating Systems, BASF SE, Evonik Industries AG, 3M Company, Jotun, Kansai Paint, Nippon Paint Holdings, RPM International Inc, Wacker Chemie AG, Hempel AS, Dow Inc, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Graffiti Coating Market Segmentation

By Product Type

- Permanent Anti Graffiti Coatings

- Sacrificial Anti Graffiti Coatings

- Semi Sacrificial Anti Graffiti Coatings

By Technology

- Water Borne Coatings

- Solvent Borne Coatings

- Powder Coatings

- UV Curable Coatings

By Substrate

- Concrete and Masonry

- Metals

- Wood

- Glass and Plastics

By Application

- Transportation

- Construction and Infrastructure

- Industrial Equipment

- Street Furniture and Signage

- Heritage and Monument Preservation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Graffiti Coating Industry

- Sherwin Williams Company

- Akzo Nobel NV

- PPG Industries Inc

- Axalta Coating Systems

- BASF SE

- Evonik Industries AG

- 3M Company

- Jotun

- Kansai Paint

- Nippon Paint Holdings

- RPM International Inc

- Wacker Chemie AG

- Hempel AS

- Dow Inc

- Sika AG

*- List not Exhaustive