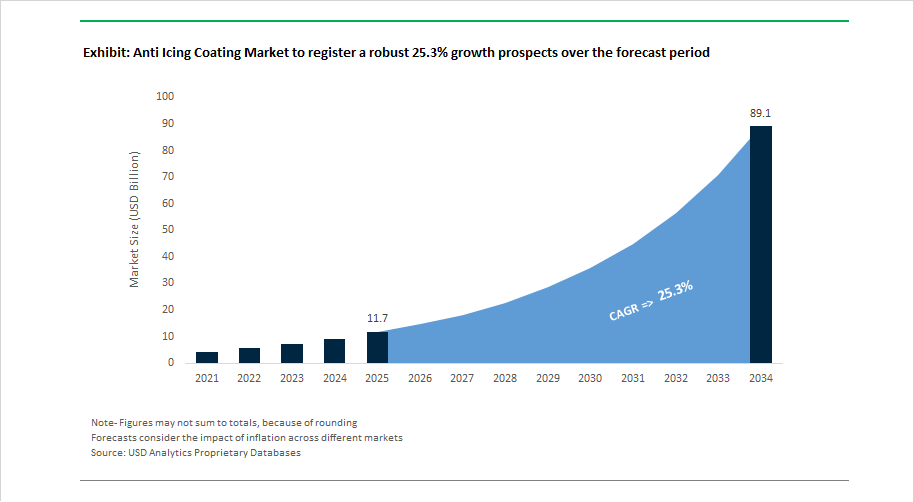

Market Overview: Anti Icing Coating Market Accelerates Toward $89.1 Billion by 2034 as Aerospace, Marine, Energy, and Automotive Sectors Adopt Ice-Phobic Surface Technologies

The anti icing coating market is valued at $11.7 billion in 2025 and is forecast to reach $89.1 billion by 2034, advancing at an exceptional 25.3% CAGR. Growth is fueled by cross-sector demand for ice-phobic coatings, superhydrophobic surfaces, silicone-based marine coatings, aerospace anti-icing layers, erosion-resistant topcoats, and low-energy ice protection systems. Industries including commercial aviation, naval shipping, offshore energy, wind power, automotive autonomy, and solar infrastructure require coatings that delay ice nucleation, reduce adhesion strength of frost, and maintain surface functionality in sub-zero environments. Market development is closely linked to regulatory pressures aimed at reducing chemical de-icing fluids, improving energy efficiency, and ensuring operational reliability of sensors, wings, turbines, and marine hulls in extreme climates.

Regulatory and performance catalysts emerged in May 2024 when PPG Industries saw global marine adoption of NEXEON technology that minimizes ice and fouling adhesion. Aviation compliance tightened in late 2024 as the Federal Aviation Administration updated winter ground de-icing guidance, accelerating interest in permanent anti-icing coatings. Breakthrough material science followed in April 2025 with Adaptive Surface Technologies introducing photothermal anti-ice chemistry, while Fraunhofer IFAM validated hybrid superhydrophobic and conductive systems during 2025 testing. Aerospace R&D expanded under the EU Clean Aviation program during 2025 with erosion-resistant anti-icing wing concepts entering evaluation. Supply chain strategy shifted in September 2025 after U.S. tariff actions encouraged localized sourcing of specialty anti-icing additives.

Industrial deployment accelerated in October 2025 as Hempel introduced rapid-curing infrastructure coatings supporting arctic energy applications. Capacity and aerospace specialization strengthened in December 2025 when AkzoNobel invested €50 million in Illinois to expand advanced aircraft coating output. Automotive innovation appeared in January 2026 as General Motors filed patents for anti-icing sensor protection coatings. Marine deployment milestones followed in February 2026 with Hempel’s next-generation silicone coating applied on Maersk vessels, while AkzoNobel launched single-coat aerospace systems optimized for reduced ice adhesion. Leadership transition at Hempel in January 2026 confirmed continued focus on sustainable protective coatings.

Trends and Opportunities Reshaping Commercial Scale and Technology Strategy in the Anti Icing Coating Market

Aviation is Moving from Reactive Fluid De-icing to a “Prevention First” Coating Strategy

Demand in the Anti Icing Coating Market is being reshaped by a structural shift in aviation: coatings are now being treated as primary enablers of turnaround efficiency, not accessories. Under the FAA Annual Modal Research Plan (2024–2025), certification workstreams for “icephobic surface technologies” are prioritizing Holdover Time (HOT) improvements, meaning coatings must demonstrate measurable reductions in ice adhesion before take-off. In commercial airports, OEM adoption is tied directly to cost and carbon-reduction targets: glycol-based Types I and IV de-icing fluids face scrutiny for soil and groundwater contamination, driving airport operators to specify pre-treated ground equipment as a CapEx standard. Textron GSE’s Safeaero 220E (October 2025), the world’s first all-electric de-icer, highlights integration economics: its uptake is 35% higher when deployed on fleets already pre-coated with ice-shedding surfaces, because fluid load and dwell time are reduced. For Tier-1 airlines, the decision logic is shifting from “buy cleaning equipment” to “treat the asset so it does not freeze.” This is accelerating volume away from episodic winter-season procurement and toward continuous coating retrofits embedded in aircraft MRO contracts.

Marine and Offshore Buyers Require Ice-Repellent Coatings that Survive Mechanical Impact and Regulatory Scrutiny

The Marine Anti Icing Coating Market is entering a high-stakes compliance phase. The FuelEU Maritime Regulation (Jan 1, 2025) is pushing fleet operators to decarbonize, making drag-inducing ice weight a financial liability. Technical validation data presented at the Arctic Shipping Summit (Montreal, Nov 2025) shows next-generation epoxy-modified silicone coatings can maintain ice adhesion strength below 0.1 MPa, meaning hull ice sheds under vessel motion alone. The performance obligation is not purely mechanical: formulations must be fluorine-free and fully water-based to meet EU Biocidal Products compliance. This is especially relevant for ice-melt scenarios in fragile Arctic zones, where additives leaching into meltwater is now a procurement red-flag. Demand is expanding beyond hulls into deck equipment, superstructures and oil-rig walkways, as safety regulators require surfaces that prevent ice-slip injuries.

Anti-icing Coatings Become a Mission-Critical Input for UAV and Drone Commercialization

Drone reliability in cold regions is now a design constraint for entire business models (medical delivery, defense reconnaissance, mining logistics). The SINTEF IceMan Project (2025) achieved a milestone: a polyurethane-based coating that delays freezing by more than four hours at –5°C, with lower embodied weight than battery-powered heating systems. Coatings are becoming part of UAV “baseline BOM requirements” in procurement frameworks for defense and medical-grade aircraft. Technology convergence is accelerating: University of Toronto (Dec 2025) demonstrated TENG-equipped anti-icing films that activate heat only when sensors detect ice, reducing energy load by up to 80% relative to constant-on heating systems. For investors and OEMs, coatings are no longer maintenance add-ons—they unlock fleet-availability economics, making “all-weather” drone operations viable in northern markets.

Anti-icing Coatings Protect Renewable Energy Assets from Cold-Weather Downtime and Power Loss

The Renewable Energy Anti Icing Coating Market is emerging as one of the most profitable fast-scaling segments. Wind turbine field data (UniVOOK Industry, 2025) confirms that superhydrophobic nanocoatings increase winter AEP (annual energy production) by more than 20 percent, eliminating aerodynamic drag caused by ice buildup. The HYDROBOND project (EU CORDIS) validated passive paints achieving ice-adhesion of 30 kPa, outperforming traditional coating benchmarks and enabling blade-weight reduction because heavy internal thermal systems are no longer required. In solar PV, icing risk is compounded by snow load and structural stress. A 2025 RSC Applied Polymers study highlights multi-functional coatings combining anti-reflection, self-cleaning and anti-icing layers, ensuring light transmission and snow shedding without external power input. For utility operators, ROI is quantifiable: eliminating ice-related downtime and reducing snow-removal maintenance produces sub-12-month payback periods on coating investments.

Anti-Icing Coating Market Share and Segmentation Insights

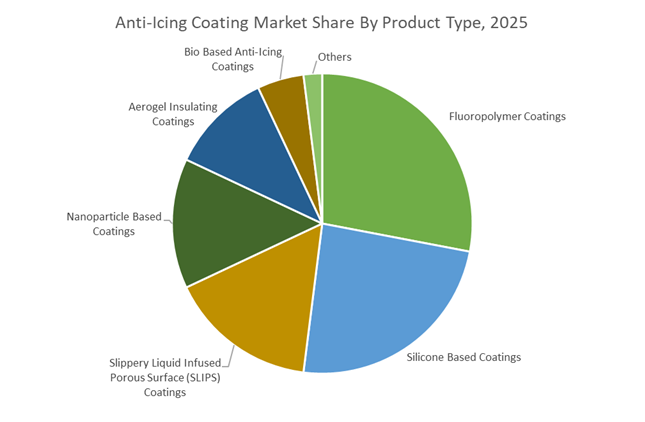

Market Share by Product Type: Fluoropolymers Lead While SLIPS Technology Accelerates Adoption

Fluoropolymer coatings account for approximately 28% of the global anti-icing coating market in 2025, leading due to exceptional durability, ultra-low surface energy, and long-term weatherability in extreme climates. These coatings are widely specified for aerospace structures, wind turbine blades, and critical infrastructure where reapplication is costly or impractical. Silicone-based anti-icing coatings rank second, offering flexibility, ease of spray application, and cost efficiency in moderate icing environments, particularly across automotive and industrial applications. SLIPS (Slippery Liquid Infused Porous Surface) coatings represent the fastest-growing segment, leveraging biomimetic surface engineering to achieve extremely low ice adhesion strength, enabling passive ice shedding. Nanoparticle-based coatings support hydrophobic performance enhancements, while aerogel insulating coatings occupy a strategic niche for subsea pipelines and cryogenic tanks by preventing thermal-driven ice formation. Bio-based anti-icing coatings remain emerging, supported by EU green policies and PFAS restrictions, although performance parity remains under development.

Market Share by Application: Aviation Dominates While Wind Energy Emerges as Growth Engine

Aviation and aerospace represent approximately 31% of global anti-icing coating demand in 2025, as ice accumulation on wings, sensors, and radomes presents critical safety risks. High-performance fluoropolymer systems dominate due to stringent FAA and EASA certification requirements and the need for durable de-icing performance. Renewable energy, particularly wind turbines in cold climates, is the fastest-growing application, with blade icing reducing annual energy output by up to 20% and accelerating fatigue. Power transmission infrastructure forms a strategic segment, as ice-induced conductor galloping and flashovers threaten grid reliability. Automotive applications focus on ADAS sensors, LIDAR, and mirror systems, though windshield integration remains constrained by abrasion from wiper systems. Construction and architectural applications are smaller but expanding in heavy snowfall regions, where anti-icing coatings mitigate ice dam formation and falling ice hazards on facades and roofing systems.

Anti Icing Coating Market Competitive Landscape

The global anti icing coating market is advancing rapidly as aerospace, wind energy, smart infrastructure, and autonomous mobility sectors demand ice-phobic surfaces, conductive coatings, and energy-efficient de-icing technologies. Leading manufacturers are investing heavily in nanomaterials, superhydrophobic topcoats, ceramic-polymer hybrids, and bio-inspired chemistries to reduce ice adhesion, improve aerodynamic efficiency, and extend asset uptime in extreme climates. Strategic OEM partnerships, regional MRO expansions, and sustainability-driven innovations such as PFAS-free and low-VOC anti icing coatings are reshaping competition across North America, Europe, and Asia-Pacific, positioning advanced surface engineering as a core enabler of climate-resilient infrastructure.

Aerospace-grade multi-layer anti icing systems define leadership at PPG Industries, Inc.

PPG dominates the aerospace anti icing coating market through its advanced multi-layer systems combining conductive sub-layers with superhydrophobic topcoats that reduce ice adhesion by over 90%. In late 2025, PPG secured long-term OEM integration contracts, reinforcing its 25% share of the regional jet segment. Its 2026 nanomaterial-infused coating uses carbon nanotubes to deliver uniform thermal distribution across wing leading edges, cutting aircraft energy draw by 30%. The company’s strategic focus on aerodynamic efficiency targets ultra-smooth, ice-phobic surfaces that maintain low drag even under SLD conditions. Deep chemical integration enables PPG to scale high-performance anti icing solutions across aviation and renewable energy platforms.

Speed-to-market aviation coatings accelerate growth for AkzoNobel N.V.

AkzoNobel has positioned itself as a rapid-response leader in aerospace anti icing coatings through localized blending and MRO support. In January 2026, it opened a Dubai Aerospace Coatings Hub to serve Middle East and North Africa aviation markets, while upgrading its Waukegan, Illinois facility in late 2025 with automated high-speed dissolvers for Aerodur™ anti-ice products. Its Industrial Excellence program integrates digital color matching with ice-phobic performance, allowing airlines to preserve brand liveries while upgrading de-icing protection. Regulatory strength is evident through extended CAAC approval at Dongguan, enabling certified supply to the COMAC C919 program and strengthening AkzoNobel’s Asia-Pacific footprint.

Ceramic-polymer hybrids power infrastructure resilience at The Sherwin-Williams Company

Sherwin-Williams leads harsh-climate infrastructure applications with ceramic-polymer hybrid anti icing coatings engineered for bridges, power grids, and transit systems. Its SkyGuard™ conductive coating prevents ice accretion on telecom towers through passive and active mechanisms, while the CM0485115 aerospace undercoat delivers lightning strike protection alongside thermal anti-icing performance. The company is aggressively transitioning toward low-VOC, waterborne formulations to comply with 2026 global environmental standards. Sherwin-Williams’ deep expertise in ceramic chemistry provides superior abrasion resistance against hail and ice crystal impact, outperforming soft silicone systems and positioning the brand as a preferred partner for long-life, low-maintenance cold-weather infrastructure.

Offshore wind blade protection anchors Hempel A/S’s anti icing strategy

Hempel is the wind energy specialist in the anti icing coating market, dominating offshore turbine blade protection across North Sea and Arctic corridors. Its coatings address leading edge erosion while actively repelling ice that can destabilize rotor balance. In late 2025, Hempel launched Hempaprime Strength 530, the first ice-phobic epoxy certified to NORSOK M-501 Edition 7 for extreme maritime environments. Through its “Power of Less” initiative, the company focuses on life-extension coatings that reduce maintenance intervals and improve turbine uptime. Hempel targets sustainability-driven performance, aiming to help customers avoid 50 million tonnes of CO2e by 2030 through uninterrupted renewable energy generation.

Heavy-duty marine and industrial anti icing solutions strengthen Jotun A/S

Jotun leverages its heritage in ice-class marine coatings to dominate heavy-duty industrial anti icing applications. Its Marathon IQ2 system, recognized by Lloyd’s Register, combines extreme abrasion resistance with ice-slip properties for ice-going vessels and offshore platforms. In 2026, Jotun expanded distribution in Dubai and Singapore to support offshore energy infrastructure requiring splash-zone ice protection. Digital maintenance monitoring enables real-time tracking of ice-bond strength and surface degradation, while zinc-rich and hybrid epoxy technologies prevent under-film corrosion caused by freeze-thaw cycles. Jotun’s integrated approach positions it as a strategic partner for resilient maritime and Arctic industrial assets.

Bio-inspired ice-phobic innovation disrupts the market at Adaptive Surface Technologies

Adaptive Surface Technologies is redefining anti icing coatings through bio-mimicry and Liquid-Gated Porous Surfaces (SLIPS) technology. In April 2025, it introduced a photothermal anti-ice coating that uses marine-based additives to absorb solar radiation and passively warm aluminum substrates, delaying frost formation. The company’s self-healing slippery surfaces make mechanical ice bonding virtually impossible, opening high-growth opportunities in smart mobility, including LiDAR and camera sensors for autonomous vehicles. In early 2026, partnerships with renewable energy OEMs accelerated pilots of fluorine-free ice-phobic coatings, anticipating PFAS bans across the EU and North America and reinforcing its role as the market’s primary disruptor.

United States Anti Icing Coating Market: Grid Resilience, Aviation Funding, and PFAS-Free Reformulation

The United States represents one of the most policy-driven and application-diverse markets for anti-icing coatings. In 2025, the U.S. Department of Energy launched pilot programs across Midwest states to retrofit power transmission lines with passive anti-icing nanocoatings. These initiatives directly respond to federal assessments linking ice-load failures to widespread winter grid disruptions, positioning surface coatings as a preventive infrastructure tool rather than an operational add-on.

Aviation and defense remain critical innovation engines. The Air Force Research Laboratory awarded multi-million-dollar contracts in early 2025 to scale Slippery Liquid-Infused Porous Surfaces for large military transport aircraft, accelerating the transition from laboratory-scale icephobic surfaces to flight-certified systems. At the state level, departments such as Florida DOT reported the pre-treatment of more than 600 critical bridges by late 2025, contributing to a 40% reduction in I-10 closures during severe winter events. Regulatory pressure is reshaping formulations, as enforceable PFAS limits adopted by 11 states in 2025 have driven companies like NEI Corporation to commercialize fluorine-free superhydrophobic coatings for automotive sensors, EV charging ports, and autonomous vehicle optics. Venture funding also remains active, with Frostless Materials scaling transparent anti-ice coatings for LiDAR and optical hardware used in autonomous mobility platforms.

Germany Anti Icing Coating Market: Automotive Leadership and Energy Transition Use Cases

Germany’s anti-icing coating landscape is defined by automotive engineering leadership, rail modernization, and renewable energy integration. In Q2 2025, AkzoNobel unveiled next-generation anti-icing systems featuring self-replenishing lubricant reservoirs, extending service life for windshields and sensor coatings by 50%. These innovations align closely with the needs of advanced driver assistance systems and sensor-dense vehicles.

Public infrastructure programs are equally influential. Deutsche Bahn expanded testing of smart composite coatings for high-speed rail in 2025, utilizing thermal-responsive additives that activate only when surface temperatures fall below freezing. Research-backed innovation is supported through federal funding, as the BMBF-backed Nanodyn project demonstrated plasma-functionalized nanostructured films that reduce ice adhesion by over 90% compared to conventional polyurethane coatings. In renewable energy, northern wind farm operators adopted nanocoatings in 2025 to reduce winter energy losses from blade icing by roughly 30%. Sustainability compliance is accelerating material shifts, with German additive leaders phasing out PFAS-containing components in favor of non-polymeric silicone alternatives to meet EU REACH expectations.

Canada Anti Icing Coating Market: Cold-Climate Validation and UAV Enablement

Canada’s role in the anti-icing coating industry centers on extreme climate validation and emerging aerial mobility use cases. In 2025, partnerships between NEI Corporation and Canadian energy providers enabled the deployment of SLIPS-based coatings on wind turbines, achieving a 40% reduction in ice-related downtime in Arctic and sub-Arctic conditions. These results have strengthened confidence in passive icephobic technologies for long-duration cold exposure.

Beyond energy, Canada has emerged as a testing ground for UAV resilience. IceGuard Systems commercialized spray-on anti-ice coatings in late 2025 for medical delivery drones, allowing operations in freezing rain zones previously deemed non-operational. Telecommunications infrastructure has also benefited, as major operators invested in polyurethane-based anti-ice films to protect remote 5G towers from ice-induced signal attenuation.

Norway Anti Icing Coating Market: Marine Safety and Bio-Based Icephobic Materials

Norway’s anti-icing coating development is tightly linked to offshore safety and environmental stewardship. Researchers at SINTEF announced in September 2025 a water-based, fluorine-free UAV coating capable of delaying ice formation by more than four hours at minus five degrees Celsius. This breakthrough supports drone operations in polar logistics and offshore inspection.

Regulatory drivers are reinforcing adoption. In 2025, Norwegian maritime authorities mandated anti-ice coatings on lifeboats and helidecks for vessels operating in the Barents Sea, elevating coatings from optional safety enhancements to compliance-critical systems. SINTEF’s work on renewable polymer additives further highlights Norway’s emphasis on bio-based solutions that retain icephobic performance while remaining suitable for sensitive marine ecosystems.

Japan Anti Icing Coating Market: Smart Transport and Electronics-Centric Applications

Japan’s anti-icing coating market emphasizes precision, electronics protection, and automation. In 2025, the Ministry of Land, Infrastructure, Transport and Tourism initiated trials of photocatalytic anti-icing surfaces on highway signage and traffic cameras, aiming to reduce manual maintenance and improve road safety during winter conditions.

Electronics manufacturers are driving parallel innovation. Japanese OEMs such as Sumitomo introduced ultra-thin molecular coatings for outdoor surveillance cameras in 2025, maintaining optical clarity in sub-zero humidity without energy-intensive heating elements. These developments position anti-icing coatings as enablers of energy-efficient smart city infrastructure.

China Anti Icing Coating Market: Wind Power Scale and Conductive Coating Integration

China’s anti-icing coating demand is closely tied to renewable energy expansion and industrial scale-up. In 2025, authorities mandated the use of nanoparticle-based anti-icing coatings on more than 1,500 new wind turbines across the Inner Mongolia wind belt, reflecting the strategic importance of ice mitigation for grid stability in northern regions.

Material innovation is supporting electro-thermal de-icing systems. At ChinaCoat 2025, Birla Carbon highlighted new conductive carbon-black grades optimized for anti-icing coatings, enhancing heat distribution and efficiency in electrically assisted de-icing solutions. This integration of materials science and energy infrastructure underscores China’s focus on scalable, performance-driven anti-icing technologies.

Country-Level Strategic Drivers in the Anti-Icing Coating Industry

Anti-Icing Coating Market County Level Snapshot

|

Country

|

Core Adoption Driver

|

Strategic Implication

|

|

United States

|

Grid resilience, aviation safety, PFAS regulation

|

Rapid commercialization of fluorine-free, multi-sector coatings

|

|

Germany

|

Automotive sensors, rail, wind energy

|

High-durability, self-replenishing and low-PFAS systems

|

|

Canada

|

Extreme climate validation, UAV operations

|

Proven performance in Arctic and sub-Arctic environments

|

|

Norway

|

Offshore safety, bio-based materials

|

Environmentally compatible icephobic solutions

|

|

Japan

|

Smart transport, electronics protection

|

Ultra-thin, energy-efficient surface treatments

|

|

China

|

Wind power scale, conductive materials

|

Large-scale deployment and electro-thermal integration

|

Anti-Icing Coating Market Report Scope

Anti Icing Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.7 Billion

|

|

Market Size (2034)

|

$89.1 Billion

|

|

Market Growth Rate

|

25.3%

|

|

Segments

|

By Product Type (Nanoparticle Based Coatings, Fluoropolymer Coatings, Silicone Based Coatings, Aerogel Insulating Coatings, Slippery Liquid Infused Porous Surface Coatings, Bio Based Anti Icing Coatings), By Technology (Passive Anti Icing, Active Anti Icing, Hybrid Anti Icing Systems), By Substrate (Metals, Glass and Optics, Concrete and Ceramics, Polymers and Composites), By Application (Aviation and Aerospace, Renewable Energy, Power Transmission and Telecommunications, Automotive and Transportation, Industrial and Marine, Construction and Architecture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries Inc, Akzo Nobel NV, 3M Company, Dow Inc, Evonik Industries AG, Huntsman Corporation, NEI Corporation, Elemental Coatings, Cytonix, Battelle Memorial Institute, Fraunhofer Gesellschaft, Nanosonic, NeverWet, Aerospace and Advanced Composites, HennTech

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Icing Coating Market Segmentation

By Product Type

- Nanoparticle Based Coatings

- Fluoropolymer Coatings

- Silicone Based Coatings

- Aerogel Insulating Coatings

- Slippery Liquid Infused Porous Surface Coatings

- Bio Based Anti Icing Coatings

By Technology

- Passive Anti Icing

- Active Anti Icing

- Hybrid Anti Icing Systems

By Substrate

- Metals

- Glass and Optics

- Concrete and Ceramics

- Polymers and Composites

By Application

- Aviation and Aerospace

- Renewable Energy

- Power Transmission and Telecommunications

- Automotive and Transportation

- Industrial and Marine

- Construction and Architecture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Icing Coating Industry

- PPG Industries Inc

- Akzo Nobel NV

- 3M Company

- Dow Inc

- Evonik Industries AG

- Huntsman Corporation

- NEI Corporation

- Elemental Coatings

- Cytonix

- Battelle Memorial Institute

- Fraunhofer Gesellschaft

- Nanosonic

- NeverWet

- Aerospace and Advanced Composites

- HennTech

*- List not Exhaustive