Anti-Slip Coatings Market Size and Growth Driven by Workplace Safety Compliance and Infrastructure Demand

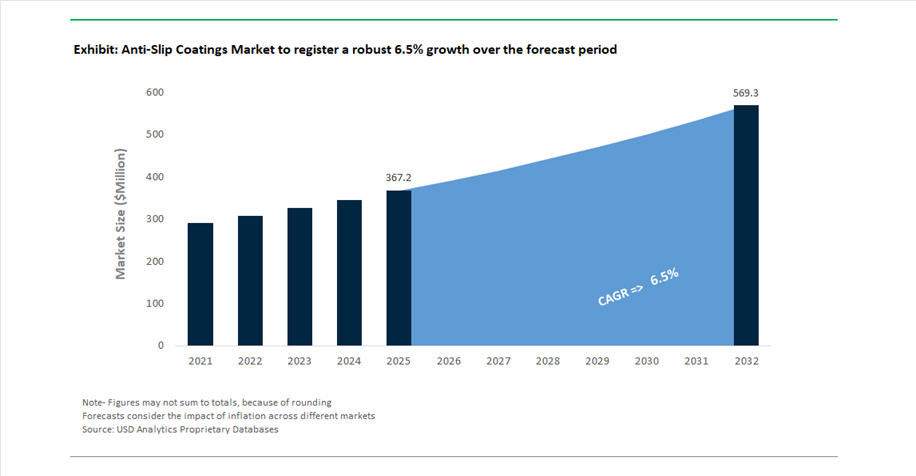

The Anti-Slip Coatings Market is valued at USD 367.2 million in 2025 and is projected to reach USD 570.6 million by 2032, expanding at a CAGR of 6.5%. This growth is fundamentally driven by the rising emphasis on workplace safety standards, regulatory compliance, and accident prevention across industrial, commercial, and residential environments. As slip-and-fall incidents remain a major cause of workplace injuries globally, anti-slip coatings are becoming a mandatory safety solution rather than an optional enhancement.

These coatings are engineered to provide high-friction surfaces through the incorporation of aggregates or textured finishes, ensuring traction even under wet, oily, or high-traffic conditions. Key application areas include marine decks, industrial walkways, ramps, staircases, commercial flooring, and transportation infrastructure, where safety and durability are critical. Regulatory frameworks such as OSHA and ADA guidelines are compelling industries to adopt certified anti-slip systems, particularly in sectors like oil & gas, marine, construction, manufacturing, and public infrastructure.

The market is also benefiting from increasing investments in infrastructure modernization, urban development, and transportation safety, especially in emerging economies. Additionally, there is growing demand for multi-functional coatings that combine anti-slip properties with corrosion resistance, fire protection, and weather durability, enabling broader application across complex industrial environments. Technological advancements are focused on fast-curing, high-solids, and environmentally compliant formulations, including water-based systems that meet sustainability requirements without compromising performance.

From a competitive standpoint, the market is shaped by product innovation, strategic acquisitions, and cross-segment integration, with manufacturers leveraging expertise in performance coatings to deliver high-durability, application-specific solutions. The increasing intersection of safety, sustainability, and operational efficiency is positioning anti-slip coatings as a critical component of modern surface protection systems

Strategic Consolidation, Safety-Driven Innovation, and Industrial Applications Expanding Market Scope

The anti-slip coatings market is evolving rapidly through strategic mergers, advanced product development, and expanding industrial applications. A major industry development occurred in March 2026, when AkzoNobel and Axalta announced a merger of equals, creating a global coatings leader with enhanced capabilities in performance coatings. This consolidation is particularly significant for anti-slip technologies, combining AkzoNobel’s expertise in marine deck coatings with Axalta’s advanced industrial flooring systems, strengthening innovation in high-traction surface solutions.

Product innovation is increasingly focused on integrated safety systems. In March 2025, Hempel launched Hempafire Extreme 550, an epoxy passive fire protection coating designed to work alongside anti-slip topcoats, enabling dual-function solutions for industrial steel structures where both fire safety and slip resistance are essential. Similarly, Jotun’s June 2025 introduction of advanced powder coatings for EV battery systems incorporates textured surfaces that enhance slip resistance, addressing safety needs in emerging sectors such as electric mobility and energy storage.

Strategic investments and acquisitions are reinforcing market capabilities. RPM International’s acquisition of Ready Seal Inc. (June 2025) expands its portfolio in wood coatings, where anti-slip additives are widely used for decks and outdoor walkways. Additionally, RPM’s Innovation Center of Excellence (January 2024) is accelerating the development of fast-curing, high-performance anti-slip formulations, aligning with evolving safety regulations.

Marine and transportation sectors continue to be key growth areas. AkzoNobel’s March 2026 contract to supply anti-slip coatings for high-capacity ferries highlights the importance of durable, high-friction surfaces in wet and high-traffic maritime environments. Similarly, Hempel’s successful application of Hempaguard NB (February 2026) demonstrates the integration of hull performance systems with deck safety coatings, ensuring comprehensive protection for newbuild vessels.

Capacity expansion and product diversification are also shaping the competitive landscape. AkzoNobel’s $50 million upgrade to its Waukegan aerospace facility (February 2026) supports increased production of specialized aircraft walk-way coatings, while Henkel’s April 2026 expansion into anti-skid paper coatings introduces high-traction barrier solutions for logistics and packaging, reducing slippage during transport.

Stringent OSHA and EU-OSHA Standards Driving Adoption of Certified High-Traction Coatings

The anti-slip coatings industry is experiencing a regulatory-driven surge as workplace safety authorities intensify enforcement of slip resistance standards. OSHA’s 2026 inspection priorities place significant emphasis on fall protection, with slips and trips consistently ranking among the most cited workplace violations. Approximately 35,000 inspections annually are expected to focus on identifying non-compliant flooring conditions, particularly in high-risk environments such as manufacturing plants, warehouses, and food processing facilities where moisture and oil exposure are prevalent.

The financial implications of non-compliance are substantial. OSHA penalty structures now allow fines of up to $16,550 per serious violation and over $165,000 for repeated or willful breaches, compelling facility operators to adopt certified anti-slip coatings as a proactive risk mitigation strategy. In parallel, European and UK safety frameworks are standardizing the use of the Pendulum Test Value as a quantitative measure of slip resistance. Industrial flooring systems are increasingly required to achieve a minimum PTV of 36 under wet conditions to be classified as low slip risk, setting a clear performance benchmark for coating manufacturers.

This shift toward measurable compliance has elevated the importance of coatings that deliver consistent friction performance over time. Aggregate-reinforced systems incorporating aluminum oxide, quartz, or silicon carbide are gaining traction due to their ability to maintain high Coefficient of Friction values under heavy wear conditions. Additionally, regulatory mandates are driving the need for documented proof of compliance, leading to increased adoption of coatings that are pre-certified and supported by laboratory test data.

100% Solids Epoxy and Polyaspartic Systems Dominating High-Durability Anti-Slip Applications

The transition toward 100% solids epoxy and polyaspartic coating systems is redefining performance standards in the anti-slip coatings market. Driven by stricter VOC regulations and the need for enhanced durability, these advanced formulations are rapidly replacing traditional solvent-borne systems. By 2026, waterborne and 100% solids chemistries are expected to account for more than 60% of new industrial coating specifications, reflecting a clear industry-wide shift toward environmentally compliant solutions.

High-build epoxy coatings offer a structurally robust matrix capable of suspending larger anti-slip aggregates, resulting in significantly improved wear resistance and extended service life. Compared to thin-film solvent-based coatings, these systems can increase operational lifespan by up to 50%, making them particularly suitable for high-traffic environments and heavy-duty industrial applications. Adhesion performance has also improved, with modern epoxy systems engineered to bond effectively with concrete substrates while withstanding mechanical stress from automated equipment and repeated chemical wash-down cycles in smart manufacturing facilities.

Polyaspartic coatings further enhance operational efficiency through rapid curing capabilities. Facilities can resume full operations within 2 to 4 hours of application, a critical advantage in industries where downtime costs can exceed $10,000 per hour. This fast return-to-service capability is driving adoption in sectors requiring continuous production cycles, including logistics, automotive manufacturing, and pharmaceuticals.

The convergence of low-VOC compliance, durability, and rapid curing is positioning 100% solids epoxy and polyaspartic systems as the preferred choice for next-generation anti-slip coatings, enabling manufacturers to meet both regulatory and operational performance requirements.

Offshore Wind Infrastructure Driving Demand for High-Performance Anti-Slip Coatings

The expansion of offshore wind energy is creating a specialized demand segment for anti-slip coatings designed to operate under extreme environmental conditions. Transition pieces and access platforms on offshore wind turbines require coatings that provide reliable traction while resisting continuous exposure to saltwater, UV radiation, and biological fouling.

Performance requirements in this segment are stringent. Anti-slip coatings must maintain a Coefficient of Friction of approximately 1:1, ensuring safe footing even under wet and contaminated conditions. Traditional epoxy-based non-skid coatings are increasingly being supplemented or replaced by advanced thermal spray systems utilizing cored wires filled with materials such as aluminum or silicon carbide. These next-generation coatings are up to 45% lighter than conventional high-build systems, contributing to reduced structural load on offshore platforms.

Lifecycle durability is a key decision factor for operators. Given the high cost and logistical complexity of offshore maintenance, coatings are expected to deliver service lifespans of up to 10 years without requiring reapplication. This is driving interest in dual-function coatings that combine anti-slip properties with C5-M grade corrosion protection, reducing the need for multiple coating layers and simplifying maintenance strategies.

Urban Transit Expansion Fueling Demand for Anti-Slip Flooring Solutions in Public Transportation

The modernization of urban transportation systems is creating a substantial opportunity for anti-slip coatings in public transit applications. Regulatory mandates, such as India’s AIS-216 standard, are driving the widespread adoption of low-floor bus designs to enhance accessibility for elderly and disabled passengers. These requirements place increased emphasis on slip-resistant flooring solutions that ensure passenger safety during boarding, transit, and disembarkation.

Design constraints in low-floor buses necessitate ultra-thin coating systems that provide high abrasion resistance without adding significant vertical thickness to the flooring structure. Anti-slip vinyl coatings and sprayable systems are being engineered to meet these requirements while maintaining durability under high foot traffic conditions. Public transit vehicles often experience thousands of passenger movements daily, requiring coatings that can withstand continuous mechanical wear and exposure to aggressive cleaning agents used in routine sanitization.

In addition to functional performance, visual safety is becoming an important consideration. Transit authorities are incorporating textured coatings with embedded contrasting colors to clearly demarcate hazard zones, including step edges and wheelchair access areas. This enhances passenger awareness and reduces the risk of accidents, particularly in crowded or low-visibility conditions.

With urban mobility initiatives accelerating globally, the demand for high-performance anti-slip coatings in public transportation is expected to expand rapidly, driven by regulatory compliance, safety considerations, and the need for durable, low-maintenance flooring solutions.

Aggregate-Injected Anti-Slip Coatings Lead Market with 47% Share Driven by High-Friction Industrial Safety Needs

Anti-Slip Mechanism Analysis: Aggregate-Injected Systems Dominate with Superior COF and Hydroplaning Resistance

Aggregate-injected coatings account for a leading 47.0% share of the anti-slip coatings market in 2025, positioning them as the preferred solution for industrial safety flooring, commercial kitchens, marine decks, and high-risk environments. These systems utilize hard angular aggregates such as aluminum oxide, silicon carbide, and polymer beads, embedded into epoxy or polyurethane coatings to achieve a coefficient of friction (COF >0.85) even under wet, oily, or greasy conditions. Their durability ensures long-term performance, as the exposed aggregate structure resists wear from heavy foot and vehicle traffic. A major growth driver is customizable safety gradients, where applicators adjust aggregate mesh size and broadcast density to meet specific industry requirements—from fine textures in food processing plants to coarse finishes for offshore helidecks. Unlike textured coatings, aggregate systems prevent hydroplaning by enabling fluid drainage channels, making them essential for breweries, industrial flooring, and wet-area safety compliance.

Industrial Manufacturing Sector Drives 28.5% Market Share with OSHA Compliance and High-Traffic Safety Demands

End-Use Industry Analysis: Factory Flooring and ESD Integration Boost Anti-Slip Coating Adoption

Industrial manufacturing holds the largest 28.5% share of the anti-slip coatings market in 2025, driven by stringent OSHA safety regulations and the need to mitigate slip hazards across factories, warehouses, and assembly plants. High-risk zones such as loading docks, CNC machining areas, and mezzanine walkways demand durable anti-slip epoxy coatings capable of withstanding oil exposure, moisture, and heavy equipment traffic. A significant trend is the shift from rubber safety mats to seamless anti-slip floor coatings, eliminating trip hazards, improving hygiene, and reducing maintenance costs. These coatings also enhance operational efficiency by preventing disruptions caused by slips and falls—the leading cause of workplace injuries. Additionally, a high-value niche is emerging in ESD (electrostatic dissipative) anti-slip coatings, particularly in electronics manufacturing and battery production, where conductive fillers are combined with anti-slip aggregates. This dual-functionality ensures both worker safety and protection of sensitive electronic components, driving premium demand in the global anti-slip coatings market.

Anti Slip Coatings Market Competitive Landscape Driven by Safety Compliance and High-Performance Flooring Systems

The anti slip coatings market is driven by high-friction epoxy coatings, polyurethane floor coatings, and textured powder coatings designed for industrial safety and durability. Key players are focusing on VOC-compliant additives, fast-curing systems, and integrated flooring solutions across infrastructure, data centers, marine, and commercial environments.

PPG Industries advances anti slip coatings with integrated safety systems and data center solutions

PPG Industries leads the anti slip coatings market through vertically integrated coating solutions and industrial safety innovations. The company reported $15.9 billion in net sales in 2025, with strong growth in protective and marine coatings supporting demand for anti-slip flooring systems. In January 2026, PPG introduced next-generation anti-slip additives compatible with both liquid coatings and powder coatings for industrial flooring and decking applications. At Data Center World 2026, it showcased anti-static anti-slip coatings designed to enhance technician safety and operational reliability in hyperscale data centers. Its single-source capability integrates pretreatment, electrocoat, and specialized safety coatings with professional application services. Product development continues to focus on high-performance, safety-compliant coating systems.

Sherwin-Williams expands global anti slip coating standards with infrastructure-focused systems

The Sherwin-Williams Company strengthens its position in anti slip coatings through its Global Core product strategy for infrastructure and construction projects. The expanded Global Core portfolio ensures consistent anti-slip coating performance across regions, supporting multinational infrastructure developments. Its epoxy zinc phosphate coatings and urethane topcoats such as Acrolon 7700 meet Slip B safety requirements for structural connections in bridges and highways. The Macropoxy® 2600 system features low-temperature curing, enabling application of anti-slip textures in sub-zero conditions and extending construction timelines. Ongoing R&D efforts focus on eco-friendly anti-slip additives with reduced VOC emissions for commercial and residential flooring. Product innovation aligns with safety compliance and environmental standards.

AkzoNobel enhances powder-based anti slip coatings with laser-curing and EV applications

AkzoNobel advances anti slip coatings through powder coating technologies and energy-efficient curing processes. At PaintExpo 2026, the company demonstrated laser-based curing in partnership with IPG, enabling faster and more efficient curing of textured anti-slip coatings. Its Resicoat portfolio includes electrical insulation powder coatings with integrated slip-resistant properties for EV battery housings and motor components. The company reported €1.44 billion in adjusted EBITDA in 2025, supported by €98 million in operational cost savings. The ongoing merger with Axalta Coating Systems aims to strengthen capabilities in high-durability 2K anti-slip coatings for automotive and marine applications. Product development focuses on advanced powder coatings and mobility-driven safety solutions.

Rust-Oleum drives contractor-focused anti slip flooring with fast-cure technologies

Rust-Oleum, under RPM International, leads the professional anti slip coatings segment through contractor-centric solutions and fast-curing systems. In January 2026, the company introduced a digital system selector tool under the Citadel brand to help contractors match coefficient of friction requirements with appropriate flooring systems. The SafeTex® Easy-Tread solution, launched at World of Concrete 2026, delivers high-traction performance with a rapid 24-hour return-to-service capability. Its integrated systems, including EP-55 Low-Prep Primer and Poly-4XT Wear Coat, ensure strong adhesion on challenging surfaces such as damp or oil-contaminated concrete. With over 40 years of expertise in fast-cure technologies, Rust-Oleum supports reduced downtime in industrial and logistics facilities. Product innovation continues to focus on durability and application efficiency.

Axalta strengthens anti slip coatings portfolio with AI-driven safety and mobility applications

Axalta Coating Systems is expanding its presence in anti slip coatings through high-performance resins and mobility-focused innovations. The company reported a record adjusted EBITDA of $1.13 billion in 2025, achieving a 22.0% margin driven by efficient production and high-value coatings. It received a 2026 Edison Award for AI-powered color technology and EV safety solutions, including high-visibility anti-slip coatings for emergency egress applications. The launch of the Zencore™ coating system integrates aesthetic finishes with slip-resistant textures for premium residential and commercial surfaces. Axalta’s mobility coatings segment includes anti-slip solutions for commercial vehicle steps and high-wear exterior components. Product development continues to focus on safety, durability, and advanced coating technologies.

China Anti-Slip Coatings Market: Infrastructure Expansion and Industrial Safety Regulations Driving High-Performance Coatings

China’s anti-slip coatings market is expanding rapidly, fueled by large-scale infrastructure investments and stringent industrial safety mandates. Government initiatives under the “14th Five-Year Plan” are accelerating the adoption of high-performance protective coatings across state-funded projects, particularly in logistics, transportation, and manufacturing sectors. The country’s massive logistics overhaul is generating strong demand for industrial-grade polyurethane anti-slip floor coatings in automated warehouses, cold storage facilities, and distribution hubs.

Technological advancements are further enhancing market growth, with the integration of graphene-enhanced additives providing both slip resistance and electrostatic discharge (ESD) protection in high-tech manufacturing environments. Regulatory frameworks promoting green building standards are driving the transition toward zero-VOC waterborne anti-slip coatings. Additionally, the widespread deployment of high-friction epoxy coatings in high-speed rail platforms and metro systems highlights the increasing focus on public safety and infrastructure durability. Innovations in bio-based acrylic materials are also supporting sustainability goals, reinforcing China’s leadership in advanced anti-slip coating technologies.

United States Anti-Slip Coatings Market: OSHA Compliance and Smart Coating Technologies Transforming Safety Standards

The United States anti-slip coatings market is experiencing steady growth, driven by stringent occupational safety regulations and increasing adoption of advanced coating technologies. Updated safety standards for industrial and commercial environments have led to a surge in retrofitting projects, particularly for ramps, stairways, and high-traffic areas requiring enhanced traction and durability.

Technological innovation is playing a critical role in shaping the market landscape. The integration of smart coatings embedded with sensors is enabling real-time monitoring of surface wear and slip resistance, improving maintenance efficiency and safety compliance. Fast-curing polyaspartic coatings are gaining popularity due to their ability to minimize operational downtime, particularly in retail and commercial spaces. Infrastructure investments are also driving demand for anti-slip coatings in public transport and marine applications, while sustainability initiatives are encouraging the use of recycled materials in coating formulations.

India Anti-Slip Coatings Market: Infrastructure Development and Urbanization Accelerating Demand

India’s anti-slip coatings market is witnessing significant growth, supported by extensive infrastructure development and rapid urbanization. Large-scale government initiatives are driving the adoption of anti-slip coatings in transportation networks, industrial corridors, and smart city projects, where safety and durability are critical requirements.

Technological advancements tailored to local conditions are enhancing market adoption. Moisture-cured urethane coatings are widely used in high-humidity environments, ensuring consistent performance in tropical climates. The rapid expansion of metro rail networks and urban transit systems is further increasing demand for high-friction floor coatings in public spaces. Additionally, policy measures promoting domestic manufacturing are strengthening supply chains and encouraging the development of advanced coating technologies. Strategic industry consolidation and investments are also contributing to market expansion, positioning India as a key growth region in the global anti-slip coatings market.

Germany Anti-Slip Coatings Market: Sustainable Formulations and Industry 4.0 Integration

Germany’s anti-slip coatings market is characterized by its strong focus on sustainability and advanced manufacturing technologies. The transition toward bio-attributed resins is reducing the environmental impact of coatings while maintaining high-performance standards required for industrial applications. Strict regulatory compliance is driving the development of eco-friendly formulations that eliminate hazardous substances and improve safety.

The integration of Industry 4.0 technologies is enhancing coating performance and lifecycle management. Innovations such as self-cleaning anti-slip surfaces are improving efficiency in industrial environments by maintaining high traction levels with minimal maintenance. Demand from renewable energy sectors, particularly offshore wind, is also driving the adoption of durable anti-slip coatings designed to withstand harsh environmental conditions. Additionally, infrastructure renovation projects are increasing the use of advanced coating systems for enhanced safety and corrosion protection, reinforcing Germany’s leadership in sustainable coating technologies.

Japan Anti-Slip Coatings Market: Advanced Materials and Safety Solutions for Aging Population

Japan’s anti-slip coatings market is driven by its focus on advanced materials and the need to improve safety for an aging population. Significant investments in research and development are supporting the creation of innovative coatings that combine high durability with enhanced slip resistance, particularly in public and healthcare facilities.

The demand for specialized coatings in residential and commercial environments is increasing, with micro-bead acrylic coatings offering both aesthetic appeal and high safety standards. Technological innovations such as nano-silica infused coatings are delivering superior hardness and long-lasting performance. Regulatory measures mandating safety improvements in industrial environments are further driving adoption, while investments in advanced materials are supporting the development of next-generation coating solutions. These factors are positioning Japan as a leader in high-performance anti-slip coating technologies.

Brazil Anti-Slip Coatings Market: Mining Operations and Offshore Infrastructure Driving Demand

Brazil’s anti-slip coatings market is experiencing strong growth, supported by its mining and offshore energy sectors. The need for enhanced safety in heavy industrial environments is driving the adoption of durable anti-slip coatings across mining operations, particularly in conveyor systems and processing facilities.

Infrastructure investments are further boosting market demand, with large-scale development projects in ports, airports, and transportation networks requiring advanced safety coatings. Technological advancements such as cold spray repair techniques are improving maintenance efficiency while preserving coating performance. Regulatory standards in marine environments are also reinforcing the need for high-performance anti-slip coatings capable of withstanding harsh conditions. Additionally, localized production of coating materials is reducing costs and strengthening the domestic market, contributing to sustained growth in Brazil’s anti-slip coatings industry.

Anti-Slip Coatings Market Report Scope

Anti-Slip Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$367.2 Million

|

|

Market Size (2032)

|

$570.6 Million

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Resin Chemistry (Epoxy, Polyurethane, Acrylic, Polyaspartic and Polyurea, Alkyd and Chlorinated Rubber, Specialized Hybrids), By Technology Type (Water-borne, Solvent-borne, Solvent-Free, Reactive Systems), By Anti-Slip Mechanism (Aggregate-Injected Coatings, Textured Coatings, Soft-Grip Coatings, Chemical Etching Solutions), By Substrate Compatibility (Concrete and Masonry, Metal, Wood and Timber Decking, Fiberglass and Composites, Natural Stone and Ceramic Tiles), By End-Use Industry (Industrial Manufacturing, Construction and Infrastructure, Marine and Shipbuilding, Healthcare and Pharmaceutical, Food and Beverage, Oil and Gas, Aviation and Aerospace), By Performance Class (Low Slip Potential, Moderate to High Slip Potential, Extreme Slip Potential, Coefficient of Friction)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, The Sherwin-Williams Company, PPG Industries, Inc., RPM International Inc., Akzo Nobel N.V., Axalta Coating Systems Ltd., Hempel A/S, Jotun A/S, Sika AG, Amstep Products, Randolph Products Co., Tesoplas, Henkel AG & Co. KGaA, Kansai Paint Co., Ltd., Meon Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti-Slip Coatings Market Segmentation

By Resin Chemistry

- Epoxy

- Polyurethane

- Acrylic

- Polyaspartic and Polyurea

- Alkyd and Chlorinated Rubber

- Specialized Hybrids

By Technology Type

- Water-borne

- Solvent-borne

- Solvent-Free

- Reactive Systems

By Anti-Slip Mechanism

- Aggregate-Injected Coatings

- Textured Coatings

- Soft-Grip Coatings

- Chemical Etching Solutions

By Substrate Compatibility

- Concrete and Masonry

- Metal

- Wood and Timber Decking

- Fiberglass and Composites

- Natural Stone and Ceramic Tiles

By End-Use Industry

- Industrial Manufacturing

- Construction and Infrastructure

- Marine and Shipbuilding

- Healthcare and Pharmaceutical

- Food and Beverage

- Oil and Gas

- Aviation and Aerospace

By Performance Class

- Low Slip Potential

- Moderate to High Slip Potential

- Extreme Slip Potential

- Coefficient of Friction

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Anti Slip Coatings Market

- 3M Company

- The Sherwin-Williams Company

- PPG Industries, Inc.

- RPM International Inc

- Akzo Nobel N.V.

- Axalta Coating Systems Ltd.

- Hempel A/S

- Jotun A/S

- Sika AG

- Amstep Products

- Randolph Products Co.

- Tesoplas

- Henkel AG & Co. KGaA

- Kansai Paint Co., Ltd.

- Meon Ltd.

*- List not Exhaustive

Table of Contents: Anti-Slip Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Anti-Slip Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Anti-Slip Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Workplace Safety Compliance and Regulatory Drivers

2.4. Infrastructure Modernization and Industrial Demand Expansion

2.5. Technological Advancements in High-Friction and Low-VOC Coatings

3. Innovations Reshaping the Anti-Slip Coatings Market

3.1. Trend: Regulatory-Driven Adoption of Certified High-Traction Coatings

3.2. Trend: Transition to 100% Solids Epoxy and Polyaspartic Systems

3.3. Opportunity: Offshore Wind and Marine Infrastructure Applications

3.4. Opportunity: Urban Transit and Public Transportation Safety Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Anti-Slip Coatings Market

5.1. By Resin Chemistry

5.1.1. Epoxy

5.1.2. Polyurethane

5.1.3. Acrylic

5.1.4. Polyaspartic and Polyurea

5.1.5. Alkyd and Chlorinated Rubber

5.1.6. Specialized Hybrids

5.2. By Technology Type

5.2.1. Water-borne

5.2.2. Solvent-borne

5.2.3. Solvent-Free

5.2.4. Reactive Systems

5.3. By Anti-Slip Mechanism

5.3.1. Aggregate-Injected Coatings

5.3.2. Textured Coatings

5.3.3. Soft-Grip Coatings

5.3.4. Chemical Etching Solutions

5.4. By Substrate Compatibility

5.4.1. Concrete and Masonry

5.4.2. Metal

5.4.3. Wood and Timber Decking

5.4.4. Fiberglass and Composites

5.4.5. Natural Stone and Ceramic Tiles

5.5. By End-Use Industry

5.5.1. Industrial Manufacturing

5.5.2. Construction and Infrastructure

5.5.3. Marine and Shipbuilding

5.5.4. Healthcare and Pharmaceutical

5.5.5. Food and Beverage

5.5.6. Oil and Gas

5.5.7. Aviation and Aerospace

5.6. By Performance Class

5.6.1. Low Slip Potential

5.6.2. Moderate to High Slip Potential

5.6.3. Extreme Slip Potential

5.6.4. Coefficient of Friction

6. Country Analysis and Outlook of Anti-Slip Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Anti-Slip Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Anti-Slip Coatings Market Size Outlook to 2032

7.1.1. By Resin Chemistry

7.1.2. By Technology Type

7.1.3. By Anti-Slip Mechanism

7.1.4. By Substrate Compatibility

7.1.5. By End-Use Industry

7.1.6. By Performance Class

7.2. Europe Anti-Slip Coatings Market Size Outlook to 2032

7.2.1. By Resin Chemistry

7.2.2. By Technology Type

7.2.3. By Anti-Slip Mechanism

7.2.4. By Substrate Compatibility

7.2.5. By End-Use Industry

7.2.6. By Performance Class

7.3. Asia Pacific Anti-Slip Coatings Market Size Outlook to 2032

7.3.1. By Resin Chemistry

7.3.2. By Technology Type

7.3.3. By Anti-Slip Mechanism

7.3.4. By Substrate Compatibility

7.3.5. By End-Use Industry

7.3.6. By Performance Class

7.4. South America Anti-Slip Coatings Market Size Outlook to 2032

7.4.1. By Resin Chemistry

7.4.2. By Technology Type

7.4.3. By Anti-Slip Mechanism

7.4.4. By Substrate Compatibility

7.4.5. By End-Use Industry

7.4.6. By Performance Class

7.5. Middle East and Africa Anti-Slip Coatings Market Size Outlook to 2032

7.5.1. By Resin Chemistry

7.5.2. By Technology Type

7.5.3. By Anti-Slip Mechanism

7.5.4. By Substrate Compatibility

7.5.5. By End-Use Industry

7.5.6. By Performance Class

8. Company Profiles: Leading Players in the Anti-Slip Coatings Market

8.1. 3M Company

8.2. The Sherwin-Williams Company

8.3. PPG Industries, Inc.

8.4. RPM International Inc

8.5. Akzo Nobel N.V.

8.6. Axalta Coating Systems Ltd.

8.7. Hempel A/S

8.8. Jotun A/S

8.9. Sika AG

8.10. Amstep Products

8.11. Randolph Products Co.

8.12. Tesoplas

8.13. Henkel AG & Co. KGaA

8.14. Kansai Paint Co., Ltd.

8.15. Meon Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures