Antiblock Additive Market Size and Growth Driven by Sustainable Packaging and Film Processing Efficiency

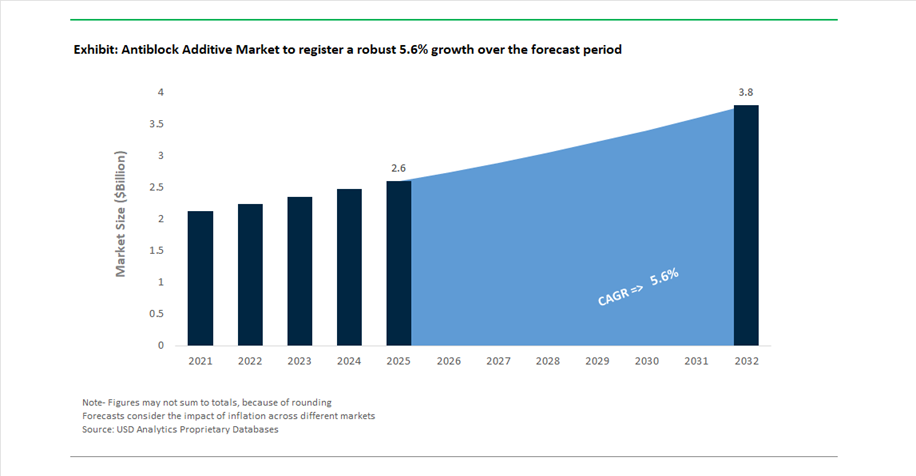

The Antiblock Additive Market is valued at USD 2.6 billion in 2025 and is projected to reach USD 3.81 billion by 2032, growing at a CAGR of 5.6%. This growth is primarily driven by the increasing demand for high-performance plastic films in packaging, agriculture, and industrial applications, where preventing film adhesion is critical to maintaining processing efficiency and product quality.

Antiblock additives are essential components in polymer films, designed to reduce surface friction and prevent adjacent film layers from sticking (blocking) during manufacturing, storage, and transportation. These additives, which include inorganic materials such as silica and talc, as well as organic waxes and amides, play a crucial role in ensuring smooth film unwinding, improved optical clarity, and consistent mechanical performance. With the rapid expansion of the flexible packaging industry, particularly in food, pharmaceuticals, and e-commerce logistics, the demand for advanced antiblock solutions is steadily increasing.

A major market driver is the shift toward sustainable and recyclable packaging materials, which introduces new technical challenges such as maintaining film integrity and surface quality in high-recycled-content plastics. As a result, manufacturers are investing in next-generation antiblock systems compatible with circular economy requirements, including bio-based additives and PFAS-free formulations. Additionally, advancements in multi-layer film extrusion and high-speed processing technologies are increasing the need for precise control over coefficient of friction (CoF) and surface morphology, further driving innovation in antiblock additive chemistry.

The market is also witnessing growing adoption in specialty applications, including agricultural films, automotive packaging, and electronics protection, where performance reliability under varying environmental conditions is critical. Competitive dynamics are shaped by material innovation, supply chain optimization, and integration with broader polymer additive systems, positioning antiblock additives as a key enabler of efficient and sustainable film manufacturing processes.

PFAS-Free Innovation, Mineral Additive Expansion, and Supply Chain Optimization Driving Market Evolution

The antiblock additive market is evolving through regulatory-driven innovation, strategic acquisitions, and advancements in material science, particularly in response to sustainability and performance demands. A major milestone was achieved in November 2024, when Clariant completed its transition to a fully PFAS-free additive portfolio, including polymer processing aids and antiblock solutions. This proactive shift enables packaging manufacturers to comply with stringent global environmental regulations while maintaining high-performance film properties.

Supply chain optimization and distribution enhancements are also shaping the competitive landscape. In February 2026, Evonik restructured its North American distribution network, appointing new regional partners to improve technical support and supply reliability for its silica-based antiblock additives. This move reflects the increasing importance of localized supply chains and application-specific technical services in supporting film manufacturers.

Innovation is strongly aligned with circular economy initiatives and recycled material performance. BASF’s introduction of sustainable additives at CHINAPLAS 2024, including the IrgaCycle® range, demonstrates how additive systems are being designed to restore the mechanical and surface properties of recycled plastics, often working in conjunction with antiblock agents to prevent processing issues. Similarly, Clariant’s AddWorks® PPA line (November 2024) enhances film extrusion quality by improving melt flow and surface characteristics, complementing antiblock functionality in high-speed production environments.

Strategic acquisitions are strengthening raw material supply and product portfolios. Imerys’ January 2025 acquisition of a perlite and diatomite business reinforces its position in mineral-based antiblock additives, enabling expanded offerings of natural silica solutions that improve film transparency and friction control. This is further supported by Imerys’ “Project Horizon” (October 2025), aimed at optimizing global production capacity and enhancing supply efficiency for talc and silica-based products.

Product development is also advancing toward bio-based and high-performance additive systems. Fine Organic Industries’ 2025 focus on bio-based additives highlights the shift toward renewable, oleochemical-derived antiblock agents, catering to food-contact and environmentally sensitive applications. Meanwhile, Honeywell’s upgrades to its AClyn® and A-C® wax additives target high-end applications requiring thermal stability and low volatility, such as electronics and automotive packaging.

Infrastructure and R&D investments are further accelerating innovation. W. R. Grace & Co.’s March 2024 capacity expansion in Michigan supports increased production of high-purity silica-based additives, while Croda’s expanded European application laboratory enables real-world testing of slip and antiblock formulations, allowing for faster customization and improved performance validation.

REACH Entry 78 Enforcement Accelerating Phase-Out of Synthetic Polymer Antiblocks

The antiblock additive industry is entering a decisive regulatory phase as the EU REACH Entry 78 restriction on intentionally added microplastics moves into full enforcement. This regulation directly impacts synthetic polymer-based antiblock additives, including cross-linked acrylates and treated synthetic silicas that do not meet biodegradability or solubility criteria. As of May 31, 2026, manufacturers are required to submit detailed annual reports to the European Chemicals Agency, documenting the identity and emission profiles of all synthetic polymer microparticles used in coating and packaging formulations.

The introduction of a strict compliance threshold of 0.01% by weight for non-biodegradable polymers has fundamentally altered formulation strategies across the flexible packaging sector. Products exceeding this limit are now subject to mandatory labeling requirements and phased elimination timelines, significantly increasing administrative and operational burdens. As a result, approximately 55% of the packaging industry has already initiated a transition toward biodegradable, organic, or mineral-based alternatives to avoid compliance risks and reporting complexity.

To ensure market access and regulatory alignment, manufacturers are increasingly adopting ISO 20200 compostability testing protocols to validate “microplastic-free” claims. This standardization is becoming critical for export-oriented suppliers targeting European markets, where regulatory scrutiny continues to intensify. The enforcement of REACH Entry 78 is therefore not only a compliance challenge but also a catalyst for innovation, accelerating the development of next-generation antiblock additives that combine environmental sustainability with high-performance characteristics.

Bio-Based and Renewable Antiblock Additives Driving High-Performance Packaging Innovation

In parallel with regulatory pressures, the antiblock additive market is undergoing a strategic shift toward bio-based and renewable materials, driven by global decarbonization targets and increasing demand for sustainable packaging solutions. Traditional mineral-based antiblocks such as talc and diatomaceous earth are gradually being replaced by organic amide-based additives and renewable feedstock-derived materials, particularly in high-value applications such as food-grade and pharmaceutical packaging.

Major chemical producers have expanded biomass balance portfolios in recent years, enabling converters to incorporate renewable carbon content into BOPP and polyethylene films without modifying existing processing infrastructure. This seamless integration is accelerating adoption across packaging converters seeking to reduce carbon footprints while maintaining production efficiency. From a performance standpoint, advanced bio-based antiblock additives are delivering superior optical and frictional properties. These materials can achieve a coefficient of friction below 0.2 while maintaining film haze levels under 2%, outperforming conventional mineral fillers in applications requiring high clarity and surface smoothness.

Operational advantages further strengthen the case for organic additives. Low-dust formulations are reducing workplace particulate emissions by up to 40%, aligning with updated environmental health and safety protocols for industrial processing environments. Additionally, organic antiblocks enhance recyclability by minimizing abrasive residue in regrind streams, preserving the mechanical integrity of post-consumer recycled resins. This compatibility with mono-material recycling systems is a critical factor in advancing circular packaging initiatives.

High-Purity Antiblock Additives Enabling Performance Gains in EV Battery Separator Films

The rapid expansion of the electric vehicle ecosystem is creating a highly specialized demand for antiblock additives in lithium-ion battery separator films. These ultra-thin membranes, typically ranging from 12 to 25 micrometers in thickness, require precise surface engineering to prevent film adhesion during high-speed manufacturing while maintaining critical electrochemical performance.

Particle size distribution is a key parameter in this application. Antiblock additives must be engineered to maintain separator porosity between 40% and 60%, ensuring adequate ion transport without compromising mechanical strength. Thermal stability is equally critical, as additives must remain structurally and chemically stable at temperatures exceeding 150°C to support the separator’s thermal shutdown functionality during overheating scenarios.

Purity requirements in this segment are among the most stringent in the coatings and additives industry. High-voltage battery systems demand antiblock additives with metallic impurity levels below 10 ppm to prevent internal short circuits and ensure long-term reliability, with target cycle lifespans exceeding 2,000 charge-discharge cycles. Additionally, advanced functionalized silica additives are being developed to enhance electrolyte wettability, improving ionic conductivity by up to 15% and contributing to overall battery efficiency.

Functional Antiblock Additives Supporting Controlled Degradation in Biodegradable Mulch Films

The shift toward sustainable agriculture and precision farming is creating new opportunities for functional antiblock additives in soil-biodegradable mulch films. Unlike conventional polyethylene films, biodegradable mulch films are designed to degrade within a defined timeframe, requiring additives that support both processing performance and environmental compatibility.

Next-generation biodegradable mulch formulations are engineered to lose approximately 50% of their mass within a single growing season, necessitating antiblock additives that do not interfere with microbial degradation processes in the soil. Inorganic nanocellulose and mineral-based antiblocks are emerging as preferred solutions, as they eliminate the risk of long-term microplastic accumulation—a key concern associated with traditional low-density polyethylene films, which can persist in the environment for centuries.

In addition to environmental performance, functional antiblock additives are being optimized for agricultural productivity. These materials are engineered to enhance light management by scattering specific wavelengths, improving Photosynthetically Active Radiation and supporting crop growth. At the same time, mechanical integrity remains critical. Advanced formulations enable biodegradable films to maintain tensile strengths of approximately 98 MPa, ensuring durability during automated installation and field use.

By combining biodegradability, optical optimization, and mechanical performance, functional antiblock additives are playing a pivotal role in enabling next-generation agricultural films, supporting both sustainability objectives and productivity gains in modern farming systems.

Inorganic Antiblock Agents Dominate Market with 72% Share Driven by Silica-Based Performance Efficiency

Product Type Analysis: Synthetic Silica Leads High-Volume Antiblock Additive Demand

Inorganic antiblock agents command a dominant 72.0% share of the global antiblock additive market in 2025, driven by their cost-effectiveness, chemical inertness, and superior performance in polymer film processing. Key materials such as synthetic silica (diatomaceous earth), talc, and calcium carbonate are widely used to create micro-rough surfaces that prevent film-to-film adhesion. Notably, synthetic silica alone accounts for over 50% of total antiblock additive volume, owing to its high porosity and ability to absorb migratory slip agents like erucamide, enhancing film handling performance. A major growth driver is the shift toward liner-less packaging solutions, where inorganic antiblock additives are essential to prevent film rolls from fusing during storage and high-speed unwinding. In 2025, innovation is centered on engineered narrow particle size distribution silicas, which deliver optimal antiblocking while preserving film clarity and transparency, critical for fresh produce packaging and medical-grade flexible films.

Food & Beverage Packaging Drives 48.5% Antiblock Additive Demand with High-Speed Film Processing Needs

The food and beverage segment holds a leading 48.5% share of the antiblock additive market in 2025, fueled by the exponential demand for flexible packaging films such as BOPP (biaxially oriented polypropylene) and LLDPE (linear low-density polyethylene). These materials are extensively used in snack food packaging, fresh produce bags, and beverage shrink sleeves, where antiblock additives ensure smooth film separation and efficient processing. With packaging lines exceeding 400 units per minute, even minor film blocking can cause costly downtime and material waste, making antiblock additives critical for maintaining line efficiency and operational uptime. A key industry trend is the shift toward non-migratory antiblock solutions, particularly synthetic silica, due to increasing regulatory scrutiny on organic slip agents that may migrate into food. Compliance with FDA 21 CFR 177.1520 standards further strengthens the adoption of inorganic antiblock additives, ensuring food safety, product integrity, and high-performance packaging operations in the global market.

Antiblock Additive Market Competitive Landscape Driven by High-Clarity Film Performance and Sustainable Additive Technologies

The antiblock additive market is driven by synthetic silica, fatty acid amides, and mineral-based additives designed to reduce film blocking and optimize coefficient of friction (CoF). Key players are focusing on high-clarity polyolefin films, sustainable packaging, and low-dosage, high-efficiency additives for flexible packaging and industrial film applications.

Evonik leads antiblock additive market with advanced synthetic silica and low-dosage efficiency

Evonik Industries AG holds a leading share in the antiblock additive market, driven by its expertise in synthetic precipitated silica for polyolefin films. The company reported €14.1 billion in sales in 2025, with its Custom Solutions segment contributing €5.49 billion. In May 2026, Evonik optimized its North American distribution network through partnerships with regional technical specialists to enhance customer support. Its latest innovation includes surface-modified synthetic silica that prevents interaction with slip additives, maintaining low CoF even at high processing speeds. The company is advancing high-efficiency additives that deliver strong antiblocking performance at dosages as low as 0.5%. Product development continues to focus on optical clarity, processing efficiency, and advanced film performance.

Croda advances bio-based antiblock additives with low-migration solutions for healthcare packaging

Croda International Plc leads the organic antiblock additives segment with fatty acid amides and bio-based solutions targeting consumer care and medical packaging. The company achieved 6.6% revenue growth in 2025, with its Consumer Care division expanding by 8%. Its innovation pipeline is strengthening, with New & Protected Product sales rising by 5% and co-creation initiatives increasing by 12%. Croda’s low-migration antiblock additives are increasingly used in pharmaceutical and medical packaging where regulatory compliance and material safety are critical. The company’s strategic roadmap targets organic growth and operating margins above 20% through 2028. Product development focuses on sustainable additives and high-purity formulations.

Imerys strengthens mineral-based antiblock additives with circular economy focus

Imerys S.A. holds 17.1% of the antiblock additive market, supported by its extensive portfolio of talc, kaolin, and diatomaceous earth. The company reported €546 million in adjusted EBITDA in 2025, maintaining a 16.1% margin despite macroeconomic pressures. Its Project Horizon initiative aims to generate €50–60 million in annual savings by 2026 through operational efficiency improvements. Imerys is focusing on surface-treated talc to enhance mechanical properties and recyclability of plastic films, aligning with circular economy trends. Its additives are widely used in agricultural films and industrial packaging applications requiring cost-effective antiblocking performance. Product development emphasizes sustainability and material optimization.

W. R. Grace enhances high-purity silica antiblocks for premium flexible packaging

W. R. Grace & Co. commands a steady market share in the antiblock additive market, specializing in micronized synthetic silica under the SYLOID® brand. The company targets high-performance film applications, particularly in food packaging where clarity and safety are critical. Its silica additives feature controlled pore structures that optimize slip agent adsorption and prevent blooming, improving printability and lamination quality. Expansion of technical service labs in APAC supports growing demand from regional film manufacturers. Grace also offers additive masterbatch solutions that integrate antiblock, UV stabilizers, and antioxidants into a single formulation. Product development focuses on high-purity additives and advanced film processing performance.

Honeywell expands specialty antiblock additives with polymer processing innovations

Honeywell International Inc., through its Solstice Advanced Materials spin-off, is strengthening its position in specialty antiblock additives. The parent company reported $37.4 billion in sales in 2025, while the new materials entity focuses on sustainable packaging solutions. Honeywell specializes in polyethylene-based synthetic wax additives that provide effective antiblocking performance in thin-gauge films, accounting for a 7.2% market share. Its innovation pipeline includes smart additives designed to improve processing of biodegradable polymers such as PLA and PBAT, which exhibit higher blocking tendencies. The company is aligning product development with low-global-warming-potential materials and circular packaging trends. Product innovation focuses on processing efficiency and sustainability.

United States Antiblock Additive Market: PFAS-Free Transition and High-Clarity Film Innovation Driving Growth

The United States antiblock additive market is undergoing a significant transformation, driven by regulatory pressure and innovation in high-performance polymer additives. The industry-wide shift toward PFAS-free antiblock additives is accelerating due to tightening EPA regulations and state-level restrictions on fluorinated compounds. This transition is pushing manufacturers to develop advanced polymer processing aids (PPAs) and high-clarity antiblock masterbatches that meet stringent environmental and safety standards.

Technological advancements are centered around sustainability and precision engineering. The commercialization of bio-based antiblock additives such as behenamide derivatives is improving film lubrication while maintaining low haze levels in thin packaging films. Demand is also rising in medical packaging applications, where Class VI compliant, zero-migration antiblock additives are critical for ensuring product safety in IV bags and blister packaging. Additionally, the expansion of e-commerce logistics is driving adoption of high-slip antiblock masterbatches in poly-mailers for automated sorting systems. Investments in advanced silica technologies and multifunctional masterbatch production are further strengthening the United States’ position as a leader in high-performance antiblock solutions.

China Antiblock Additive Market: High-Volume Production and Nanotechnology Integration Across Industries

China dominates the global antiblock additive market through large-scale production and rapid adoption of nanotechnology-based solutions. The agricultural sector is a major growth driver, with widespread use of infrared-transparent antiblock additives in greenhouse films to enhance crop productivity while preventing film adhesion during storage and transport.

In the electronics sector, the adoption of ultra-fine nano-silica additives is improving the performance of protective films used in foldable smartphones and OLED displays. Government initiatives supporting specialty chemical production are strengthening domestic capabilities in high-purity antiblock additives. The transition toward high-concentration masterbatch systems is improving manufacturing efficiency and workplace safety. Additionally, innovations focused on recycling-compatible additives are supporting the circular economy by enabling the effective use of post-consumer recycled plastics. These developments reinforce China’s leadership in high-volume and technologically advanced antiblock additive production.

Germany’s antiblock additive market is defined by its expertise in precision masterbatch formulation and sustainable materials innovation. The country leads in the development of advanced antiblock systems optimized for high-speed extrusion processes, particularly in biaxially oriented films used in packaging applications.

Sustainability remains a core focus, with significant investments in green silica production and compostable antiblock masterbatches for bio-based films. Regulatory frameworks promoting recyclable packaging are driving demand for additives that maintain performance without compromising material recovery. The automotive sector is also contributing to market growth, with antiblock additives being used in interior laminates to enhance durability under high-temperature conditions. Continuous innovation and alignment with environmental standards position Germany as a leader in high-performance and eco-friendly antiblock additive solutions.

India Antiblock Additive Market: FMCG Packaging Expansion and Domestic Manufacturing Boost

India’s antiblock additive market is experiencing rapid growth, driven by increasing demand for flexible packaging in the FMCG sector and strong government support for domestic manufacturing. Regulatory updates are encouraging the use of low-migration antiblock additives in food-contact packaging, ensuring compliance with safety standards.

Infrastructure investments in multi-layer film production are enabling the development of thinner, high-performance packaging materials. The expansion of e-commerce is further boosting demand for antiblock additives in packaging films designed for humid environments. Government initiatives promoting local production are strengthening the supply chain and reducing import dependency. Additionally, innovations in agricultural films are improving crop yield and efficiency, supporting the broader adoption of advanced antiblock technologies across industries.

Saudi Arabia Antiblock Additive Market: Polymer Integration and Export-Oriented Production Expansion

Saudi Arabia’s antiblock additive market is evolving as a key global supplier, leveraging its strong upstream polymer industry. The production of pre-compounded resins with integrated antiblock and slip properties is streamlining manufacturing processes and enhancing product performance for export markets.

Technological advancements are focused on developing high-temperature stable additives suitable for challenging processing environments. Strategic partnerships with global chemical companies are strengthening local production capabilities and expanding international market reach. Investments in research and development are also driving innovation in polymer processing technologies. Additionally, the introduction of recycled resins with integrated antiblock additives is supporting sustainability goals, positioning Saudi Arabia as a competitive player in the global antiblock additive market.

Japan Antiblock Additive Market: Ultra-High Purity Additives and Advanced Electronics Applications

Japan’s antiblock additive market is characterized by its focus on ultra-high purity materials and advanced technological applications. The development of zero-haze antiblock additives is critical for pharmaceutical packaging, ensuring high transparency and quality control in medical products.

In the electronics sector, conductive antiblock additives are being widely used to prevent electrostatic discharge in semiconductor packaging. Innovations in porous silica materials are enhancing functionality by combining antiblock properties with additional features such as scent delivery and antimicrobial action. Government initiatives supporting recycling-compatible additives are further strengthening sustainability efforts. Japan’s leadership in optical films and high-performance materials continues to drive innovation in the global antiblock additive market.

United Arab Emirates Antiblock Additive Market: Masterbatch Hub Expansion and Smart Manufacturing Integration

The United Arab Emirates is emerging as a key hub for antiblock additive production, driven by investments in advanced masterbatch manufacturing and strategic logistics advantages. The expansion of production facilities is enabling the development of multifunctional additive systems that combine antiblock, UV stabilization, and antioxidant properties.

Technological advancements such as AI-driven formulation and quality control are improving efficiency and reducing production lead times. The country’s strategic location is facilitating rapid distribution to global markets, strengthening its role in international supply chains. Additionally, the adoption of advanced testing standards is ensuring product quality and compatibility with global requirements. Investments in smart city infrastructure and sustainable materials are further driving demand for high-performance antiblock additives in diverse applications.

South Korea Antiblock Additive Market: High-Performance Films and Next-Generation Electronics Applications

South Korea’s antiblock additive market is advancing through innovations in high-performance materials and next-generation electronics applications. The integration of antiblock additives in battery separator films is critical for improving performance and safety in electric vehicle batteries.

The country’s leadership in display technologies is driving demand for advanced antiblock coatings in flexible OLED screens, enhancing durability and user experience. Government support for research and development is accelerating the development of innovative polymer additives, including self-healing materials. The semiconductor industry is also contributing to market growth, with demand for ultra-clean materials used in high-precision manufacturing processes. Additionally, investments in bio-based plastics are supporting sustainability initiatives, positioning South Korea as a leader in advanced antiblock additive technologies.

Antiblock Additive Market Report Scope

Antiblock Additive Market

Parameter

Details

Market Size (2025)

$2.6 Billion

Market Size (2032)

$3.8 Billion

Market Growth Rate

5.6%

Segments

By Product (Inorganic Antiblock Agents, Organic Antiblock Agents, Hybrid and Specialty Formulations), By Polymer (Low-Density Polyethylene, Linear Low-Density Polyethylene, High-Density Polyethylene, Polypropylene, Polyvinyl Chloride, Polyethylene Terephthalate, Polyamide), By Form (Masterbatches, Powders, Liquid Emulsion Systems), By Performance Property (Optical Clarity and Haze Control, Coefficient of Friction, Thermal Stability, Non-Migratory and Low-Migration Grades, Anti-Stat and Anti-Fog Multi-functional Blends), By Application (Food and Beverage, Healthcare and Life Sciences, Agriculture and Horticulture, Industrial Manufacturing, Automotive and Transportation, Retail and Consumer Electronics)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

Evonik Industries AG, Imerys S.A., Grace, Honeywell International Inc., Clariant AG, Ampacet Corporation, Avient Corporation, LyondellBasell Industries N.V., BASF SE, Cargill, Incorporated, Croda International Plc, Sibelco Group, Fuji Silysia Chemical Ltd., Fine Organics, Kafrit Group

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Antiblock Additive Market Segmentation

By Product

Inorganic Antiblock Agents

Natural Silica

Synthetic Silica

Talc

Calcium Carbonate

Zeolites and Ceramic Spheres

Kaolin and Feldspar

Organic Antiblock Agents

Amides

Stearates

Waxes

Silicones

Hybrid and Specialty Formulations

By Polymer

Low-Density Polyethylene

Linear Low-Density Polyethylene

High-Density Polyethylene

Polypropylene

Polyvinyl Chloride

Polyethylene Terephthalate

Polyamide

By Form

Masterbatches

Powders

Liquid Emulsion Systems

By Performance Property

Optical Clarity and Haze Control

Coefficient of Friction

Thermal Stability

Non-Migratory and Low-Migration Grades

Anti-Stat and Anti-Fog Multi-functional Blends

By Application

Food and Beverage

Healthcare and Life Sciences

Agriculture and Horticulture

Industrial Manufacturing

Automotive and Transportation

Retail and Consumer Electronics

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Antiblock Additive Market

Evonik Industries AG

Imerys S.A.

W. R. Grace & Co.

Honeywell International Inc.

Clariant AG

Ampacet Corporation

Avient Corporation

LyondellBasell Industries N.V.

BASF SE

Cargill, Incorporated

Croda International Plc

Sibelco Group

Fuji Silysia Chemical Ltd.

Fine Organics

Kafrit Group

*- List not Exhaustive

Table of Contents: Antiblock Additive Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Antiblock Additive Market Landscape & Outlook (2025–2032)

2.1. Introduction to Antiblock Additive Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Role of Antiblock Additives in Film Processing Efficiency

2.4. Impact of Sustainable Packaging and Circular Economy Trends

2.5. Demand Across Flexible Packaging, Agriculture, and Industrial Films

3. Innovations Reshaping the Antiblock Additive Market

3.1. Trend: PFAS-Free Additives and Regulatory-Driven Reformulation

3.2. Trend: Bio-Based and Renewable Antiblock Additives

3.3. Opportunity: High-Purity Additives for EV Battery Separator Films

3.4. Opportunity: Functional Additives for Biodegradable Agricultural Films

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Antiblock Additive Market

5.1. By Product

5.1.1. Inorganic Antiblock Agents

5.1.1.1. Natural Silica

5.1.1.2. Synthetic Silica

5.1.1.3. Talc

5.1.1.4. Calcium Carbonate

5.1.1.5. Zeolites and Ceramic Spheres

5.1.1.6. Kaolin and Feldspar

5.1.2. Organic Antiblock Agents

5.1.2.1. Amides

5.1.2.2. Stearates

5.1.2.3. Waxes

5.1.2.4. Silicones

5.1.2.5. Hybrid and Specialty Formulations

5.2. By Polymer

5.2.1. Low-Density Polyethylene

5.2.2. Linear Low-Density Polyethylene

5.2.3. High-Density Polyethylene

5.2.4. Polypropylene

5.2.5. Polyvinyl Chloride

5.2.6. Polyethylene Terephthalate

5.2.7. Polyamide

5.3. By Form

5.3.1. Masterbatches

5.3.2. Powders

5.3.3. Liquid Emulsion Systems

5.4. By Performance Property

5.4.1. Optical Clarity and Haze Control

5.4.2. Coefficient of Friction

5.4.3. Thermal Stability

5.4.4. Non-Migratory and Low-Migration Grades

5.4.5. Anti-Stat and Anti-Fog Multi-functional Blends

5.5. By Application

5.5.1. Food and Beverage

5.5.2. Healthcare and Life Sciences

5.5.3. Agriculture and Horticulture

5.5.4. Industrial Manufacturing

5.5.5. Automotive and Transportation

5.5.6. Retail and Consumer Electronics

6. Country Analysis and Outlook of Antiblock Additive Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Antiblock Additive Market Size Outlook by Region (2025–2032)

7.1. North America Antiblock Additive Market Size Outlook to 2032

7.1.1. By Product

7.1.2. By Polymer

7.1.3. By Form

7.1.4. By Performance Property

7.1.5. By Application

7.2. Europe Antiblock Additive Market Size Outlook to 2032

7.2.1. By Product

7.2.2. By Polymer

7.2.3. By Form

7.2.4. By Performance Property

7.2.5. By Application

7.3. Asia Pacific Antiblock Additive Market Size Outlook to 2032

7.3.1. By Product

7.3.2. By Polymer

7.3.3. By Form

7.3.4. By Performance Property

7.3.5. By Application

7.4. South America Antiblock Additive Market Size Outlook to 2032

7.4.1. By Product

7.4.2. By Polymer

7.4.3. By Form

7.4.4. By Performance Property

7.4.5. By Application

7.5. Middle East and Africa Antiblock Additive Market Size Outlook to 2032

7.5.1. By Product

7.5.2. By Polymer

7.5.3. By Form

7.5.4. By Performance Property

7.5.5. By Application

8. Company Profiles: Leading Players in the Antiblock Additive Market

8.1. Evonik Industries AG

8.2. Imerys S.A.

8.3. W. R. Grace & Co.

8.4. Honeywell International Inc.

8.5. Clariant AG

8.6. Ampacet Corporation

8.7. Avient Corporation

8.8. LyondellBasell Industries N.V.

8.9. BASF SE

8.10. Cargill, Incorporated

8.11. Croda International Plc

8.12. Sibelco Group

8.13. Fuji Silysia Chemical Ltd.

8.14. Fine Organics

8.15. Kafrit Group

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Antiblock Additive Market Segmentation

By Product

Inorganic Antiblock Agents

Natural Silica

Synthetic Silica

Talc

Calcium Carbonate

Zeolites and Ceramic Spheres

Kaolin and Feldspar

Organic Antiblock Agents

Amides

Stearates

Waxes

Silicones

Hybrid and Specialty Formulations

By Polymer

Low-Density Polyethylene

Linear Low-Density Polyethylene

High-Density Polyethylene

Polypropylene

Polyvinyl Chloride

Polyethylene Terephthalate

Polyamide

By Form

Masterbatches

Powders

Liquid Emulsion Systems

By Performance Property

Optical Clarity and Haze Control

Coefficient of Friction

Thermal Stability

Non-Migratory and Low-Migration Grades

Anti-Stat and Anti-Fog Multi-functional Blends

By Application

Food and Beverage

Healthcare and Life Sciences

Agriculture and Horticulture

Industrial Manufacturing

Automotive and Transportation

Retail and Consumer Electronics

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The antiblock additive market is valued at USD 2.6 billion in 2025 and is projected to reach USD 3.81 billion by 2032, growing at a CAGR of 5.6%. Growth is supported by increasing demand for high-performance polymer films in packaging, agriculture, and industrial applications. The expansion of flexible packaging and e-commerce logistics is further accelerating adoption globally.

The primary growth driver is the rapid shift toward sustainable and recyclable packaging materials, which require advanced antiblock solutions to maintain film performance. Opportunities are emerging in high-value applications such as EV battery separator films, biodegradable mulch films, and high-clarity food packaging. Innovations in multi-layer extrusion and high-speed processing are also increasing demand for precise CoF control.

Regulations such as EU REACH Entry 78 are significantly reshaping the market by restricting synthetic polymer-based additives and enforcing microplastic limits of 0.01% by weight. This has accelerated the transition toward bio-based, mineral, and biodegradable antiblock solutions. Compliance requirements, including ISO compostability standards, are driving R&D investments and reformulation strategies across the industry.

Inorganic antiblock agents dominate with a 72% market share, led by synthetic silica due to its superior performance in friction control and optical clarity. The food and beverage packaging segment holds 48.5% share, driven by high-speed film processing requirements. Emerging traction is also seen in non-migratory additives and bio-based formulations for regulatory compliance and sustainability.

Key players include Evonik Industries AG, Imerys S.A., W. R. Grace & Co., Honeywell International Inc., Clariant AG, BASF SE, and Croda International Plc. These companies focus on silica innovation, PFAS-free solutions, and sustainable additive technologies.