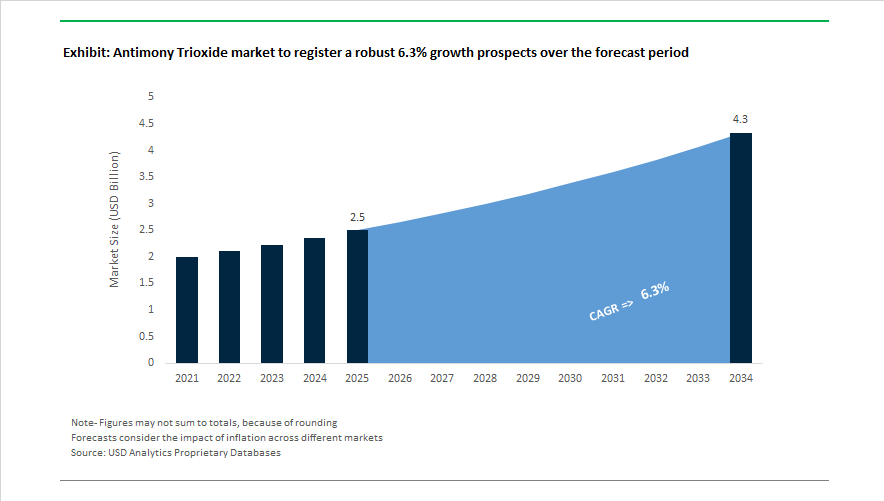

Market Overview: China Export Controls and Western Supply Chain Rebuild Drive Antimony Trioxide Market to $4.3 Billion by 2034

The antimony trioxide market is valued at $2.5 billion in 2025 and is projected to reach $4.3 billion by 2034, expanding at a 6.3% CAGR. Growth is supported by rising demand for antimony trioxide flame retardants, ATO synergists in halogenated systems, semiconductor-grade antimony oxide, battery safety materials, military-grade alloys, and polymer fire protection additives used across electronics, EV battery enclosures, cables, construction materials, and defense applications. Market fundamentals shifted in September 2024 when China imposed strategic export controls on antimony products, triggering immediate global shortages. Prices escalated sharply and approached $60,000 per tonne by mid-2025, establishing a new pricing benchmark for high-purity ATO. In August 2025, China further consolidated its antimony sector under dominant players such as Hunan Gold Corporation, strengthening state influence over global supply channels.

Western nations accelerated domestic supply initiatives throughout 2025. In March 2025, Campine reported record performance driven by proprietary recycling technologies that reduced its dependence on Chinese metal to below 5%. In April 2025, United States Antimony Corporation announced the expansion of its Montana smelter, the only operating antimony smelter in the United States. September 2025 marked a major defense milestone when the U.S. Defense Logistics Agency awarded USAC a five-year IDIQ contract worth up to $245 million to secure domestic military supply. The same month, Perpetua Resources secured preliminary EXIM Bank financing of up to $2 billion for the Stibnite Gold Project, followed by project groundbreaking in October 2025, positioning the site to meet more than 35% of annual U.S. antimony demand. In November 2025, AMG Critical Materials confirmed plans to establish U.S.-based antimony oxide processing capacity.

Geopolitical dynamics remained fluid. China announced a temporary suspension of mineral export bans to the U.S. in November 2025, valid through November 2026, creating a limited restocking window for Western buyers. Supply diversification continued in 2025 as Nihon Seiko expanded specialty ATO output for semiconductor and EV safety applications using non-Chinese feedstocks. Domestic U.S. infrastructure development intensified in January 2026 when USAC acquired the Radersburg flotation facility in Montana, followed by a February 2026 joint venture between USAC and Americas Gold & Silver at Idaho’s Galena Complex to increase domestic antimony concentrate production.

Trends and Opportunities Reshaping Antimony Trioxide Demand, Regulatory Risk, and Margin Pools

Regulatory Bans Forcing Portfolio Repositioning Toward Mission-Critical Flame Retardants

Global chemical policy is no longer simply restricting halogenated flame retardants. It is structurally reallocating where antimony trioxide (ATO) can legally operate. As of October 28, 2025, the EU POPs Regulation Amendment (EU 2025/1482) cut allowable PBDE mixture limits from 500 mg/kg to 10 mg/kg, effectively removing halogenated flame retardants from mass-market consumer products. ATO, once a broad-application additive, is being pushed into exempt industrial and high-performance categories where thermal resistance and UL94 V-0 certification remain mandatory.

U.S. state-level restrictions further accelerate this polarization. New York’s December 2024 ban on organohalogen flame retardants in electronic display housings and Massachusetts’ May 2025 restriction on 11 flame-retardant chemistries are driving a 19% market pivot toward phosphorus-nitrogen FR systems across furniture, textiles, and children’s products. However, high-purity ATO consumption remains resilient within engineered polymers: aerospace and EV applications accounted for 37.2% of new flame-retardant innovation pipelines in 2025, driven by battery housing insulation and electronics safety requirements.

Geopolitical Pressure Redefining Antimony as a Strategic Mineral

Supply chain security is emerging as a primary procurement criterion. China’s near-monopoly—controlling 70 to 80% of global antimony supply—shifted into geopolitical risk status following export licensing controls implemented September 15, 2024. Enforcement escalated in September 2025, when Beijing launched a national crackdown targeting “third-country” routing. Smuggling volumes surged 300% prior to these rulings, indicating the depth of dependency Western supply chains face.

In contrast, the United States is directly localizing strategic reserves. The Defense Logistics Agency’s $245 million contract with U.S. Antimony Corporation (September 2025) marks the country’s most aggressive ATO security action to date and coincides with a six-fold expansion of domestic smelter capacity, targeting completion in January 2026. Pricing volatility reflects this tension. After rising from $5/lb in 2024 to early-2025 levels exceeding $25/lb, stabilized international averages now sit within $45,000–$57,000 per tonne, reshaping multi-year contracts and renegotiation schedules across polymer and catalyst procurement teams.

High-Purity Catalytic ATO for PET and rPET Resin Expansion

The most durable volume growth engine for antimony trioxide is PET polymerization, where ATO remains the dominant catalyst. 77.5% of all PET catalysts used in 2025 were antimony-based, and 85% of global PET output still requires ATO or derivatives to achieve fast-cycle polycondensation and optical clarity in bottles and thermoforms.

Technical innovation is widening the opportunity. Low-antimony PET formulations—commercialized in 2025—allowed 12 to 15% catalyst loading reduction without sacrificing clarity, enabling food-contact manufacturers to meet retailer-imposed “reduced-metal” specifications. Parallel growth in PET capacity across Southeast Asia and Latin America (6–8% annual increase) is being driven by beverage brands localizing supply chains to avoid freight exposure and carbon-intensity penalties.

Fire-Protective Coatings for Mass Timber Construction and Green Building Codes

ATO is gaining new relevance in intumescent coating systems engineered for cross-laminated timber (CLT) and tall-wood buildings. Updated 2024–2025 IBC allowances for multi-story mass-timber construction require fire-retardant systems capable of preserving structural integrity under prolonged heat exposure. ATO functions as a char synergist, enhancing intumescence and thermal insulation on wood substrates.

Industrial coating demand is rising accordingly—22% year-over-year growth in 2025—as designers seek V-0-rated surfaces and municipal regulators in the EU enforce EN 13501 fire classification compliance. In an era of carbon-neutral construction, antimony trioxide is becoming a niche strategic material: one that enables cities to adopt timber without compromising fire-code parity against concrete and steel.

Antimony Trioxide (ATO) Market Share and Segmentation Insights

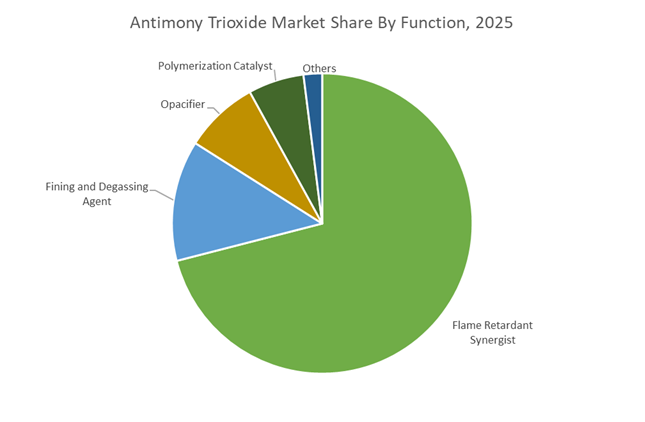

Market Share by Function: Flame Retardant Synergist Anchors Demand While Catalyst Use Faces Structural Decline

Flame retardant synergist applications account for approximately 71% of global antimony trioxide (ATO) consumption in 2025, making it the overwhelmingly dominant functional segment. ATO operates synergistically with halogenated flame retardants, forming antimony halides that quench free radicals in the gas phase and suppress combustion. This chemistry is critical for UL 94 V-0 compliant printed circuit boards, wire and cable insulation, connectors, and automotive components. Supply risk remains elevated, as China controls nearly 80% of primary antimony production, contributing to price volatility. Fining and degassing in display and pharmaceutical glass represent the second-largest function, tied to LCD/OLED production cycles. Opacifier demand persists in architectural and solar glass but faces titanium dioxide competition. Polymerization catalyst use in PET is structurally declining in developed markets due to toxicity and migration concerns, with titanium-based alternatives gaining share. Recycling offsets less than 15% of demand, reinforcing critical raw material status.

Market Share by End-Use Industry: Electronics Lead While EV Fire Safety Sustains Automotive Growth

Electrical and electronics account for approximately 48% of ATO demand in 2025, driven by flame-retardant housings, FR-4 laminates, high-performance connectors, and expanding data center and 5G infrastructure buildouts. Despite regulatory pressure to reduce halogenated flame retardants, technical substitution remains challenging, preserving ATO’s market position. Automotive ranks second, with growing EV penetration increasing ATO intensity per vehicle through high-voltage wiring harnesses, battery pack fire protection, and thermal management systems. Glass and ceramics serve display glass, pharmaceutical packaging, solar panels, and architectural segments, offering relatively stable demand. Textile backcoatings for hospitality and aviation face gradual decline in Europe under REACH restrictions. Chemicals and captive catalyst use are under pressure from titanium substitution and migration scrutiny in food-contact PET. Regulatory momentum toward halogen-free systems presents long-term risk, though cost-performance parity has yet to be achieved at scale.

Antimony Trioxide Market Competitive Landscape

The global antimony trioxide (ATO) market is being reshaped by critical mineral security policies, circular economy sourcing, EV battery flame-retardant demand, and semiconductor-grade purity requirements. Competition is intensifying around recycled antimony feedstocks, hydrometallurgical recovery, ultrafine ATO grades, and regional supply chain resilience, especially as raw antimony prices surged close to USD 60,000/ton during 2025–2026. Leading producers are differentiating through urban mining, low-emission roasting, nanoscale particle control, and photovoltaic glass integration, while governments increasingly classify antimony as a strategic material. Market leadership now hinges on purity consistency, ESG compliance, and localized production for plastics, flame retardants, batteries, electronics, and solar glass applications.

Circular-economy ATO leadership powered by urban mining at Campine NV

Campine dominates the European antimony trioxide market through proprietary recycling technology that decouples ATO production from volatile primary ore supply. In 2025, the company posted record specialty chemical sales following the expansion of its Beerse facility near Antwerp, integrating metal waste recycling directly into high-purity ATO manufacturing. To manage the 2025–2026 antimony price spike, Campine implemented shorter payment terms and prepayment models to stabilize liquidity. Its unique integration of antimony recovery with lead and tin recycling enables precious metal extraction while supplying flame-retardant grade ATO. Core strengths include low-carbon “urban mining” feedstocks and BPR-compliant supply for European OEMs seeking alternatives to Chinese imports.

Mine-to-market ATO security driven by domestic processing at United States Antimony Corporation

United States Antimony Corporation is the only fully integrated antimony producer outside China and Russia, positioning itself at the center of North American critical mineral independence. In February 2026, USAC announced a joint venture with Americas Gold and Silver to build a hydrometallurgical processing plant in Idaho, significantly expanding domestic ATO output. Its licensed commercial-scale hydromet technology improves recovery while cutting processing costs by an estimated 15–20%. With vertically integrated mines in Mexico and Montana and a smelter in Coahuila, USAC controls ATO purity and particle size end-to-end. Strategically, the company is leveraging the FAST-41 initiative to become a defense-grade ATO supplier for U.S. government programs.

High-tech antimony trioxide for EV batteries scaled by AMG Critical Materials N.V.

AMG Critical Materials targets high-value ATO applications across EV batteries, advanced metallurgy, and aerospace. In early 2025, AMG committed USD 150 million to expand its South Carolina antimony trioxide facility, addressing accelerating demand for flame retardants in electric vehicle battery systems. The company supplies high-purity ATO for LIVA batteries, improving alloy thermal stability in lead-acid and next-generation energy storage. AMG aligns its antimony business with lithium and vanadium under a decarbonization strategy, focusing on low-CO2 materials. Its Technologies segment delivers specialized furnace engineering that reduces sulfur dioxide emissions by 25–30%, reinforcing AMG’s positioning as a sustainability-driven critical materials supplier.

Global price leadership and ultrafine ATO scale at Hsikwangshan Twinkling Star Co. Ltd.

Hsikwangshan Twinkling Star, often called the “Antimony King,” is the world’s largest antimony trioxide producer and a central force in global ATO price formation. Based in Hunan Province’s Antimony Capital, the company controls the world’s largest stibnite reserves, ensuring unmatched supply security. It secured priority placement on China’s 2026–2027 MOFCOM export list, preserving global market access under stricter mineral quotas. Strategic investments in AI-driven ore sorting upgrade stibnite quality in real time, cutting waste by 12–15%. Its extensive ATO portfolio spans standard 99.5% grades for plastics to ultrafine products for electronics and military-grade flame-retardant textiles.

Nanoscale antimony trioxide precision engineered by Nihon Seiko Co., Ltd.

Nihon Seiko specializes in high-purity and nano-sized antimony trioxide for semiconductor materials, coatings, and advanced polymers. During 2025–2026, it scaled its PATOX-U grade featuring ~20 nm particle size, delivering high catalytic activity with minimal separation for electronics and specialty paints. Its PATOX-MZ and CZ lines use precision classification to eliminate coarse particles, essential for fine-structure electronic components. The company reported trailing twelve-month revenue of approximately USD 235 million in late 2025, driven by PET polymerization catalyst growth. With strict Tokyo-based quality inspection and OEM-certified PATOX-MK production, Nihon Seiko sets the benchmark for consistency in high-end ATO markets.

Solar glass and sodium antimonate integration advanced by Yunnan Muli Antimony Industry Co., Ltd.

Yunnan Muli represents China’s next-generation ATO producers, strategically aligned with photovoltaic glass and renewable energy supply chains. The company is pivoting toward sodium antimonate production, a critical clarifier that enhances light transmission in PV glass, supporting a solar sector that installed over 270 GW of capacity in 2025. Under China’s late-2025 “anti-involution” policies, Yunnan Muli consolidated smelting operations and reduced toxic by-products by 15–20% using bio-leaching. Deep integration within Yunnan’s industrial ecosystem enables direct supply to leading solar panel manufacturers. Despite price volatility, the company maintains resilience through balanced exposure to automotive, construction, and solar end markets.

China Antimony Trioxide Market: Export Centralization and Strategic Mineral Reclassification

China has reinforced its dominance over the antimony trioxide supply chain through direct state control rather than volume expansion. Effective January 1, 2026, the government implemented a two-year export qualification review system, limiting exports to just 11 state-approved entities, including Yunnan United Antimony and the trading arm of Twinkling Star. This policy sharply centralizes global antimony trioxide flows for the 2026–2027 cycle and increases pricing and supply visibility control for Chinese authorities.

This tightening aligns with China’s late-2025 decision to elevate antimony to the same strategic classification as rare earth elements. Export permits and quality inspection certificates have been reinstated to prevent leakage of high-purity antimony trioxide required for domestic AI semiconductor, EV battery, and electronics applications. At the production level, environmental enforcement is reshaping industry structure. In Hunan province, the world’s largest antimony hub, mid-2025 “Blue Sky” audits forced smaller refiners to consolidate into state-monitored, environmentally compliant operators. Concurrently, Jiangsu-based chemical clusters accelerated adoption of antimony-bromine synergist systems in recycled polymers, improving flame-retardant carbon char formation for EV battery enclosures.

United States Antimony Trioxide Market: Defense Security and Domestic Resource Rebuilding

The United States is repositioning antimony trioxide as a defense-critical material after decades of import reliance. A major inflection point came in October 2025, when Perpetua Resources broke ground on the Stibnite Gold Project in Idaho following a final Record of Decision. This site contains the only known domestic antimony reserve in the U.S., estimated at 148 million pounds, and is explicitly prioritized under federal supply chain transparency and national security frameworks.

Beyond mining, federal funding is accelerating midstream recovery and processing. In November 2025, the U.S. Department of Energy announced $355 million in funding opportunities aimed at recovering critical minerals such as antimony from coal waste and industrial byproducts. Military-grade demand is also shaping downstream investment. Perpetua issued an RFP in late 2025 to identify domestic partners, including Clarios and Trafigura, to refine antimony trisulfide for ammunition and armor. Parallel research funded by the Office of Critical Minerals is scaling the use of antimony trioxide in liquid metal batteries, targeting long-duration grid storage lifespans of up to 20 years.

Belgium Antimony Trioxide Market: Recycling-Centric Supply Security and Occupational Compliance

Belgium has emerged as Europe’s most reliable non-Chinese source of antimony trioxide through advanced recycling rather than mining. Campine NV reported a 35% year-on-year increase in global antimony trioxide sales volumes in 2025, driven by its proprietary recycling technology that converts battery scrap into high-purity trioxide. This closed-loop model insulates Campine from primary antimony price volatility and aligns closely with EU circular economy objectives.

Financial performance underscores the strategic value of this approach. Campine forecasted first-semester 2025 revenues of €380 million, more than double its 2024 performance, as overseas buyers sought alternatives to increasingly restricted Chinese supply. Product innovation has also been targeted at regulatory pressure points. In late 2025, Campine launched low-dusting antimony trioxide masterbatches designed to help European plastics and textiles manufacturers comply with tightened occupational exposure limits, reducing handling risks without compromising flame-retardant performance.

Vietnam Antimony Trioxide Market: Midstream Expansion and Asia-Pacific Re-Export Positioning

Vietnam is positioning itself as a strategic midstream processor rather than a volume exporter. Under Decision 2634/QD-TTg, the government updated its 2025–2035 mineral roadmap, setting a proven antimony reserve target of 4,756 tons and prioritizing smelting and deep processing facilities in northern provinces. This policy signals a shift away from raw ore exports toward higher-value antimony trioxide production.

The country’s geographic advantage is enabling it to function as a re-export and processing hub for Asia-Pacific markets. In 2025, investment groups began establishing Shanghai–Hanoi logistics corridors to support the layout of high-purity smelting plants. This positioning allows Vietnam to capture value from regional antimony flows while offering downstream customers partial diversification away from direct Chinese sourcing.

Oman Antimony Trioxide Market: Clean Roasting and Defense-Oriented Non-Chinese Supply

Oman has rapidly emerged as a critical non-Chinese antimony trioxide supplier for Western defense and aerospace markets. Strategic & Precious Metals Processing, through its Oman Antimony Roaster, achieved a major milestone in 2025 by utilizing its full 20,000-tonne-per-annum capacity to deliver high-grade antimony trioxide to European and North American buyers.

Financial backing has reinforced this trajectory. In 2025, SPMP secured an additional $40 million debt facility from Bank Nizwa to further optimize its clean-roasting technology, with a specific focus on reducing sulfur dioxide emissions. This positions Oman as a compliance-ready, environmentally differentiated supplier at a time when ESG scrutiny is reshaping procurement decisions in aerospace, defense, and advanced materials.

Strategic Roles of Key Countries in the Antimony Trioxide Industry

Antimony Trioxide (ATO) Market County Level Snapshot

|

Country

|

Strategic Role

|

Core Differentiator

|

|

China

|

Global supply gatekeeper

|

Export qualification control and strategic mineral status

|

|

United States

|

Defense-driven reshoring

|

Domestic reserves and federal funding for recovery

|

|

Belgium

|

Recycling-based supplier

|

High-purity trioxide from battery scrap

|

|

Vietnam

|

Midstream processor

|

Smelting and re-export hub development

|

|

Oman

|

Non-Chinese defense supplier

|

Clean roasting and ESG-compliant production

|

Antimony Trioxide (ATO) Market Report Scope

Antimony Trioxide market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Grade (Standard Grade, High Purity Grade, Ultra Fine Grade), By Function (Flame Retardant Synergist, Polymerization Catalyst, Fining and Degassing Agent, Opacifier), By End Use Industry (Electrical and Electronics, Automotive, Textiles, Glass and Ceramics, Chemicals), By Form (Powder, Masterbatches, Aqueous Dispersions)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hunan Gold Corporation, Campine NV, Yunnan United Antimony, Perpetua Resources Corp, AMG Critical Materials, Huachang Antimony, Hsikwangshan Twinkling Star, Strategic and Precious Metals Processing, Nihon Seiko Co Ltd, Gredmann Group, Suzuhiro Chemical, Young Poong Corp, US Antimony Corporation, Yiyang Huachang Antimony, Sanyuan Antimony

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antimony Trioxide Market Segmentation

By Grade

- Standard Grade

- High Purity Grade

- Ultra Fine Grade

By Function

- Flame Retardant Synergist

- Polymerization Catalyst

- Fining and Degassing Agent

- Opacifier

By End Use Industry

- Electrical and Electronics

- Automotive

- Textiles

- Glass and Ceramics

- Chemicals

By Form

- Powder

- Masterbatches

- Aqueous Dispersions

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Antimony Trioxide Industry

- Hunan Gold Corporation

- Campine NV

- Yunnan United Antimony

- Perpetua Resources Corp

- AMG Critical Materials

- Huachang Antimony

- Hsikwangshan Twinkling Star

- Strategic and Precious Metals Processing

- Nihon Seiko Co Ltd

- Gredmann Group

- Suzuhiro Chemical

- Young Poong Corp

- US Antimony Corporation

- Yiyang Huachang Antimony

- Sanyuan Antimony

*- List not Exhaustive